Fossil Fuel investments – who to blame for high energy prices ? (David Einhorn, Warren Buffett, ESG)

David Einhorn’s latest quarterly letter is clearly an expression of his frustration. However I wanted to pick out one passage that blames “ESG Investing” for being responsible for high energy prices:

and

So Einhorn blames both, his own under performance and the bad performance of energy stocks (and much more) mostly on the rise of ESG investing and politicians. He is not alone in his opinion that “ESG Investing” is the main culprit for the currently high energy prices.

First counter argument: Jim Chanos from 2013

As a first contradicting “Evidence” I would want to quote Jim Chanos from the year 2013 (!!):

Chanos said his Kynikos Associates fund was bearish on both national oil companies and the integrated majors.

“The costs of finding this stuff (oil) has gone through the roof,” Chanos said. “The economics are clearly deteriorating.”

“It isn’t the same cash flow generating business it used to be.”

Exxon Mobil and other oil producers like it continue to spend heavily not only to find new reserves but also to pay dividends and fund buyback programs, prompting concerns the companies have limited growth potential, Chanos said.

As recently as 2010, Exxon Mobil’s free cash flow, a measurement of cash flow minus capital spending, eclipsed the cost of share buybacks and dividend payouts. Yet executives have been buying back stock at a breakneck pace in recent years. In 2012 the company spent $30.97 billion on dividends and buybacks, with $21.9 billion in free cash flow.

So 8 years ago, when ESG investing was not existing, the Oil majors already preferred to buy back stocks and increase dividends instead of investing into new oilfields tata would create future growth. As a typical time horizon for new development of (offshore) is 8-15 years, cleary ESG investing alone cannot be the culprit.

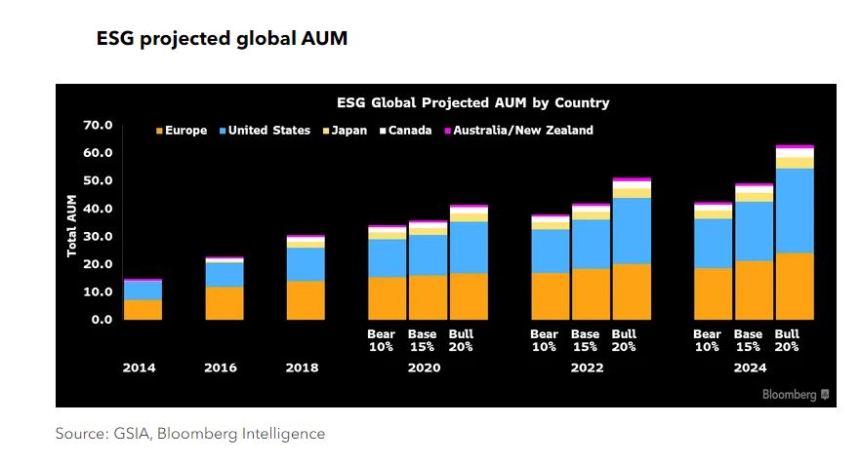

What is the size of the “ESG Market” anyway ?

According to Bloomberg, ESG mandates could reach 1/3 of total AuM in 2025, the historic development can be seen in this chart:

At current ~150 trn total AuM, ESG mandates at them moment comprise 20% of the market, meaning that 80% of the market are “non ESG”. In 2014 this was more like 10%. If current fossil fuel upstream capacity is not enough, this is a result of decisions of 10-15 years ago when ESG investing played little to no role. It is a mirage to belive that the 20% of global assets that run under some ESG mandate now “force” everyone to stay away from energy projects.

Who or what is then to blame ? Maybe Warren Buffett ?

Provocatively one could say that it actually might be Warren Buffett’s responsibility. Ever since he bought See’s Candy in 1973, he kept reiterating that the best businesses need little capital to grow and have pricing power.

Now look at the typical oil company: It need boat loads of capital to grow and has absolutely no pricing power as it produces a commodity with an extremely volatile price.

In the last 10-15 years, even the hard core “Graham” Value Investors (with the exception of Mr. Einhorn) have joined the bandwagon of “Big Tech”. Most Value Investor portfolios look quite similar: Apple, Google, Facebook, Salesforce etc.,, maybe a few Visa or Mastercard positions on top and a legacy Berkshire holding. Even Mr. Buffett himself has made Apple his biggest public holding and not some natural resource company.

