Special situation update: Innogy, Osram, PNE AG, AGROB & Comdirect

Innogy Tendered Shares

A quick update on this “cheap option play”: To a small extent this has developed better than I intitially thought as I had mentioned in the comments. My initial expectation would have been a small loss. However, E.On now has increaesd the price for the tendered Innogy shares voluntarily to 37.59 EUR which, inclding the dividend of 1,40 will lead to a small profit (before taxes and cost) . However the ultimate upside, if there is a lawsuit, will be smaller as the E.On shares dropped to 9 EUR and the theoretical value of the tendered shares is now 4.371*9= 39,34 EUR.

Paladin so far did not comment on this, so let’s see how this develops. The tendered shares have stopped trading and the money should be paid pretty soon.

Osram

The Osram story got more interesting. To recap: After the initial bid of Bain & Carlyle for 35 EUR, I sold my stocks slightly above that level as the smaller Austrian company AMS AG came in with a (at that time weak) bid of 38,50 EUR. In the meantime a lot of open issues have been resolved. Now however, in a very interesting turn, Bain announced second bid, however this time with another PE partner, Advent. For timing reasons (?) they did not formally issue the bid. On the other hand, the old Bain offer and the AMS offer only run until October 1st and the AMS offer requires a 62,5% acceptance rate. AMS already has bought some shares in the open market. At the time of writing, Osram shares trade at 38,70 EUR, slightly above the AMS AG offer.

A very complicated but interesting situation with 3 bids at the same time. I’ll stay out of it but watch closely in order to learn as much as possible.

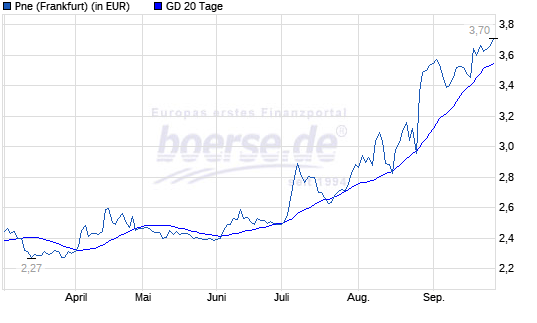

PNE AG

PNE AG is a small company building and owning wind parks. The company went through rough times but at the end of August, the company released the news that Morgan Stanley Infrastructure Partners has approached the company and that they are negotiating a potential take over in the range of 3,50 to 3,80 EUR per share, a premium of ~30-40% vs. the undisturbed price.

Back then I bought a tiny position to watch this as for a real special situation, this is too early for me.

In the meantime other bidders have joined the race: Macquarie and EQT. As my bungled Cars.com investment shows, even many more bidders cannot guarantee a deal, so for the time being a stay outside watching with my tiny position. Maybe there is a chance to earn a small (but more secure) spread when the real bids are issued.

AGROB

AGROB is a small Munich based real estate company that has been majority owned by Unicredit (Hypovereinsbank) for a long time. Quite surprising, two days ago PE Apollo offered a bid of 32 EUR for the common shares and 28 EUR for the Pref shares after having signed a deal at the same terms with Unicredit. Interestingly the shares already trade above the offer. Apollo will need to acquire more shares to be able to squeeze out minorities.

Especially the prefs could be interesting: As far as I know, for a squeeze out, Prefs are often treated by the courts similar to common shares, so the prefs could be an interesting play at this stage, although there is no clear time table on the squeeze out. Some experts that I know claim that the “fair” value of the stock is even higher than the 32 EUR per common share.

Comdirect

Commerzbank, the struggling number 2 in the private German banking makret, announced a few days ago that they want to fully integrate their listed subsidiary Comdirect, So far they held around 80%.

Now the official offer is out: 11,44 EUR per share, which is around 5% lower than the current share price and ~25 % higher than the undisturbed price. As in AGROB’s case, Commerzbank needs more than 90% in order to squeeze out minorities.

Hallo mmi, ich habe mir die paladin innogy kalkulation nachdem die e.on den preis „freiwillig“ auf 37,59 erhöht hat nochmals angesehen, da ich versucht hab, die 59 cents „nachbesserung“ zu verstehen.

paladin geht in ihrer rechnung mE davon aus, dass der komplette preis in E.on Aktien bezahlt wird, dem ist aber nicht so, grob umrissen, umfasst die sharekomponente 23% des gesamtdeals, setze ich dies mit dem preis der e.on aktien zum zeitpunkt des deal-closings an, kommt man ziemlich genau auf die 37,59…

Hallo, kannst du die Berechnung etwas detaillierter darlegen? Wie kommst du auf 23% aktiensnteil ?

kann auch sein, dass ich einen denkfehler habe…

hier die verschiebung der vermögenswerte, und hieraus erkennt man, dass der aktienanteil und somit durch börsenkurse beeinflusste komponente am rund 23% am gesamtdeal ausmacht.

und eigentlich kann es nur um die durch börsenkurse beeinflussbare werte gehen, wenn es darum geht die gleichstellung nach WpÜG zu gewährleisten.

und diese rechnung

“Was genau ergibt sich aber auf Basis des heutigen E.ON-Kurses für die zum Verkauf angedienten innogy-Aktien. Die Antwort ist ein relativ leichter Dreisatz:

RWE erhält für je eine innogy-Aktie 4,37098692 neue E.ON-Aktien (was sich aus obigen Umtauschrelationen ergibt)

Der aktuelle E.ON-Kurs notiert bei 9,70 Euro. Bereinigt um die Dividende von 0,43 Euro, die die heutigen E.ON-Aktionäre, nicht aber RWE im Jahr 2019 erhalten, ergibt sich ein Wert von 9,27 Euro pro E.ON-Aktie

9,27 Euro x 4,37098692 = 40,52 Euro”

stellt aber mE darauf ab, dass die RWE komplett mit E.ON aktien bezahlt wurde…

Danke. Paladin hat mittlerweile kommentiert:

https://paladin-am.com/investorenbrief/investorenbrief-q32019/

Sie sehen keine weitere Upside. Am Ende schöne Geschichte aber nicht viel rausgekommen…..

Pingback: Special situation update: Innogy, Osram, PNE AG, AGROB & Comdirect