All German Shares – Part 9 (Nr. 101-125)

And another 25 stock batch with some very interesting companies. At some point in time I will release a table with all the stocks and a link to the respective posts.

Nr. 101: Baumot Group AG

36 mn market cap company that calls itself the “clean air” company. According to the company huge potential if hardware exhaust filtering for problematic Diesel cars would kick in which the company is manufacturing. However, currently the company is in deep trouble, sales tanking and huge losses. Several capital increases and debt equity swap. “pass”.

Nr. 102: BHS Tabletop AG – ISIN: DE0006102007

A traditional B2B tableware manufacturer with a 55 mn EUR market cap, equipping hotels, airlines etc with plates, cups etc. Profitability is declining since 2018 and margins are very small (EBIT margin <5%). “pass”.

Nr. 103: Alstria Office REIT

Alstria is a 2.7 bn office REIT with a rock solid development over the last few years. They offer a decent dividend yield (3,6%) and if someone would force me to invest into Real Estate, Alstria would be one of my prime choices. Especially the REIT structure avoids double taxation of profits as REITS are a “Pass through” structure. However, I guess for many investors, the limit on leverage makes such a REIT less sexy than more highly levered listed real estate plays. As I don’t consider investing into a general real estate vehicle anyway, the result for this exercise is a “pass”.

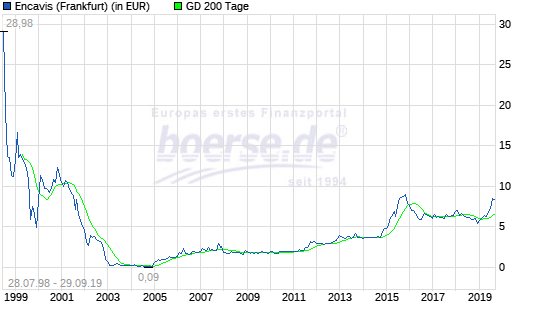

Nr. 104: Encavis AG (ex Capital Stage)

The 1.1 bn EUR market cap company is a “child” of the Dot.Com boom and was “reverse IPOed in 2001. The company initially was named Capital Stage AG and invested as PE into Solar companies before pivoting into buying solar parks and wind parks and running them. As the stock chart shows, the company performed very well over the past few years but still hasn’t reached its Dot.com hieghts yet:

Looking a little bit into the numbers, one things stands out: As an asset play, Encavis trades at 2x NAV which is rich. To make things worse, the NAV consists to 100% of Goodwill and the amount of debt matches 1:1 the amount of “real” assets. So there seems to be built in a lot of optimism into the share price of what these windparks and solar parks are worth. As far as I understand, Encavis also doesn’t have the ability to actually develop this assets but buys them from developers. Therefore it is quite interesting how they can justify the Goodwill on their balance sheet. So despite the fact that this sector is “super ho”, I’ll “pass”.

Nr. 105: GAG Immobilien AG

Within the German Small Cap community, GAG is a quite well known “special” company On the surface, it is an extrem cheap residential real estate company focused on the Cologne area, on the other hand, the company is majority owned (88%) by the City of Cologne. Minority shareholders are not a priority and the Citiy of Cologne is famous for their special version of corruption which has even an own name (“Kölsche Klüngel”). Of course, the company used a weakness in German law to delist the company from the official market in 2016 and the stock now is traded OTC in Hamburg only.

I guess this stock could be interesting für people who like long fights against bureaucracy and corrupt cities, but for me it always has been a “pass”.

Nr. 106: Agennix AG

1.5 mn market cap company which is in liquidation. “Pass”

Nr. 107: M4e AG

Media company, has been squeezed out already. “Pass”

Nr. 108: Itn Nanoinvation AG

7 mn market cap, something with Nano. Insolvent in 2018, management gone and fines from the regulator. “Pass”.

Nr. 109: Phicomm AG

1 mn EUR market cap company with 6 (?) name changes in the last few years. “Pass”.

Nr. 110: LS Telecom AG

43 mn market cap specialist for technology around radio networks. 2017/2018 loss making, the first 6m 2018/2019 looked like a turnaround. Business seems to depend on large projects but management seems to be confident that the turnaround will last and 5G plus industry 4.0. will create opportunities. “Watch” but with lower priority.

Nr. 111: Brain AG

210 mn market cap “white biotech” company. I do not understand what they are actually doing, but net profit margin is around -30% and reporting is very intransparent. “pass”.

