All Swiss Shares Part 9 – Nr. 81-90

Another week, another 10 randomly selected Swiss stocks. This time, 2 stocks might be worth watching.

One quick comment on why I continue to go through all Swiss stocks despite many of the good ones being very expensive: First, I like to finish projects that I started. Second, I think there is always a lot to learn to look at any company, even if it is expensive. And third, there might be a time when stocks become cheaper again and then having a list of great companies might be very practical.

81. SoftwareOne AG

SoftwareOne is a 3,6 bn CHF market cap company that was IPOed in October 2019 at a share price of 18 CHF. Since then, the share price has made little progress at currently 22,50 CHF, considering the run in other software related stocks.

SoftwareOne seems to allow companies to manage their various software applications via some sort of cloud environment. The majority of revenues seems to come direct or indirectly via Microsoft products, their main business seems to be reselling Microsoft licenses which is actually a pretty crowded market.

KKR seems to have been involved only for 4 years or so.

Looking at the P&L reveals that their margins are not very Software like, but rather look like a wholesale business: 7,9 bn CHF in sales only result in ~190 mn EBITDA.

On the surface, the 20xPE looks quite cheap, but around 50% of the profit seem to be poorly explained valuation gains. On the plus side, the company has net cash and seems to be able to run with negative working capital. On the negative side, I actually do not understand what they are actually doing and hwo dependent they are on Microsoft. “Pass”.

82. Cembra Money Bank

Cembra is a 2,9 bn CHF market cap bank that according to their IR presentation is a Swiss only retail bank that offers mostly personal or auto loans and offers credit cards. Compared to other banks, their ROE looks quite healthy, ususally in the range of 15-17%. With a P/E of around 19, the stock is not super expensive. However the chart looks “vulnerable”:

In principle, I do like the simple business model and the clear focus. I’ll put them on “watch”.

83. Zug Estates Holding

Zug Estates is a 930 mn CHF market cap real estate company that invests surpsisingly only in and around Zug. Maybe this could be a hidden bet on Crypto (Zug positions itself as Crypto Valley) but for me it is a “pass”.

84. Tornos AG

Tornos is a 110 mn CHF market cap CNC machinery maker. As such, the business is extremely cyclical. In 2020, sales fell by -50% and the company had to show a loss of -30 mn CHF on sales of 100 mn CHF.

In a good year (2018), Tornos makes 15 mn profits, on average over the fast 5-10 years a lot less. The company has no net debt which is good for such a cyclical business. Maybe it is possible to time a rebound, but for me, Tornos is a clear “pass”.

85. Swisscom AG

Swisscom is the main Swiss Telecom company with a market cap of 21,8 bn CHF and is majority owned (51%( by the Swiss Government.

As many other TelCos, long term value creation has been a problem. The stock price is still below the highs of the DotCom mania more than 20 years ago:

With a PE of around 14,5x and a dividend yield of ~ 45%, the stock looks quite cheap, cheaper than for instance Deutsche Telekom which trades at ~20x PE and 3,4% dividend yield.

The question clearly is if and where any further growth could come from. Market share is >50% for Mobile. As I am not really a fan for TelCos, I’ll “pass”.

86. Zurich Insurance Group

Zurich is a global, 53,3 bn CHF market cap insurance company that is active globally. Compared to the Swiss banks, ROEs look more healthy with 13% for the relatively weak 2020. With a trailing P/E of around 14x, the stock is not too expensive compared to the overall market. Interestingly the stock is still struggling to surpass the highs from “pre GFC”:

Part of this struggle is clearly the fact that low interest rates limit the ability of “non Berkshire” insurers to earn money on their float. Another topic to be cautious about is the risk, that higher inflation often has a very negative effect on P&C companies, especially those active in the “Long tail” business, i.e. insurance where the claims can happen long after the actual time of insurance (e.g. D&O insurance) and assumption on (long term) inflation rates must be made.

In this regard, their Farmers US business is very attractive because they only earn management fees there, but the rest of the business is exposed.

If I would need to invest into a large insurance Group, Zurich would be one of my favorites, but as I don’t have to do this, I’ll “pass”.

87. Straumann AG

Straumann is a 23,4 bn CHF market cap company that is supposed to be a global leader in dental implants and related technology.

A very quick look into the 5 year numbers shows that this is a high quality company with a very attractive business. With the exception of 2020, the business was growing at close to 20% p.a. with EBIT margins of 25%.

Covid-19, after the initial shock interestingly led to a “repricing”:

So instead of 50 times 2019 PE, the stock is now priced at 70x 2019 PE. If the resume growing by 20% p.a., this could be justified. Q1 2021 went into the right direction with sales going up by >30% yoy.

I really like this comany but a PE of 60-70 is just too far away from what I can stomach at the moment, therfore I’ll “pass”.

