Hannover Re: An overlooked Reinsurance Compounder & Comparison with Munich Re

Spoiler: This rather long post contains no actionable investment ideas.

Background:

Hannover Re is a stock that for some reason I have ignored for some time although I consider Insurance stocks as part of my circle of competence. Why did I ignore them ? I was always put off from the ownership structure. Hannover Re is majority owned by Talanx, which itself is also listed. Talanx again is owned ~80% bei HDI, which is owned by …I don’t know.

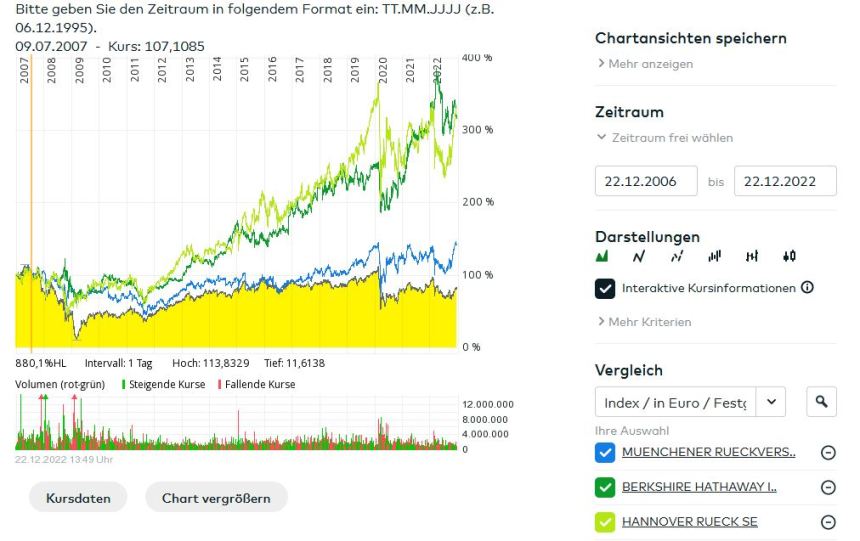

Looking at the chart, I should have considered them earlier: Over the past 15 years, Hannover outperformed the larger and better known peers like Munich Re and Swiss Re by a wide margin and ties with Berkshire (before FX):

This is very interesting, considering that Hannover Re is only the No. 3 global Reinsurer and Berkshire only number 5. Absolute size doesn’t seem the drivig factor for shareholder returns in the Reinsurance industry.

Deep dive Comparison: Hannover Re vs. Munich Re

As Munich Re and Hannover Re are both German based companies, I thought it might be fun to compare these two , as both have to report under iFRS and are subject to Solvency II regulation with BAFIN as main regulator. Both, Swiss Re and Berkshire run under very different regimes and cannot be compared so easily-

One small caveat: Whereas Hannover Re is a “pure play” Reinsurance company, Munich Re via ERGO is also active in primary retail insurance. Before jumping into the comparison, let’s just quickly summarize what Reinsurance is all about.

The Reinsurance business

Many Warren Buffett followers think that (Re) Insurance is a quite easy business: You collect the premiums, make money on the insurance side, which then creates the famous “float at negative cost” and then you earn even more money with smart investments.

Unfortunately, in reality this is not so easy. Reinsurance is to a certain extent a “wholesale” business, with the main commodity that they are holding in stock for their clients, the primary insurers, is capital. Primaray insurers “cede” an amount of their premium for the case that claims are larger than a primary insurer can or want to swallow. Therefore the forgive the chance to earn return on the float.

The theory behind this is of course diversificaion, I.e. that international reinsurers are better diversified and have a lower cost of capital etc. In reality however, Reinsurance is a pretty arcane art and similar to “structured finance” often has the main goal to make their clients “look better” instead of actually transferring a lot of risk.

In the old times, it was not unusual to actually give out loans to primary insurers and call them Reinsurance. In 2006 for instance, even Berkshire was fined with more than 1,2 bn for such “pseudo reinsurance” contracts whose main goal was to arbitrage insurance regulation.

Reinsurers are generally also regulated a little bit less than primary insurers because their clients are “sophisticated businesses”, so rules and restriuctions for reinsurers are ussually a little bit relaxed.

