All Swiss Shares Series Part 4 – Nr. 31 – 40

Another week, another 10 Swiss stocks, this time with one stock to “watch”.

31. Plazza AG

Plazza is a 581 mn CHF market cap real estate company that invests in and around Zurich. The company seems to trade close to NAV and as a rule I normally don’t consider listed real estate as part of my investment universe, therefore I’ll “pass”.

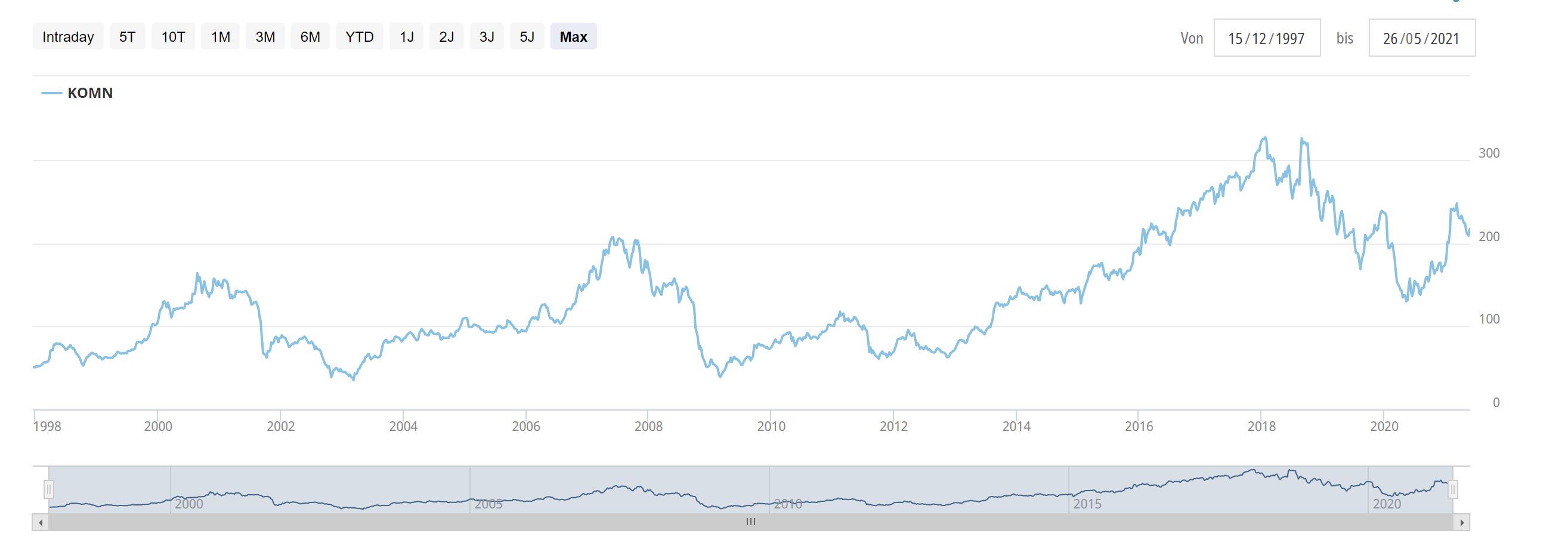

32. Komax AG

Komax is a 831 mn CHF market cap company that supplies cable automation machines to mainly car manufacturers but also the Aerospace industry as well as other industries. As a automobile supplier, business suffered already in 2019 before getting hit again in 2020.

The stock chart shows a significant cyclicality which is not a surprise:

The share price has already recovered despite a relative cautious outlook from Management for 2021 (~10% vs. 2019). In the mid term, the company targets an EBIT of 50-80 mn p.a. Overall, the company looks somewhat interesting but I am not sure if it is the best way to invest into the automobile supplier industry at this stage. Therefore I’ll “pass”.

33. Thurgauer Kantonalbank PS

Thurgauer Kantonalbank is a 2,1 bn market cap local bank which has listed “participation rights” which are similar to a pref share. The share trade at around book value and ~15x P/E, with a dividend yield of 3%. The bank looks super solid, profitability seems to be OK. For yield starved Swiss retail investors, this could be interesting, but I’ll happily “pass”.