Nr. 112: Beta Systems AG

120 mn EUR market cap software company, specializing in Data Center Management software and IT access management. One doesn’t need to be a genius that Datacenter management is not such a great business anymore with more and more companies moving into the cloud. Not surpisingly, the last full year result 2017/2018 showed a -8% decrease in sales and a -50% decrease in net profit. In the first 6 months of the current FY sales rebounded but is not really transparent how much the recent acquisitions contributed. The company has a big cushion of liquidity but with one big caveat: A lot of the liquidity is parked by it’s majority shareholder Deutsche Balaton. Dt. Balaton is one of these companies in Germany which doesn’t have the best reputation, therefore I “pass”.

Nr. 113: ThyssenKrupp AG

One of Germany’s industrial icons, still 8 bn market cap. However badly managed for a long time. Loss making steel division got cross subsidized by successful divisions like elevators. Large pension liabilities. Currently sale of elevator division under review. nevertheless, life is to short to invest in such a company. “pass”.

Nr. 114: Schulte Schlagbaum AG

16 mn market cap small cap, Specialises in certain access solutions (locks) for commercial use. The company is debt free, however looking at the 2018 annual report shows, that the profitability of the company is deteriorating. Margins were never that big anyway but since 2016 sales have stganated and the small proft has turned into a loss. The first 5 months of 2019 didn’t show any improvement. If the company can’t make money in a relatively positive economical situation, things will clearly not improve if Germany actually goes into recession. “pass”.

Nr. 115 Aurubis AG

Aurubis AG, formerly known as Norddeutsche Affinerie, is a 1.8 bn market cap copper producer. the biggest one in Europe and the second biggest worldwide. The core business is clearly cyclical and margins depend on the mix of copper prices, scrap etal prices and energy cost.

Nevertheless I had a good impression form their financial reports. For instance I liked that management is incenitviced by both EBIT and ROCE which for such a capital intensive business makes sense. Largest shareholder is steel company Salzgitter, but also special Situations fund Silchester owns a 5% position. The company has lost more than -50% from its 2018 top, but also profits are shrinking since a few quarters. Nevertheless and interesting stock that will move on “watch”.

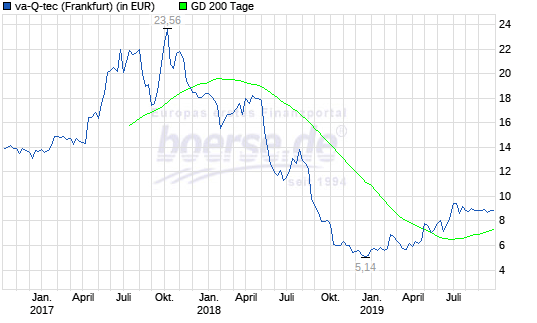

116. Va-q-tec AG – ISIN DE0006636681

Va-q-tec is a company that has been spun off from the University Würzburg and IPOed in 2016. The company specializes in insulation technology with the major application of cooling containers for medical purposes that don’t need energy to keep the temperature at a constant cool level. It is also one of the German companies that I totally missed and didn’t know that they existed. The company ipo’ed at 12,30 EUR per share, increased ~100% until 2018 but then got hammered in 2019:

At 9 EUR per share the comapny is valued at 117 mn. For this we get annualized sales of around 65 mn EUR, annualized EBITDA of 9 mn and a current growth rate of ~25%. Then however we need to also add around 40 mn gross bank debt to EV.

The company not only produces the boxes but also leases them out which might explain the high bank debt, but which clearly increases the financial and company risk. Nevertheless this company looks somehow interesting, therefore “watch”.

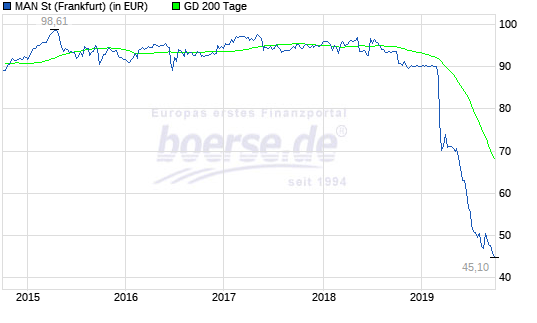

117. MAN SE

MAN SE is a German heavy truck manufacturer, now part of Volkswagen’s heavy truck subsidiary Traton which had recently ipo’ed. I actually owned MAN SE as a special situation back in 2013-2015 but luckily sold and didn’t become too greedy. What happened was interesting: Volkswagen actually cancelled the profit-and-loss transfer agreement, that guaranteed a fixed dividend and in result, the risk of the security went from more or less fixed income back to full exposure towards the underlying business.

The stock has lost >50% since then as we can see in the chart.

For me, MAN SE is clearly a “watch” and should be looked at together with Traton.

