All Swiss Shares Part 12 – Nr. 111-120

Half time. With this post I will have covered more than 50% of the 217 SIX listed stocks. This time only one stock made it onto the watch list. Again, I will be on vacation when this scheduled post will be published.

111. Basler Kantonalbank AG

Basler KB is another one of the Swiss regional banks. The listed stocks seem to be “participation” shares only. As the other regional banks, the stock looks cheap with a dividend yield of almost 5%.

However, as the other banks, Business has been stagnating for some time and I don’t see any scenario that looks better. “pass”.

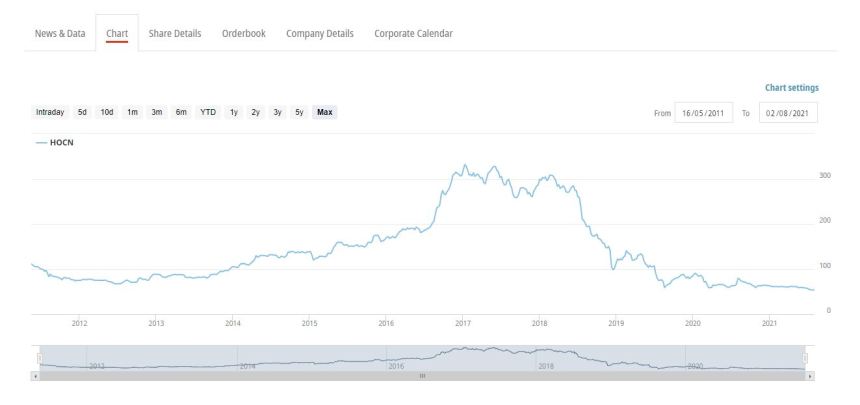

112. Hochdorf Holding AG

Hochdorf is a 115 mn CHF market cap Dairy company that has a surprisingly exciting chart for such a boring business:

The chart of course leads to the question: Why did the share price go up so much until 2017 and what happened thereafter ?

Looking into the 2017 annual report shows a decent increase in slales and a +100% jump in net profits to 40 mn CHF. This seems to have been driven by the acquisition of a company called Pharmalys that is based in Tunesia.

2018 then saw a small decline in sales but a -90% decline in net profit. The compan leveraged up like crazy from 2016 to 2018, issuing more than 400 mn CHF in a mixture of debt, convertible debt and hybrid financing.

In 2019, they sold the Tunesian company for an overall loss of -240 mn CHF. 300 of the 400 mn new debt remained on the balance sheet with little to show.

In 2020, the pain was not over and they still had to write down assets and did not receive the purchase price. Also other recently acquired companies had to be written off and the previous CEO, who wanted to create the next Nestle was finally kicked out.

Hochdorf got a new CEO in December 2019, but he will not have a lot of fun cleaning up the mess. The convertible converted and diluted the number of shares and there is still more than 200 mn CHF debt outstanding at teh end of 2020.

Overall, Hochdorf seems to be a great example how one can screw up a perfectly fine company with over ambitious M&A transactions. “Pass”.

113. Blackstone Resources

Blackstone Resources is a 147 mn CHF market cap company that has nothing to do with PE giant Blackstone. The company seems to have been active in mining and claims now to produce “3D printed batteries” and sells assets for profit which don’t translate into positive cash flow. The founder and CEO holds 67% of the shares. This looks very much like a “promotional stock”. “Pass”.

114. Aevis Victoria SA

Aevis is a 1,15 bn CHF market cap company that describes itself as follows:

AEVIS VICTORIA SA invests in healthcare, hospitality & lifestyle and infrastructure. AEVIS′s main

shareholdings are Swiss Medical Network SA, the only Swiss private network of hospitals present

in the country’s three main language regions, Victoria-Jungfrau AG, a luxury hotel group managing

nine luxury hotels in Switzerland, Infracore SA (jointly controlled), a healthcare-related infrastructure

company, Swiss Hotel Properties SA, a hospitality real estate division, Medgate group (40%), the

leading telemedicine provider in Switzerland, and NESCENS SA, a brand dedicated to better aging.

Covid-19 was obviously not great for a hospital and hospitality business. Freefloat of the stock is less than 20% and the company deploys significant leverage (more than 800 mn CHF in debt). A large chunk of the Hotels has been bought at the end of 2019.

This looks very much like a real estate business. For me it’s a “pass”.

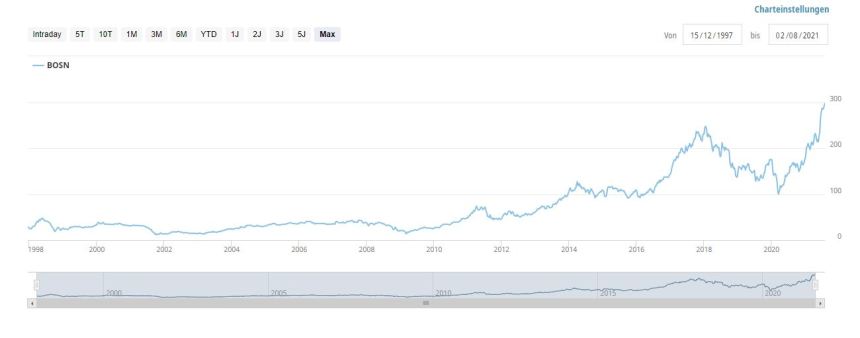

115. Bossard AG

Bossard is a 2 bn CHF market cap fastener technology and logistics company with its headquarters in Zug. A quick look at the chart shows a familiar pattern: Covid-19 propelled the stock after a brief slump into all time highs:

Sales in 2020 declined by -7%, but interestingly, Bossard managed to keep margins more or less constant with EBIT margins at ~11%. ROE and ROCE looks decent at 22% resp. 15%. Based on 2019 earnings, the shares trade at around 30xPE. However, as some other companies, already 2019 saw a decline in profits which explains the dip in the share price already pre-Covid. Somehow investors seem to think that Covid has pushed them back into a growth path.

