Und noch ein wichtiger Akteur ist auf dem Markt.

Panic Journal – Ukraine/Russia edition part 4: Power & Gas prices, Merit Order and other Ramblings

Background:

With European Gas and Electricity prices trading like “Meme stonks”, it is time for another “panic post”. As always, these posts are mostly for myself in order to better structure my thoughts and educate myself and should not be seen as any kind of advice.

Just to quickly revisit the last post from part 3. One of my predictions back then with regard to the economic impact (unfortunately) aged quite well:

One explanation that I have read is that Russia and Ukraine are only 2% of Global GDP, so a “loss” of these countries is no big deal. Personally, I do think that this is not a very useful number. Russian oil and gas is powering a significant amount of European (and Global) GDP. A supply disruption from Russian oil and gas would impact a much larger share of GDP globally and might make Covid-19 supply chain disruption like a toddler party.

Turmoil in European Gas and Electricity markets:

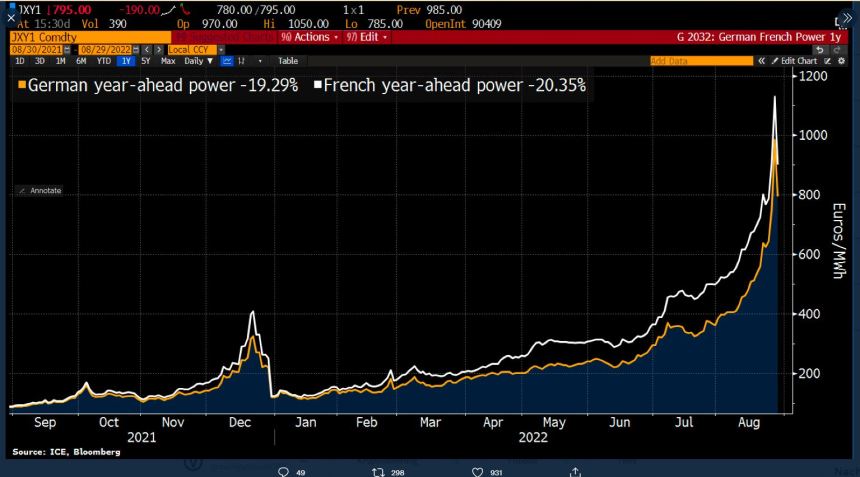

The fact that European Gas and electricity markets face absolute mayhem has now clearly reached the headlines. I have stolen two Charts from Twitter(@Schuldensuehner), one showing electricity prices until yesterday, and one natural gas:

Despite a current pullback, levels both, for gas and electricity are somewhere between 10x and 20x higher than before the crisis and not sustainable.

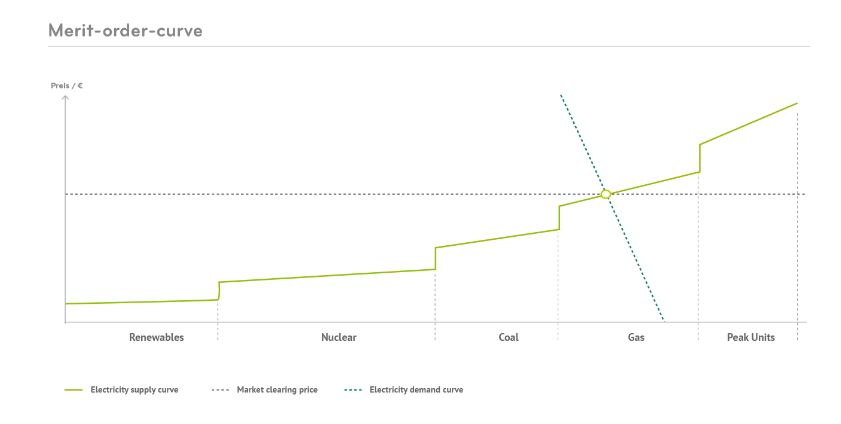

Natural Gas prices are high because Russia is not delivering that much gas anymore, but why did Electricity prices explode as well ? As many of us have learned in the last few days, the main culprit especially for politicians is the European electricity market which works along the “Merit order”.

Merit order effect

The merit order effect can be explained as follows:

In the energy industry, the term ‘merit order’ describes the sequence in which power plants are designated to deliver power, with the aim of economically optimizing the electricity supply. The merit order is based on the lowest marginal costs.

and

The mechanism to determine the clearing price and volumes in a power exchange market is based on the merit order curve.

So in my own words, the price for electricity in this system is determined by the most expensive source that is required to fill a given level of demand.

