All German Shares Part 20 (Nr. 401-425)

Another 25er batch of German stocks based on my random selection criteria. This time the result are 3 new entries into my watch list.

401. Kampa AG

Insolvent “zombie” stock. Pass.

402. Dinkelacker AG

A 480 mn market cap former brewery that transformed into a real estate company focusing on the region around Stuttgart. Very small free float, not my cup of tea, “pass”.

403. Bavaria Industries AG

Bavaria industries Ag is a listed PE company valued at 273 mn EUR_ The company started out as many similar ones with “1 EUR” purchases, i.e. buying quasi insolvent companies for 1 EUR and trying to turn them around. They were lucky with some early successes. More recently however after some exits, the company switched into listed equities and now seems to be more a family office for the founder who controls a large amount of the share capital. The majority of the portfolio was in cash, therefore the stock price only moved a little bit since the beginning of the crisis. Although they showed good foresight with their conservative approach, for me it is still a “pass”.

404. YOC AG

YOC AG is a 9 mn EUR market cap mobile advertising company. The company is however unprofitable and has negative equity. Not a good position to go into a crisis that will see a drastic fall in ad revenues. “pass”.

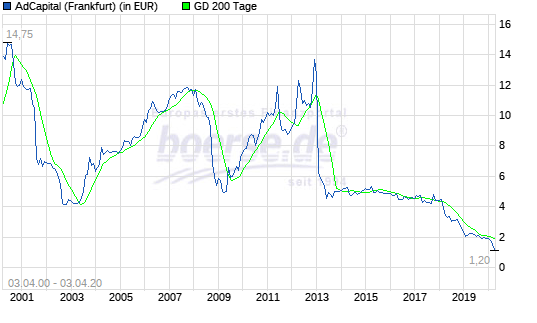

405. Ad Capital AG

Ad Capital is one of many listed “holding” companies with a market cap of 16.8 mn EUR. The company has seen better days as the stock price shows:

The portfolio didn’t perform well in 2019, therefore again, going into a crisis will be very difficult and I guess this is reflected in the current share price. “Pass”.

406. Pittler Maschinenfabrik AG

4 mn machinery company which seems to be loss making and reports infrequently. The have been in liquidation (or still are). “pass”.

407. HumanOptics AG

HumanOptics AG is a 34.5 mn EUR market cap specialist for eye implants (lenses). That sounds interesting but the company is stagnating and only losses and financial debt are increasing. Nothing to see for me, “pass”.

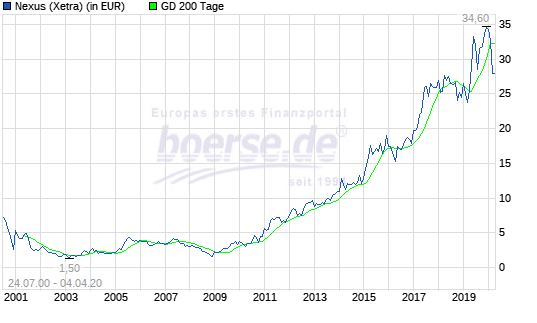

408. Nexus AG

Nexus is a 443 mn EUR market cap software company that specializes in solutions for hospitals. Looking at the history of this very young company, it clearly seems to be some kind of “hidden champion”, showing very nice growth over a long period of time.

Looking at the long term chart we can see that after its IPO in 2001, nothing happened for a long time until the stock started on a pretty impressive growth trajectory after the GFC:

Based in trailing earnings, the stock is not cheap, despite the recent drop: With around 10 mn earnings in 2019, Nexus trades at a trailing PE of 40.

“Under the hood”, things look slightly better; The company produced around 17 mn fre CF and has around ~26 mn EBITDA (adjusted for capitalized development). This translates into an EV/EBITDA of ~16 which is not too bad for a good Software company. The company bought the majority of IFA Systems in 2019 which seems to have been a pretty decent acquisition. Interestingly, the company doesn’t seem to have a dominating shareholder. Management owns ~5%.

What I really like about the company that they have positioned themselves also quite well in the tele medicine area which is of course now booming like crazy.

Nexus is a very interesting candidate. I will “watch” the stock closely and hopefully have a deeper look at it soon.