The main factor for being able to grow a Reinsurance business is capital. Without capital, regulators will not allow Reinsurance companies to do more business. So preserving and growing capital is very important for Reinsurers which in turn means the higher the return on capital (equity) the better.

Other than industrial companies, Reinsurance companies must have “tangible” Equity as main source of capital. Subordinated debt can alos be used as capital but “hard tangible equity” is the main source.

Hannover Re vs. Muncih Re – The details

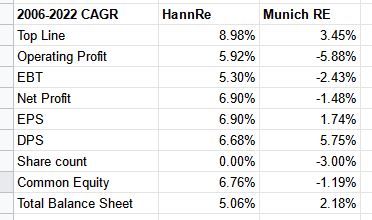

Let’s start with a few “Compound annual growth rate” (CAGR) numbers for the years 2006 to 2022 which already show a big difference between the two:

A few first comments here:

Hannover Re could increase their topline by almost 9% p.a. vs. only 3,5% at Munich Re. Operating profit increased “only” by ~ 6% p.a. for Hannover whereas it declined by -6% for Munich Re.

For Munich Re, only EPS growth is positive and this is due to a decreasing number of shares outstanding. The only category where Munich Re comes close is the growth rate in divdends per share.

Interestingly, Muncih Re has now less Equity than 15 years ago, despite a growing balance sheet. Overall, the 15 year numbers clearly show a big difference between Hannover Re and Munich Re.

The question now is of course: Why ? Why did Hannover better ?

Here are some more numbers that might explain part of the story:

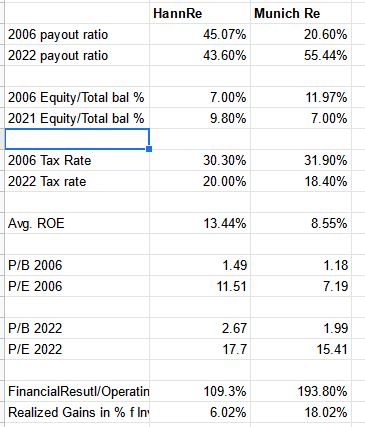

First we can see that Munich Re achieved their increase in dividends per share mostly through an increase in the payout ratio whereas Hannover’s payout ratio remained constant.

The second set of numbers is even more interesting: This is the percentage of Equity to total balance sheet value. In Hannovers Case, equity as % actually increased wheres in Munich Re’s case, this ratio almost halfed. So effectively, Munich Re is leveraging its Balance sheet much more. If we transalte this into leverage multiples: Hannover has decreased its leverage from 14x to 10x, whereas Muncih Re has increased the leverage from 8x to 14x.

Another interesting aspect is that in both cases, tax rates have declined significantly. This is clearly an effect that cannot be easily repeated. The decrease in tax rates mostly explains the difference between the EBT CAGR and the Operating Profit CAGR for both of them (roughly 1% p.a.).

Depite the much more conservative balance sheet, the average ROE for Hannover Re is ~5% higher over the 15 years than for Munich Re. To a certain extent, this is reflected in a higher valuation for Hannover, both in 2006 and now for 2022. But this difference is huge.

The final two lines look at the signifcance and the construction of the financial result, i.e. the result of the float.

In both cases, Financial results are higher than the operating income which means that over these 15 years, both company lost money with Insurance, i.a. the float was not free.

However, in Hannover Re’s case, Insurance almsot broke even, whereas in Muncih Re’s case the Insurance result was significantly negative.

The last line finally shows us how much of the financial results consits of “ongoing returns” (dividends, interest payments) and what amount is based on realized gains. Again, Munich Re’s financial result is of lower quality

Comparison summary:

In comparison, Hannover Re clearly looks like the better business. They managed to grow much more, achieve better ROE’s despite having a much more conservative balance sheet.

Munich Re in contrast seemed to have focused mostly on returning capital to shareholders. This sounds great in theory but for Reinsurance, where capital is the main resource for growth, it might not be the optimal strategy.

