All Swiss Stocks Part 16 – Nr. 166-180

As last time, I throw in an extre 5 stocks at no extra cost for my readers (2 candidates to watch) !!! To make it an even more compelling offer, I add this link which explains how German investors can mitigate the 35% withholding tax for Swiss dividends.

166. Walliser Kantonalbank AG

Walliser is one of the many regional banks with a market cap3 of ~1,6 bn CHF. As the other Kantonalbanken, the have a decent dividend (~3,3%) but the stock price is flatlining for many years. “Pass”.

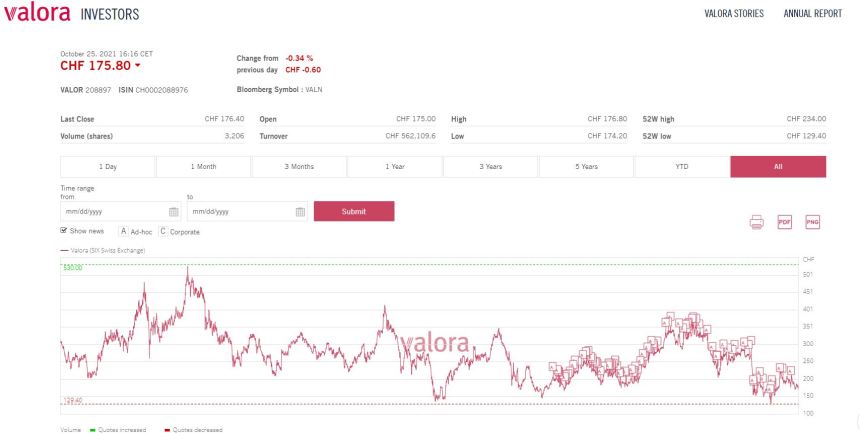

167. Valora AG

Valora is a 775 mn CHF market cap company that is active in food and convenience retailing. If I understand it correctly, they run both, own outlets as well as franchises and have a certain focus on bakery products. 75% of sales are done in Switzerland.

The long term share price looks extremely uninspiring:

Valora’s business had been hit hart by Covid and the first 6M 2021 are still ~-20% vs 2019. The company however stayed profitable in 2020. If Valora’s business returns to pre-Covid levels, the stock would be relatively cheap, however I am not an expert in food retail. “Pass”.

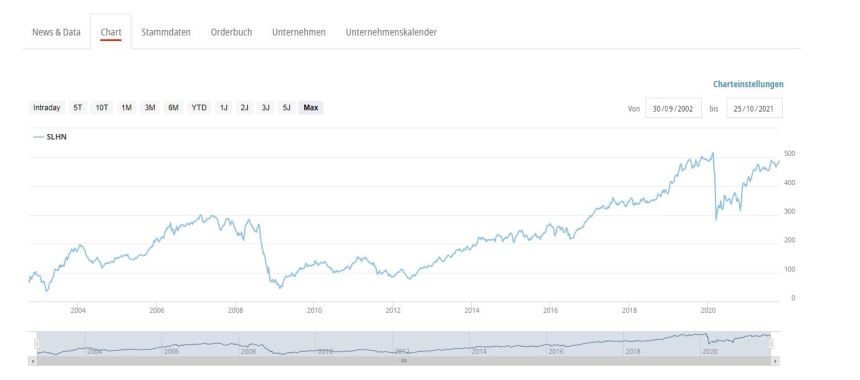

168. Swiss Life Holding AG

Swiss Life is one of the great names of Siwss High Finance. With a market cap of 15,4 bn CHF, the company these days is clearly “the little Sister” of Zurich. Nevertheless, SwissLife did rebound nicely from the GFC which I wouldn’t hae believed back then:

At a first glance, especially their main Swiss business seems to do well and ROE is at around 11% which is great for a Life Insurance company. A big contributor to this seem to have a shift into “alternative” assets like Private Quity and Real Estate. I think out of curiosity I would need to dig a little bit deeper at some pint in the future. “Watch”.