By coincidence, Microsoft, Google & Co. also have a relatively low CO2 foot print and that’s why the same stocks liked by “New Value” investors are also often the biggest positions in any ESG related fund. Here is a link to the biggest positions of the biggest ESG funds and, surpise, Alphabet and Microsoft are the top positions.

So to cut a long story short: In my opionion, ESG funds are not to blame for potential underinvestment in the oil and gas industry but the fact that the business model of most natural ressource companies is relatively unattractive compared to Microsoft &Co.

As many other declining businesses. many Oil & Gas companies preferred debt financed share buy backs and dividends in order to keep shareholders somehow happy instead of investing into the future. This is what Jim Chanos identified already in 2013, long before ESG investing had any impact at all.

The same applies also for instance to other capital intensive industries such as insurance.

US Fracking

A great example that capital is not scarce for Oil and Gas is clearly US fracking. Based on a new technology (Fracking) the big problem was that simply too much capital went into fracking leading to too much capacity and too low prices which bankrupted many of the over leveraged fracking players. At the peak of the boom, just a few years ago, actually the big Oil Majors started to buy fracking companies at Fantasy prices. Here is for instance a relatively recent article on how capital was destroyed in the fracking mania.

All of this came a little over a year after investors had begged the industry to stop taking on debt to produce oil that it sold for a loss. This resulted in promises from the industry to do just that and an analyst telling the Wall Street Journal, “Is this time going to be different? I think yes, a little bit.”

It wasn’t different, however, and the industry borrowed more money to produce more oil and gas — and lost more money doing it.

A 2020 report by Friends of the Earth, Public Citizen, and BailoutWatch estimates that the U.S. oil and gas business borrowed another $100 billion in 2020 while Bloomberg estimates over $62 billion in new losses for U.S. shale producers last year. These losses occurred despite U.S. oil production decreasing by approximately one million barrels per day in 2020 compared to 2019. Despite the pandemic, and prices for natural gas being the lowest in decades, U.S. natural gas production only declined 1 percent in 2020.

Let’s face it: Big Oil has an awful capital allocation track record in the past decade or even two and that is in my opinion one of the major reasons for low valuation. Not ESG and lack of access to capital , but destruction of capital at large scale.

Low interest /Discount rates vs. long term growth

This is going to be slightly nerdy but important. One of the big drivers of stock valuations in the past 25 years or so have been decreasing discount rates. All other things equal, a decreasing discount rate (driven by lower risk free rates) increases the value of any cash flow producing asset as its NPV goes up.

But now comes an interesting feature of DCF: The effect is higher for stocks with high long term growth rates because with high lower discount rates, profits in the distant future are much more valuable.

So let’s look an example of two companies who both produce a cashflow of 1 mn USD today and will grow for 3% for the next 10 years. However, company A will continue to grow at 3% in perpetuity whereas company B will not grow anymore (growth rate 0%).

These Cashflow profiles result at a discount rate of 10% an NPV of ~13,5 mn for company A and around 11,7 mn for company B. So the difference in the 3% more growth from year 11 onwards is worth around 2 mn.

Now let’s do the same calculation with a 6% discount rate. Suddenly company A is worth 31.3 mn USD and company B 20,2 mn USD. So that future growth suddenly is worth 11,1 mn vs 2 mn at the higher discount rate.

As the Oil and Gas industry had itself preferred to distribute cash instead of investing ionto future growth I think this DCF effect also explains a lot of the underperformance in the last decade or so, independent of any ESG funds. It’s just pure DCF, nothing else. As I have wirtten before: These companies are cheap for a reason (or two).

Short term vs. long term prospects and conscience

Of course, some Oil & Gas stocks might perform very well in the near future if enough investors are believing that these stocks are a great deal. However I do think that most of them are “fundamentally challenged” and personally I do think that Renewable Energy companies have the better future.

With regard to a “clean conscience”: I don’t think that even ESG investors should fully divest, rather the opposite: ESG investors should support these companies that are doing better than others with regard to CO2. Oil and Gas is needed for some time (and for chemicals for instance forever), so I do think investing into the industry either to press for change or support companies that are doing much better than competitors is a very valid strategy.

However what I don’t like are “phony”investors who for instance claim to be concerned about climate change but then collect dividends from a really dirty producer like Gazprom. This is something I could personally not do and still watch myself in the mirror every morning and with these kind of people I do not want to have any relationship.