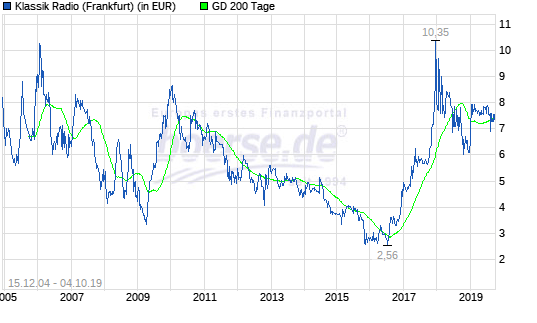

118. Klassik Radio AG

Klassik Radio AG is, as the name indicates a small, 34 mn EUR market cap radio station focusing on classical music. The company went public in 2004 and as the stock chart shows had some rough times:

Recently however, the company shows good growth and profitability. Therefore I will put them on “watch” to look at them at a later point, however not with high priority

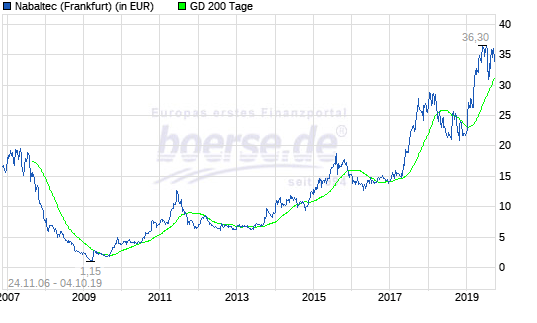

119. Nabaltec AG

Nabaltec is another company I never looked at. With 300 mn market cap it is not that small. Nabaltec is a specialty chemicals company, producing among others fire inhibiting materials which they claim are environmental friendly.

Nabaltec went public in December 2006 and after the financial crisis the company had to go through a deep hole but now clearly is on a run as the stock chart shows:

The company has solid double digit EBIT margins, is growing decently and has only a relatively manageable amount of debt (net ~40 mn). However there are some pension liabilities and with an EV/EBIT valuation of currently (300+40+40)/25= 15x the stock looks fairly priced. Nvertheless a clear “Watch” candidate.

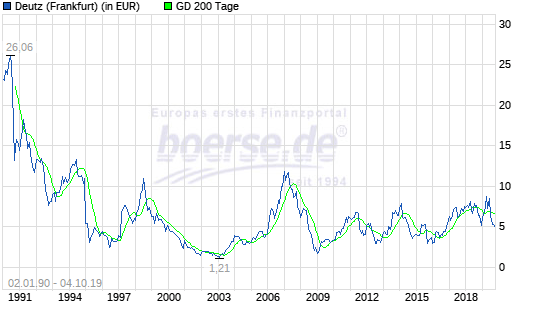

120. Deutz AG

Deutz is a 617 mn EUR marketcap manufacturer of diesel engines that are mostly used for construction machines and other “heavy duty” uses. The company is very cyclical but over the long run hasn’t really managed to create value for its shareholders as the long term chart shows:

The stock currently looks cheap with a single digit P/E but orders are already decreasing and the next down cycle is visible. Life is to short for these kind of stocks, so “pass”.

121. 2G Energy AG

2G Energy calls itself “one of the leading manufacturers of decentralised energy generation systems using combined heat and power (CHP)”. This technology according to my limited knowledge is climate friendly as the underlying fuel is used much more effectively than traditional heat or electricity only generating models.

With a 163 mn market cap, the company is not small and the share price has almost doubled YTD 2019. Sales in the first 6 months have increased by +20%, so growth looks good. The balance sheet looks conservative and managment owns a significant stake.

However profitability is very low, with gross margins below 30% and EBITDA Margins <10% despit a growing service component. Although it might be a little bit late, I put them on “watch”.

122. Pinguin Haustechnik AG

Tiny, 4mn EUR market cap non operative shell company. Some attempts to takeover, no someone seems to have bought a majority. However a clear “pass”.

123. Wirecard AG

15 bn EUR market cap payment company, DAX member. Big fight with the Financial Times and short sellers if the company is fraudulent. A few days ago, news surfaced that there problematic Singapore sub didn’t receive an audit opinion for 2017 due to lack of information for the auditor. My mental model is to stay away in principle form these kind of situations, no matter what. “pass”

124. Activa Resources AG – ISIN: DE0007471377

0.5 mn market cap Nano stock. “pass”.

125. Ernst Russ AG

27 mn market cap Asset manager (Formerly HCI Capital AG) specializing on ship assets and now also real estate. P/B < 0.5 but assets are mostly illiquid shipping assets. Could be an interesting asset/liquidation play but not what I am looking for. “pass”.

All good but as I mentioned: I have an issue with Dt. Balaton and one thing you can be sure: Dt. Balaton will never offer a “decent price” because they have all the cash already.

