Online Travel Updates (Expedia, Booking, Tripadvisor, Trivago & AirBNB / Google)

Expedia

I invested into Expedia in February 2018 after the stock had become cheap enough. The idea was that a stock in a secular growth sector (online travel) should do well in the long run. After pretty decent fulll year 2018 numbers, with double digit increases in both, top and bottom, line, the first quarter 2019 showed a clear slowdown. Topline growth slowed to ~4%. Excluding Trivago which is still shrinking, topline sales would have grown +6%. Underlying profitability has improved although the first quarter is always the weakest one.

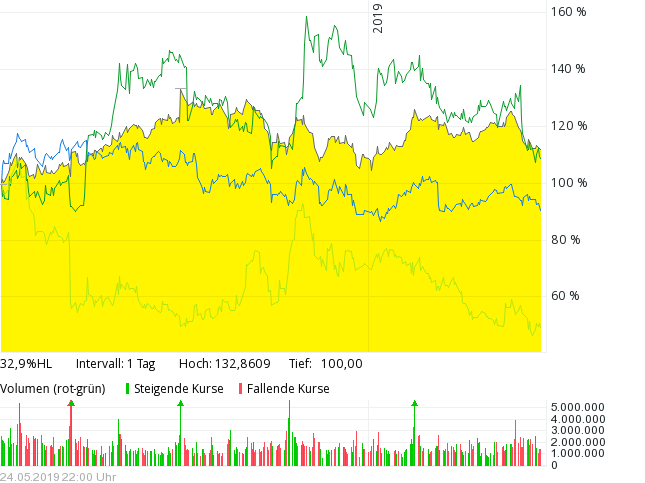

What I found interesting is the fact that Expedia performed better than Booking com. Here is a stock price comparison (including Tripadvisor and Trivago):

Booking has underperfomed Expedia by ~ -20% whereas Tripadvisor performed in line and Trivago further tanked.

SKift as always has pretty good coverage. Expedia currently has some issues with slowing growth in their rental business. On the plus side, their stake in Indonesian Traveloka has increased significantly in value. In their 2017 funding round, Expedia bought 30% for USD 350mn, implying a company valuation of roughly 1 bn USD. Recently, Traveloka raised money at a 4 bn valuation, indicating a value of more than 1 bn uSD for the stake held by Expedia.

Booking.com is another story. Their top line revenue in Q1 2019 dropped by -3%, and net income was only better because it has been juiced up by some financial gains. My guess is that the drop in volume has to do with their reduction in performance marketing expenses which droped from 1.106 mn USD to 1.030 mn., whereas Expedia has still slightly increased their marketing budget. In the Q1 call, the Booking CEO seemed to have talked a lot about acquisitions which for me is not a great sign.

Interestingly I never wrote about Booking during my travel series as I found the company to difficult to value. Great business and great moat on one hand but also quite controversial and expensive on the other side. However if the stock gets cheaper I think I will have another look at them.

Tripadvisor

Tripadvisor’s Top line is still shrinking in Q1 2019 and is now on the level of Q1 2017. Profit went up but mainly due to a reduction in marketing spend which is clearly not a long term sustainable strategy. However Tripadvisor remains a “story stock” and commands a pretty significant valuation for a stagnating company.

Trivago

Trivago is celebrating becoming profitable but achieved this by cutting advertising significantly and shrinking the topline by -20% YoY in Q1 2019. Again, this is not sustainable and it remains to be seen if their “aggregator on top of other aggregaor” business model is sustainable.

AirBnB

AirBnB, the private rental “unicorn” is on its way to a 2019 IPO. They seem to be “EBITDA profitable” already, Before their IPO they have announced some aggressive moves like slashing fees and started listing hotels alongside its core rental product. The fee structure is clearly attractive for hotels and might hurt Booking & Expedia in the lon term:

Perhaps Airbnb’s most attractive feature, at least for hotels that want to advertise on the platform, is the fact that Airbnb’s commission fee structure is significantly less costly than that of its online travel competitors, Booking and Expedia.

Whereas Booking and Expedia might charge hotels a commission fee that’s as high as 25 percent, Airbnb charges all of its hosts — hotels included — a commission fee that ranges from 3 to 5 percent, and it also collects a “guest fee” from the guest. It’s a similar model employed by Trip Advisor and HomeAway, for example. Chesky, however has publicly noted that he sees Expedia and Booking as his primary online travel competitors.

Airbnb also doesn’t require a contract from hotels like most of the online travel agencies do.