Summary:

Overall, I do not think that ESG investing has created a shortage of Oil and Gas. The industry has been simultanously underinvesting (Oil majors) and overinvesting (Fracking) and the Oil & Gas industry has a pretty ugly track record in capital allocation or rather shown all signs of large scale capital destruction.

On top, much more attractive business models came along and are competing for investor funds, making life harder for inefficient, capital intensive industries. And by coincidence these business models have much better climate footprints.

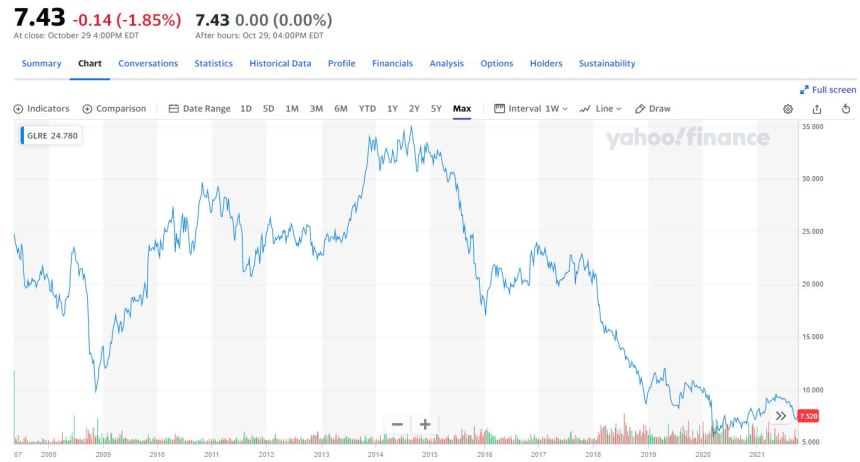

Therefore I do think that Divid Einhorn (and others) might want to look at their own investment process before blaming someone else for their misery. I still struggle to understand why such a smart person is acting so stupidly over the past 5 years or more. it’s jsut amazing how he basically killed off his public listed Greenlight Re vehicle and I am really glad that I got out without a loss a few years ago before things really got bad:

P.S.:

If you have the urge to submit Oil and Gas stock tipps: Please focus on these players who make the lowest emissions and have the most concrete plans for further reductions. Anything else is not interesting for me.

Shell has clear priorities: returning cash to shareholders. Not increasing oil production or building renewables.

https://www.ft.com/content/c3a4835b-85e5-4895-86a2-cb4d3f372940

As a german engineer and with a PhD about reliability of gearboxes for wind energy turbines, I have tried to make the numbers of the german Energiewende work already several times, but I always came to the conclusion, that shutting-off nuclear power plants + shutting-off coal plants and trying to substitute that with intermittent & low density sources will not work, while at the same time for instance the need for electrical energy is to grow substantially with the electrification of Transport. For a recent example, I refer to the 14th of August 2021. Also I can recommend Prof. Sinn‘s presentations about this matter (Energiewende ins Nichts).

In general, I think we observe a normal energy cycle after years of low prices and corresponding tight investment budgets of energy companies and rising demand post-pandemic. In Germany, due to the Energiewende the conclusions are amplified.

In my opinion, ESG is just one more factor contributing to the energy crunch. One recent example could be Thungela Resources (on which I made 60%) which now – after the spin-off – certainly has a much higher cost of capital for increasing the average mine life of their mines. And that would be absolutely necessary given countries like India, Bangladesch etc. Relying on their export products for a cheap and reliable energy supply for decades. The current price, if maintained for some time, will make it possible for Thungela to come up with the necessary investments without relying on external capital.

Disclaimer: Also as an engineer, I’am struggling to convince myself, that human-made climate change is real. Nevertheless I would of course also prefer if we could find a solution for a cleaner and cheap and reliable energy supply for the world.

Thank you for the comments. I would be very interested in more details on these gearboxes by the way 😉

Indeed, some of the assumptions towards quick electrification are much too optimistic, others may be too pessimistic.

However, as a trained Economist (BWL, sorry, no PHD) I can tell you that Prof. Sinn has many qualities but deep knowledge about any topic is not part of that. He has been continuously wrong on many topics regarding the EUro and in my opinion, still doesn’t understand the mechanics of Target2. Therefore I also don’t consider him as a high-quality source with regard to the Energiewende. He likes to be in the Spotlight and prefers controversial stand points to ensure his airtime.

I more than agree with you about Hans-Werner Sinn’s knowledge of monetary policy and the Euro.

His statements are hair-raising.

