Insurtech Massacre part 2 – Lemonade 2021 Earnings & 2022 Outlook

A few days ago, I had a first look at the “massacred” listed Insurtech sector and decided to focus on the P&C players only. This week, both Lemonade and Root reported 2021 numbers. I’ll start with Lemonade and will continue with Root in a few days

Lemonade 2021:

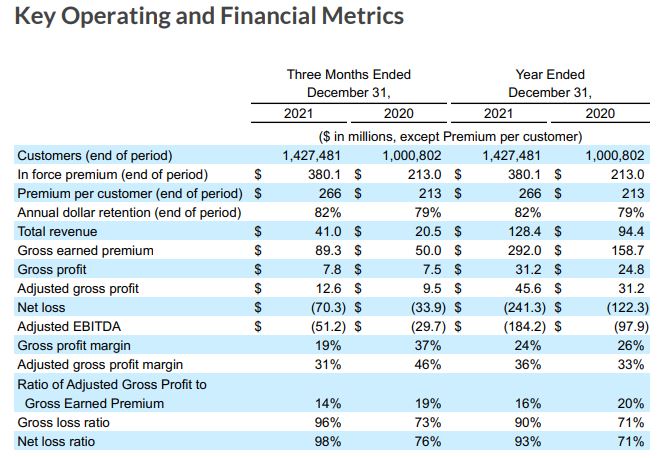

This is the overview of 2021:

Growth looks still Ok for 2021, however losses have been accelerating faster than sales which leads to a deterioration of even of some of the creatively adjusted numbers.

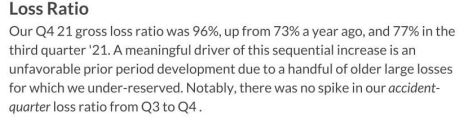

Loss ratios have been increasing, which happened also to the incumbents, but loss ratios in P&C above 90% is bad even for a “start-up”. One very concerning statement from the 8-K in my opinion is the following:

Under reserving for a fast growing insurance company is a red flag. Unfortunately they don’t provide numbers for actual losses and reserve developments “run-off” which would be standard for any normal insurance company.

In addition, they give no overview over actual premiums across products, business lines or geographies.

I think it would be important information if the company still grows within the initial product categories or only grows because they move into other countries / business lines. So transparency is really bad.

Sales and Marketing expenses

In 2021, Lemonade spend 141,6 mn USD on sales and marketing, this compares to around 163 mn additional “inforce premium” or 84% of the increase in inforce premium.

In 2021, the cost was 80,4 mn USD for an increase of roughly 100 mn USD in in-force premium (80%). Normally one would assume a certain scale effect, but Lemonade actually needed to spend more to sign one USD in premium thant the year before.

I assume that this is a result of moving into new product lines as well as market entry in Germany etc.

Another effect could be that Lemonade relies very much on Facebook advertising and with the changes that Apple made, they’re online acquisition becomes less efficient. This could be an even bigger issue in 2022.

One could also question, how value creating this growth is. In an ideal world, on a gross basis, the business might run at an 80% combined ratio (like Admiral). With 20% churn and an average lifetime of 5 years, spending 80% of a new premium dollar for acquisition, only earns back (5×0,2)/0,8 = 1,25xLTV/CAC before any overhead expenses which is very very weak. And they are very far away from an 80% combined ratio.

Lemonade Outlook 2022:

Here is their summary guidance for 2022 (pre metromile):

Guidance for Full Year 2022

For the full year 2022, please note that we expect the Metromile transaction

will close during Q2, and that our total annual IFP will grow approximately

70% during 2022. The guidance below, however, excludes the expected

impact of the closing of the Metromile acquisition:

• In force premium at December 31 of $530 – $540 million

• Gross earned premium of $423 – $427 million

• Revenue of $202 – $205 million

• Adjusted EBITDA loss of $(290) – $(275) million

• Stock-based compensation expense of approximately $80 million

• Capital expenditures of approximately $10 million

A few things stand out:

- Growth seems to decelerate significantly, from 90-10% ion the last years to only 40-45%

- Even the adjusted EBITDA numbers in relation to gross earned premium (-66-68% vs. -63%)

- And Stock based comp explodes from 44 mn USD in 2021 to 80 mn in 2022

Clearly, a lot of former high flying Growth companies need to “re-incentivize” their employees whose stock options are now deeply underwater, but 80 mn is a lot of money and hints to potential retention problems within the firm.

Summary:

In summary, Lemonade’s 2021 numbers look at a first glance “okayish” but a few worrying signs are obvious, such as the reserving issues and no scale effects whatsoever (or even negative ones).

The 2022 outlook however seems to be a big disappointment. A loss making, high growth company whose growth is disappearing does not justify any premium valuation.

In addition, their customer acquisition cost seem to be much too high even in a “mature” stage and might get even worse due to their reliance on Facebook.

Even after the recent drop below the IPO price, the stock seems far too expensive and the Metromile acquisition seems to have been more a “hail mary” play than a strong strategic deal.

Recently Google announced they would make similar ad tracking changes on Android than those which Apple introduced earlier: https://www.ft.com/content/14ebaaf6-5b99-4017-b6b0-e8e5878b1f1d

It might have an even larger impact to ad tracking for the ad industry and customers.

No, it’s cheap on 2027 earnings only if they can generate an operating profit margin of 10% by then.

If they could generate a 10% operating profit it would be cheap on 2023 earnings.

If Germany would have a border to the Mediterranean Sea, we could make a lot of money with tourism. However there is zero chance that this happens.

There is absolutely zero chance that Lemonade will make a “real” operating profit by 2023. Their numbers are all going into the wrong direction.

Catalans in BalearicIslands would love that Germans would buy out the islands and get rid of that turkish-like semi totalitarian spanish regime. Freedom for Ucraine and all oppressed people.

Allow me the comment that Germany and Europe and the Western world have higher priority problems at the moment and the foreseeable future.

Thanks for the link. If I understand all of this correctly, Lemonade is cheap based on 2027 earnings. No further comments.

alternate point of view: