Position review: Van Lanschot (SELL) plus some thoughts on Unbundling /Rebundling in Banking

Background:

Having this blog is nice because I can look back at what my original ssumptions were. I bought Van Lanschot in 2013, almost 5 1/2 years ago.

This was how I “valued” Van Lanschot back then:

Valuation:

A simple, “Berkowitz style” valuation would be: Book value

With ~0.51 times book value, Van Lanschot is one of the cheapest banks in Europe. Even Greek Banks like Piraeus Bank trade higher. The current valuation is on a level with „quality banks“ like Unicredit, Espirito Santo and Credito Bergamesco.

Interestingly, the P/B multiple for listed Private banks is a lot higher. Swiss competitors Julius Baer, EFG and Banq Privee de Rothschild for instance trade on multiples between 1.1-2.0 times book, a clear premium to „normal“ banks.

So with a “normal” result, one could argue for a valuation somewhere at 1.5 x book value. Clearly, this will be a long way, one should not expect exploding profits in the next quarters. But in a time period of 3-5 years, I could imagine that the stock can triple if the turn-around is succesful. Also, when people finally realize that not every Dutch homeowner will go broke, there might be a re-rating of Dutch financial stocks in general. But this might also take time.

It would be easy to come up with a much more complicated valuation method, but I like to keep it simple. If there are no big holes in the balance sheet and costs are kept under control, equity is at a safe level, then book value should be achievable for any bank.

So from my original purchase price of 16,50 EUR per share, Van Lanschot has clearly not tripled. Including dividends, the stock returned around 65% over 5,5 years. This is pretty much in line with the V&O portfolio in this time so no disappointment here. Interestingly, dividends and capital repayments contributed more than half of the performance.

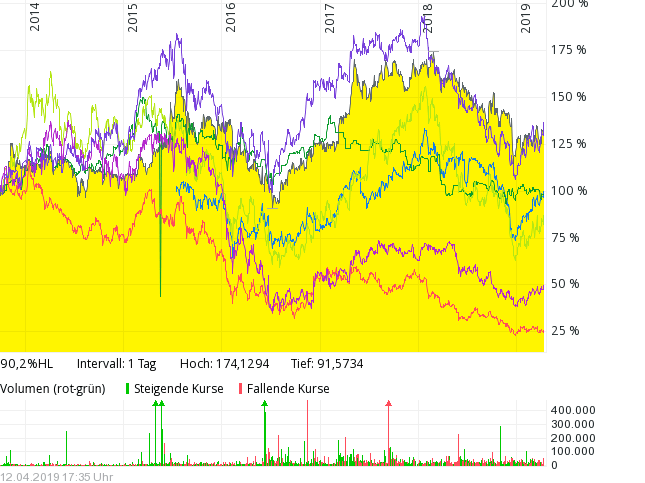

Comparing Van Lanschot to other banking stock we can look at this busy chart:

The solid yellow space is Van Lanschot plotted against ING, Commerzbank, Pfandbriefbank, Handelsbanken, Unicredit and Deutsche Bank. The only competitor who performed in line was ING, all the others did significantly worse, especially the big German banks. SO at least I selected a relative outerperformer…..

Looking at the latest annual report shows, that 2018 was not the best year. Clearly results have improved significantly since I bought the shares, but overall profitablity has not returned to pre-crisis levels.

Lets compare some numbers from 2012 with 2018:

Net interest income 2012: 235,7 (interest margin 1.29%, loans 13,5 bn EUR)

Net interest income 2018: 175.4 (interest margin 1.15%, loans 8.6 bn EUR)

Net commission income 2012: 216.8 mn

Net commission income 2018: 293.7 mn

Staff cost 2012: 218.5 mn

Staff cost 2018: 263.7 mn

Opex 2012: 408.7 mn

Opex 2018: 440.2 mn

Gross result 2012: 115.8 mn

Gross result 2018: 102.8 mn

Equity 2012: 1.352 (Intangibles 173 mn)

Equity 2018: 1.286 (Intangibles 183 mn)

In a nutshell, the operating result of Van Lanschot in 2018 is lower than 2012. Within Opex, staff cost now have a greater share but most notably, interest income shrank due to a smaller loan book which has been compensated by an increase in commissions. However the increase in OPEX has been eating up any progress here.

Clearly commission income is “higher quality” income than net interest, which explains the slightly better valuation.

With a current market cap of 900 mn, Van Lanschot still only trades at ~70% of book value (or 82% of tangible book value) but with the low return on equity that is maybe justified. Julius Baer for instance trades at 1.67x book value but generates around 13% ROE compared to the 5.8% of Van Lanschot.

Earnings quality

Van Lanschot’s earning quality is also not so good For financial institutions, where equity drives the amount of business possible, Comprehensive Income is the most important measure.

In Van Lanschot’s case, the bridge from Net income to comprehensive income looks as follows:

Net result: 80.3 mn EUR

– minorities -5.7 mn

– other compr. income -19.8 mn

Compr. Income 54.8 mn EUR

So almost a third of the result “disappears” somewhere along the minority / CI section. The remaining ~55 mn represents ~4% of ROE which of course is far too low.

