All German shares part 8 (Nr. 76-100)

As I am making good progress, I included this time 25 stocks. The first 100 are done, another 700 or so to go 😉

Nr. 76: Uniwheels AG – ISIN DE000A13STW4

Uniwheels is a 800 mn EUR market cap car supplier. Interestingly the German company floated its shares in Poland in 2015. Their main products are aluminium rims / wheels for cars. In 2017, the founders of Uniwheels sold their majority to US based Superior. Maybe a squeeze out opportunity, but I know little on how this works in Poland. “Pass”

Nr 77: Foris AG

14 mn EUR market cap litigation finance company. However no growth over the years and loss making in 2018. “Pass”.

Nr. 78: KPS AG

280 mn EUR market cap consulting company specialising in “digital transformation”. Profit 2017/2018 dropped significantly, however in the 9M of the current year recovered. Stock is not cheap at 11x EV/EBITDA but still a candidate for the “watch” list.

Nr. 79: Ecolutions GmbH & Co KG

Initially French listed but now insolvent renewable energy company. “Pass”.

Nr. 80: Spark Networks SE

130 mn EUR market cap provider of specific themed dating sites. Basically a “roll up” of fringe dating sites. Very ambitious targets but business seems to be shrinking and company made significant losses. “Pass”.

Nr. 81: Hydrotec AG

Insolvent “water technology” company. “pass”.

Nr. 82: GxP German Properties AG

40 mn Office property company. Stock price below NAV but not clear what the controlling shareholder’s intentions are. “Pass”

Nr. 83: Softline AG

13 mn market cap IT consulting and support company. Sales are stagnating and company is currently unprofitable. For some reason, despite the small size company expanded unprofitably into other countries. “Pass”

Nr. 84: Wild Bunch AG

Trroubled Media distribution company. Involvement of Lars Windhorst /Sapinda. “pass”.

Nr. 85. Wüstenrot und Württembergische AG

1.7 bn market cap insurer and real estate savings player. Optically very cheap but fundamentally impacted by low interest rates. Nevertheless “Watch”.

Nr. 86: Global PVQ SE

Eur 1 mn pennystock. “Pass”

Nr. 87: Nebelhornbahn AG

43 mn Cable Railway operator. Stock performed quite well over the past 3 year although I don’t really know why because the business is capital intensive and subject to non controllable influences (weather, snow etc.) “Pass”

Nr. 88: MPC Capital AG

Once high flying “alternative” 60 mn market cap asset manager specializing on ships, real estate and infrastructure. However a lot of their projects were total losses and the company is being sued from unhappy investors which creates significant risks. Despite book value of 100 mn EUR a clear “pass”.

Nr. 89: Ringmetall AG

77 mn EUR market cap Holding company for several small metal working companies. Good: management owns >50 %, limited leverage; bad: net income declining (lower than 2016 for 2018, further EBITDA decrease despite acquisition 6M 2019). but a “watch” candidate.

Nr. 90 Maier & Partner AG

Insolvent “shell” company. “Pass”.

Nr. 91. HWA AG

Despite a boring name, a 80 mn EUR market cap car racing company working exclusively for Daimler. The founder of HWA had also founded AMG, now Daimler’s own tuning/racing subsdiary. Company is controlled and owned by insiders, only relatively small free float. Topline has been growing nicely, but profitability is lacking. “Pass”.

Nr. 92: GBS AG

Company has been liquidated. “pass”

Nr. 93: SMA Solar AG

Solar technology company (inverters) with 850 mn market cap. Big net cash position but declining sales and low profitability. Not my area of expertise. “Pass”

Nr. 94: Crop Energies

500 mn EUR market cap ethanol producer. 75% of the stocks are owned by Südzucker AG and related parties, only 25% free float. Volatile profits due to high Capex and impact of oil prices. But a “watch”.