It is pretty clear that AirBnB will become a “full stack” competitor to Expedia and Booking. However, once they are a public company, it needs to be seen if and how they can continue to operate at this profitbility level. Maybe this is one of the reasons why they more recently seemed to have cooled down a little bit on the 2019 IPO target.

AirBnB clearly is an interesting comapny as this open Letter from their CEO shows, but if that justifies a valuation of 35 bn needs to be seen. A ~ 10x revenue multiple for a travel company is quite hefty, compared to 1.5x at Expedia and 5x at Booking.

Google Travel

Just a few days ago, Google announced that they now have a new combined tool called Google Travel. At first sight, it looks like a pretty serious competior to the likes of Trivago and Tripadvisor but so far they leave the booking part to Exepdia & Co. However in the long run, Google Travel will become a compeitor to Expedia and Co. as they themselves acknowledge:

But today, with launch of flights, hotels, packages and trip-planning features on desktop, as well as making them all available on mobile, Google has taken a large step toward becoming an all-encompassing travel planning and booking destination.

Yes, Google is letting its travel advertising partners, from airlines to hotels and online travel agencies, keep doing most of the booking, but it is a challenge to them, as well.

Why go to Expedia.com to make your travel plans, for example, when travelers can do it all in the Google search engine, along with everything else they use Google for all day long.

It’s no wonder then that Mark Okerstrom, the CEO of Expedia Group, which spent $1.53 billion on sales and marketing in the first quarter alone, said last year that Google is Expedia’s chief competitor. The lion’s share of that sales and marketing spend undoubtedly went into Google’s coffers

I am not 100% sure, but I think this is maybe a defensive move from Google. The big online travel companies are still the biggest clients of Google but as outlined above they are cutting online budgets and therefore Google needs to do something in order to increase revenues.

It still needs to be seen how well this would work. Google for instance also try to go into insurance comparison but failed to achieve any results.

Summary:

Although the travel space is clearly one of the earliest sectors that went digital, the market is still very dynamic and competitive. So far, Expedia is doing well and seems to be one of the winners, so I will keep the stock for the time being.

However one needs to clearly pay attention to Google and AirBnB. In my opinion, the typical aggregator models like Trivaga and Tripadvisor are clearly doomed and will be hurt most especially by the new Google offerings.

https://www.google.com/amp/s/www.cnbc.com/amp/2019/11/07/expedia-and-tripadvisor-stocks-tank-after-poor-third-quarter-earnings.html

Freefaaaaaall

I sold my shares today at -100.15 USD. Although i knew about google’s effort, i underestimated the impact. This really could be a game changer for otas.

Edit: reinvested tue proceeds into Admiral and p. Hartmann.

Talking my book: A detailed Expedia wirte up at Value Investors Club from April:

https://www.valueinvestorsclub.com/idea/EXPEDIA_GROUP_INC/2332020226

Some of Booking’s metrics are much better than Expedia, for instance ROE Expedia is 10%; Booking 44%. Operating margin and net margin much higher. However, last 5 years Bookings has underperformed Expedia stock. Investors should look at the future. If I look at the bookings mobile app for instance; I don’t really see much new things. There were to comfortably and the competition is heating up in the space. Moreover, I think Europe will lag US and China significantly the next decade. I sold my shares in Booking this year.

Tripadvisor has the biggest potential on the mentioned companies. TRIP reduced markedly the hotel ad budget, as you mentioned, but they channel the cashflow into the experience and dining business, where they are number one and have a big growth potential ahead. This is completely underappreciated by the market. This is where the music will play with growth rates of 100%+. The hotel business plays the role of cash cow.

I see it differently. Everyone (and his grandmother) are going for the “Experience” business. I recently booked via AirBnB and their experience offers are damned good…..

On the startup side, Getyourguide has just received 500 mn USD (!!!) from Softbank for exactly this market.

At Tripadvisor, the growth rate for “experiences and dining” in Q1 was +29%. The profit in that segment indeed increased 500% but with a negative sign.

I remain very sceptical. As I said, Tripadvisor is a story stock. 2 years ago the story was booking, now it’s attractions. Let’s wait and see but for me Tripadvisor is not good value at this valuation.

Regarding Booking Holdings, I recommend reading the 10-Q or the call transcript in addition to the Skift website.

“Last year, Easter was on April 1st, and therefore, the majority of Easterrelated travel revenue was recorded in the first quarter. This year, with Easter on April 21st, Easter travel revenue will be recorded in Q2. Our Q1 non-GAAP revenue growth rate on a constant currency basis and adjusted for Easter timing was about 8%.”

