Notes & impressions from Omaha 2026

This year, after a 7 year break, I once again went to the US to attend the Berkshire AGM. Just for clarification: I don’t own Berkshire shares and unfortunately never did because I always thought that they were too expensive.

Attendance:

As mentioned elsewhere, attendance was clearly lower than in the past. The arena was only half full, the overflow rooms almost empty. On the positive side, with less people it was much more relaxed. On the negative side, prices in Omaha during the weekend are still sky high. Hotel rooms have been very expensive and Steaks in the city steakhouses cost around 60-70 USD (plus sides, taxes and obligatory tip). Most restaurants were only half full. It also seems that hotel prices for the weekend were much lower just before the weekend.

Paying 21 USD for a pretty miserable “Lunch box” during the AGM was not big fun either.

I wonder if Omaha hotels and restaurants will still be able to charge those sky high prices next year.

AGM Content:

Greg Abel is clearly not Warren Buffett. He is much more a “normal”, more operative CEO than Buffett. He also gave more air time to the other Berkshire business CEOs.

What I liked is that they clearly said that BNSF and Geico still have a lot of work to do, in order to become as good as their competitors. Another plus was that the Q&A session was not too long.

On the other side, Greg Abel clearly did not offer any philosophical insights on capital markets. This was different when Warren and Charlie were running the show and attracted the masses. And I think it is a good thing that he didn’t even try to do it.

Buffett himself appeared twice, once in a video and then in a half time break interview with Betty Quick. This interview was actually a little bit “cringe” especially when he mentioned that Greg Abel, a Canadian would become American soon and how special an American Passport is. As a Canadian Berkshire investor, I would be pretty pissed off by those comments as it kind of implies that being a Canadian is not good enough to run Berkshire. In any case, I found it super hard to actually understand what Buffett was saying during the interview.

From an “actionable idea” point of view, the only inspiration I took away from the AGM is the Tokio Marine Insurance investment. This was clearly Ajit’s idea and despite showing his age, this guy knows what he is doing in insurance. It was also interesting that this was mentioned very prominently despite being a rather small position for Berkshire.

Overall it will be interesting to see how this will develop over the next few years. Will Omoha still remain a meeting point for investors from around the world or will there be another kind of Omaha elsewhere ? We’ll find out eventually.