With the recent spike in gas prices (see below), the discussion came up that Europe needs to move away from the Merit order system in order to “decouple” electricity prices from the gas price.

Interestingly, this discussion already started in March, with Spain and Portugal asking for an exemption, but among others, Germany and Netherlands, opposing this. Nevertheless, Spain and Portugal got their (temporary) exemption.

The weakness of that systems seems to be pretty clear: When the marginal cost for the most expensive source is very high, all the other producers receive significant windfall profits. The price derived from the Merit order principle doesn’t care about the average cost. This looks very unfair especially to the consumers, who pay extremely high prices in order to make a few people/organizations very wealthy.

So why are we using the Merit Order principle anyway ?

Before criticizing the Marginal pricing/merit order principle for the electricity market, one thing should be clear. This principle applies to almost all commodity market. This article explains quite well that Merit order/marginal pricing is simply the market determining the clearing price based on a given demand and supply.

Why should any producer sell a commodity at a lower price in the market if he knows that the buyers need to pay the higher price ?

And the next question is of course: Why use a market model anyway ? The answer is relatively simple: In theory, the market should work its magic by increasing supply and reducing demand at higher prices. In addition, for other commodities, prices are also buffered by inventory levels, i.e. players increase inventories at low prices and sell inventory at high prices.

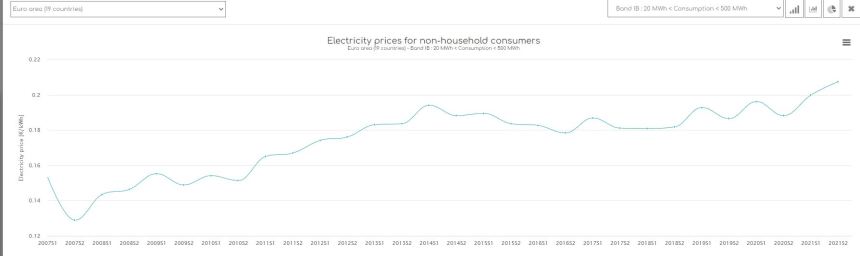

The unique characteristics of the electricity market is that there is almost no relevant inventory. Nevertheless, for the past 15 years or so, the system worked quite well and kept (non-household) electricity prices relatively stable despite significant investment into Renewable Energy as this chart indicates

Such a market model also incentives producers to use the lowest cost production facilities in order to maximize their profits in addition to adding more low cost capacities.

When looking at a typical merit order sequence in the European electricity market, we can see that even in the past, gas was always the most expensive source:

What also becomes clear is that especially for Germany, if you switch off Nuclear, you need to use more marginally expensive sources for generating electricity. the more you think about it, the more stupid it looks to switch off the Nuclear plant in this crisis environment.

So how does the “Spanish model” look like ?

As mentioned above, Spain and Portugal have been granted exemptions to the free market model already. This document here describes how they try to manage the situation:

The sustained increase in gas prices following Russia’s unjustified attack on Ukraine has led to higher electricity prices across the EU. In this context, in May 2022, Spain and Portugal notified to the Commission their intention to adopt a €8.4 billion measure (€6.3 billion for Spain and €2.1 billion for Portugal) to lower the input costs of fossil fuel-fired power stations with the aim of reducing their production costs and, ultimately, the price in the wholesale electricity market, to the benefit of consumers.

The measure will apply until 31 May 2023. The support will take the form of a payment that operates as a direct grant to electricity producers aimed at financing part of their fuel cost. The daily payment will be calculated based on the price difference between the market price of natural gas and a gas price cap set at an average of €48.8/MWh during the duration of the measure. More specifically, during the first six months of the application of the measure, the actual price cap will be set at €40/MWh. As of the seventh month, the price cap will increase by €5 per month, resulting in a price cap of €70/MWh in the twelfth month.

The measure will be financed by: (i) part of the so-called ‘congestion income’ (i.e. the income obtained by the Spanish Transmission System Operator as result of cross-border electricity trade between France and Spain), and (ii) a charge imposed by Spain and Portugal on buyers benefiting from the measure.

So the Government is paying Power produces the difference between the market price and a cap of at the beginning 40EUR/MWh. I think that didn’t look so bad in the beginning, but with current gas prices I am wondering, how long Spain and Portugal are able to do so. This is clearly an experiment with a short term impact but unknown long term effetcs.