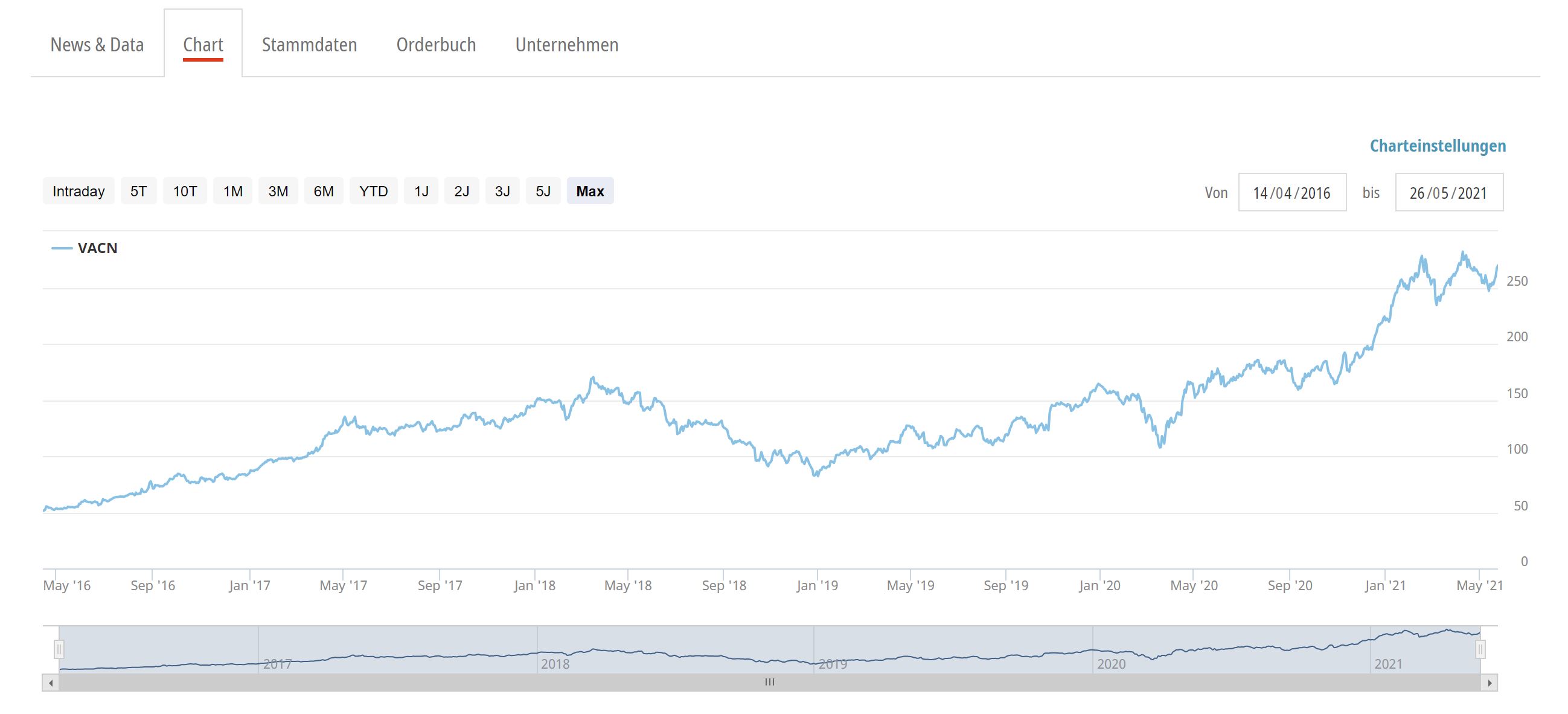

34. VAT Group AG

Vat Group calls itself the global leader in “vacuum valve technology”. The 8.1 bn CHF market cap company enjoys nice margins (31% EBITDA margin) and sells globally mainly to the semiconductor manufacturing industry. Depending on the definition, the company states market shares globally between 50-70% which indicates that this might be a “hidden global champion”.

However the share price indicates that this has been noticed by invetsors already:

The company managed to increase sales in 2020 by more than +20%, net profit by +80%. However at the current valuation, this translates into a trailing P/E of around 60x. The company expects significant “mid teen” top line growth in 2021 although Q1 started a little slow with only low single digit topline growth.

Again, VAT looks like a super interesting company but with a hefty price tag, therefore I’ll “pass” for the time being.

35. Orascom Development Holding

Orascom is a 475 mn CHF market cap company that nominally sits in Switzerland but is mainly a developer/owner of real estate mainly in the Arab world. The annual rpeorts have great pictures from the ressorts but the company has been making losses since 2018. “Pass”.

