Uber – Business model and “sum of parts” valuation attempt

Health and safety warning: This is not investment advice. Please do your own research !!!!!

Following my book review of “Super Pumped” a few days ago I felt motivated (or “pumped up”) to look a little bit into Uber as a stock.

Uber is interesting in my opinion for a couple of reasons:

- They really disrupted the taxi market with their app and even managed to create a new verb “Ubering”.

- They managed to earn a dominent market share in many countries in a short time

- In the markets where they failed, they ended up with significant stakes in the leading players (Chine/Didi. Russia/Yandex, SE Asia Grab)

- The stock is extremely controversial

- the lock-up for old investors has just expired

- the stock price has been tanking for some time now

- the company is not easy to understand

Business model Ride sharing

Uber’s core ride sharing business is a typical 2 sided market place: On the one side we do have the drivers, on the other side the customers or “riders”. The business shows relatively strong network effects which can be summarized as follows: Customers normally (among other things) prefer that a driver will show up in a very short time. To ensure that riders will be able to show up quickly, a ride hailing company needs to employ a certain amount of drivers. In order to attract drivers, there need to be enough customers to make it worthwile driving. So achieving a certain minimum amount of drivers and riders is key to be able to offer a satisfying service.

One of the special features of the ride sharing business is however that it is what experts call an “asymptotic” market place as more drivers increase the value only up to a certain extent which is explained for instance here:

The third subcategory of marketplace nfx, illustrated by the red curve on the graph above, is what we call Asymptotic Marketplace nfx. It has the inverse properties of OpenTable’s delayed value curve. The initial supply quickly adds value to the demand side, but soon the value of increased supply starts to diminish.

The most famous examples of an Asymptotic Marketplace are ridesharing companies like Uber and Lyft, as we wrote about in this Uber case study. Up to a point, more drivers benefit riders because of reduced wait times. But beyond a certain point, the value to the rider steeply diminishes. Waiting 4 minutes for a ride as opposed to 8 minutes is a huge difference. But 2 minutes instead of 4 minutes? The value of increased supply diminishes drastically around the 4-minute mark.

Asymptotic Marketplaces are more vulnerable to competition than other marketplaces for this reason. If Uber has 1000 drivers in a certain area, a competitor might be able to provide comparable service with half as many.

Adding to this vulnerability, Asymptotic Marketplaces can be very susceptible to multi-tenanting. Many people use both Lyft and Uber to get around, depending on which one has lower pricing and faster waits at any given time. On the supply side, many drivers use both Uber and Lyft, depending on pricing and wait times.

This means that it is not a winner takes it all business, even the leader must be on guard not to create an opening for competitors.

Uber’s current shift to become a platform

The ride hailing business model as such is not a proven business model. Globally, I do not know of any really profitable stand-alone ride hailing company. Maybe because of this, Uber under the new CEO clearly tries to become a platform company, i.e. trying to leverage their user and driver base for other services.

In Septmember, Uber in a big event presented what they plan to offer. And just a few days ago, they launched Uber Money which looks like an intersting product both for drivers and customers. At them moment, clearly only Uber Eats has reached a certain size, although Uber Freight (basically an Uber style freight forwarding service) seem to have a relavnat size. Also the recent acquisition of Cornershop, a grocery delivery service makes a lot of sense when thinking about a platform business.

The platform game is clearly a gamble but in my opinion this is the only way for Uber to stay relevant and morph into a kind of “super app” to manage many online/Offline transactions, similar for instance what happens in Asia with players like Didi, Go-Jek or WeChat.

A Valuation attempt:

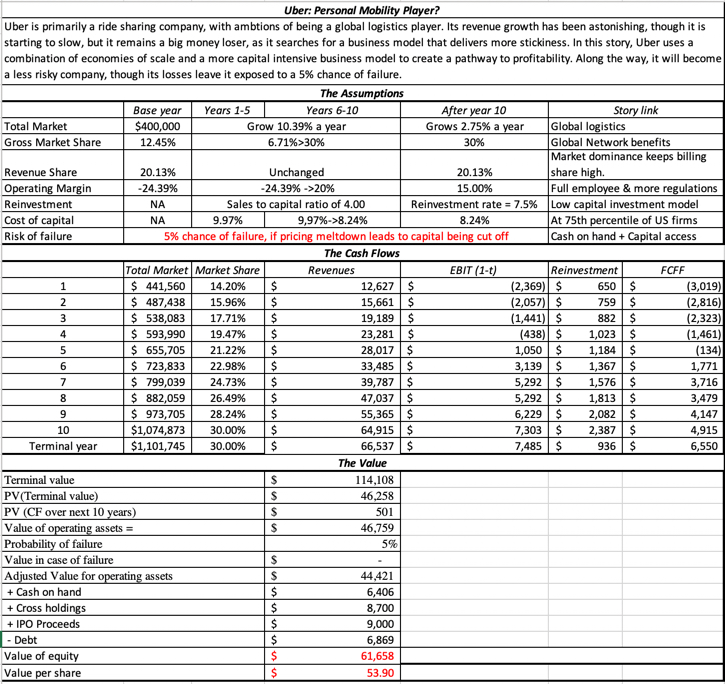

Before now developing my own model, and as I don’t want to reinvent the wheel, lets look at how “the professor” has been valuing Uber:

Remark: With an updated sharecount, this results in a value at around 31-33 USD per share.

