All German Shares – Part 10 (Nr. 126-150)

Another 25er batch with in total 6 candidates for my watch list. Enjoy (and only around 650 or so to go…..)

126. Norddeutsche Steingut AG

18 mn market cap ceramic tile manufacturer. Despite building boom, stagnating/shrinking sales and increasing losses. P/B below 0.5 but high bank debt. “Strong pass”.

127. DCI Database AG

IPOed at the peak of the 2000er internet boom, this 2.5 mn EUR market cap company surprisingly still exists. The company creates ~3 mn sales and shows profits of 300k. I guess it is kind of a privet vehicle for the CEO. Instead of dividends, the CEO takes out the money as salary. “Pass”.

128. Comdirect AG

1.8 bn listed subisdiary of Comemrzbank. Commerzbank amde an offer to buy out the minorities at 11,44. The current price of 12.80 EUR indicates that shareholders hope for a better offer. “Watch” as special situation.

129. OVB Holding

240 mn market cap insurance distribution company, majority owned by German Insurer Signal Iduna. Free float only 3%. Had a very mixed reputation in the past for extremely aggressive selling especially in Eastern Europe. Company is very cash rich but profitability is surprisingly low for such a kind of business and maybe is driven by the shareholders interests. “pass”

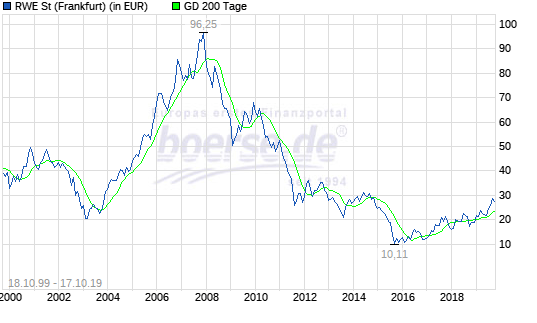

130. RWE AG

17 bn market cap utility. I actually owned the stock once but luckily sold before the structural change kicked in. Overall in my opinion not a good business model for the future. The stock price did recover from its low but long term the company did not create or even retain value. “pass”

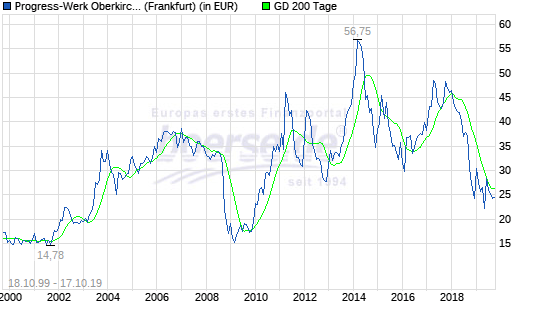

131. PWO AG

76 mn EUR market Cap auto supplier. Typical “Mittelstand” company. Very volatile business as depending fully on the business of the major automobile companies as one can see in the chart:

The 2018 annual report shows the main problem: Sales are increasing every year but profit is lower than 5 years ago. This indicates a lack of pricing power, for whatever reason. Company has significant leverage and returns on capital are very low. “pass”.

132. Biotest AG

870 mn market cap company produing pharamceuticals based on blood plasma. I actually owned the stock once (pre blogging) and made a good cut but back then management was not high quality.

In between, Biotest has been majority acquired by a Chinese investor and had to sell its US subsidiary to competitor Griffols. The current share price at 22,30 EUR is significantly below the 28,50 offer from 2 years ago.

However there seems to be another complicated 3 party deal going on including another Chinese company and competitor Griffols.

Could be an interesting situation, but another mental model of mine is to stay away from anything that is owned by Chinese investors. Therefore “pass”.

133. BMP Pharam Trading AG

6.5 mn market cap company trading bulk pharmacuetical products. Annual report does not show consolidated numbers “pass”.