With decent price I meant if Beta Systems can buy someone at a decent price. Balaton for sure won’t overpay for Beta Systems , and it is not strategically interesting for someone external to buy it for a “strategic” high price. If you don’t like Balaton I can’t blame you though.

My thought what they want with Beta: Balatons business is to be a holding company, but they don’t have much operative experience. But they see that software is a very good and cash-generative business model, so I suspect they rather might use Beta Systems as a holding for software investments. This would ensure that there is someone who knows how to operate IT/software businesses, and Beta clearly has the money to acquire some. On the AGM they complained a lot about high prices, so probably they will only get some smaller, slow growth IT companies – but this might of course be good capital allocation.

Risks: If Beta’s stock tanks Balaton might be tempted to do a takeover bid at low prices and delist. And if they are really evil they might force Beta to buy a software company from the Balaton portfolio at too high prices. But at least Zours is not Förtsch, so I think he will try to use Beta as indirect holding vehicle.

What issue do you have with Dt. Balaton?

No issue, I just don’t want to be involved with them.

Like with the italian mafia, the spanish totalitarian regime, the balkan mafia, the turkish government, or the ebola. Abolute no contact with them

Hi, mmi. I’m a long time Catalan follower of your blog (from the Boss score times!) and victim of the Spanish totalitarian regime, and all I can say is that I could not agree more with you.

And congratulations for your excellent blog, full of interesting content and thoughtful investing ideas. Keep up this great work!

Hi,

one remark to Beta Systems as I have bought it and also was at the AGM last year: It is true that the core market is shrinking, but with surprisingly low speed. Especially the large financial institutions (banks and insurances) run still on IBM mainframe computers and need such a software. I remember that they said the competitors basically stopped product development already, so they are in a good position to gain some market share in this shrinking market. The fluctuations you noted are at least partly due to the way they sell licenses and recognize revenue. Companies buy a license often 3 or 5 years if I am correct, and this revenue is recognized immediately. So they can quite well predict which years will be good ones and which ones are bad. 19/20 should be good, 20/21 rather poor and 21/22 quite good. This is what they communicated recently:

“””

Im Geschäftsjahr 2019/20 wird unter der Annahme einer einigermaßen stabilen

volkswirtschaftlichen Entwicklung in den Kernmärkten aufgrund der kürzlich

getätigten Akquisitionen sowie eines gut laufenden Bestandsgeschäft eine

weitere Verbesserung des Umsatzes und des Ergebnisses erwartet. Vor diesem

Hintergrund erwartet der Vorstand der Beta Systems Software AG im kommenden

Geschäftsjahr 2019/20 einen Konzernumsatz zwischen EUR 60,0 Mio. und EUR

66,0 Mio. (Geschäftsjahr 2017/18: EUR 45,9 Mio.). Das

Konzernbetriebsergebnis (EBIT – Ergebnis vor Zinsen und Steuern) wird auf

Basis der aktuellen Planungen und Konzernstruktur (d.h. inklusive der in

diesem Jahr getätigten Akquisition der Habel/Akzentum Gruppe)

voraussichtlich zwischen EUR 7,0 Mio. und EUR 10,0 Mio. liegen

(Geschäftsjahr 2017/18: EUR 3,8 Mio.). Für das EBITDA (Ergebnis vor Zinsen,

Steuern und Abschreibungen) wird ein Wert zwischen EUR 9,0 Mio. und EUR 12,0

Mio. erwartet (Geschäftsjahr 2017/18: EUR 5,5 Mio.).

Wie bereits mehrfach berichtet, hängt die Höhe des Umsatzes und des

Ergebnisses insbesondere auch von den im Geschäftsbereich DCI zur

Verlängerung anstehenden Kundenverträgen ab. In dem darauffolgenden

Geschäftsjahr 2020/21 ist wie im Geschäftsjahr 2017/18 von einem

vergleichsweise geringen Volumen der zur Verlängerung anstehenden

Bestandskundenverträge auszugehen. Deshalb geht der Vorstand hier davon aus,

dass das Konzern-EBITDA sich im Intervall von EUR 5,0 Mio. bis EUR 8,0 Mio.

Euro bewegen wird. Das anschließende Geschäftsjahr 2021/22 hingegen wird

voraussichtlich ein starkes Verlängerungsjahr werden, so dass hier von einem

EBITDA zwischen EUR 13,0 und EUR 16,0 Mio. ausgegangen wird. Diese Werte

sind als absolut indikativ zu betrachten, da aufgrund des sehr langen

Betrachtungszeitraums noch viele ungeplante Effekte positiver und negativer

Natur auftreten können.

“””

In my opinion a quite safe (lots of cash) and boring stock, that might have good potential if they manage to get a takeover done for a decent price…