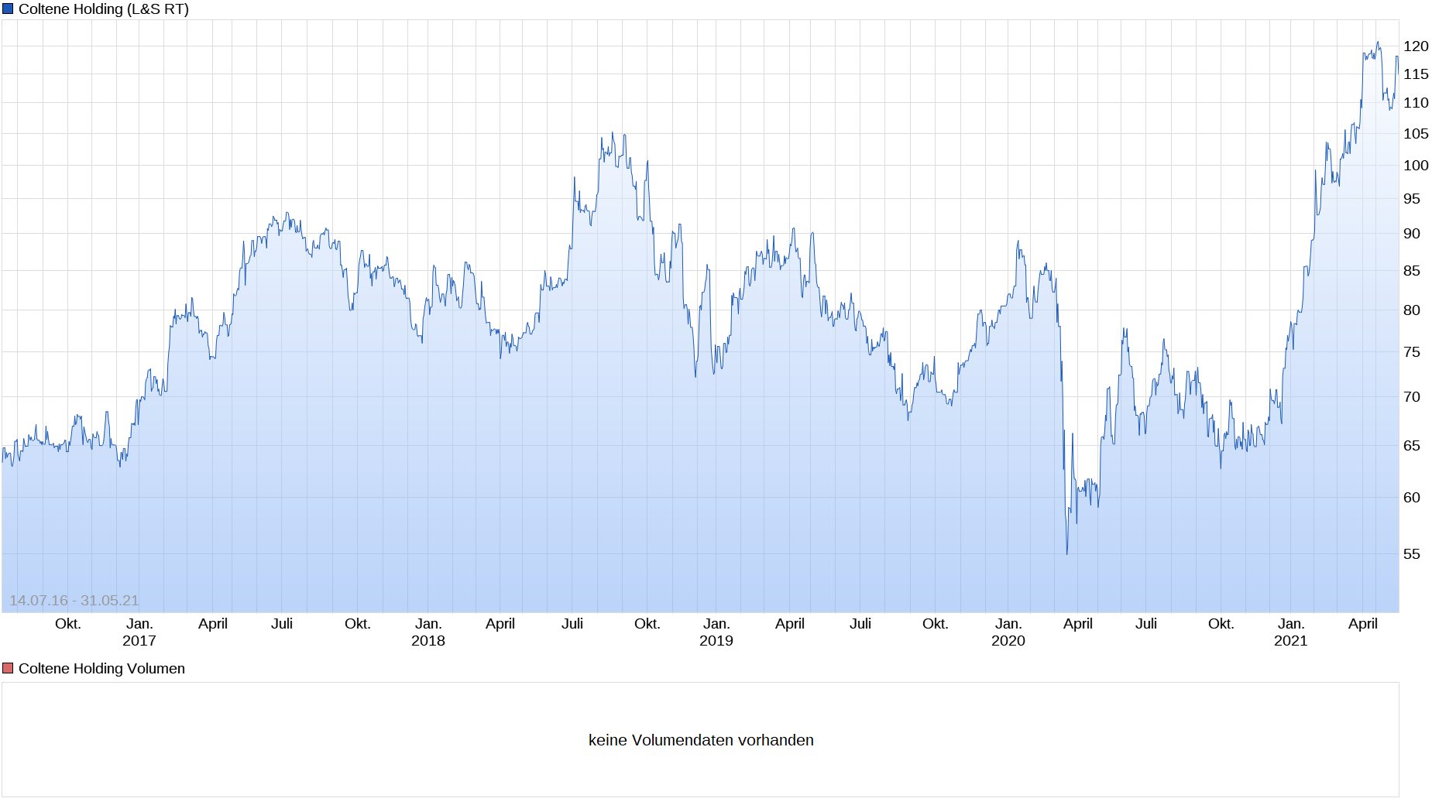

36. Coltene AG

Coltene is a 754 mn CHF market cap company that offers a wide variety of supplies for the dental industry/dentists. The company sells more than 50% of its products in North America. 2020 hasn’t been that good as going to the dentist was not so popular during Covid, but Coltene still managed to generate a profit despite a -10% drop in sales. Profit would have been higher if they wouldn’t have sold a Brazilian sub at a loss.

Looking at the stock price, we can see that the stock has more than fully recovered since March 2020:

At ~120 CHF per share, Coltene trades at around 36x 2019 earnings and this despite the fact that earnings have been declining since 2017. Maybe this has been driven by their “Infection control” segment which could benefit from Covid. Although the business seems to be quite profitable (~12% EBIT margin in 2019), somehow I do not feel an urge to look at this more closely, therefore I’ll “pass”.

