All German Shares part 7 (Nr. 60-75)

Upfront remark:

This time, I increased the number of shares per post to 15. I am making good progress with the underlying analysis so I guess it makes sense to speed up the series somewhat.

Nr. 60: Ludwig Beck AG

Barely profitable retailer with a 110 mn market cap. However “super prime” freehold property in my hometown Munich. The in 2015 acquired retail chain Wormland has been put in run off and led to significant losses in 2018 and 2019. “Pass”

Nr. 61: S&O Agrar AG – ISIN: DE0005236202

Another Biogas penny stock, “pass”

Nr. 62: Cybits AG – ISIN: DE0007240004

Bankrupt penny stock. “Pass”.

Nr. 63: Data Modul AG – ISIN: DE0005498901

Specialist for industrial displays with 187 mn market cap. From 2014 to 2017, stock price went up by 6x. However YTD sales are down -20% yoy, business seems to be very cyclical. Another sector that I do not know much about, therefore “Pass”

Nr. 64: Deutsche Grundstücksauktionen AG – ISIN: DE0005533400

26 mn EUR real estate auctioning specialist. Could be more interesting in an economic downturn. However for me a “Pass”

Nr. 65: Aquamondi AG – ISIN: DE000A0KF6W7

4 mn market comapny with little observable activity “Pass”.

Nr. 66: Ferax Capital AG – ISIN: DE000A2LQ710

Tiny 4 mn market cap investment company. “pass”

Nr. 67: Adidas AG – ISIN: DE000A1EWWW0

I looked at Adidas in 2014, didn’t like (or understand) it and missed out on the best perfoming German large cap in the last 5 years. Now it is super expensive, therefore still “Pass”.

Nr. 68: Medigene AG – ISIN: DE000A1X3W0

170 mn market cap “Biopharma” company trying to develop a cancer cure. Loss making and not really my area of competence. “pass”.

Nr 69: Fintech Group – ISIN: DE000FTG1111

570 mn market Cap Online Brokerage renamed to “Fintech” (“it’s a tech comany baby…”) some time ago, but now being renamed again to “Flatex” as it looks. Phenominal performance of >800% over the last 3 years. Stock price is very volatile and it looks like that the company is “for sale”. “Watch” as potential special situation.

Nr. 70. Franconofurt AG – ISIN: DE0006372626

Small residential real estate (objects around Frankfurt) stock. Rarely traded, 50 mn market cap. Not my area of interest, “pass”.

Nr. 71 PEH Wertpapier AG – ISIN: DE0006201403

36 mn EUR market cap asset manager with Flagship fund PEH Empire. Fund is basically flat for the last 5 years. More interesting is the segment fund administration which is listed seperately on the stock exchange. “Pass”.

Nr. 72: SinnerSchrader AG – ISIN: DE0005141907

“Neuer Markt” survivor, digital marketing agency, however take over from Accenture and officially delisted. “Pass”

Nr. 73: Varengold Bank AG – ISIN: DE0005479307

Small 35 mn market cap bank however with a BIG tax fraud problem. “Pass”

Nr. 74 Lang & Schwarz AG – ISIN: DE0006459324

42 mn market cap small brokerage house, however with one interesting business line: Wikifolio, which allows almost anyone to become a fund manager. However, strange tax issues since 2018 (taxes higher than pre tax profits). “Watch”.

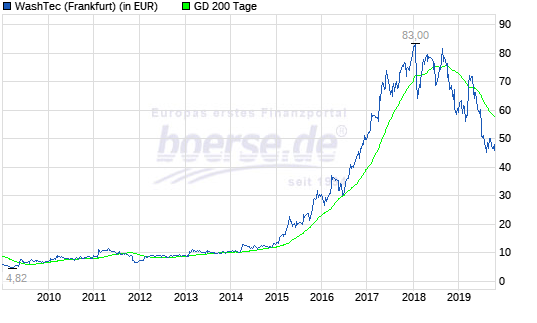

Nr. 75: Washtec AG – ISIN: DE0007507501

One of the typical “hidden Champions” with a 650 mn EUR market cap. Company designs, manufactures and services car washing facilities. Clear market leader in Germany. After a 8x increase from 2012 to 2018, stock is now consolidating.

The recently published Q3 numbers show stagnating sales and decreasing profits, although EBIT margin is still around 10%. For me a clear candidate to “Watch”.

Lang & Schwarz: „However, strange tax issues“

Reading your blog can save readers a lot of money. 😉

To be honest, i didn’t knew about cum ex issues.

Schaeffler

???

Schäffler… has been my worst investment 😦

Got lucky on that one. I stil think there is something there but I got out with only a small loss. As listed automotive suppliers go, this is a more promising one. I usually dismiss suppliers out of hand and this one should be on my “too hard pile” or “low return on braindamage pile” as well.

What irks me is the control structure and the fact that the Schaeffler familiy wants to sell down even more while maintaining control.

This attempt failed last time they tried. I think the behaviour of the controlling shareholder is a big issue in this one. It needs to be factored in that this control could be used against the best interest of owners of non-voting shares.