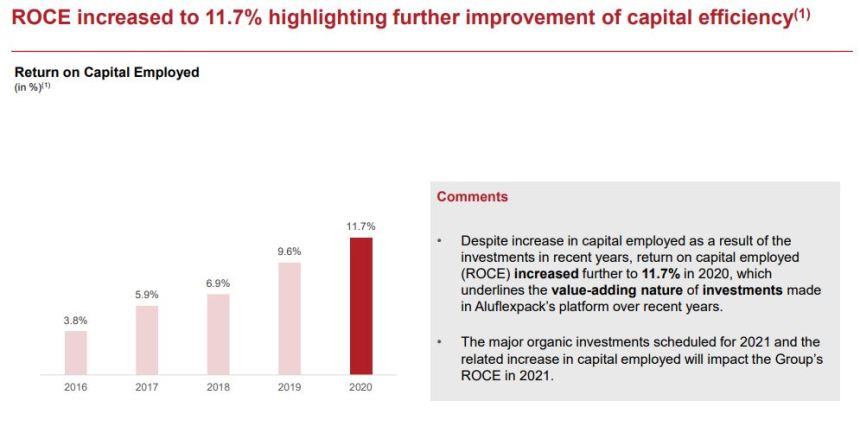

88. Aluflexpack AG

Aloflexpack is as the name indicates a 586 mn CHF market cap company that produces aluminium based packaging. The company is growin at mid teen levels, even in 2020. The company enjoys decent EBITDA margins (15%), however the business is capital intensive which leaves a lot slimmer EBIT and NI margins.

The company IPOed in 2019 and so far it looks like a success:

Interestingly, the company uses no debt. What is interesting is that ROCE has been increasing every year to a current level of 11,7%, which is not great but it seems to keep improving and there seem to be some economies of scale here as this chart shows:

With a PE> 60 and EV/EBIOTDA of 15 however, a lot of growth seems to be priced in. Nevertheless, this could be one to “watch”.

89. Graubündner Kantonalbank

Graub KB is yet another, 1,1 bn regional bank. The stock price is basically a flat line over the last 3-4 years. The stock looks cheap but there is very little growth potential, this rather looks like a bond. “Pass”.

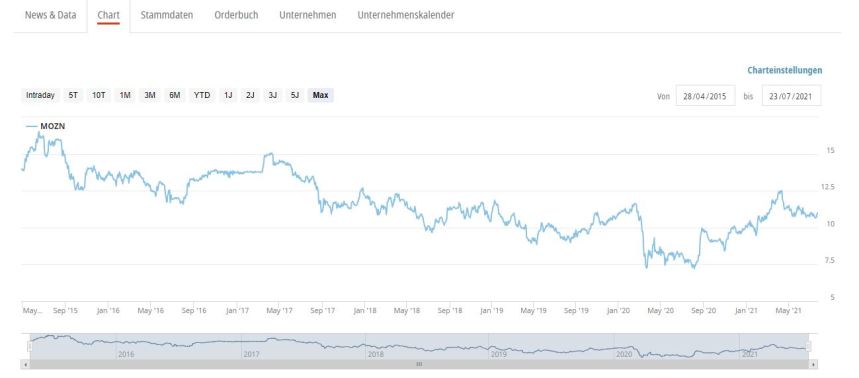

90. Mobilezone Holding AG

As the name indicates, this 490 mn CF market cap company is active in TelCo, among others selling used phones and repairing phones via a own retail network. The company runs a low gross margin business and 2020 saw a -25% profit decrease. Interestingly, around 75% of sales are realized in Germany.

The stock chart looks not very inspiring:

As TelCo is a sector I don’t like that much, I’ll “pass” here.

I know you dont like telcos, but maybe take a look at Telenet – dividend yield is approx 9% and so twice that of Swisscom

On Tue, 3 Aug 2021 at 06:35, value and opportunity wrote:

> memyselfandi007 posted: “Another week, another 10 randomly selected Swiss > stocks. This time, 2 stocks might be worth watching. 81. SoftwareOne AG > SoftwareOne is a 3,6 bn CHF market cap company that was IPOed in October > 2019 at a share price of 18 CHF. Since then, the share pric” >

SoftwareOne is a reseller therefore looking at sales margins is almost meaningless as they pass through the cost of software and only take a small margin. Its actually a very high margin business when you look at Gross profit to Op Profit conversion. And it can also be very high quality. Look at Softcat in the UK as an example although obviously SoftwareOne does not have the same organic growth performance

Well, this would be an argument for many wholesale businesses. For me a “high margin” business, unfortunately, starts at the top with Gross margins.

The difference is that most wholesale businesses have fixed cost of sale component (warehousing, logistics labour, etc) which is a risk if the business suddenly declines in a crisis. Software resellers on the other hand have 0% fixed cost component in their cost of sale. Its pure pass through

Only to a certain extent. On the other hand, wholesale or distribution businesses have often a clear “real moat” because of the infrastructure that can not easily be copied.

I actually don’t really understand why the “pass through” is required at all´, i.e. what the real value add is for these guys.

From my very superficial view I also think that the company is very dependent on Microsoft.

I’m not sure what you mean by “only to a certain extent” – the business models of a distributor and reseller are economically different. One other difference is working capital. Resellers usually run at negative working capital. Distributors have heavy working capital requirements.

Happy to explain the value add if you want. If you are in any doubt that this can be a good business (not saying SoftwareOne in particular is), just look at the SoftCat chart which is all organic btw.

Honestly I don’t even care about Swiss stocks and never bought a single one but your writing makes it really interesting to read, quite a talent. Thanks for writing and keep it up.