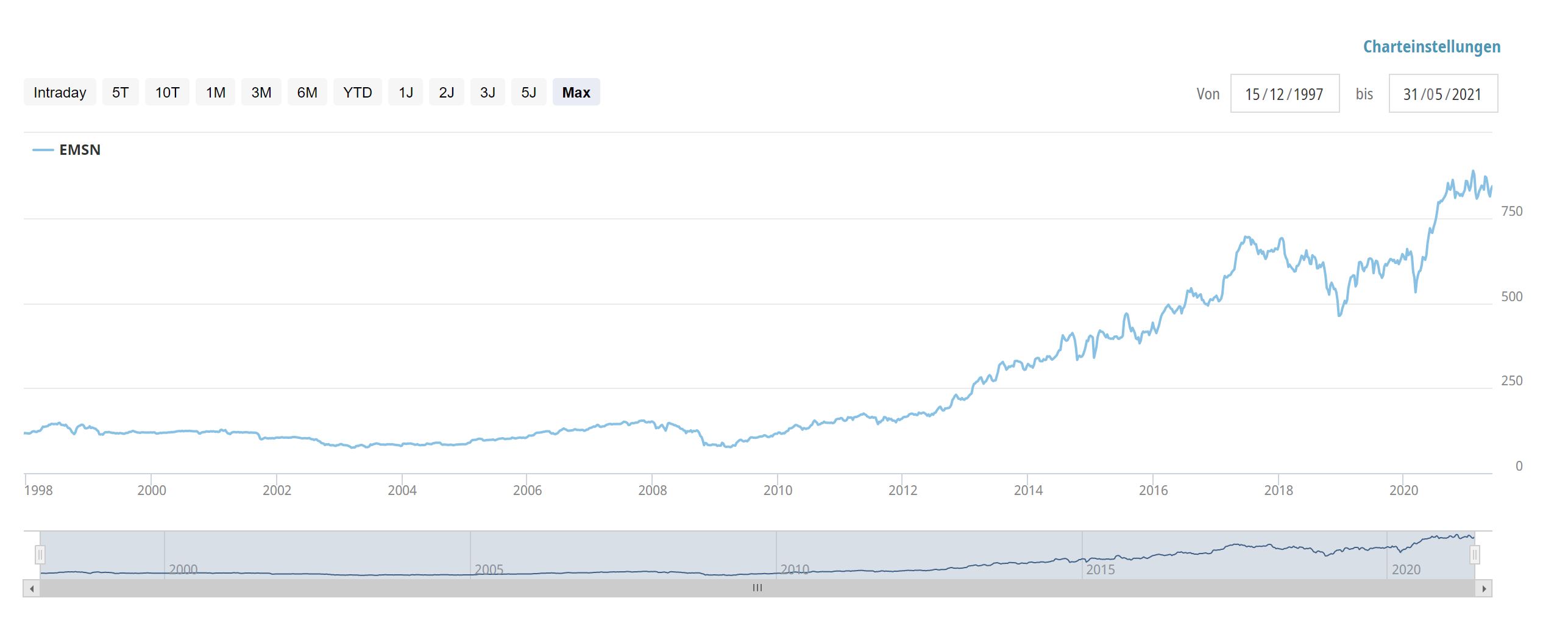

37. EMS Chemie AG

EMS Chemie is a 19.7 bn CHF market cap chemical company with a very remarkable stock chart:

The stock managed to do 10x over the last 10 years. What is also quite remarkable is the fact that they make ~28% in EBIT margin which for a company that produces around 50% of its product in Switzerland is even more remarkable.

The company is majority owned by the Blocher family, the Patriarch Christoph Blocher is a somewhat controversial “nationalistic” politician in Switzerland. EMS managed to more than double its EPS from 2010 to 2020, but the big kick came from a multiple expansion of around 10x in 2010 to >40 these days.

On one hand it would be really interesting to understand how they manage to achieve these results, on the other hand I don’t think that I have the time for this, therefore I’ll “pass”.

38. Perfect Holding AG

Despite its name, Perfect is a 12 mn CHF market cap “Penny stock”. They do something with aviation but is not so clear what it actually is. They don’t make any profit. “Pass”.

39. OC Oerlikon AG

Oerlikon is a 3,5 bn CHF market cap Siwss Industrial Group which is one of the companies where Russian Oligarch Viktor Wechselberg own a significant stake (~40%).

At a first glance, the company doesn’t seem to be very profitable and even on an “adjusted EBITDA” basis things don’t look that good.

As I want to stay away from evil looking Russian Oligarchs, I’ll “pass” without further analysis.