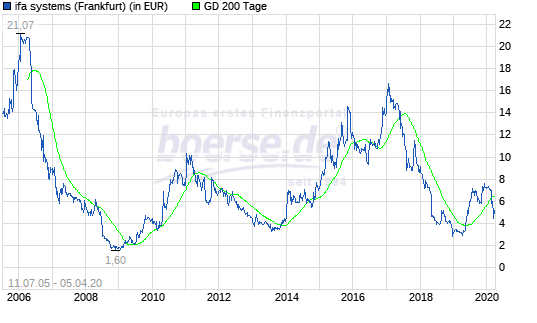

409. ifa Sytems AG

ifa systems is a 13.9 mn market cap software company that specializes on oculists and has created a specialized health record for their patients. In 2019, Nexus AG acquired around 53% of ifa systems. The company had very rough years esp. in 2016 and 2017. Historically, IFA seems have to capitalized a lot of development costs that then had to be written in off in 2017. The stock price clearly shows the issues:

Interestingly, after the majority acquisition by Nexus (from a company called Topcon), they announced a significant one time licensing agreement for their database which will result in a very good 2019 result. It will be interesting, how the company will perform going forward with the new owner, therefore it will go onto the “watch” list.

410. Philipp Holzmann AG

Many years ago, this was Germany’s biggest construction company. Now it is a bankrupt “zombie stock”. “Pass”.

411. Horus AG

Horus AG is a 1.3 mn EUR Nanocap, majority owned (~80%) by Scherzer AG. “Pass”.

412. vpe Wertpapierhandelsbank AG

Munich based “Globally active” bank with a 3.1 mn market cap. Company is loss making and had to rasie capital in 2019. “Pass”.

413. GTG Dienstleistungsgruppe AG

Another insolvent Zombie stock. “Pass”.

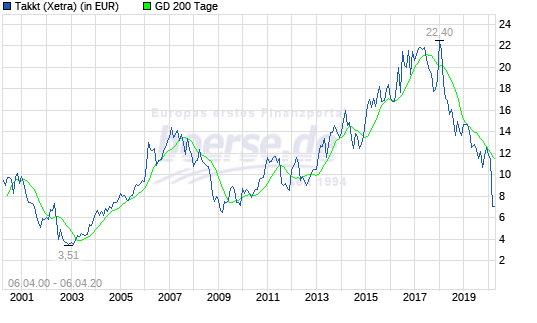

414. Takkt AG

Takkt is a 465 mn EUR market cap B2B Distributor of office equipment. The company has been hit super hard by Covid-19 but was already on a downward trend since 2017/2018 as the stock chart shows:

According to the 2019 results presentation, organic sales decreased by -1.4% in 2019 and net profit by -10%. Especially the Quarter in quarter trend is worry some. From +5% sales growth in Q1, Takkt slipped to -7% in Q4 with no real explanation, other than a strong exposure to German car manufacturers.

The company, which seems to have run their units quite independent now seems to transform into a more centralized structure. In my experience, these kind of restructurings are often a sign of weakness. Takkt is majority owned (50%+) by Haniel, a troubled German conglomerate. Nevertheless I will put Takkt on “watch”, as the valuation with an EV/EBITDA of around 5 looks cheap. However it needs to be seen if the home office trend has negative effects.

415. Zoologischer Garten Berlin

This is the second Zoo in Germany (besides Munich) which has a listed stock. The company has a market cap of 28.1 mn EUR and has performed quite well over the last few years. The Belrin Zoo seems to be quite profitable, however based on the articles of association, profits are only allowed to be used for the Zoo and shareholders have no right whatsover. However, being a shareholder seems to entitle the right to buy a lifelong ticket for a price of 575 which includes 2 relatives. With a regular cost of ~100 EUR per year, Belrin residents need to calculate if this justifies the price of around 700o EUR for the stock. For me it is a “pass”.

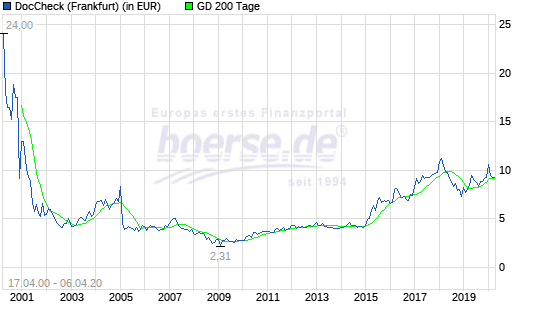

416. Doccheck AG

Doccheck AG (the former Antwerpes AG) is a 49 mn EUR market cap Healthcare marketing company and healthcare professionals “Community”. The founding family owns 71%, free float is only 20%. The company has net cash and the business as such seems to be quite profitable (EBIT Margins >10%). In 2018, the company stagnated, however in the first 6 months 2019 they returned to growth and preliminary numbers for 2019 looked pretty strong. In the beginning of March, The company announced an official share repurchase tender at 10 EUR per share, but pulled it 2 weeks later due to Covid-19. The stock price reflects this a little bit but other than that remained remarkably stable:

I personally find the company very interesting and put it on “watch”.

