All German Shares Part 24 (Nr. 501-525)

Another 25 randomly selected German stocks including four stocks this time who made it onto my “watch” list:

501. Fair Value REIT

Fair Value is a listed REIT with 104 mn EUR market cap. The portfolio includes a >50% share of retail objects which will be extremely challenged. The stock price has dropped a little but not much. “pass”.

502. Fortec Elektronik AG

Fortec is a 49 mn EUR market cap distributor / developer of electronic components. Sales have been stagnating even before the Covid-19 crisis and EBIT has declined significantly in the first 6M of the current FY. Although the company looks cheap and is relatively solid from a financial point of view, I don’t “warm up” to the company and the business model. “Pass”.

503. Hasen Immobilien AG

Hasen Immobilien is a 105 mn ER market cap real estate company. The company is a more “old school” real estate company which is not aggressively revaluing its portfolio, profits therefore look modest. 92% of the shares belong to the Inselkammer family who made their money with breweries and still runs a tent on the Oktoberfest. One of the few potentially interesting real estate companies in Germany, but still for me a “pass”.

504. GSW Immobilien AG

GSW is a 4.6 bn residential real estate company which is majority owned by Deutsche Wohnen. GSW shareholders only are entitled to a guaranteed gross dividend of 1,60 EUR due to a profit and loss transfer agreement. “Pass”.

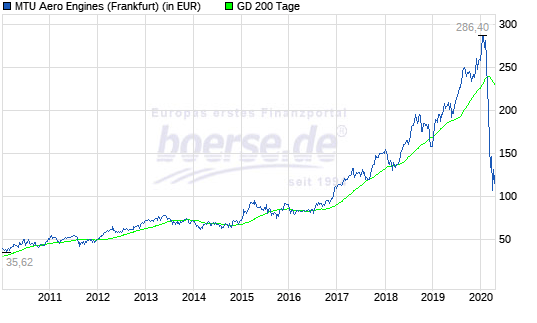

505. MTU Aero Engines

MTU is a 5.8 bn EUR market cap manufacturer of airplane jet engines. As with many other similar aerospace companies, the story over the last year was always the same: There is only one way demand goes which is up up up. Well, now in a post Covid-19 world, it is pretty clear in hindsight that this was too optimistic and paying very high multiple based on very long term growth projections is risky. The stock chart shows how MTU outperformed and then got hammered:

Part of that outperformance is also clearly driven by the fact that MTU has become part of the DAX in September 2019.

The stock now trades ~13x 2019 P/E. The company enjoyed great EBIT margins (16%) in the past which to my understanding are mostly driven by aftermarket services.

At the moment, no one knows how a “new normal” looks for the Airlines and when this new normal will kick back in. On that basis, I don’t think that MTU looks very attractive at this level, nevertheless it is a stock to “watch”.

506. Valora Effekten Handel

Valora is a 2 mn Nanocap, however in principle the company would be interesting: They specialize in market-making for non-listed stocks (grey market). With the change in regulation, de-listing has become quite easy in Germany, therefore their market should expand. Unfortunately this doesn’t show in the numbers. Additionally, there seems to be a pretty dirty fight ongoing between the company and the infamous “Reich Gruppe”, who are one of the shadiest actors in the German stock market (to put it mildly). therefore I’ll “pass”.

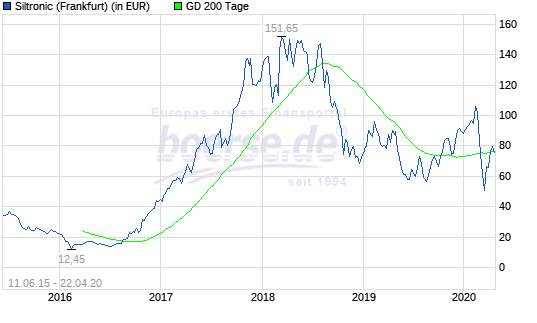

507. Siltronic

Siltronic is a 2.3 bn market cap company that is one of the leading producers of silicon wafers that are used top produce computer chips and processors. The business is capital intensive and volatile which leads to significant fluctuations in the stock price:

Depending on the timing you could realize a 10 bagger from 2016 to 2018 or lose more than -60% even before the crisis. The company was initially a subsidiary of Wacker AG, a German chemicals group but Wacker has sold down and is only keeping 30%.

