On Buffett’s 100 bn “War chest”

One story which is currently making the rounds is that of Warren Buffett’s huuuuuuuuuuge cash pile or “war chest” at Berkshire.

Bloomberg had an article in May about the 86 bn “war chest” , and then 2 days ago Bloomberg said that his “cash pile” is now close to 100 bn USD.

Speculations are rampant what he could do with it for instance:

There are no signs that anything is on the immediate horizon, but they can’t resist fixating on the record amount of cash piling up at Mr. Buffett’s Berkshire Hathaway Inc. — conceivably enough to manage a transaction with a 12-figure price tag. That would put a takeover of, say, Nike Inc. or Costco Wholesale Corp. in range, to cite examples of companies that might appeal to Mr. Buffett’s tastes.

“A $100 billion deal seems possible” given the cash on hand, said Richard Cook, an investment manager in Birmingham, Ala., whose fund holds Berkshire shares.

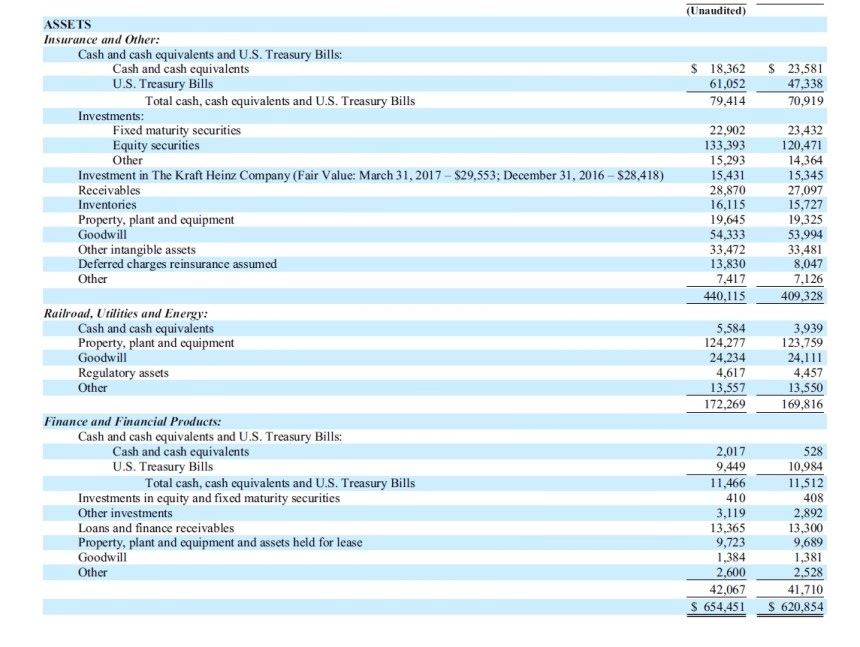

Personally, I am still surprised how little understanding people seem to have of Berkshire and Insurance in general. This is a snapshot of Berkies Q1 balance sheet:

So it is relatively easy to see that in Q1 79 bn cash was inside the insurance (and other)s operations and “only” 17 bn are outside insurance. Now most commentators assume that you can just use the insurance cash the same way as any other cash and go out and buy a Costco or so.

But unfortunately this is not the case. Although Insurance regulation in the US is quite liberal compared to for instance Europe or Australia, you can’t do everything with insurance money.

Some time ago I have quoted this passage from Berkshire’s 2016 annual report:

Berkshire has a partial offset to the favorable geographical location of its cash, which is that much of it is held in our insurance subsidiaries. Though we have many alternatives for investing this cash, we do not have the unlimited choices that we would enjoy if the cash were held by the parent company, Berkshire. We do have an ability annually to distribute large amounts of cash from our insurers to the parent – though here, too, there are limits. Overall, cash held at our insurers is a very valuable asset, but one slightly less valuable to us than is cash held at the parent level.

Fitting to be called the “Oracle of Omaha” he doesn’t tell us specifics, but clearly he knows what he can do with the cash and what he can’t.

Rule of thumb for insurance assets

In order to get a little bit more transparency into his “war chest”, let’s look at a general “rule of thumb” used in the insurance industry:

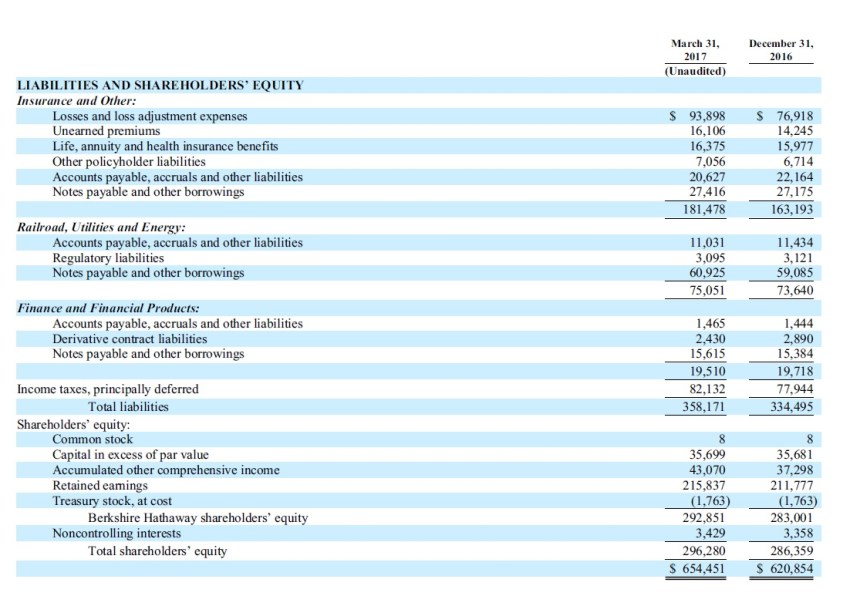

As a rule of thumb in Insurance, you should at least cover your (net insurance) insurance liabilities with (high quality) fixed income and cash. With the rest of that money at least in the US you can go out and buy equities. If we look at the liability side of Berkshire in Q1 we can see that they had around 181 bn of gross Insurance liabilities:

Although I do not have the detailed regulatory filings, I would estimate net insurance liabilities at 181 bn minus 14 bn reinsurance assets minus 29 bn insurance receivables resulting in ~138 bn net insurance liabilities.

If we compare this to the asset side of the insurance part again, we only see 22,9 bn fixed maturity assets. If we add cash and cash equivalents to this, we end up with only 102 bn “fixed income” like securities. This means that Buffet most likely is covering already ~36 bn or 25% of his insurance liabilities with equities. Even under US insurance regulation that looks quite aggressive.

As i said, I didn’t look at the regulatory filings and Berkshire’s reporting is very opaque in this respect, but I think it is highly likely that most of the insurance cash is required to cover reserves. [Technical comment: For some strange reasons, US-based Insurance Groups do not need to publish consolidated regulated accounts. That makes it extremely difficult to understand ANY US-based insurance company from a regulatory point of view]

The cash pile within insurance most likely in my opinion is a bet on rising interest rates and Buffett at some point in time will convert them back into longer term and higher yielding fixed income.

Looking at Berkie’s balance sheet, i am not even sure if the 11,5 bn cash in the financial segment are freely available for acquisitions or if cash in regulated utilities or railroads can be used easily.

Summary:

So at the end of the day it think it is much more realistic that Buffett’s huge “war chest” on a consolidated level is much more an “intra insurance” interest rate bet than a freely available 100 bn USD war chest to buy each and anyone.

Clearly he can raise cash by selling existing equities, but his “organic” cash reserve for acquisition in my opinion is rather limited, maybe something in the area of 10-20 bn USD. But I think it is more realistic that we will again see debt financing liek in the Precision Castparts acquisition.

Oh, and for the Fans of the so-called “Buffett Berkshire buy back put”: You can’t buy own shares with insurance money either……..

P.S.: I am not sure if anyone uses EV based multiples to value Berkshire, but to be on the safe side one should add the insurance liabilities to total debt. And no haircut, unless you also deduct the insurance earnings.

Edit:

Many comments start with “Buffett said this” or “Buffett said that. I would recommend however to read the actual insurance regulation. For instance this:

http://www.naic.org/store/free/MDL-280.pdf.

Section 26 is the relevant one…..

Lol I dunno, Munger has been on record saying they could do over $100Bn deal if they wanted (obviously they don’t thread lines), and Buffett has commented similarly. Has Buffett been known to mislead shareholders, ever? Either he’s lying and flaunting the rules with which he has been familar since he began building current-form Berkshire in 1965, or the author of this piece is dead wrong and picking bones for reasons which are unfathomable.

Actually, why don’t we just check back on this article’s premises / conclusions about the way in which regulations apply to Berkshire (i’m sure a 65 page regulatory document covers the myriad jurisdictions in which berkshire operates…) in a few years? Or better yet, why doesn’t the author merely pose this question at a berkshire meeting? (it seems an intelligent enough question; to get attention, pose the Q in German and send it to one of the german-speaking journalists who do the Q&A at the meeting).

IMO, The poster Jose had the right logic. One last thing: buffett doesn’t build up cash as a bet on interest rates etc. (Analogy: Sure, if you buy a home using a mortgage, you’re short the dollar, but you bought the home to house your family, not to short the damn dollar.) Cash is merely a residual, growing when opportunities in the market are light, and contracting when opportunities are aplenty. This is such an obvious point that it bewilders me when pundits try to explain it as a macro play, or his grandwizardry understanding of credit cycles.