The French model:

France in comparison has simply capped electricity prices until the end of 2022. That is relatively easy as most of the electricity supply in France is Government owned (EDF). And while they are at it, they decided to take EDF private in July to keep the losses in the family. For France, the cap is less of an issue as a significant part of their capacity is Nuclear with relatively low marginal prices. However, due to the maintenance of their Fleet, France needs to import a lot of electricity at the moment which will make this cap very expensive.

Other EU countries:

Other countries have introduced a variety of measures, mostly some subsidies and some extra taxes, but all of them rather short term oriented.

Summary of measures:

When looking at all these measures, the depressing fact is that all these measures assume that by the beginning of 2023 everything is back OK and they only treat the symptom (high electricity prices) and not the root cause (Natural gas consumption is higher than supply).

The Natural Gas market – German Government as a new, price insensitive buyer

So it is not exactly hot news, that very little gas is flowing from Russia. Nevertheless NatGas prices rallied significantly in the previous weeks, despite consumption being already a lot lower than in previous years.

On Monday, the German Minister of Economy and trade released some “great news”: German Gas storage levels are higher than initially planned and he expects Natural Gas prices to go down. So far so good.

What I found much more interesting is this part of his statement: “Das führe dazu, “dass wir nicht mehr für jeden Preis einkaufen werden. “ So what he is effectively saying is that up until the weekend, they were buying independent of any price level. What is not very well known in the public is the fact that as part of the new law for minimum levels of the German Gas storage sites, the German Government also awarded themselves the mandate to buy Natural Gas why a company called THE (Trading Hub Europe). THE is a private company owned by various Gas Transport networks.

To me it is not clear how much money they already spent but its seems to be at least something in the Neighborhood of 20 bn EUR. And as this is of course not their own money and they have “strategic goals”, no one cares about the price that the are paying.

In the German Wirtschaftswoche, there was an interesting interview with a German Energy trader who confirms the impact of Germany as a Gas buyer on electricity prices:

Wen meinen Sie?

Ich meine auf dem Gasmarkt. Über das Merit-Order-System hat der Gaspreis eine direkte Auswirkung auf den Strompreis. Und der Gaspreis ist zuletzt auch dadurch getrieben worden, dass die Trading Hub Europe, der Gasmarktverantwortliche in Deutschland, im Auftrag der Bundesregierung für bis zu 15 Milliarden Euro Gas einkauft, um die Speicher zu füllen. Das hat durchaus Auswirkungen. Das kommt meiner Meinung nach zu kurz in der Diskussion.

So just to reiterate this point: The German Government as a buyer has been pushing up the price of natural gas thorough its price insensitive purchases. This in turn increases the price of Electricity and this triggers the wish to dismantle the “unfair” current system. Congratulations.

More Government interventions on the way

What becomes more and more clear is that every one action of the Government leads to some effects which in turn require more Government intervention and so forth.

It all started with Putin declaring war and sanctions, but now we seem to be spiraling into Government intervention overdrive. Due to rising Natural gas prices, the German Government had introduced a “Gasumlage” which it has now to change again. Then it had to bail out Uniper again, then it will need to bail out either local utilities, retail customers or both.

The pain is spreading to other countries. Energie Wien, a local Austrian utility seems to be short 10 bn EUR or more. Poland seems to be short some significant amounts of Natural Gas as well for the winter.

However the EU wants to dismantle the Electricity market that has worked quite well for the past 15-20 years or so with unknown long term impact. And of course everyone one wants to tax those evil Renewable Energy operators who earn these obscene amounts of unjustified profits.

All of these actions however do little to address the actual problem or might actually create the opposite effect: Demand needs to be lower and supply needs to be increased.

With regard to demand reduction, my favorite piece advice is that of Mr. Kretschmer, the Green Prime Minister of the State Baden Wuerthemberg, who recommended to wash oneself only with washcloth instead of showering, after mentioning that he of course owns a solar PV roof and a wood pellet heating.

What I am missing is a structured plan with clear incentives to save energy in significant amounts and some coordination at European level.

Waiting for Magic to happen in 2023

Everyone now is focusing on how to “survive” the winter 2022/2023, most measure are very short term. Implicitly everyone seems to believe that all problems are going away in Spring 2023.

However I am not so sure. Yes, hopefully already at year end, two new LNG terminals should be up and running,with more of them coming, provided that all the LNG can be bought including the shipping capacity. However few large infrastructure projects in Germany have been completed in time in the past few years. Also, these Terminals, at least not the first two cannot fully replace the Russian gas. And when the storage is empty in Spring, the same cycle begins as well.

So for some time in the foreseeable future, Natural Gas will be a very scarce commodity in Europe. However almost all of the Government actions are only targeting the short term symptoms.