The stock looks cheap with a P/E of 10, but profits and sales were already on their way down in 2019. Maybe something for traders, but for me it’s a “pass”.

508. Mainova AG

Mainova is a tiny regional utility with a market cap of 28 mn EUR. Freefloat is super small (0,3%) and the majority is owned by the city of Frankfurt. “Pass”.

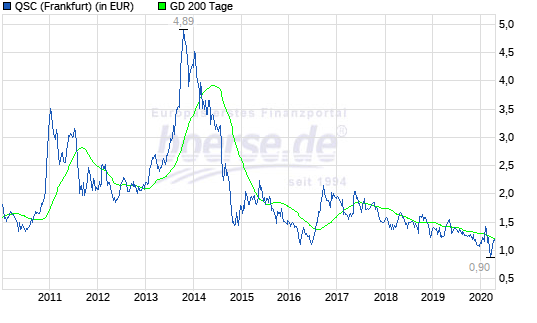

509. QSC AG

QSC is a 142 mn EUR market cap Telco service company that tries to reinvent itself into a IoT/Cloud/Big Data something. The company sold its core Telco Business in June 2019 and is sitting on significant cash (70mn). The two founders own ~25%

The remaining company has 120 mn EUR in sales. The remaining business is EBITDA negative but should be close to neutral after fully concluding the sale according to Management. Going forward they want to use the cash pile to grow the business including M&A. The stock market doesn’t seem to believe the story:

However I find it a potentially interesting situation and put it on my extended “watch” list.

510. Effecten Spiegel AG

Effecten Spiegel AG is a a “classic” for any German small cap investor. The company runs a small stock tip magazine and has invested its equity in listed stocks. The founder and former owner was an “eccentric” guy. I didn’t follow the company for a long time but a quick look shows that the capital allocation abilities seem to be “limited” and the curren ~20% discount to NAV seems to be justified. For someone with a lot of time this could be an interesting special situation, but for it is a “pass”.

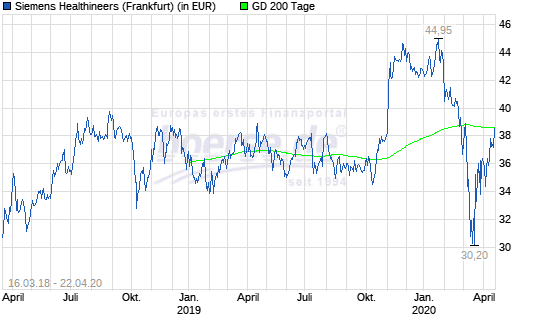

511. Siemens Healthineers

Siemens Healthineers is a 37.6 bn IPO/spin off from Siemens and comprises the healthcare business of Siemens. Siemens still owns ~85% of the company. The stock price has performed Ok but no great since the IPO. The stock had a good run end of 2019 but that was stopped by the crisis:

In 2019 they achieved +6% top line growth and net incoem growth of +24%. The company trades at around 24x 2019 PE. The major part of the business is medical imaging which I would call “Hardware” healthcare business which I don’t like that much. Personally, I am also not such a big fan of “pseudo” listings within a large conglomerate therefore I’ll “pass”.

