Metro AG – Update & Playing the Devil’s Advocate

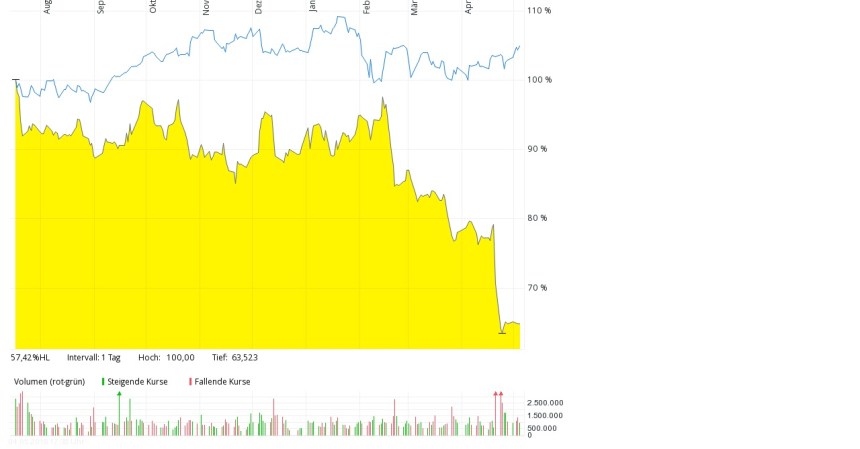

Metro, the spin-off stock I bought last year, doesn’t look very good at the moment. The stock priced tanked significantly over the last weeks and the stock is now a proud member of “V&O Flop 10“:

When a stock price moves like this, the fist thought is always: I need to do something, either to sell, or more often, to buy more. This was for instance one of the mistakes I made with Silver Chef, where I Increased my position at least temporary.

What often happened to me when I was holding a stock who dropped was, that I start looking at what happened and looked for reasons to keep or even increase the decision. I looked for more positive information which then would support my initial position. This clearly is the “Confirmation Bias” working in overdrive.

So in the Metro Case I try it differently: I try to look at anything that is not good. I try to play my own “Devil’s Advocate”.

What happened exactly ?

In February during the release of their Q1 numbers Metro management said the following:

FY guidance

• 9% growth (at constant currency) of EBITDA excluding real estate gains in line with FY guidance of c. 10% growth

Then, 2 weeks ago, they came with this “shocker” in form of a profit warning:

At first, this doesn’t read so bad. Instead of an EBITDA growth of 10%, they only expect flat EBITDA because of Russia, which to a certain extent might be understandable when looking at the latest developments between Russia and the rest of the world.

However why this exactly changed within 2 months is not explained. It also interesting that they seemed to have already fully included the potential savings from an ongoing labor conflict in Germany at Real, which to me seems to have been overly optimistic from the beginning.

Nevertheless, the drop of the stock price looks overblown in the beginning. The stock looks cheap and some of the issues should have been already in the stock price. So time to buy more ?

The Devil’ advocate

So this time I am trying to think of everything what I know so far which doesn’t look as good as I thought and why the stock might do even worse in the future:

- Profit warnings often come in series (Bilfinger, Vossloh etc.)

- Reporting of Metro is (still) relatively intransparent

- Metro has been one of the most shorted German companies –> Do the hedgies know more ?

- Metro is active in Russia & Turkey. These are countries where irregularities are rather common –> is the bad outlook in Russia maybe related to a fraud case ?

- Maybe Metro as a German company has been targeted by Russian/Turkey Governement ?

- They clearly failed to turn around Real and seem to have no clue what to do with it

- No insider buys despite drop in share price (CEO bought for 1 mn EUR shares in the beginning at~18 EUR /per share but nothing now

- Chairman of the board has been accused of Insider Trading late last year

- as other retailers, Metro has significant “off-balance” sheet Operating lease liabilities [EUR 5bn) which will come “on balance sheet” soon. Maybe investors are afraid that this will have negative implications

Russia:

To be honest, already the Q1 report clearly showed that there were issues in Russia. Like for like growth was -10%. With Russia being the main contributor to Metro’s profits (~350 mn EBITDA of a total 1.430 according to a Moscow Capital day presentation), this reduction in sales should lead to even larger reduction in Net profits over the full year.

Further indications of issues in Russia ist this information that a new Russia boss has just been appointed this week.

Experience shows that there is a high probability that a new boss at an already troubled unit might detect further problems. So this is clearly an issue, however the ultimate question is: How much of this is reflected in the stock price and how relevant is it in the long run ?

Edit: In this German article it is mentioned that Russian retailers Magnit & Dixy seem to enter Metro’s wholesale market. More competition is clearly not good for margins.

So what to do now ?

For me, it is currently too early to do something. It is not clear to me if the stock price has overreacted or if more trouble is coming along especially from Russia.

Selling now would be clearly an uninformed decision as well as buying more. The next step will be the release of the 6M report next week. I think I will then still wait and see how Russia develops. If, for instance there would be a further profit warning because of Russia, then this would be a clear sell signal.

Looking back, I clearly overweighted the stock compared to the amount of research I have done into this.

Metro stock moves very weirdly… Quite nonsense. Interestingly yesterday Germany sold a big stake on Pfandbriefbank, bringing the price down (or div.yield above 8%!). Might considering entering it…

Insider buying: https://www.metroag.de/investoren

Koch bought again.