My inflation rate is not your inflation rate & time lags

Another observation that I make on a personal level is, that contrary to for instance food or petrol, price increases in electricity and gas hit people very differently on an individual basis and with a significant time lags.

Personally for instance, i have not received any notice from my local utility on any electricity price increase and for reasons out of my control, I am heating with wood pellets, where I was able to fill up my still in February at an acceptable price.

So far I do not know anyone personally whose bills have gone up 10x, but for some friends, bills and monthly installments are starting to increase significantly.

I am not yet sure what impact that will have on social cohesion and this will add a lot of uncertainty for the next months /years.

Summary:

To be honest, I have the feeling that I could barely scratch the surface of this topic. But still the question remains: what are the implications of all those observations above ?

My gut feeling is, that similar to the beginning of the Ukraine war, again, this will not be over as quickly as many people think. Maybe we have seen a peak in the European Wholesale prices for some time, but the demand / supply imbalance for natural gas will not go away by Government intervention into a quite well functioning electricity market, maybe even the opposite.

Also the effects on German and European household incomes will only materialize over a longer period of time.

Our politicians seem to be in populist “activity” mode which might make things worse before they get better.

From a lot of people I hear the question: “How can I profit from high electricity /Natural gas prices ?”. For me the better question would be: “How will I not get hurt badly by longer than expected turmoil in energy markets ?”.

I might be wrong, but I think it is still better to play defense for some time to come instead of trying to Yolo into the next opportunity.

For the portfolio, I already reduced my positions in German Renewable stocks in the beginning of the week, with the exception of ABO Wind. I am really worried of some kind of stupid “Robin Hood tax” for renewable producers.

Also, I think one still should be very cautious with regard to energy intensive businesses with little pricing power and discretionary consumer goods. I would be also very cautious with leveraged residential real estate as the real pain for renters will just start. I now it is boring, but “quality remains king”.

Stay safe & stay warm.

Someone needs to say the truth .. the first remedy german people can do is to boot out and jail green politicians who are completely in pockets of Americans. These people are anti german & anti EU.

Thanks for listening to my rants

I can see this point with regards to the remaining nuclear plants. But, with regards to everything else I think there are worse parties here. The greens were also the ones that pushed renewables. Without renewables we would be in a more desperate situation as the German nuclears had they not been shut down would probably face similar problems at the moment as the french ones. As we know – the phasing out of nuclear was not even a decision finally taken by the greens but by FDP and CDU. At the same time FDP was severely damaging the renewables industry in Germany.

And when it comes to gas I hope you don’t support further gas deliveries from Russia. The Greens (and FDP) were actually against North Stream 2 which was certainly the right idea.

I think this is a very good history and judgment on German Energy Policies:

https://jeromeaparis.substack.com/p/how-messed-up-was-germanys-energy?utm_source=profile&utm_medium=reader2

Another important point made there: the way we treated gas as just another commodity best traded on spot markets leading to a massive dependence on the cheapest form (pipeline Gas from Russia) was a major mistake. I can’t see how this was particularly the greens fault.

Maybe, a good time to allocate 1% of the portfolio into $GBTC or directly into BTC?

Why on Earth would I do that ? I would rather give my money to a real charity.

I really loved the merit order comparision with 2 potato farmers.

2 Farmers, 100% commodity product. One with traditionel farming cost per potato 2€, other modern farmer (using tractors whatever) cost per potatio 1€.

Hence on a rational market the price will be above 2€. There is nothing wrong with merit order, just polictical framing. ”

All we need” is a recession and the price will collapse..

Gov intervention will do more harm than good and just keep the demand up..

Der Ministerpräsident von Baden-Württemberg, der den Kommentar mit dem Waschlappen gemacht hat, ist Kretschmann. Kretschmer ist der Ministerpräsident von Sachsen.

Guter Punkt, aber irgendwie sind die sich doch alle recht ähnlich 🙂

Maybe expensive energy can be hedged by shorting or buying puts on those that are hurt most by expensive energy. I am not doing this and believe this trade might be too late. Just a thought…

Thanks for the great inside! Since you’re very pessimistic here some numbers from Bundesnetzagentur to give some hope: https://twitter.com/shabjako/status/1562816089943592963?s=21&t=zT_2GPrnf9_zULstOksbhQ

Looks like with current storage the gas supply is quite safe.

I couldn’t believe it until I checked the numbers myself! That’s under the assumption that deliveries from Nor, Bel, Ne stay constant but that doesn’t seem too unrealistic imho.