He did some theoretical research on corporate taxation and tax competition in the 70s and 80s. These works are solid, I think. So I would disagree that he has no deep knowledge of anything.

But he really has no idea about monetary policy.

I can’t judge his statements on the energy transition conclusively. But there is no reason to trust him there.

I can‘t talk about Prof. Sinn’s academic achievements in general, but his thoughts and computations regarding the Energiewende deserve some merits from my point of view.

Regarding the gearboxes, feel free to contact me by mail. As indicated in the past, I profited so much from this blog that I‘am happy to give something back.

Regarding ideas: I recently stumbled again over National Varco (former holding of TGV Partners Fund) and I realised that they use their oil offshore experience to also build a business for the wind-offshore industry and I think they will profit from an increasing installation of wind energy capacities as well as an uptick in the classical oil and gas business.

For me the analysis regarding tech and fossils is over simplistic, probably Gazprom will outperform Microsoft in the next years as it did in the past months. Fossils maybe the new „tobacco industry“ with outsized gains over a longer period of time.

As I mentioned, maybe in the short to midterm gazprom outperforms, maybe not.

Klement on investing recently had a good point on performance of energy companies and the price of oil. Basically highly correlated and there is a question on how high oil will run from here? This is too hard bucket for me. Btw., I am a Swedish engineer living in Bavaria. Not an expert on anything, but I often notice how Germany / Europe is late on trends and new technologies. Sometimes good but usually not.

Your analysis is mostly right, but there is a flaw in your analysis. Without ESG Wallstreet would have provided hundreds of billions to shale at these sky high oil prices as it did in the past. It is for a reason that shale was called „swing producer“ easily turned on and easily turned off. There are shale companies with P/E multiples in the low single digits, which is not a market clearing price. Regarding the mayor oil producers your analysis is right, the decision was made years ago.

Another goal of the ESG crowd is to make fossils more expensive in order to make renewables more competitive. Since ESG killed the business models of fossils, there is no reason for OPEC+ to finance the decarbonisation of the industry and use there spare capacity to bring prices down although Joe Biden is continously begging Saudi Arabia. In a free oil market this would probably be the case, but not with a cartel. In my opinion they will use their pricing power to make as much money as possible over the next 10-20 years. As an example Europe and Asia is just experiencing who has the pricing power in Natgas. In the past 10 years OPECs pricing power was limited because of shale oil, but this competition will vanish in the next years. One reason is ESG investing.

We will have to live with high oil prices because OPEC+ regained their pricing power, investors refuse to finance shale and the ESG crowd wants these high energy prices.

Regarding Natgas the analysis maybe more complicated because it is used for electricity generation.

I guess you haven’t fully read the post. Investors still put money into shale and still lose huge anounts of money.

I disagree completwly with regard to ESG. As described in the post, the oil majors preferred to pay big dividends and share buy backs instead of investing into new developments.

Overall I do think that as a society, getting rid off the fossil fuel addiction will not be easy but worth the effort. Why should we want to be dependent on Countries like Russia and Saudi Arabia for the foreseeable future ?

Without ESG Wallstreet would pour a lot more money into shale as it did in the past, just look at the number of drill rigs as an indicator. The time lag is something about 6-9 months. The output usually went up with high prices and went down with low prices. At the moment the ouput is quite stable despite high prices. Would shale contribute another additional 1-2 mio barrels because of higher investments the price would be lower.

I completly understand that you would like to promote ESG for personal reasons, but you should not mix up facts in order to provide the desired outcome. ESG is partly responsible for high prices for the reasons I described in my post. It is the stated goal of the ESG crowd the make fossils more expensive, how can ESG then not be responsible for high prices? CO2 Certificates are going through the roof. Your reasoning regarding oil majors is right but you do not get the whole picture right because of your ESG addiction. If you e.g. favor tech companies over fossils you should have a closer look at the “S” an “G” of ESG.

By the way, I am an owner of Gazprom and quite happy with my investment.

Just repeating your initial arguments doesn’t make them more valid. Of course less money goes into shale because hundreds of billions have been lost and even Wallstreet is able to learn.

You seem to be happy with your Gazprom investment which is ok with me. Our country is still a free country compared to others.

I also do not have a perdonal ESG agenda. Yes, I am concerned about climate change but I simply think that companies that try to mitigate their CO2 foot print will be better long term investments.