417. KHD Humboldt Wedag International AG

KHD Wedag is a 71 mn EUR market cap holding company. The company is popular among “deep value” investors as it has a rather large cash position, however the company is loss making and is part of a Chinese conglomerate which has accessed the cash already via an inter-company loan. “Pass”.

418. ERWE Immobilien AG

55 mn market cap company that started out as a Technology investment company that transformed into a Real Estate company. “Pass”.

419. Readcrest Capital AG

1 mn market cap company with frequent name changes. “Pass”.

420. Snowbird AG

Defunct former German-Chinese fraud. “Pass”.

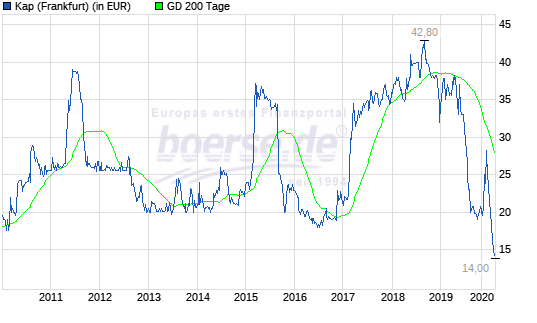

421. KAP Beteiligungs AG

KAP is a 113 mn market cap holding company with activities in diverse areas. In a surprising move, US PE giant Carlyle bought a majority stake from the founder who wanted to step back. Looking at the stock chart, this might not have been the best investment ever for Carlyle:

The company turned into a loss position in 2019. Carlyle seems to have reduced their stake but still own 45%. The company warned that Covid-19 would be a major issue for them. Overall this looks like a low margin turn-around case which is not my preferred kind of investment and might get into real trouble in 2020. “Pass”.

422. Private Assets AG

A 0.4 mn EUR market cap nanocap with little or now active business. “Pass”.

423. I:fao AG

I:fao is a 143 mn EUR market cap software company that specializes in procurement of business travel for businesses. The company is 88% owned by Amadeus IT, the Spanish GDS and only has a “pink sheet” listing in Germany. Initially, Amadeus planned to merge with I:fao and squeeze out minorities, but this has been canceled recently. The company doesn’t issue reports anymore. As a minority shareholder, i:fao doesn’t look very attractive, so “pass”.

424. BBS Kraftfahrzeugtechnik AG

Bankrupt company shell. “Pass”.

425. McKesson Europe AG

This is the former Celesio, which, after the take over by McKEsson has been delisted and now is only traded on the “Pink sheets”. The company has a profit transfer agreement with its shareholder, so shareholders only are entitled to 0,83 EUR dividend and maybe some extra money if a squeez out at some point in the future will happen. This is something for speciailsts, for me it is a “pass”.

Yes, there is a huge amount of crappy stocks listed in Germany. Yes, I’ll keep a list of the companies I’ll watch. For better supsense, I’ll publish the list at the end…..

But you do not have any ratio (watch:pass) just yet, right?

~20% of the stocks on average went on watch, however with different priorities

Very little success stories among small companies Our friend Galloway would say this is a catastrophe and a consequence of the excessive monopoly & power of the blue chips and the lack of competitivity of small fish in the ocean. I would mostly agree (Probably he is 80-85 % right). 😦 !!

Well, at least for the German market this would be the wri´ong conclusion. Despite the many “Small Crap” stocks, the smaller inideces (MDAX, SDAX, Techdax) have outperformed the DAX by a wide margin over the past years.

Quite astonishing how many micro caps and shell companies there are in Germany (not the country of common shareholders 😀 that is [sadly] for sure!)

Do you keep track overall (sorry if you linked it in some prioir part)? From the 425 how many got a pass, watch ?

Best, s4v

Micro crap’s