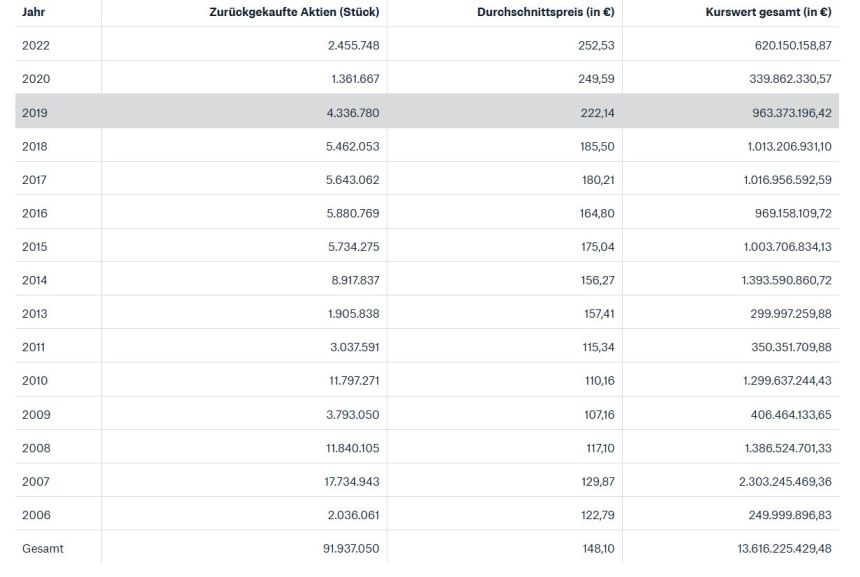

Munich Re has a great overview on their share buy backs:

So it is interesting to see that despit massive buy backs at prices well below today’s share price, Hannover Re has created significantly more value by retaining capital and growing the business instead.

So it is interesting to see that despit massive buy backs at prices well below today’s share price, Hannover Re has created significantly more value by retaining capital and growing the business instead.

Is Hannover Re now a “buy” ?

If I would be forced to buy one of the two stocks, I would clearly go for Hannover Re. Despite the slighly higher valuation, in my opinion the quality of the business is significantly better.

However the big question is: Is Hannover Re a stand-alone buy ?

The Reinsurance industry is supposed to enter a “hard market”, which means increasing prices and increasing profits if there are no large Cat losses. In addition, higher interest rates should increase interest income over time. Some investors even consider Insurance stocks as something of a “no brainer “right now.

On the other hand, with a trailing P/E of ~18, Hannover Re trades at an historically very high level (ex 2008/2009). With regard to Price/Book, the current level of 2,7x book value, reflects a premium of more than 100% to the historic average.

Hannover Re has clearly been trading too cheap for many years, but now, the stock looks to me about fairly valued. The stock clearly has momentum and could run higher on the back of increasing profits in 2023, but for my typical inevstment horizon of 3-5 years, I don’t see that much upside.

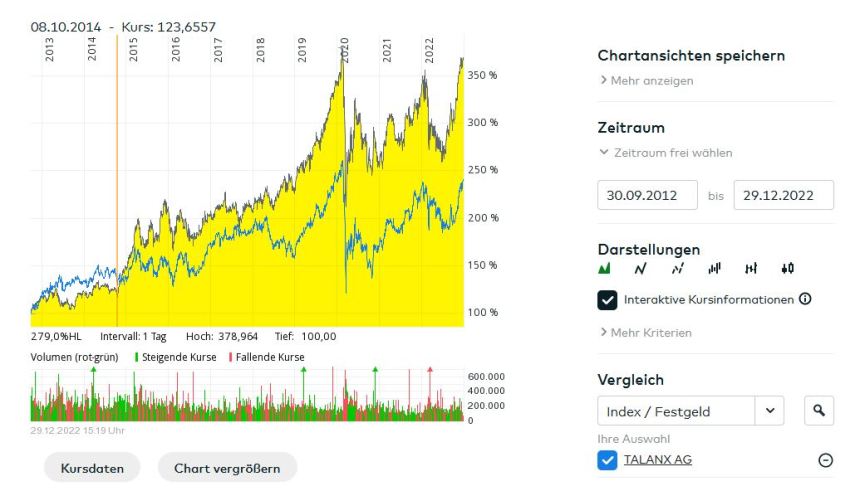

Is Talanx a buy instead ?