8% is below their recent history but far from declining.

In terms of acquisitions, I judge them by what they do, not what they say. Over the last 3 years they spend less than $1bn on acquisitions, while generating $14bn in operating cash. I think they will continue that way, but similar to you, I would see a large purchase as rather negative. Let’s see what is in store.

Lastly, BKNG is one of the few companies that views stock-based compensation as real cost (which of course it is). Many companies (incl. Expedia) add them back in their “adjusted EBITDA” In Expedia’s case it is quite significant (around 25% of operating profit).

For more on Expedia’s accounting I suggest the following:

https://lt3000.blogspot.com/2018/02/expedia-and-dodgy-accounting.html

Thanks for the comment. A few points:

– the calendar effect should apply to all travel companies. So in relative terms Booking still doesn’t look good compared to the peers

– stock based compensation was around 200 mn in 2018 (and 50 mn in Q1), for Booking the number as such is ~50% higher at ~320 mn USD in 2018

– Booking seems to capitalize some of their Software development costs as well. I didn’t do a deep dive but this is from the 2018 annual report:

“Depreciation and amortization expenses consist of: (1) amortization of intangible assets with determinable lives; (2) depreciation of computer equipment; (3) depreciation of internally developed and purchased software; and (4) depreciation of leasehold improvements, furniture and fixtures and office equipment. Depreciation and amortization expenses increased during the year ended December 31, 2018, compared to the year ended December 31, 2017, primarily as a result of increases of $36 million in data center equipment depreciation expenses and $19 million of internally developed software”

– I think I commented on the linked blog post already. Yes, one needs to adjust for this but again one also needs to adjust for the “extra” assets like Traveloka etc.

Overall, even if you adjust Expedia’s earnings for stock based compensation and depreciations, it is still cheaper. And at least in Q1, growth seems to be better.

It will be interesting to see if and when Booking will ramp up ad spending again.

Thanks for engaging in a discussion. To your point, timing of peak travel events like Easter have a different impact depending on the business model. BKNG follows the agency model (mostly), recognizing revenue when people travel (at check-out to be precise). EXPE is strong in merchant, where revenue accrues when booking the travel (but not always). Some Q1 Easter booking? Yes. Easter traveling? No.

EXPE grew revenues 7% without specifying Easter impact. BKNG grew 8% incl. c2% Easter impact. So, I still disagree with you: Growth at Booking is not worse, it’s roughly on par with EXPE. But what does a single quarter mean?

Since you touched upon valuation: On Reported Profits, which do not exclude costs that appear real to me, valuation discount of EXPE flips to a premium. BKNG: 16x, EXPE: 24x

I am also curious if they will revert back to massive advertising spending. My hunch is: NO.

BookingH I liked, yet 200m of stock comp… (resp. 320m)… I find insane, unless that is accross all the company.

Thanks for the high quality discussion., this is unfortunately not always the case especially if I am not enthusaiatic about a particular stock.

Coming back to booking: What I find interesting is that if you strip out Merchant revenues at Booking, their core agency revenues dropped from 2.113 mn to 1.949 mn, a drop of around -8% in ACTUAL revenues. So it needs to be seen how large of an impact Easter really is. If they aim for double digit growth (which their stock price implies), Q2 should be a killer quarter fro agency revenues.

P/E is of course a very rough meassure and does not include extra assets. I haven’t looked at Booking very close, but if the price keeps dropping. it will become of course more interesting, especially if what you claim turns out to be true.

Thanks for the comments. I have recently invested in Booking and I think the explanation for the difference in share price and quarter performance is that Expedia is much more US focused and Booking Europe focused. Last 2 quarters Booking has commented on European macro being weak (Brexit among other things). Why I would recommend looking at Booking 1) they aggressively are buying back shares and just announced a new large buyback program. 2) they are quite successful in the alternative accommodation space (check latest call for comments), this puts pressure on margins in the short run. Stock hasn’t been moving for a while, whilst share count is coming down and operating income continues to grow

To be honest, a share buy back as such does not mean a lot. If they can’t grow their top line. This is still a growth sector, so not growing means significant loss of market share.

Agreed that share buyback does not mean a lot per se, but the growth is still there. Room nights book grew 10% in q1 (I think it is a better proxy for growth than revenues, partly because of FX). Rev growth was 16% constant currency over 2018. I think the current valuation, growth rate (declining, bur still there), cash comversion makes it interesting enough to take a look