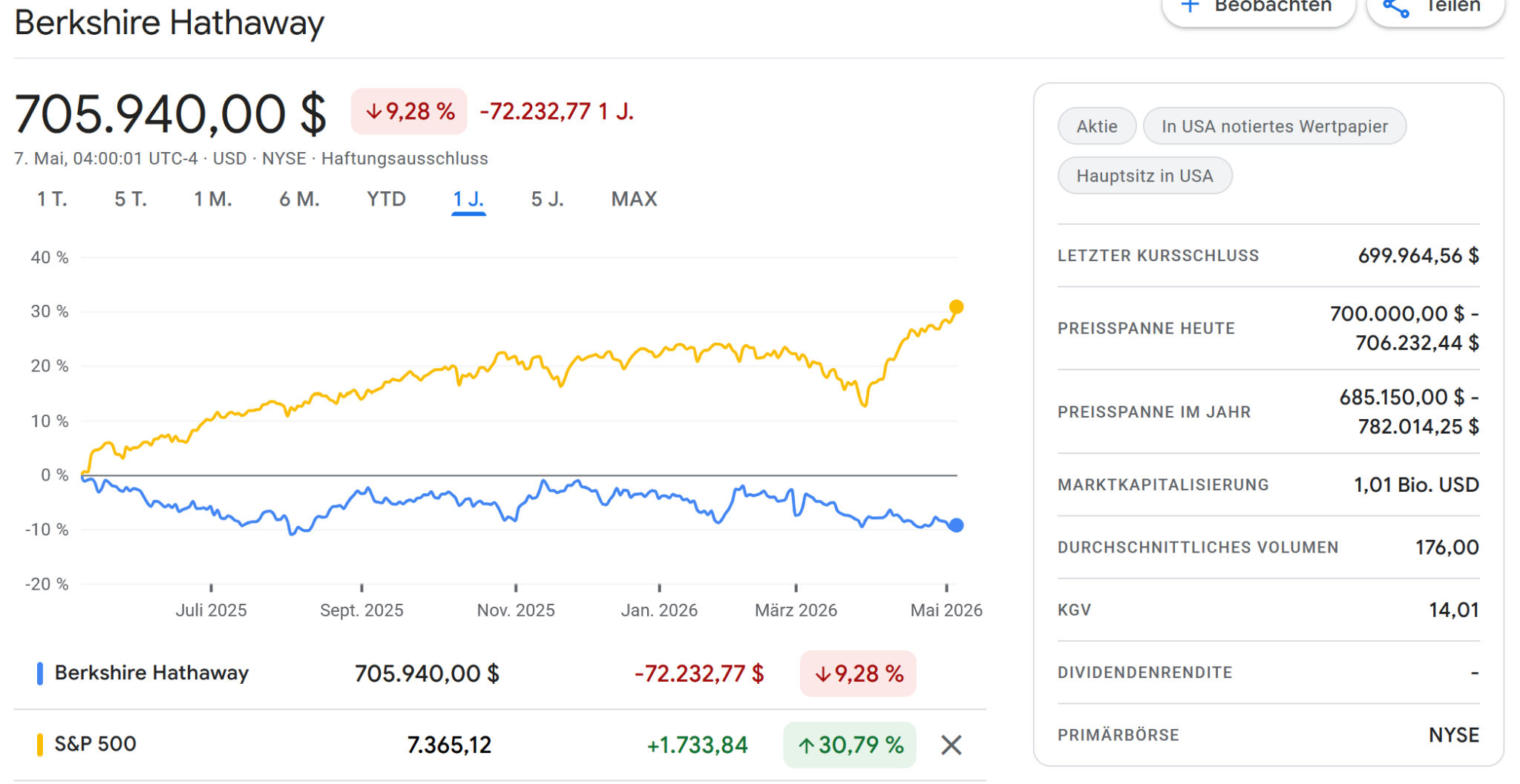

Berkshire Stock

For Berkshire, I do think the biggest risk is that the company will be seen as a “normal” HoldCo or a normal Insurance company. Normal Holdco’s often trade at steep discounts to their “sum-of-the-part” value. Berkshire so far could always count on the “Buffett factor”, but it will be interesting if and for how long this lasts, especially as it is not easy to really understand who owns what (Insurance, Non-insurance) at Berkshire.

Another aspect is that Berkshire in the past was also seen as a good proxy for the overall US economy due to its significant diversification. These days, this is no longer the case as the portfolio lacks exposure mainly to Big Tech/Cloud/KI and Defense which have been the strongest performers over the previous years.

Maybe that will be an advantage going forward but Berkshire is clearly not a good proxy for the overall US economy anymore.

As I mentioned, I was never a shareholder, but at the moment I would be really cautious with the stock. The market seems to think in similar ways:

The most interesting question is clearly, what Greg Abel will do with the cash pile at Berkshire. The AGM provided very little insight into this unfortunately.

General observations:

As in the past, for me the reason to go there is mostly the network of investors and the pre-AGM events. I was again able to attend a two day meeting of German Speaking investors in Omaha and before that did some company visits in Dallas with a group of German “investor friends”. As in the past, the actual Berkshire AGM was always only the cherry on the top.

I actually contemplated for some time if I should go to the US at all because of all the political noise and scary stories about the immigration. However, in my case, immigration was super easy and even kind of friendly (Dallas airport).

As in the past, in all private encounters, Americans are always super friendly. We were often asked by random people in the Supermarket or elsewhere where we come from and when we said “Germany” everyone was super friendly and mentioned relatives or previous visits. So on a personal level, at least the Americans that I met, were as friendly as they always were.

However, in most business settings it was clear that Americans are obviously avoiding to say anything negative about the current US Administration. We never pressed the topic but it is really interesting that no one seems to be willing to say anything critical at all.

In Dallas, one could see quite a lot of Waymos driving around plus some of the autonomous Ubers.

Price levels in general are clearly higher than in Europe. Restaurants, apart from basic Fast food places, are at least 50% more expensive than even in my very expensive hometown Munich, especially if you include taxes and the more or less obligatory 20% tip. It is also interesting how aggressively tipping is demanded even for basic non-service offerings like in airports or coffee shops. Unfortunately this is now much more common in Germany, too.

Another cost factor is that there is very little in the form of public transportation. You either need a rental car or pay for an Uber. Over can be sometimes quite expensive. In Denver, where I had a forced overnight stop-over, I paid almost 60 USD for a 15 minute ride, with Uber charging almost 50% of the total fee at 11 pm.

A final observation is that flying domestically in the US is also a pretty miserable experience. If you don’t pay extra, you will need to wait longer at Security and will board last. Boarding is always a “high stress” event as many Americans travel with the maximum allowed onboard luggage, so compartments fill up very quickly.

My personal highlight was the visit to a real Rodeo outside of Omaha. I have never been to such an event but it was great fun and even good “value for money”.

Will I go there again ?

Currently I am not sure. Overall, it is quite an expensive trip and the main attraction is to meet people that in theory, I could meet much easier in Europe than in far away Omaha. In addition, I had a pretty exhausting trip back.

From a pure financial perspective, going to Omaha is clearly not “great value”. However, on a personal level it was clearly a net positive. experience.