Overall, this seems to be a decent company, but at the current valuation, there seems to be a lot of upside already priced in. “Pass”.

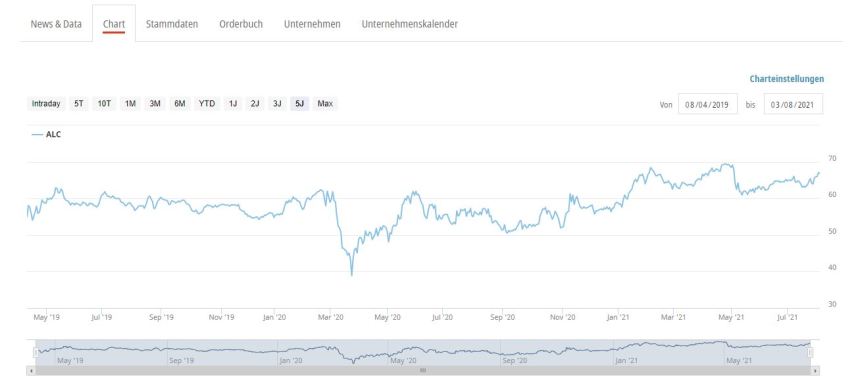

116. Alcon AG

Alcon is a 33,4 bn CHF market cap company that was spun off from Novartis in 2019. The company specializes on eye care. Since the spin-off, not much happened to the share price:

One of the reasons for this is that Covid-19 had a certain impact and under IFRS the company has been showing a loss both in 2019 and 2020.

Believing in “adjusted” earnings, they will do most likely 2 CHF per share in “profits”, resulting in a PE of ~33. For such a large cap company that is already a very “rich” valuation. therfore I’ll “pass”.

117. Luzerner Kantonalbank

Luzerner Kapitalbank is another, 3,6 bn CHF market cap regional bank. At a quick glance, Luzerner seems to be in a little bit better shape than other KBs, but in general these banks do not fit into my search “Pass”.

118. ENR Russia Invest

ENR Russia is a 24 mn CHF market cap investment company that, surprisingly, invests only in Russia.

The stock has lost -75% since 2014 which indicates that the strategy has encountered some issues. The current portfolio consists of a office building, a flower growing business and a parking garage.

Shareholders equity is 50% higher than the share price. In any case, I’ll try to stay away from anything related with Russia, therfore I’ll “pass”.

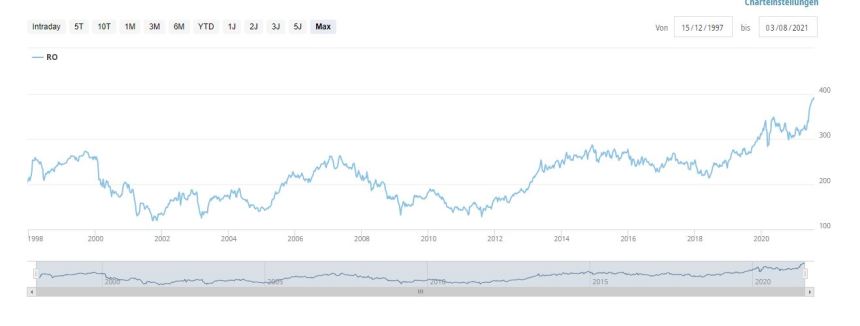

119. Roche Holding

Roche is a 298 bn CHF mega cap pharma / diagnostic giant. During Covid-19, pharma suffered, whereas diagnostics boomed. This resulted in lower slaes but higehr profits. Interestingly, the share price has reached new highs recently:

Assuming EPS of somewhere around 18-20 CHF per year, Roche is clearly one of the “cheapies” in the Swiss stock market. Interestingly, no one other than Softbank (!!!) recently disclosed to have bought a 5% stake in Roche.

Again, same as Nestle, If I would need to invest in Mega Caps, Roche would be a good choice, however I do think that smaller companies offer better opportunities in the long term. “Pass”.

120. Ypsomed

Ypsomed is a 1,9 bn CHF market cap medtech company that manufactures injector and infusion devices as well as insulin pumps. The company seems to be the result of the founder selleing a company to Roche and then byuing back certain activities that form the core of the current Ypsomed business

In the FY 2020/2021, Ypsomed earned 9 mn EBIT. Interestingly they target 100 mn EBIT in the “mid term”. The stock chart doesn’t show a clear trend:

Strategically, there seem to be some interesting developments in the pipeline, such as a collaboration with Eli Lilly to distribute their insulin pumps in the US.

The founder Willy Michel seems to own more than 70%, his son Simon is now CEO. There have been some dealings between Ypsomed and the main shareholder. Overall the founder seems to be a very interesting character. A previous cooperation partner pulled out in 2018.

The company has some net debt. Overall I find the situation interesting and will “watch” how this develops.