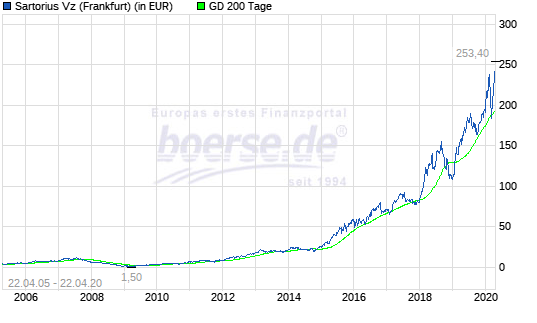

512. Sartorius AG

Sartorius is maybe one of the biggest growth stories in the German stock market ever and I have to admit that I never had a look at the company. The 19.2 bn market cap Health Care company. The company is growing nicely. Sales doubled from 2015 to 2019 as well as EBITDA. EBITDA margins are in the high twenties. The long term stock chart looks insane:

On the other side, the current valuation is an implied P/E of 100x which looks “rich”. The value creation seems to have happened in their French listed subsidiary Sartorius Stedim Biotech, in which Sartorius owns 75% and which is valued at 20 bn EUR. Sartorius Stedim was created in a merger in 2007/2008. If I understand correctly, the company offers the “shovels” for Biotech companies which looks like a good business considering the current boom in Biotech. If I would have more time, I would try to dig into old reports to see if there would have been a chance to spot this crazy value creation at some early point in time. Other than that, it is unfortunately a “pass”.

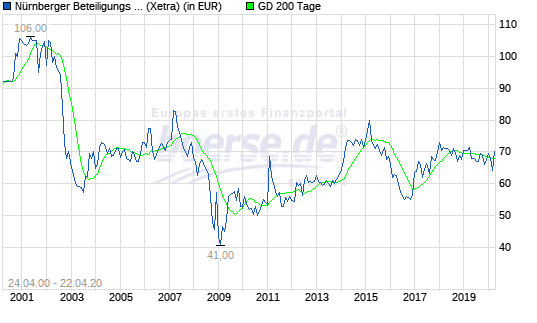

513. Nürnberger Beteiligungsgesellschaft AG

Nürnberger is a regional diversified insurance company with a market cap of ~800 mn EUR. The company always looked cheap but the long term chart shows that they failed to create value over the years:

On the plus side, the stock reacted very little to the crisis. As many other smaller insurance companies, Nürnberger is struggling with diminishing investment returns and increasing costs. The 2019 result for instance is lower than 2001-2013 despite a significant larger balance sheet. A specialty of Nürnberger is that the main shareholders are other insurance companies, among them Munich Re, DaiIchi Life and state owned Bayerische Versicherungskammer. This special construction seems to secure independence but clearly does not create a big incentive to create value on top of dividends. “Pass”.

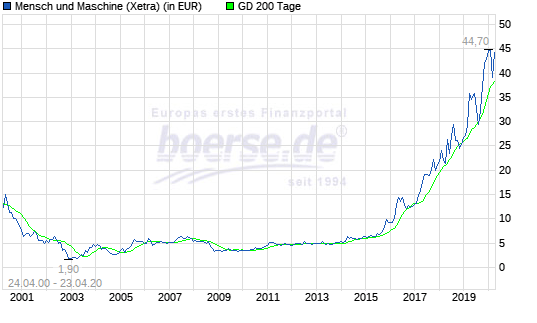

514. Mensch und Maschine AG

Mensch und Maschine is a software/IT services company active mostly in CAD/CAM tools. The company is one of the few “Neuer Markt” hype companies that did not only survive but especially in the past few years showed impressive growth. The stock price shows that in between there was a long time where nothing happened:

Since 2015, the stock went up by around 10x. Especially 2019 was a blockbuster year with top line +33% and profit +43%. Even Q1 2020 still looked very good. As far as I understood, the switched from selling licenses to SaaS 2 years ago. Software is around 1/3 of the business and of course more profitable.

The clients are mostly industrials (2/3), the rest is construction and landscaping. At first sight this looks like an interesting company. On the other side, their client base will suffer, but automation will clearly continue. I think MuM is worth to put on the “watch” list although the stock doesn’t look cheap-

515. Isra Vision Parsytec AG

Isra Vision Parsytec is a 65 mn EUR market cap company that is majority owned by Isra Vision and only has a “pink sheet” listing. The company has gone “dark” and only issues minimal reports. “pass”.

