Zur Rose AG (ISIN: CH0042615283) – Loss making failed IPO or long term growth opportunity ?

Disclaimer: This is not investment advice. DO YOU OWN RESEARCH !!!!

The company

Zur Rose AG is a Swiss company that specializes in selling / distributing pharmaceuticals. The core business is Swiss distribution business where they distribute pharmaceuticals to Doctors, as in some parts of Switzerland, Doctors canboth, prescribe and sell pills. In 2012, Zur Rose made a smart/lucky buy: For only 25 mn EUR, they bought German based online Pharmacy Doc Morris from Celesio, a German Pharmaceuticals wholeseller that got later acquired by McKesson (I owned the stock as special situation)

Zur Rose officially IPOed in July 2017 for 140 Swiss Franks. The company acquired subsequently more online/mail order pharmacies, becoming the dominant player in the German market. According to their 2018 release, they now have 31% market share in the German online/mail order market.

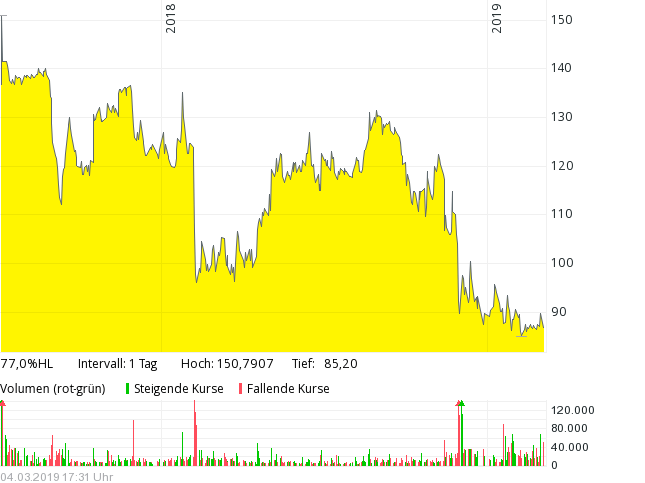

Ckearly, for IPO investors, the initial price now seems much too high and one could even call it a “failed IPO” to a certain extent.

The stock chart clearly doesn’t look nice:

The German online pharmacy market

There are different sources, but all agree that the online pharmacy market in Germany will grow significantly over the coming years.

Currently around 13% of OTC pharmaceuticals are sold online, including prescriptions, the market shares is around 5% (only). So there is a lot of room to grow, most studies estimate around 10-15% growth per annum for the next 5 years or so.

However, the regulatory environment in Germany is difficult. Traditional pharmacies have a super strong political lobby and try everything to stop the (unavoidable) Trend. Lawsuits are raised on an ongoing basis (here for example).

The current regulation is messy, for instance Non-German online pharmacies can give discounts (DocMorris is Dutch), whereas German cannot. The German pharmacy lobby at the moment lobbies for banning online distribution of prescription medicine. (in Germany). However as DocMorris is a Dutch company, no one can prevent Germans from ordering in the Netherlands. In my opinion this is also one of the underestimated benefits of the EU which makes those local monopolies a lot harder to sustain.

However in my opinion, it is unavoidable that the online share will increase significantly going forward. Especially for people who need the same pills on a regular basis, online is a huge advantage. Another driver will be that the German Government is now pushing telemedicine as well as digital prescriptions. The current German health minister is rather innovation friendly, but personnel change in the German Government is always a risk.

At the moment, prescriptions need to be physically obtained at the doctor and doctors are not allowed to write prescriptions based on tele medicine consultation only. Currently it is planned for 2021 that both, tele medicine prescriptions and electronic prescriptions will be implemented and this could in my opinion could even turbo charge growth.

As always with regulatory change, this could take longer as currently expected and will not be a smooth ride.

Competitor Shop Apotheke

Dutch company Shop Apotheke is the main competitor in Germany. They also have been acquiring competitors. In 2018, Shop Apotheke estimated around 570 mn EUR in sales whereas DocMorris was slightly ahead with 580 mn EUR in sales /+34% growth).

I think Zur Rose has one big advantage compared to Shop Apotheke: On their Swiss home market they have a very good testing ground in a more advanced health system. For instance they are trying to put pharmacy branches into Supermarkets or they provide the Software for Germany’s first experiments with electronic prescriptions in Hamburg.

So compared to ShopApotheke, I think Zur Rose has more options to play a larger role in the future in Healthcare than Shop Apotheke.

ShopApotheke is clearly a serious competitor but besides them there is little else. Yes, there are some people who try to compete via Amazon market place but to be honest, I don’t fear this so much at the moment as Amazon has thoroughly screwed up their search with “sponsored articles”. I also think that Amazon will not enter this market directly on their own in the near future. They will do something in healthcare but I am very sure that they will not try this in Germany on their own. Plus, the profit pool of the whole business in my opinion is much too low to justify a huge effort for Amazon, especially as their existing logistics cannot be used for pharmaceuticals.

I could actually imagine that they at some point in time try to acquire either Zur Rose or Shopapotheke similar to their PillPack acquisition in the US.