Disruption – Unbundling & Rebundling in banking

Some years ago I thought that banking as such would be a durable business model. Everyone needs an account/ card and as the business includes actually “printing money”, this should be a good one. However the last few years have shown that “disruption” in banking is actually happening. A few examples where either new companies or some competitors have been taking away business from the “Traditional” players.

A bank like Van Lanschot is bundling a lot of financial services: Loans, Asset management, payments, wealth managment, merchant banking, stock trading, M&A advice etc. However there is a significant amount of “Unbundling” going on, just to name a few of the developments:

- payments: Banks basically missed this completely. Companies like Paypal, Ayden, Stripe etc. show the banks how to do this in the internet age

- Asset management: Index funds, robo advisors etc. the first index funds have been launchen with negative TERs. There is only one way for AM fees: down

- loans: P2P, loan platforms etc. targeting the most valuable clients of traditional banks (SME)

- Stock trading: free trading like Robin Hood, super cheap and efficient trading for pros via Interactive Brokers etc.

- Multi Family offices are taking clients in Wealth Management

- Many new boutique M&A advisory firms have opened up and snatching lucrative M&A advisory mandates

- Custody (Apex, FNZ, Blockchain (!!!)

- in retail, players like N26, Revolut and Monzo are adding customers in the millions

This is in my opinion very similar to the Bundling/Unbundling in Cable Television vs. Netflix as brilliantly laid out by Ben Thompson here.

Especially the aggressive retail players like Revolut and N26 are trying to rebundle retail services in a more convenient way. Both started with very narrow services (FX for Revolut, current account & credit card for N26) and are now adding more services however in a mobile first and very customer friendly way. Other rebundling occurs in online based SME banks like Tide or players like Square. Plus you have more and more of the big Tech companies like Amazon, Apple and Co. entering the space via payments, cards etc.

These developments clearly do not only apply to Van Lanschot but also to all other traditional banks. Some might be able to adjust but in my opinion a lot will get into problems. In Van Lanschot’s case they tried to adjust by launching “EVI” but looking at their numbers (almost no customer growth) it clearly looks more like a typical “let’s build an app” approach than a real attempt to transform the business model.

Of course I also need to revisit Handelsbanken. Handelsbanken is a “special case” but there is clearly a risk that they will miss out as well on these structural changes.

Summary:

In general, the old “Banking bundle” is clearly under attack from many sides. Maybe there is a “last puff” in banking stocks when the next merger wave starts, but for me at least for Van Lanschot I am not convinced if going forward they will be able to generate value on top of the dividend they are paying.

Therefore I sell my Van Lanschot stake (2,0% of the portfolio) after 5,5 years at 21,50 EUR/share.

Click to access investor-presentation-march-2019-van-lanschot-kempen.pdf

I would be in ibkr, or tiger broker…

Interesting views. It would be even more interesting to know what do you plan to make with the cash. To me markets now seem quite heated, and valuation very high… I wonder if sustainable (?). Maybe it would be smart to just #sellinmayandrunaway ?

Or just buy some put options…

I have already invested the proceeds. But you will have to wait until early next week to find out where…. 😉

Waiting will be my ‘Easter penitence’…

Interesting post as usual. Question on process.

It seems you did some analysis, bought the stock. Then some time elapsed during which you read a lot of stuff on a lot of other investments. And then at some relatively arbitrary point in time (about 5.5 years) you decided to take another look and sell. This does doesn’t strike me as optimal. Wouldn’t it be better to keep an updated list of performance of all your portfolio and then compare every time you read about a new stock to the worst stock in the portfolio and make a switch / no-switch decision? Otherwise what are you going to do with the Van Lanschot cash now?

#pogonific,

thank you for the comment. Yes it may sound a little bit arbitrary and to a certain extent it is. As i mentioned in the blog sveral times, for certain (personally very positive) reasons I have a lot less time to research stocks and write on the blog. I have also mentioned several times that I intent to lengthen my holding periods.

My stated time horizon for investemnts is in general 3-5 years. So reviewing a stock after 5,5 years in my opinion is OK.

For the cash part: Van Lanschot was only 2% of the portfolio.

Interesting views. It would be even more interesting to know what do you plan to make with the cash. To me markets now seem quite heated, and valuation very high… I wonder if sustainable (?). Maybe it would be smart to just #sellinmayandrunaway ?

Or just buy some put options…

Sounds fair.

I suppose five years it at least a good time to reevaluate if your original investment thesis ist still valid.

I am looking forward reading your analysis about Handelsbanken.

I really like their outsider-behaviour and I think they made a very good job in UK, but the digital time may test their business model as well.

by the way, I did quite like this interview with Bouvin from handelsbanken: https://internationalbanker.com/banking/interview-with-mr-anders-bouvin-president-and-group-ceo-of-handelsbanken/

Great interview. Thank you Roger