134. Aovo Touristik AG

5 mn EUR market cap travel company. specializing in “event trips”. Losses in 3 out of the last 5 years but profitable in 2017 and 2018. Company is not growing much but has landed an interesting contract for 2020 (Passionspiele Oberammergau). Nevertheless too small and therefore “pass”.

135. Stinag Stuttgart Invest AG

380 mn market cap company that was originally a brewery. However the operating business was sold in 2018 at a loss and the company now only runs a real estate portfolio plus some development activity. Not my area of interest. “pass”.

136. Arn. Georg AG

Strange 5 mn market cap company. Almost no information, no homepage. Some information on W:O. “pass”.

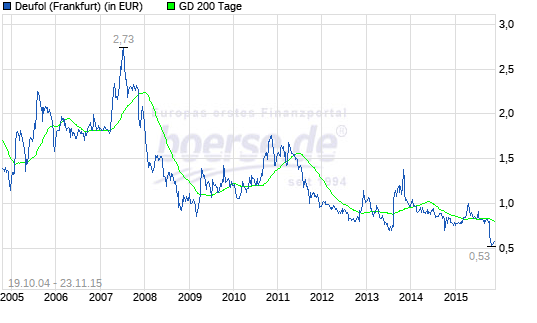

137. Deufol SE – ISIN: DE000A1R1EE6

48 mn EUR market cap logistics/packaging company. Optically cheap (P/B < 0,5), but shrinking top line and high debt. Very low profitability. Stock chart indicates terminal decline risk:

Not sure if there is a puff left in this cigar butt. “Pass”

138. Uzin Utz AG

270 mn market cap “Mittelstand” supplier for the construction industry. Currently nice growth and significant non-german business (2/3). OK margins and currently nice growth. Some financial debt but return on capital not so great (below 10%). “pass”.

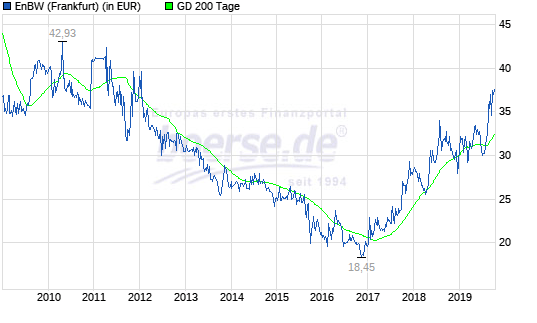

139. EnBW AG

10.7 bn market cap regional utility. Stock price is on a nice recovery since 2 years:

However, company is majority owned by Government entities which for me is a direct reason to “pass”.

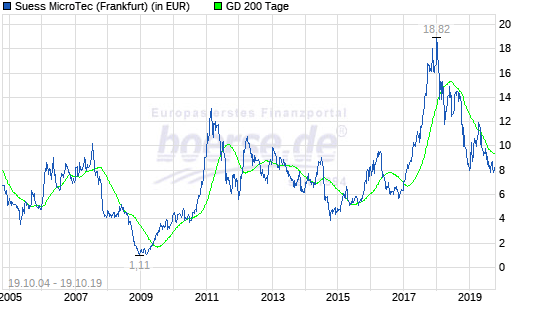

140. Suess Microtech AG

162 mn EUR market cap supplier to the semiconductor industry. ~68% of the sales are actually in Asia. Profitability is very volatile but on average quite low. (EBIT margin between 5-8%). Financially solid with net cash and high free float make the a potential take over target. However, almost now shareholder value has been created over the last 2 decades:

141. Nynomic (ex M-U-T) AG

97 mn market company active in measuring technology.. 15% EBIT margin in 2018 looks promising. However the first 6 months saw a pretty drastic reduction in sales without a really good explanation. All in all still a candidate to “watch”

142. Plenum AG

8 mn EUR market cap consulting company with low profitability (EBIT margin 5%). “pass”

143. OAB Osnabrücker Anlagen- und Beteiligungs-AG Aktie ISIN: DE0006864101

0.5 mn market cap shell company. “pass”

144. Elumeo SE

5 mn market cap company selling (cheap) jewellery. Scandal stricken company / management. Maybe some remaining entertainment value but “pass”.