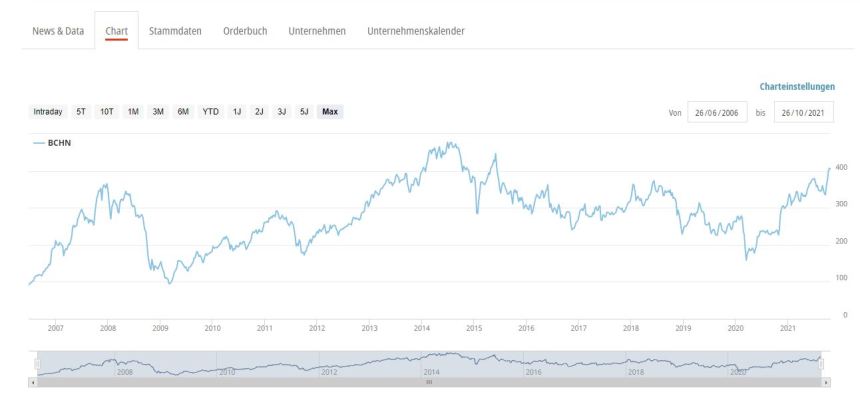

169. Burckhardt Compresson AG

Burckhardt is a 1,4 bn CHF market cap company that specializes in compressor technology. Compressor technology s mostly needed to compress gases and as such Burckhardt is active in and around the Natural Gas industry but also in other areas. One interesting aspect is that Hydrogen is clearly also a gas and if this would be a big business, Burkhardt would benefit.

Interestingly, Burckhardt showed no negative impact from Covid and had a strong 2020 (FY goes from March to March). The share price has recovered nicely since March 2020 but is still below the highs from 2014.

The business as such is split into a low margin equipment segement and a very high margin servicebusiness. Overall they reached close to 10% EBIT margin. They claim to have 30% market share and being nr. 1 in the relevant global markets.

Valuation wise, the stock is not cheap at 31x trailing PE, but I really think that this is a very interesting company, therefore I’ll “watch” them carefully.

170. Villars AG

Villars is a 75 mn CHF market cap thinly traded company that seems to own real estate and run some retail stores and bars/restaurants. In 2019 they made around 25 CHF profit per share which puts them at a trailing PE of around 30x.

The most interesting point about this stock it that the share price wasn’t affected at all by Covid although the business really tanked in 2020. Not my circle of interest, “Pass”.

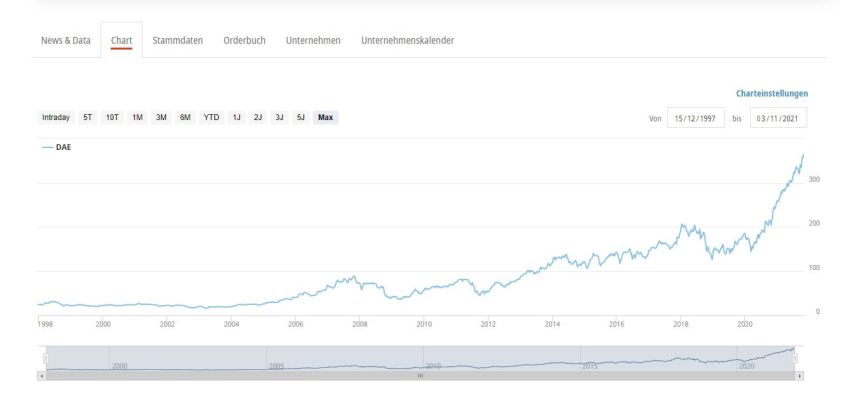

171. Daetwyler AG

Just looking at the chart, Daetwyler, a 4,6 bn market cap stock looks like your typical “Swiss Corona winner” stock, having doubled vs. pre-Covid levels:

According to the investor presentation, the company is active as a supplier to pharmaceutical and healthcare companies as well as the automotive industry.

The company projects 6-10% growth in the next years and EBIT margins of up to 20% which looks nice. The company completely reorganized in 2020 and 2021, selling off less profitable divisions. THE EBIT run-rate for 2021 is somwhere around 180-190 mn CHF, ROCE at a healthy 25%. After the recent increase, the stock is not cheap but I still find it very interesting, therefore I’ll “watch”.