Damodaran basically modelled the adressable ridesharing market over 10 years and assumed a market share of 30% at that time as well as market growth of ~10%. What I find interesting is the fact that he uses a rather low discount rate, starting with around 10% and then goign down to 8%. He deducts 5% of the resulting EV as “risk of failure” but subjectively I would assume a higher risk at the moment, especially following the WeWork extravaganca.

He adjusts for Net debt and the extra assets (Grab, Yandex, Didi) although these stakes are extremely hard to value.

“Sum of parts valuation” more appropriate ?

However I think Damodaran’s model lacks one crucial feature: He omits anything that is not ride hailing. Uber itself in its 9 month report divides its business into 5 pillars:

- Rides

- Eats

- Freight

- other bets

- ATG and other

Rides

Instead of Damodaran’s DCF, I would use rather the trading multiple of competitor Lyft. Lyft is currently valued at ~12.9 bn USD and 955 mn revenue in Q3 which for simplicty reasons I would annualize to 4 bn. Deducting ~ 3bn in net cash, this results in a revenue multiple of 10/4=2,5 for Ride Hailing. Uber had ~3 bn revenue in the rides segment in Q3, which then on an annualised basis gives us 3x4x2.5=30 bn value for ride hailing.

Eats

Eats in Q3 had gross booking of around 3.7 bn and net revenues of ~400 mn. GrubHub for instance, which generated 320 mn in Revenue in Q3 on 1.4 bn bookings is valued at 3 bn USD. So I think Uber Eats at least should have the same valuation although it is growing much faster. I would actually estimate the value closer to 4-5 bn USD.

Freight

Freight is an interesting new business, matching more than 50000 truckers with freight opportunities. Freight had around 220 mn USD in Q3 sales and is growing at around 100% yoy. The freight market is potentially huge and some mor infor can be found in this Goldman Sachs report. Standalone, such a business would clearly be worth at least 2-3 bn USD in my opinion.

Other bets

With 38 mn in Q3 revenue, the other bets are at an infant stage. I would give this segement a 500 mn valuation as it is rapidly growing (10x sales yoy)

ATG

Now ATG, which is their “moonshot” division is an interesting case. This division is bruning around 500 mn annualy and not making any sales. Normally, one would attach a negative value to this. However, Uber managed to sell a 1 bn stake at a 7.25 bn post valuation to Softbank, Toyota and Denso. After the WeWork debacle, I would haircut anything that Softbank does at 50%, so this would give us ~3 bn USD for the remaining stake in this division.

Extra assets: Grab, Didi, Yandex

Valuing Uber’s stakes in Didi, Yandex and Grab is not so easy as all are non-traded companies and values are hard to get.

Didi’s last valuation has rumoured to be 62 bn when (again) Toyota invested. In april 2019, Grab seems to have been valued at 14 bn USD, Yandex which seems to go for an IPO soon, is supposedly valued at around 8 bn USD. I do not know what the current % holdings of Uber are, but in March, Uber owned 20% in Didi, 28% in Grab and 37% in Yandex. This would give us a value of around 20 bn USD, much higher than Damodaran estimated back then However, these companies are not valued in a vacuum, so I would apply the loss that the Uber Stock suffered since the IPO to these stakes as well which amounts to -40%

Bringing it all together:

| Uber Valuation | No of shares | 1705.969049 | |

|---|---|---|---|

| Sum of parts | bn usd | Per share | |

| – Rides | 29 | ||

| – Eats | 4.5 | ||

| – Freight | 2.5 | ||

| – other bets | 0.5 | ||

| – ATG | 3 | ||

| Net Cash | 12.7 | ||

| Didi, Yandex, Grab | 11.8 | ||

| Sum | 64.0 | 37.5 | |

| Current Market cap | 46.3 | 27.1 | |

| “Discount” | 17.7 | 10.4 | |

| Upside in % | 38.2% | 38.2% | |

| Extra Assets | Valuation 100% | % | Value |

| Didi | 64 | 20% | 12.8 |

| Yandex | 8 | 37% | 2.96 |

| Grab | 14 | 28% | 3.92 |

| 19.68 | |||

| minus Uber Discount | -40.0% | ||

| Value adjusted | 11.808 |

So at the moment my “model” shows a “fair value” of around~37 USD, an implicit upside of almost 40%. However, in Uber’s case, that might not be enough.