Other observations

Not everything is great at Zur Rose. The company shows a loss for 2018 and even the established Swiss Business was only slightly profitable in 2018. However I do not have a problem with this especially as the unit economics look quite good for DocMorris and I am sure that once the dust settles, that they can achieve profitability. There is clearly the risk that the integration of the acquisitions takes longer than expected.

Another negative aspect is the, to put it mildly, suboptimal execution of their capital raise a few months ago. For instance, the largest shareholder, the Frey family did not participate due to a “bank transmission error”.

Just yesterday it was announced, that 2 members of the “Verwaltungsrat”, among them the representative of the Frey family, resigned. It seems that they are not happy about the recent pace of acquisitions.

Management / Shareholders

I haven’t done a deep analysis but what I have read from the CEO for instance this interview makes a lot of sense. Management seems to own 5% of the company which is Ok. Overall I would judge management to be a slight positive despite the issues around the capital increase. There are clearly some issues with the major shareholder as mentioned above.

Valuation

Zur Rose communicated that they target an EBITDA MArgin of 5-6% in the year 2022. For next year they expect sales of 1.6 bn CHF and 10% organic growth in the years thereafter.

Putting this together, management expects an EBITDA between 85 mn and 106 mn CHF for 2022 which, using a few assumption would translate into a target EPS range of 7,80 CHF to 9,70 CHF.

A reasonable P/E for a company growing by 10% p.a. in my opinion is around 15-20 times earnings, resulting in a 4 year price target between 117 to 197 CHF. This again translates into a 4 year IRR range of 7,9% p.a. to 22.6% with a midpoint of around 15,5% (based on a share price of CHF 87)

Summary:

There are clearly many risks involved with this Stock. They need to proof that the German market will be profitable, there is significant regulatory risk, potential issues with integrating the acquisitions and there is always the threat of Amazon. Plus, the 15% shareholder might decide to sell shares at any time.

On the other hand, in my opinion the company is in a “sweet spot” regarding long-term growth opportunities. The german market has a good chance to grow double-digit organically and there might be additional opportunities in Europe.

Therefore I have established a 3% position at an average price of CHF 87,5 per share. For me this is part of my longer term “growth bucket”. This is clearly not a short term play but at least a 3-4 year “bet” on the health market especially in Germany. In the short term there could be clearly downside volatility.

I plan to add more shares if the integration of the acquisitions goes according to plan.

I have sold my remainder of the Zur Rose position at 127 CHF/per share. Main reason: unclear outlook,

Very bullish update from Zur Rose:

https://zurrosegroup.com/websites/zurrosegroup/German/201010/medienmitteilung.html?newsID=2058561&date=2021-01-21%2007%3A00%3A07

Zur Rose continues to move into “Digital Health”. This time together with Novo Nordisk:

https://www.deraktionaer.de/artikel/pharma-biotech/zur-rose-mit-top-news-zusammenarbeit-mit-novo-nordisk-die-hintergruende-20223483.html

I must say that I am positively surprised so far, however one needs to see what is storytelling and what the actual impact will be.

Zur Rose (together with IBM) seems to have won the “Beauty contest” for implementing the German solution for digital prescriptios:

https://www.pharmazeutische-zeitung.de/ibm-und-zur-rose-tochter-bauen-das-deutsche-e-rezept-system-121794/

I consider this to be VERY positive in the medium and long run.

Interesting in this context, though only concerning the US so far: Amazon starts selling prescription drugs, with two-day delivery for Prime members

https://www.vox.com/recode/2020/11/17/21570768/amazon-prescription-drugs-pharmacy-pillpack-medication

Thanks for the link. Following their Pillpack acquisition, this is not a total surprise. I think part of the “Bull Case” for Zur Rose would be that it could be an interesting target for any big player trying to enter Europe.

Solid Q3 sales update from Zur Rose:

https://www.zurrosegroup.com/websites/zurrosegroup/English/201010/press-releases.html?newsID=2038038&date=2020-10-21%2006%3A50%3A02

It looks like that they will come out above the initially projected 1.6 bn CHF sales in 2020. Germany is doing really well.

Interesting move from Zur Rose: They are taking over a German tele health startup called Teleclinic:

https://www.dgap.de/dgap/News/corporate/zur-rosegruppe-akquiriert-teleclinic-den-fuehrenden-telemedizinanbieter-deutschland/?newsID=1370891

Interesting move….

Sold 1/10th of the position today at 202 CHF. Exposure Management as the position became slightly too big compared to the risk.

Sold another 10% of the initial position at 220 CHF. Crazy how the stock moves currently.

Sold another 1/10 of the initial position yesterday at 288 CHF

Sold another 1/10 of the initial position at 297,50 CH

https://www.handelsblatt.com/politik/deutschland/verschreibungspflichtige-medikamente-spahn-will-auslaendischen-versandapotheken-rabatte-verbieten/24120680.html?ticket=ST-385856-5blSX0szlDxR3kGwCcMV-ap1

The great Gartner videos, here in a presentation in Munich…. Highly relevant for the Zur Rose…

the role of Amazon in online pharmacies.