And maybe just to clarify: I don’t have anything against Gazprom shareholders as such. Only against the ones who are lecturing others on climate change while cashing in Gazprom dividends at the same time 😉

The argument, that shale oil burns money, is as old as shale oil itself. I read it the first time in 2014. Repeating this argument in 2021 does not really make sense. If the loss would be the reason that Walltreet stopped the money flow, they would have stopped in 2016 at the latest. Just read the annual letter of Larry Fink of Blackrock as an example why the markets do not support these kind of oil investments anymore.

Anyway, I will stop the discussion here, obviously you are not interested in any serious exchange otherwise you would have answered to the several points I made on this topic and not simply repeating your initial arguments.

Good luck with your ESG agenda.

Ok. I’ll try to be constructive here. Blackrock currently has AuM of around 9,5 (US) trillion or 6% of global traded AuM.

Interestingly (or naturally) they own large stakes in Fracking and Oil and Gas companies for instance here

https://fintel.io/so/us/clr/blackrock

https://fintel.io/so/us/chk/blackrock

https://fossilfreefunds.org/blog/2021/04/20/blackrocks-carbon-transition-fund-packed-big-oil.html

So looking at Larry Fink’s annual report in my opinion doesn’t explain any under-investment in the Oil and Gas industry at all.

But maybe I am just not smart enough and you can enlighten me ?

In any case, good luck with your Gazprom investment. You might need it.

For the record: Good Thread on why the US is not the “Swing producer” anymore:

Hint: Not ESG but ROE 😉

From reading David Einhorn’s book „Fooling Some of the People All of the Time“, he has one fatal flaw in his attributes—he is very righteous.

Maximum profit for a short position is 100%. Yet a wildly successful long position the profit is infinite. For Einhorn’s short in Allied Capital, is it all worth it to be dragged through the mud with people with questionable characters? Greenlight publicly bickered with the company, spent time and effort finding witnesses, entangled in legal battles…etc. Meanwhile Allied Capital used shareholders‘ money to pay for publicists and lawyers to fight with Greenlight. Greenlight won in the end but this came at the costs of years of borrowing costs, legal fees, wasted time and energy.

Through this ordeal Einhorn was about being morally right than making money. When his action has deep moral underpinnings this is probably when he is no longer objective. The fact profits from shorting Allied were donated to charity made it worst, it gave Einhorn a moral boost.

Maybe from then on some positions he could not just admitted defeat and move on. Maybe he put extra ego and pride into his investment decisions.

Also I feel like Einhorn was no longer satisfied with simple investment cases. There have be some kind of fancy financial calculations or legal maneuver. Sometimes it is better to go to the basics and buying plain old boring companies with great value.

Very good write up.

I still wonder about the impact investments into dirty companies have (or don’t have). Do investments (i.e. share purchases) into dirty companies lead to higher emissions? Why/how?

The impact is indeed more indirect: a higher valuation means lower cost of capital which in turn creates more profit and more potentially dirty investments in the future.

Thank you! My current understanding is that buying shares of dirty companies has no negative impact as long as these companies aren’t issuing new shares and the impact could be somewhat positive if these companies do buybacks. Would you agree? Or am I missing something?

In principle, the higher valuation enables the financing of projects that would otherwise not be profitable.

Share buybacks then really make no sense. If, in the opinion of management, the company is overvalued by the capital markets, one would rather issue new shares.

You don’t have to issue shares either. Financing through bonds or bank loans also becomes cheaper.

Why should a company not implement a project that is now profitable thanks to low financing costs?

A valid counter-argument is, of course, that if responsible investors stop investing in Gazprom, only irresponsible shareholders will remain. So it might be a better solution to use one’s voting rights to effect internal changes toward a more climate-conscious corporate culture.

The problem in the case of Gazprom is that the governance of this company is very opaque and it is not clear how much power foreign shareholders can exercise.

It would be really interesting to see how an activist campaign would look like with Gazprom. Maybe there is a hedgie out there who is thinking about suicide in any case and gives it a try.

Isn’t that exactly what our former Social Democratic Chancellor has been trying to do in recent years? Since I would never accuse him of bad intentions, I cannot interpret his statements otherwise. 😅

https://www.wired.com/story/germany-rejected-nuclear-power-and-deadly-emissions-spiked/

As I mentioned: Ms. Merkel made the decision. Not the Greens.

I would like to know why you call Gazprom as dirty. NatGas is atleast better than cheap coal being used in germany which itself happened because the self proclaimed greens in germany lobbied for closing Nuclear plant which were producing clean energy in first place. For disclosure iam not Russian or putin’s friend.