Nr. 95: Amalphi AG

5 mn market cap IT services company. According to the website one of Germany’s leading IT services company with 2 mn sales, loss making. “Pass”

Nr. 96: BASF AG

60 bn market cap chemical giant, famous for its “Verbund” production site in Ludwigshafen. Currently stagnating top line and significantly shrinking operating results due to overall business climate. Although the company is relatively well run, they were unable to create equity value over the last 7 years or so. “Pass”

Nr. 97: bluepool AG

Insolvent shell company. “Pass”

Nr. 98 Norma Group SE

Norma Group, IPOed in 2011 with a 1.1 bn market cap is somehow similar to Stabilus: A company producing small ticket fasteners etc. for the car industry with relatively healthy margins and historically also good growth. However in the first 6 months 2019, organic sales growth shrank and the profit margins shrank even faster. Similar to Stabilus, the stock price at the time of writing has lost already -50% from the peak in 2018. However leverage is not insignificant (~500mn EUR) and in my understanding, their products are mainly used for combustion engines. Overall not a bad company but at this stage I will “pass”.

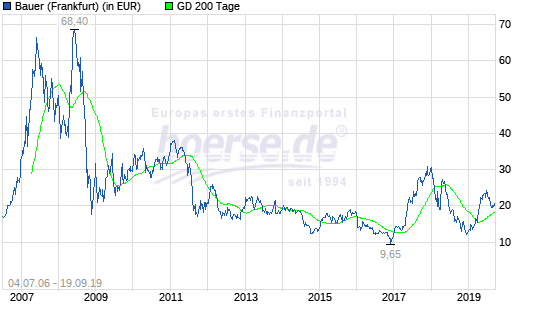

Nr. 99: Bauer AG

Bauer AG is a combined special construction company and construction equipment manufacurer. I actually owned the shares long time ago after the IPO (2006/2007) and made some profit with it before the stock dropped a lot and then went more or less only sideways for the last 10 years:

The problem with Bauer is that the two segments, construction and machinery is very different. Machinery is actually a nice business with 10% EBIT margins, however construction has been unprofitable for a long time. Additionally, the company is very capital intensive and they finance themselves with a lot of bank debt. Other construction companies have the ability to attract prepayments but somehow Bauer AG does not. After problems rolling over the debt they were able to reduce net debt in 2018 but are in my opinion still vulnerable to a future economic downturn. Therefore I “pass”

Nr. 100: Seven principles AG – ISIN: DE000A2AAA75

Smaller size 50 mn market cap IT consulting company specializing in digitizing business models. However the business is currently in trouble. Sales go down and the company is making significant losses. The CEO left a few months ago. “pass”

I stumbled upon Crop Energies while looking into Südzucker. Thought it was a better idea than the parent.

After some digging around I found that there are many struggeling bio ethanol companies around.

It looked like a tricky businenss and was a pass for me then because:

– Volatile commodity in- and outputs – not necessarily moving in parallel

– Extremely dependent on subsidies and regulation

– Negative image because of turning food into fuel

– Low and volatile “profits”

Wüstenrot und Württembergische AG has looked for years supercheap. Valuetrap?

My subjective view: Yes. Low interest rates kill both, their savings and the insurance business.

On Nebelhorn: wasn’t Rib Vinall invested in Engelberg-Titlis cable car? Guess for it to be interesting, Asian tourists have to love it and it has to be high enough to have natural snow in winter. There would come pricing power with it. And the ones who run it need to understand capital allocation. Okay, all in all quite unlikely.

P.S. Still enjoy your site. Thanks for the effort!

Rob Vinall ‘s Titlis position is testimonial (~ 1% or less). My guess: he keeps it strategically only to have easier access to Engelberg’s premises (and to celebrate his annual meeting 😉 ). And because BusinessOwner portfolio has been for a while so concentrated that cosmetically it paid off to have a 10th position (otherwise fund would nominally have 9 positions only).

Hi,

What about GK Software?

Specialist for PoS Software

SAP sells their software.

Founders (G&K) still holding 50% and buying!

Strong growth in past and forecast.

Weak development of share prices (which o can’t explain/find a reason.

Well, whenever my random number Generator will point me to them, i will habe a look

It feels my enthusiasm is not helping to get your interest in that one.

You are looking at the companies based on random numbers generated, referencing to a list containing all German shares? Nice project 😉

Yes. The random part is really fun.

Good method to eliminate some bias! (at least, that is my first guess)