Talanx, itself listed, owns 50,2% of Hannover Re. With a market cap of 22,6 bn for Hannover Re, one could in theory deduct 11,3 bn from Talanx’s Market cap to see what one pays for the Primary insurance part.

Talanx itself has a market cap of only 11,3 bn, so one gets the primary insurance “for free”.The stock also has underperformed its major subsidiary significantly over the past 10 years:

Talanx had a net income of 1 bn after minorities in 2021, which includes ~ 600 mn EUR from Hannover Re. This leaves us with ~400 mn of Primaty insurance net profit, which would translate to a “fair” market cap of 4-6 bn for the primary insurance business.

At first sight, this would mean that there could be a 50% upside to fair value for Talanx. However, adjusting for the low free float and average holding discounts and an additional 1 bn in debt, the upside might be only half of that or even less.

If Hannover Re itself would be undervalued, Talanx could be a nice way to play this indirectly, however as I assume Hannover Re is fairly valued, Tlaanx doesn’t look that attractive to me at a supeficial glance.

Summary:

Although this post didn’t generate any “actionable investment ideas”, I still think there is a lot to learn, at least I did. My take aways are:

1) Hannover Re is a good example that a boring business with a moderate valuation can generate very good long term returns with relatively unspectular growth rates (~7% EPS growth per annum)

2) Munich Re is a good example, that share buy-backs are not such a “no brainer” as many investors think, especially when they come at the expense of growth.

3) In the long term, the fundamentally better run business performs better. Period.

4) Hannover Re is also a good example that creating value in Insurance via the actual insurance business might be easier than trying to “spice” things up with more risky investments.

Pingback: Würstenroth & Würtembergische AG | Value Shares

Thanks for your reply. I know the net debt concept is not applicable to insurance companies but I do not know what its best substitute is. Looking only at the gross debt at TLX and/or HNR1 would only tell part of the balance sheet story. We still need to figure out what is going on the “cash” side of things (or whatever substitute of cash makes sense). I really do not know what the substitute for net debt is with regard to insurance companies. That’s my probelm. Maybe someone smarter can enligthen me !

As mentioned, you should focus on Excess capital. Gross debt minus excess capital would be a proxy in my opinion. Forget the cash on the balance sheet.

It would seem to me a fully researched comparison between TLX and HNR1 needs to compare them through the prism of Entreprise Value to account for varying degrees of Net Debt in each balance sheet. I understand the concept of Net Debt is not really applicable to insurance companies. Does anyone have a suggestion to address this issue ?

Not sure if I agree. I think in this specific case it is enough to reflect the additional debt at Talanx level.

Maybe I did not clarify my point. The only way to assess how deep the holding discount is at the TLX level is not to focus on market cap but on EV as there may be an asymmetrical net debt situation between TLX and HNR1. For example, if TLX had a huge net debt and HNR1 had a huge net cash position, the calculations of the discount could be very significantly skewed. Is it clear ?

TLX (including a consolidated Hannover Re) has 1 bn more debt than Hannover Re stand alone. I mentioned this in the post.

Insurance companies do not have a “net cash” postion. They have maybe an “excess capital position” but balance sheet cash is a meaningless number.

Interesting you, Helmut and me looking at HNR/TLX. And each of us drawing his own conclusions.

TLX recently had an investor day, P/B currently looks pretty high (rising rates, lower bond prices) but future ROEs should be somewhat higher.

My issue with TLX is the management and ownership (the majoeity owner simply collects dividends and does nothing with it, no true shareholder perspective).

Comparable to Telekom (look at these big owners), both are theoretically very undervalued with a good asset (TMUS, HNR), but might destroy (or at least not maximize value) at the holding level.

Add: TLX’ managemt is/was incentivized on low-ish ROEs (rfr +800bps)

That’s what makes investing interesting. Very different perspectives on the same stock.

Great article with a non-intuitive comparison, thanks!

Sorry, comments were off.