Well, the problem is simple: methane Leakage. Methane creates 80 times more damage than CO2 in the short term. Russia and Gazprom are “leading leakers”, leaking for instance ~5-6 times more Methane than Saudi Arabia.

Thanks to satellites, this can now be tracked without relying on Russian numbers. Just google “Gazprom Methane LEaks” and you get a lot of results.

Fracking Gas is equally bad, however, there are sources which much lower methane footprints. NS2 is not a good idea climate-wise.

And maybe you recall that the final decision to close down the AKWs was made by Ms. Merkel after Fukushima, not the Greens. Please stay with the facts. there are other web pages where “alternative facts” are much more welcome.

For disclosure. I am not a Green and not Anna-Lena’s friend 😉

Why did Germany insist on Nord Stream 2 to be built then?

Germany classifies natural gas as ESG compliant under EU ESG regulation, so does France with nuclear power. Germany will mine lignite until 2038, Poland even until 2049! Nevertheless, energy prices for German consumers have already skyrocketed for years, not only recently. The European ESG policy is a complete mess, imo.

Agree, the European policy so far is not very coherent. Every country tries to protect its legacy assets.

Although the policy is a mess, the Germans have financed cheap PV for the rest of the world.With the massive subsidies starting 20 years ago, they created a demand that has finally lead to dead cheap solar panels produced by the Chinese.

Of course the german consumers still pay the bill.

Well, that is one interpretation and in my opinion not the correct one.

In my opinion, Germany missed a big opportunity to take a global lead in the first wave by letting the production of solar panels move to China. For Windmills, Germany is still a leading player. I hope we are smarter as a country in the next wave of Electrification.

Leakers sounds like leeches… which also aplies to these russian folks…

I think to have a proper exchange on the whole ESG thing, we should be receptive to other’s POV and opinions as the subject itself is too political. On ESG, my opinion is not to take anyone on their facevalue.

“Look at what one is doing rather than what he/she is saying”.

– Blackrock/Larry fink and wallstreet in general are all suddenly ESG champions but they wont hesitate to invest in BitCoin which is the most absured thing EsG wise (burning coal based cheap electricity in exotic locations like Mongolia to calculate a crypto code or whatever).

– As Europeans we should aim to have clean energy without being overdependent on other’s.

– ESG’s crowd always has moving target’s earlier it was nuclear, then Oil/coal and now natGas.

– Mme. Merkel did what her voter’s asked her to do. But European Green’s did a lot of harm by exploiting Fukoshima mess to push for a public opinion that Nuclear was evil without asking what would be the alternative(lignite/natGas).

– In absence of cheap and clean Nuclear, the country had to fall back on Lignite/hard coal.

– Here comes Nordstream 2 and dependence on Russian gas. I agree with you that Natgas pipelines have methane leaking problem, but this could be fixed by better technology. I read an article on this subject on bloomberg.

– Germany is supposed to phaseout lignite based plant by 2038. I suppose lignite would be replaced by Gas.

– We know that Europe as continent is poor in fossil fuels or gas, therefore this setup is not ideal for energy independence.

– After Fukoshima, the Europeans greens were putting alot of pressure on France too to phase out nuclear asap. Luckily, French political establisment was much more pragmatic. (maybe due to the fact that French voters being less hostile to nuclear).

Question to be asked : If Oil, Gas, coal, lignite are all polluting and wind/solar reliability then, would not it had been pragmatic to spend R&D dollars to make nuclear plants more safe post fukoshima instead of planing for their closures. Did Euroepans Green’s did that ?? The answer is no.

Another point : Burning lignite and buying carbon credits is not enough to save our planet as some of the utilities are doing.

Thank you for the great list of arguments, I agree with most of them. A few remarks:

– the leakage of Natural gas especially with regard to Russia is not (only) about pipelines but also about Upstream. In my understanding, the Russian infrastructure is extremely old and leaking just everywhere

– To my knowledge, “”European Greens” do not exist as a homogeneous movement. The German version for instance seems to be very special with regard to Nuclear

– personally for instance I do think that we need Carbon Capture (and storage/usage) which is also something that the German Greens don’t realize (yet)

– I am not an expert on Nuclear, but I found the concept of Wave reactors quite convincing. However one should be aware that without subsidies, Nuclear is VERY expensive, especially if the long term liability for the waste is not taken up by the state

– I fully agree that a lot of the ESG efforts by large financial institutions are more “green Washing” than anything else.