145. TAG Immobilien AG

“Legendary” German smallcap. Initially a tiny regional railway company near the beautiful Tegernsee, the company morphed into a pretty substantial 3.1 bn EUR market cap real estate company. Run for a long time by fincancier Rolf Elgeti, who resigned in 2014 after some shady real estate deals he did on the side. Elgeti is still Chairman of the supervisory board. However, I am not a big fan of real estate companies and the stock trades 20% above NAV, so for me a “pass”.

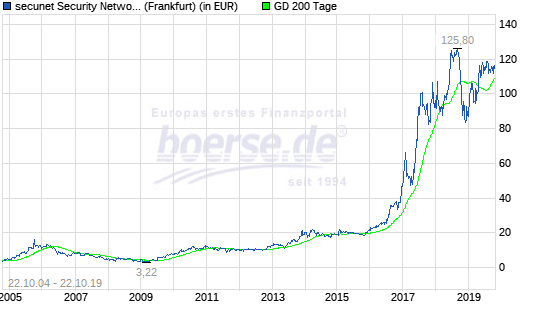

146. Secunet AG

Secunet is a 764 mn EUR market cap IT/security company focusing on the public sector in Germany. Products include everything from cryptographic encoding to automated border control systems. The company is growing nicely and margins are Ok (15% EBIT margin). The company is conervatively financed (significant net cash). On the downside, >75% of the stock is owned by Gieseke & Devrient since 2009 who might have a limited interest in a higher stock price as they might want to fully own the company at some time and the valuation is clearly not cheap (close to 20x EV/EBIT). The chart shows that up until 2017 not much happened and then the stock quintupled:

Nevertheless a stock to “watch”.

147. InflaRx NV

62 mn biopharma company with a Nasdaq listing only. The company IPOes in 2017. A few months ago it turned out that one of their products didn’t work and the stock dropped -84% on one day. Cash and securities is significantly higher than market cap but the company has no revenues and burns around 12 mn eqach quarter.

I guess this could be something for an activist but for me it is a “pass”.

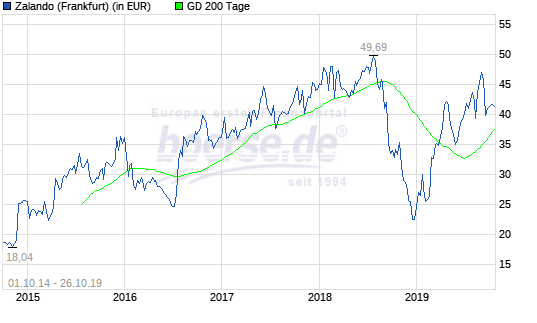

148. Zalando SE

Zalanda is with 10.5 bn market cap clearly one of the most successful German “New economy” companies. Part of the Rocket internet story, zalando is still growing at around 20-30% and plasn to do so for some time. Largest shareholder is still Kinnevik with ~26%- Late 2018 I was actually tempted to buy the stock as they suffered during the market downturn:

The stock had dropped more than -50% and looked decently valued. Now however at around 45x EV/EBIT I think the upside for the next few years is pretty much priced in. As in my opinion it is a good company and future opportunities might come, they are for me a stock to “watch”.

149. NanoRepro AG

Tiny 5.7 mn market cap company developing and selling test kits for HIV and other areas. Loss making and decreasing sales, remaining cash will be exhausted soon. Strong “pass”.

150. Verbio AG

560 mn market cap producer of bio fuel (diesel, ethanol, gas). The FY year ending on 30.06.2019 saw a 13% increase in sales and a a dramatic increase in profitability (~400%). Based on the last year the stock is moderately priced. The balance sheet is super solid, all equity financed with no debt. This is a company which is a clear “watch” candidate.

RWE ist a large holding for Exor. Wonder what they see there.

By the way, it’s in the Exor letters what they thought about RWE.

Tx 4 sharing