Despite burning cash operationally, Uber has announced 2 acquisitions (Careem, Conrershop) which will be a further drain on Cash. For Careem, the cash component is 1.4 bn USD,

Personally, I think the Cornershop acquisition plays well into the platform strategy but the main issue is clearly: Will Uber run out of cash before they manage to reap the benefits of a potential dominating “online to offline” platform ?

My gut feeling says that a higher upside is needed to compensate for this risk to justify a “full position” . On the other hand, Softbank clearly will have no interest in seeing a big second debacle soon after the WeWork Fiasco, so there is clearly a chance of more money from Softbank, as we have seen for instance with the ATG transaction. I could also imagine that Uber would be able to at least partially sell stakes in Yandex, Grab or Didi at the values that I assumed.

Quick note on Management:

Without having researched too deeply into the company, for me it seems that the new CEO Dara Khosrowshahi does a good job so far, both in cutting costs but also developing the strategically important platform model. As a side note: It looks like that former CEO Travis Kalanick already has created the next Unicorn company…..

Summary

Uber is clearly one of the most controversial stocks at the moment, with maybe the exception of Tesla and Netflix. However I do think there is value in the company and if they manage to transition to a real “platform” the upside could be huge.

However there are also things at Uber that I don’t like, for instance creating nonsense “Ride adjusted Ebitda” which is basically gross profit.

Nevertheless I decided to start a 1% position in Uber at 26,90 USD/share in order to actively monitor the comany and to potentially increase the position if my thesis on the transition to a platform plays out.

P.S.: I expect critical comments for this post. So don’t hold back but maybe support them with facts 😉

Sold my Uber shares at 35 USD. That’s slightly short of my 37 USD fair value, but the quick rebound without any significant new information made me a little bit more cautious.

Interesting article on Uber UK drivers and the gig economy:

https://www.bbc.com/news/technology-50418357

Hello. Thanks for this well balanced article. I am short uber and have just one comment/correction to your article. Based on the SEC filings Careem will (at the current share price) to be fully paid in cash. We talk, depending on due diligence and regulator approve, of 3.1 billion USD of costs. Reason for this is that Uber agreed to allow a cash claim instead of the equity if the redemption does not take place within 90 days after completion of the transaction. as the agreed price was 55 USD per share nobody will take the equity… this may also be the reason for the latest debt raising by Uber with an interest rate of around 7% (!) p.a. Please verify my statement (e.g. by checking the latest 10Q filing, which I highly recommend to read – hardly ever saw so many risks listed). Regards

Thanks for the comment. Personally, i Think 7% is quite cheap considering uber’s risk profile.

Pingback: Uber – Business model and “sum of parts” valuation attempt

When I looked at your post the first time I knew instantly that the Valuation picture is from ‘the professor’ (nice way referencing to him! by the way). I like valuation posts from authors referring to him, since I believe it is a quality-signal.

Best s4v (one of your followers)

What about the labour law changes in Spain and California and the law suits in Australia and other places? In my opinion the probability of a catastrophic loss is bigger than 5%.

I find it hard to get a good estimate of the final unit economics. At what point is the business model due to labour cost (employees vs freelancers) or failing demand (take rate that is sustainable for all stakeholders: customers and suppliers) broken?

The problems you are mentioning are valid and extend to other countries as well I guess this is one of the side effects of a really disruptive product. There are actually a lot of issues that are not as well known (i.e. VAT disadvantage in germany taxis 7%, ride hailing 19% etc.). On the other hand most of the problems are not a secret and should somehow be priced into the share price to a certain extent.

Unit economics in a two sided marketplace are difficult to determine and in a three sided one (Eats) it is even more difficult. But as I mentioned: I don’t belive that stand-alone ride hailing will be highly profitable. The platform model is the interesting one. And/or the other businesses.

Nice analysis!

To me it’s uninvestable until they sell/close ATG. There’s strong negative synergy here: they should buy such tech from best of class third party vendors, when/if it becomes usable. It’s a complete distraction from the platform business.

Some people argue they face headwinds due to regulators pushing them to employ drivers directly (it is indeed fake self employment in most cases) though I don’t see that as a problem: as all players have to follow the same rules in a given jurisdiction, they should be able to pass the cost (if any) to users ultimately (demand is probably relatively inelastic).

With regard to the employment issue: This is a double sided issue. Most dirvers drive at least for one other service. If they would actually become employees, the challenger (Lyft in the US) would really get into trouble.

Very nice this one. I’m long Softbank for 4 Years. Uber for me was a bet on self driving cars.

https://www.wired.com/story/bet-uber-bet-self-driving/

What do you think about this?

I don’t believe that autonomous driving will Come soon. If they would sell that part i would be happy.