516. Isra Vision

Isra Vision itself is a 1.1. bn market cap company that specializes in optical sensors and software for optical quality control. Recently, the company received a take-over offer from Atles Copco for 50 EUR per share where the stock currently trades and this despite (or because) the company was struggling recently. I never liked the company as earnings quality and cash conversion were not good (main issue aggressive capitalization of R&D). I am not sure why Atlas Copco paid this price but maybe I just don’t understand the technology. Anyway, a “pass”.

517. Neuhof Textil AG

Neuhof is a 2 mn EUR market cap company with very little information available. The company seems to have been insolvent a few years ago. “Pass”.

518. DGH Deutsche Grundwert Holding

A 0.6 mn market cap real estate developer with several prior name changes. “Pass”.

519. Alno Aktiengesellschaft

Alno is a 5 mn EUR market cap company that is (still) one of the leading manufacturers of kitchens for residential dwellings. The company however is struggling for many years and the listed entity is insolvent. The operating business these days seems to belng to someone else. “pass”.

520. TC Unterhaltungselektronik AG

Another Zombie company with a 0.5 mn market cap. Somehow they are still active and try to do something with Blockchain. “Pass”.

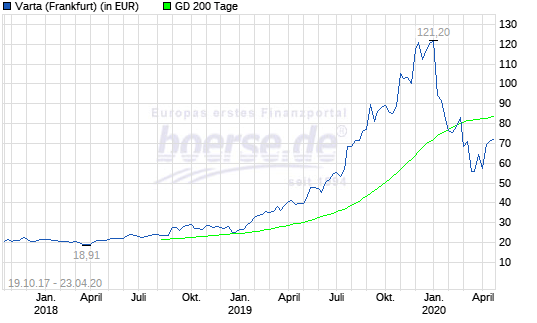

521. Varta AG

Varta is an interesting stock. The company used to be a super boring producer of consumer batteries that was taken over in the 2000s and the operating business was sold. Then, in 2017 Varta went public again and became a “Hot” battery play that is now valued at 2.9 bn EUR. there seems to be a project on the way that Varta might benefit from a German/Euopean push to start battery production for EVs in Europe.

The company could grow top line in 2019 by +30% and EBITDA almost doubled. Despite a -50% setback from the peak, the stock is still up around 4 times since the IPO:

The company is still majority owned by Montana Tech Components, a Swiss conglomerate run and owned by Austrian Billionare Michael Tojner, who also founded online betting company bwin. He seems to have bought the operating bsuiness in 2007 for 30 mn EUR. In his home country Austria however, he has a lot of negative publicity on a few real estate deals and his company seems to have been searched by authorities.

He seems to be a really “interesting character”. Although the company trades at 60x earnings, I still think it is a company worth to “watch”, but maybe form a safe distance for some time.

522. Mediqon AG

Mediqon, the former Medical Columbus is 11 mn EUR market company. The company has itself transformed ito a holding company that invests in small software companies. Although there were some issues with earn out payments in the recent past, I still think that it is one of the more promising German micro caps and have therefore added it to my “German Basket”. “Watch”.

523. DLB Anlageservice AG

DLB is a holding company that invests in liquid German small cap stocks. Although the market cap iof 3 mn EUR is only 50% of the NAV at year end, it is still a “pass” for me.

524. Pantaflix AG

The 18 mn market cap company was briefly hyped as the German answer on Netflix. The reality is that it is a crappy loss making business. “Pass”.

525. Steilmann SE

I am not sure but the insolvent Steilmann SE has maybe set a record from IPO to insolvency in only 4 months from November 2015 to March 2016. As often in Germany, the particpating banks (Oddo Seydler, IMI) took no responsibilities and there were no real fines for this. “Pass”

what do you think of varta nowadays?

The stock is much too speculative for me…