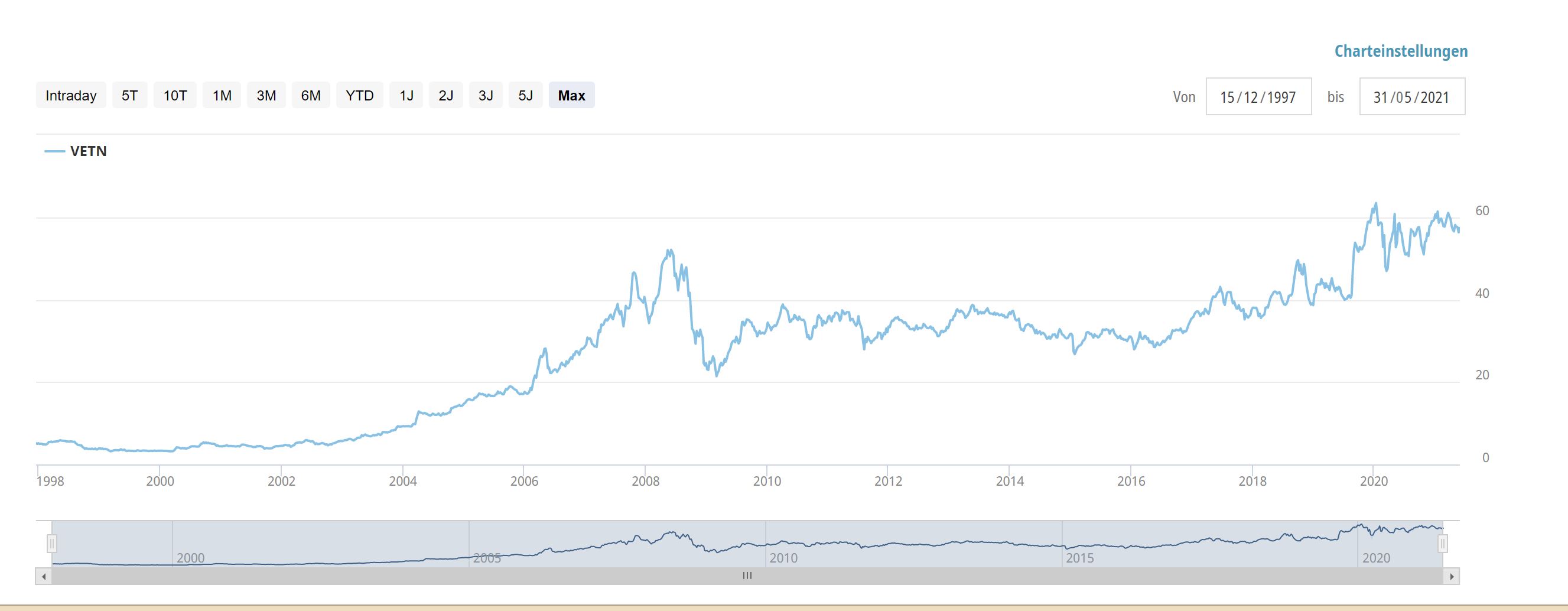

40. Vetropack AG

Vetropack, a 740 mn CHF market cap producer of glass bottles was actually in my initial blog portfolio from 2010 but I sold the shares in 2014. The company was exposed significantly to Eastern Europe, with Ukraine having been its major growth market. Looking at the chart we can see that the stock has performed not that great since 2014:

Vetropack is clearly one of the cheapest stocks in Switzerland. The company is controlled by the Cornaz family which owns close to ~70% of the voting rights, thanks to a A/B Share structure where the privately held B shares have 5 times the voting rights of the A shares. The company trades at around 20x 2019 earnings and manages to deliver double digit EBIT Margins. Return on capital are relatively low but that is to be expected for a capital intensive business.

Nevertheless, the company deserves to go onto the “watch” list for a deeper dive.

Hello memyselfandi007,

Coltene was a decent investment from mid 2019 to spring 2021. The dental business will recover now and has some surprise potential, the infection control unit will just do fine (where they bought 2 companies). The relatively high P/E and EV/EBITDA multiples need to be judged against other peers in the medtech industry. Maybe you want a look to the other 2 swiss companies, which I covered in Nov. 19 on my (German) blog? Looking forward to it!

https://www.covacoro.de/2019/11/15/schweizer-perlen/

Disclosure: Coltene sold in spring 2021 from portfolio and wikifolio, still as quality stock on my watchlist.

Tanks for the comment. I will Look at the other companies but I will strictly follow my random number generator 😉

thanks for your interesting ideas. Can you comment on why you typically don’t invest in listed real estate?