Deopax,

thanks for the link. Sounds great but the biggest issue of this calculation in my opinion is that you cannot assume that all the gas that is delivered via pipeline to Germany from the Netherlands and Norway is also used in Germany..

Historically, Germany “exported” ~35% of the imported gas to the neighbouring countries.

If you do the calculation based on this numbers with a 65% net retention, you end up with a deficiency of ~-120 TW/h.

I will invest in scarf suppliers 🙂

Ah, one last thing I forgot: a Spanish style price cap mechanism at a EU level might create (amongst other more long term inefficiencies I can’t even imagine) a massive moral hazard issue, where generators will scramble to buy as much gas as possible as they will most likely be compensated (one way or another by taxpayers) all or part of the difference between the artificial price level of the cap and the actual price, thus potentially making gas even scarcer all around. Also, countries like Italy or Holland, where the proportion of gas in the production mix is over 50% will need massive amounts of money to keep the scheme running, and I can definitely see taxpayers elsewhere not wanting to foot the bill, thus creating even more friction amongst EU member states. Let’s see what the geniuses in Brussels will come up with on Sept 9th at the emergency meeting… on a side note, and merely as a hedge for this situation, some Canadian and Australian uranium miners should reap the benefits of this whole mess, as countries like Japan and South Korea restart nuclear reactors, just my 2 cents

As a EU gas and power trader, I truly commend you for your analysis, it is absolutely spot on. A couple of things to add, that made the situation even more explosive: 1) the terrible nuclear situation in France brought about by delays in check-ups and maintenance schedules still suffering from Covid times disruptions; 2) the worst drought in forever all over Europe , which has severely hampered hydropower production. That said, the German government in the last 20 years has been very consistent in choosing (eventually) catastrophic energy policies: the ill-thought out Energiewende, which allowed renewables preferential treatment with egregious feed in tariffs (pushing many baseload plants out of the many for many years), to the closure of the nukes after Fukushima, to the all-in bet on Russian gas, and last but not least becoming the largest price insensitive buyer of gas while at the same time giving helicopter money to the likes of Uniper and crying about high gas and power prices. I may be professionally biased, but nobody is crying (except generators) when German power routinely goes negative in high wind, low demand days. If you manage to do something to bring the demand down (which is a very much neglected tool in these particularly troubled times) the market will correct itself, but I’m afraid a flashier, easier to sell solution will be peddled to the masses, and if we create long term problems (like discouraging any further investment in renewables, who are now comically the bad guys), well, that will be someone else’s problem…

Thanks for the insights !!!

Do you (or someone else) know what typical proportion of power consumption is priced at the spot (“merit order”) price and what is on long term contracts between intermediaries and generators? It’s a missing piece of the puzzle when we see reports on these sky high spot prices.

Another mystery is can the Russians run out of storage and flaring capacity on their side, and get to a point where they have a choice between delivering and blowing up their wells and so will deliver regardless of political theatre?

I remember that around 75% are OTC and longer term contracts. Whatever that means.

I’m not familiar with the Russian gas production system, but to my understanding it should be quite easy to choke back (=reduce production) a gas system. If a gas well flows easily (as in, doesn’t kill it itself due to liquid loading) it can be easily closed in by literally closing a valve on the xmas tree and started back up again by opening up the same valve. If you have let’s say 20 gas wells flowing into the gas processing system, you could either choke back all wells, or simply close a few, whatever you prefer..

World governments have ruined their countries by their panicked pandemic response while the world’s central banksters have ruined the world’s financial markets and economies (9 % inflation is not going to be transitory; continued high inflation is the only way highly indebted governments and corporations can pay their debts) by their panicked response to the 2008 crisis (itself caused by central banksters printing money and low interest rates). So why be surprised when their panicked response to possible global warming causes another crisis? Politicians everywhere should be pushing for more oil and gas production but of course that doesn’t go with their global warming crisis.

The merit Order trading volume is only 9% from the total trading volume:https://www.tech-for-future.de/preis-stromboerse/

Thanks, great link. I sm not an expert but usually the Spot price “anchors” the future prices.

Usually that might be true, esp. for commodities that are easy to store and/or dependably producable and deliverable. This, I think, is NOT true for most renewables. Though,

It can be improved with some good (weather) forecasts and managing clusters of renewable plants (shell bought such a Cologne startup)

Interesting post on how to incentivise people: Cash transfers and incentives instead of price caps.

https://marginalrevolution.com/marginalrevolution/2022/08/the-price-of-power-and-the-power-of-prices.html