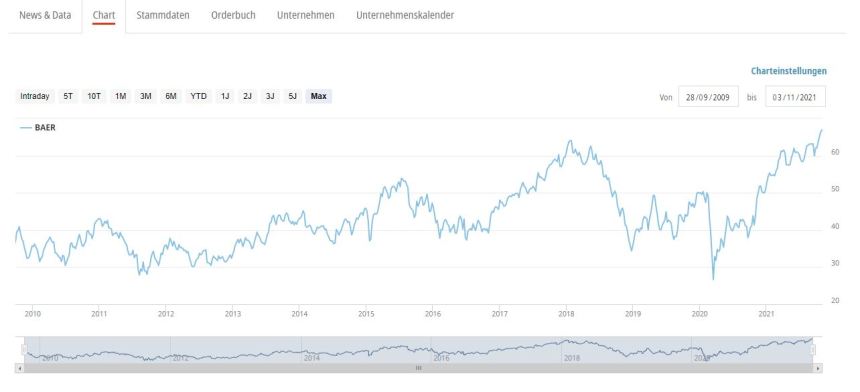

172. Julius Baer AG

Julius Baer is a 14,8 bn CHF market cap bank that is one of the biggest and most well known Swiss “Private banks”. The stock chart doesn’t look too bad compared to other banks:

Based on the 6M numbers, Julius Baer trades at around 13-14 times 2021 earnings and 2,2 times Book value. Profitability is clearly better than with “normal” banks but to be honest, I do not like the Private Banking model that much, therefore I’ll “pass”.

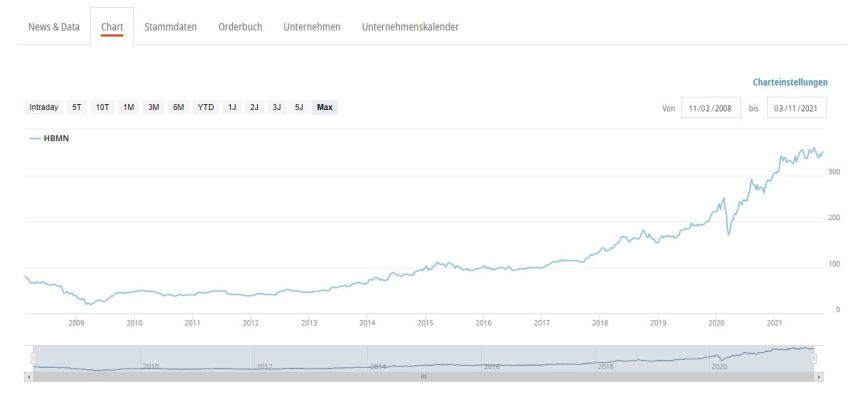

173. HBM Healthcare Investments AG

HBM Healthcare is a 2,5 bn CHF market cap investment company that, as the name implies invests into Healthcare companies. Looking at their portfolio, it seems to be a mix of private and listed company, wtih currently around 60% of the portfolio being listed stock. The track record looks impressive, with the stock having doen 10x over the last 10 years:

The shares seems to trade rouhly or slightly above reported NAV. The biggest stake with a 25% weight is a Chinese Biotech company. As this is clearly outside my circle of competence and will always be, I’ll “pass”.

174. Hypothekarbank Lenzburg AG

Hypo Lenzburg is a 302 mn market cap regional mortgage bank. The stock is flatlining since more than 15 years. “Pass”.

175. St. Galler Kantonalbank AG

Another regional Kantonalbank with a market cap of 2,6 bn CHF and a flatlining stock price. “Pass”.

176. Compagnie Financiere Tradition

CFT is a 836 mn CHF financial service company that acts as a “Broker of Brokers”, i.e. facilitiating as a market maker between large financial institutions. CFT is actually majority owned by French Viel &Cie, a company I looked at 9 years (!!) ago.

The stock price has recovered over the past few years which is quite surprising considering that the Broker-to-broker business modle was considered to be dead some years ago:

Based on 2020 profits, CFT trades at a relatively cheap 12x PE, profits have been increasing nicely over the past few years. The first 6M however di not look so good. If I would have a lot of time, i would like to underatnd how they came back, but otherwise it is a “pass”.

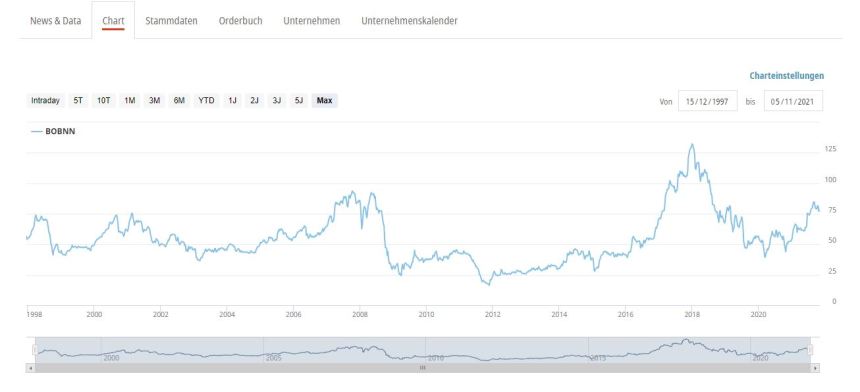

177. Bobst AG

Bobst is a 1,23 bn CHF market cap machinery company that manufactures machines for the packaging industry. Looking at the stock chart we can see that Bobst has not made that much progress over the last 20 years or so:

In the past few years, already 2019, pre Covid showed a detoriation. EBIT margins in the past have been around 5-7%, ROCE between 12-23%. Assuming average earnings of around 70 mn CHF, Bobst would trade currently at around 18x “normalized” Earnings. This is not extremely expensive, but there also seems to be limited room for long term structural growth. Bobst is clearly not a bad company, mabye comparable to Krones from germany, but also not really interesting to me, “pass”.

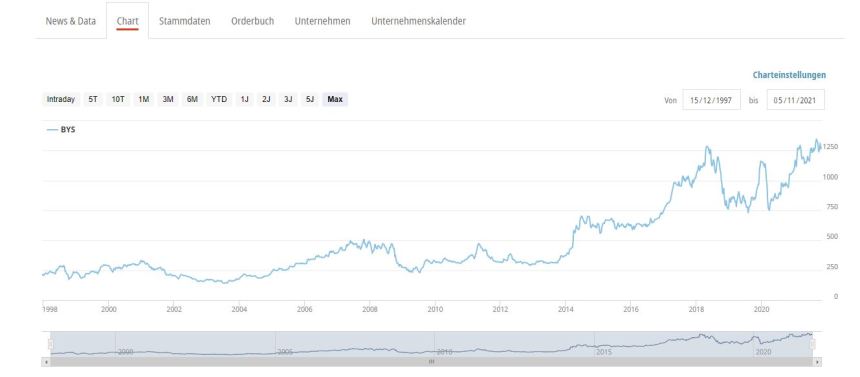

178. Bystronic AG

Bystronic is a 2,6 bn CHF market cap company that is the remainder of a conglomerate called Conzzeta. Looking at the share price, the “de-conglomeration” was a hit with investors:

At the moment, the remaining segment which again is special machinery, seems to generate ~900 mn CHF in annual alses with an EBIT margin of 7-8%. They plan with annual growth of around +5% and an EBIT margin of 12% in 2025. Assuming this is correct, this would represent an EV/EBIT (adjusted for around 500 mn net liquidity) of ~15 for the year 2025. In my opinion that is too expensive for a machinery company, “pass”.

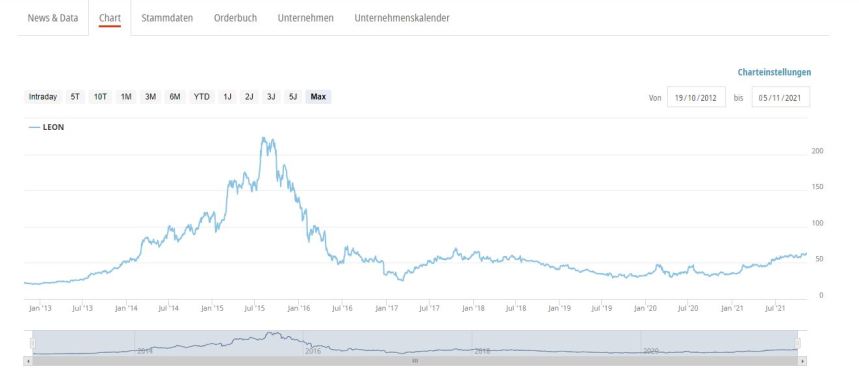

179. Leonteq AG

Leonteq is a 1,2 bn CHF market cap financial services company tha seems to offer mostly structured products, both to retail clients as well as B2B.

The company has quite volatile earnings, 2020 for instance was a bad year, the first 6M 2021 look a lot better. I guess the reason is that they are in principle short volatility. The share prcie doesn’t look too remarkable abart from that peak in 2015.

The company seems to have been founded as a subsidiary of EFG and then IPOed in 2012. In 2015/2016 they ran into deep trouble, both operationally but also with the regaultar as they seemed to have screwed over some clients in a pretty bad way.

Overall this doesn’t look like a trustworthy financial institution 8(ven in relative terms), therfore I’ll “pass”.

180. CI Com SA

CI Com is a 2 mn CHF market cap nano cap with a very ugly chart. Nothing to see here, “pass”.