The last numbers that came out tuesday were not bad, I was a bit surprised by the low free cash-flow.

Free cash flow is seasonal. It only makes sense to look at rolling 12 months numbers. On a 6 month basis, the lower FCF is explained mostly by the lower profit.

Koch buys Metro stocks worth 1M€ (yet again!):

http://www.dgap.de/dgap/News/directors_dealings/kauf-koch-olaf/?newsID=1073621

Two more points for the list of possible explanations:

# Stock is so heavily shorted as Hedge Fonds anticipate/possibly even know they get a chance to buy back cheaply when Ceconomy firesells their 9% stake in Metro at the next opportunity, as we all know Ceconomy is not holding for the long run

# Whole Foods Market was one of the heaviest shorted US grocery stocks before Amazon made the offer… If Amazon would be looking to expand their offline strategy to Europe, it would be hard for me to imagine a much better fitting acquisition target than Metro.

By the way, as long as Metro Russias sales and profits in € are decreasing in line with the rubles exchange rates, I am not extremely worried about my investment. Once the political tensions ease again, things should turn ok – political stock markets come and go…

Things back to normal when political frictions ease…

Do you anyhow anticipate Putin withdrawing from Crimea any soon?

…

Putin won’t withdraw from Crimea anytime soon. In fact, he can’t do that without losing his face.

Frankly I don’t think we need Putins withdrawl from Crimea to see the EUR/RUB going back below 60, especially with rising oil prices.

Then you should say ‘once the eur/rub goes below 60 again’… rather than once political tensions ease… I don’t think political tensions will ease, even less considering the Trump factor ! x-)

On the bright side your “in-depth” research in the travel sector is slowly paying off with EXPE. Did you have a look at CTRP or is “negative China bias” (besides relatively high valuation) a good reason not to update the travel series? 🙂

Would you buy Metro now if you didn’t hold the stock already? After admitting you basically don’t know what’s doing on?

I think that’s a more rational approach than the regret aversion (another bias) do-nothing.

Regret aversion is one of my biggest challenges as well actually….

Good question. I think the stock would be on my watchlist.

In that case… well, you shouldn’t be in the stock from a rational point of view.

Only trying to help here, I also paid my tuition fees for this lesson myself 😉

Thanks

Well, it is always more easy to give advice after something has happened. At the outset it looked like special situation with a decent risk profile. No to doesn’t look as good as before but I am not ready to throw in the towel yet.

@Thijs…. that was exactly my point ! They seem to have no plan about how to manage the situation. To me, now they seem a fair company at a “?” price, rather than a wonderful company at a fair price.

@MMI. I do agree that this is a ‘special situation’. Basically because of the “?”… It is difficult to price all the elements at play.

Personally, I would not buy a stock that I cannot price. And for the same reason, one should not stay in it.

* ‘Regret aversion’ should be taken as subclass of FOMO !

Maybe one more comment on this: I don’t agree with the “strategy” taht one should only own stocks that one would buy (again) right now. Why ? For me it is a strategy that sounds easier in theory than in practice. Most of my most succesfull investments are investments that I wouldn’t have bought tha majority of the time I was holding them. Take TFF for instance: It became too expensive pretty quickly after I bought it. So I would have needed to sell it quite early but I didn’t in this case. I sold in myna other cases when I thought the stock became too expensive which cost me a lot of money.

I guess this topic is actually worth a blog post 😉

To my modest opinion, holding on expensive price worked well because that was a wonderful company at a fair (even expensive) price… But staying in Metro seems like holding onto a fair company at a wonderful (“?”) price. Or maybe not so wonderful price.

That is the Question McMMI !

@memyselfandi007. Interested in how you would a approach the following situation. I understand the powers of long term compounding (being long in a great company), however, when a great company becomes pretty overpriced and you have for instance other potential good investment options, would you consider selling the great company stock ? Another option would be to temporarily sell it, and buy it again when it’s fairly valued, although markets can stay irrational for a long time…. I wouldn’t call this market timing, because you really base your actions on the intrinsic value of the company, but you look for ways to compound your money at the fastest pace possible.

I do not know in which tax regime you live, but for a German such a startegy would be not optimal as you woul dneed to pay cash taxes on the gains when you sell and have less capital to reinvest in another stock. So another stock will need to be a lot better to compensate for this. Anyway, I think the easier the better and when you own a “Really great” company, you should not tarde in and out in my opinion, as really good companies are almost always “too expensive”.

@memyselfandi007. I live in the Netherlands, we do not (yet) have a capital gain tax. I agree with you that really good companies are almost always “too expensive”.

A wise guy said “it’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price”. The latter seems to apply to Metro… Has management proven skill in navigating harsh environments / redress businesses? “Not for Real” ! …

I would really consider switching into something higher quality… If any can be found…

this is a special situation investment.

Am sure it’s not your case, but I’ve met lots of people who hide confirmation bias under the pretex of special situation…

Disciplined investors usually cut their losses and exit a investment thesis that has not played out fairly quickly.

(I know some who define exit triggers before they even enter a position.). Lots of red flags here for my liking but good luck for the guys sticking with it.

Ennismore bought Vossloh last month actually…

What about reduction in earnings from Turkey as the TRL has depreciated significantly? I’m in Moscow end of June (yes for the World Cup) so will have a look at the activity levels in Metro

Normall this should be off set by stronger nominal growth but this is something that worries me less than Russia.