Highly recommended !

Click to access 20190201ZurRoseGroupAG.pdf

Page 2: Time to change an 800 year old guilded system.

Page 4: Zur Rose Group: «Game Changer» in the CHF 146 bn medications market

e-commerce share:

Medications: ca. 2% (Zur Rose Group)

Apparel: ca. 15% (Zalando)

Media products ca. 40% (Amazon)

The winner takes it all!

This is an interesting situation, thanks for highlighting.

I noticed in Shop Apotheke’s latest presentation: “Due to recent changes in the competitive landscape, the Board is currently evaluating strategic options for 2019 focussing on best value for shareholders.”

It seems that current regulatory changes under Jens Spahn may evolve around the following three points (though nothing is final):

1. More fiscal support for physical apothecaries to render services to patients

2. Limit “bonuses/discounts” paid by online apothecaries to ~5 EUR per product

3. Further limit bonuses or take other measures once online apothecaries market shares reaches ~10%

Am I getting this right?

How do you see these developments? Does this allow Shop Apotheke / Zur Rose to re-enter the German market and send drugs to customers from within Germany’s borders?

Typical too “difficult basket”. Have you had a look at Rose´s RoiCs and RoAs? Good luck.

Many of the points appear here too. http://www.cash.ch/news/top-news/online-apotheke-zur-rose-walter-oberhaensli-macht-alles-richtig-1291278 …a bit of due diligence shows that the writer is not an economist but a historian… (full due diligence should chk how much predictions he got right, …hehe)

Interesting. My two cents: I almost bought a Pharmacy in Chur. Profitable business granted, but also granted was a big uncertainty on ‘HOW MUCH’ profitable. I passed, as risk was too high.

… Years ago a Pharmacy was a golden mine, now no longer…

My friends in Novartis/Roche complain systematically on the squeezed margins they face, vs high regulatory costs. Seems the industry is under pressure from all sides.

The big uncertainty in profit margin was due to the new online Pharma landscape, which is still undefined. Without a clear vision on market size, main players, swot’s, competition geography footprint etc, it was difficult to seize the risks for such enterprise… Good luck!

Pharmacy != Pharmacy industry

Novartis has a RoE that a pharmacy owner could only dream of.

Pharmacy and Pharma industry are parts of the same value chain. If pressure on profit margins is applied somewhere in that chain it is transmitted throughout (archimedes principle applied to economy).

The RoE of that particular Pharmacy was systematically above 20% (Novartis’ is below that)…. Which seems to confirm there are significant uncertainties and risks at stake.

I think there is another aspect about e-scripts that is very important. Not only will the adoption of e-script accelerate revenue growth (perhaps dramatically so), it will also reduce the need for price competition and bonuses to customers. Today, DocMorris and Shop Apotheke are giving away about 5-6% in gross margin from price discounting because they don’t have much of a choice. Because of the hassle of mailing physical scripts, customers have little incentive to move online without discounted prices. The adoption of e-scripts eliminates this problem, and the industry should (hopefully) stop highly discounting prescription drugs. Today, customers buy online primarily for speed and convenience and selection, not lower prices.

I also believe that Mr. Spahn’s desire to significantly reduce or perhaps even eliminate the bonuses would be very positive for DocMorris and Shop Apotheke in the long-run because their gross margins will instantly increase 3-6%. Not only would both companies be profitable overnight, but they would be unable to engage in price wars. Growth would probably slow in the short-term, but again, long-term it seems inevitable that there will be a lot of growth once e-scripts eliminate friction. Online prescriptions are only about 1% of the market whereas in places like the Netherlands they are 10%.

Both are very interesting companies. I am concerned by the recent resignations from the Frey’s at Zur Rose. The Frey’s are very good investors and this wasn’t a good sign. Nevertheless, the management of Zur Rose seem pretty good. The insider ownership at Shop Apotheke is much higher (with a lot of insider purchases in the last year) which is a good sign. Personally, I think these two companies should merge.

Thanks. I Think a merger though is unrealistic due to market share.

I have spoken to both companies and some industry people and I believe it is possible because combined, both companies are still just a tiny fraction of the overall market. But yes, with how protective Germany is of the pharmacists union, I could see it being blocked anyway.

Do you think a site like medizinfuchs.de could be a problem for the profitability of the subscription free segment? You can put all medicine you need in a basket and then the site shows the cheapest online pharmacy including shipping or even whether it is cheaper to split the order.

I agree for repeat customers with a chronic illness, who do not need any help, online is the best channel. Although some medicines may require cooling and the logistics of the conventional pharmacies may still be better for such special cases.

Interesting would be also how much of the 10% growth is volume and how much price inflation. After all online is better suited for more expensive stuff due to logistics cost. Another risk here is the „mindestlohn“. DPD and Hermes business model may not be sustainable with „independent sub-contractors“ below minimum wage compared to real employees.

Time will tell. There will always be people who will go the extra mile for saving a few Euros, but many people stick with the existing service if the price is “ok”.

Interesting! You mentioned the unit economics are good. Can you outline them (roughly)? Thanks