Of coursr can Berkshire do a 100 bn deal, but hat might involve significant debt and/or Berkshire stock. They used debt even for the relatively small Precision Castparts acquisition.

And no, cash is not simply a residual in an insurance company. I guess you might do some research on how insurance companies actually work.

I’m not sure that the 2nd paragraph of that reply is fair re: cash buildup. In this post and in comments it was suggested that buffett’s cash or spending power buildup (to be more accurate) is “an interest rate bet.”

I’m saying that isn’t necessarily true since he can knock 2 birds — avoiding tying up long term capital in 33x p/e fixed value investments and freeing up potential capital for no-brainer equity-coupon investments like BNSF — all with one stone (i.e. Letting cash or spending power build up). It doesn’t have to be a bet on interest rates. Das is est.

What I don’t think is knowable or all that useful to know is how Berkshire’s myriad governing jurisdictions treat insurance assets as applied to its uncashed claim checks (liabilities). This is particularly true since, reserve requirements against float differ from asset to asset (it’s not black or white; see DJCO 2016 where Munger comments about MidAmerican’s recent massive solar farm investments, which are held under their insurance subsidiaries, strongly implying for the added leverage those assets confer).

I love your blog but I think on this occasion you are wrong.

Berkshire has 110B of float and to cover this they have nearly 100B in cash, 23B in bonds and 152B in stocks (including Kraft Heinz at fair value) and 20B at fair value of other investments (BAC and RBI preferreds and warrants mainly) Also I believe that some of not all of the businesses they fully own are not in the holdco but inside the insurance subsidiaries. For example BNSF that could be worth 60-70B at comparable multiples.

That would give us a minimum of 350B in assets to cover 110B of float.

Of course you need capital, you can discount 27B of debt in the insurance, discount the equities because of their risk, income taxes deferred etc. But it is hard to argue they have only 10-20B of dry powder for acquisitions currently.

They had 25B of cash as recently as 2010 and their float has increased only 30 B or so since then. Their equities have increased greatly since as well.

To wrap it up, the question was put to Buffett and Munger and Munger said that they could do a 150B deal if needed (I presume that would include a good chunk of debt), Buffett thought that it would be smaller than that. In any case Buffett has stated that their minimum cash holding us higher than the 20B it was. Probably between 30-40 so I think they could do a 60-70B deal without taking much debt

# Jose, first small correction: berkshire has 180 bn of insurance reserves as of q1 2017. Plus it increased by almost 20 bn USD in Q1 2017 alone, so I guess your numbers are somehow outdated.

I also find it interesting that people only read waht Buffett says but not what regulation says. Suggested reading from my side for instance would be:

Click to access MDL-280.pdf

Insurance regulations are complex and change from country to country and state to state within the US. What we can not say is that equity holdings within insurance companies do not count towards covering the insurance liabilities. There are limits for sure but not ALL reserves have to be kept in cash and bonds.

If you would be right how would you explain that in 2010 Berkshire had 28B of cash and 33B of bonds to cover 65B of float.

Where their insurance subsidiaries bankrupt then and nobody knew it?

The answer I think is that Berkshire is so overly capitalized as a whole and so diversified (they most likely would turn a profit in a year with higher CAT events than what he have ever seen) that regulators give them flexibility regarding where they invest their float.

I haven’t said that all reserves have to be covered in cash or bonds. This was explictly mentioned my rule of thumb. However even the most flexible regulator will not allow him to cover all his reservs with equity. The truth is somewhere in between. By they way, if you would actually read the link you i posted in the last comment, you might find the solution 😉 (hint: Section 26….)

And just to mention again:: Due to the specifics of US regulation, a US insurance group can be in total insolvent long before the regulators will see it. But clearly, Berkshire is not insolvent, however I still believe that they have more or less maxed out the equity portion covering the float.

I agree with the above, it looks like buffet wants to minimize the duration risk in his portfolio (similar to Fairfax), Its interesting that Berkshire doesn’t disclose the duration of its insurance liabilities and its relative solvency position. does anybody know where to find this?

Berkshire has kept their bond holdings at a very low level of20-30B for years now. He hasn’t sold recently to cover duration risk. He is on the record numerous times saying that bonds are in a bubble and he thinks they are a terrible investment at the moment. A 30 year treasury at 3% is priced at 33p/e without any hope of increasing cash flows for the duration of the bond. In Europe is even worse with German 30 year at a 80-100 p/e. Even if somebody could see the future and guarantee that there is no duration risk it is still a terrible investment.

again as mentioned before. My argument is about insurance regulation and that you have to hold a certain amount of cash/fixed income against your reserves, no matter how attractive (or not) interest rates look like.

With this argument some may be misled into thinking a good chunk of Berkshire’s insurance liabilities could all come due rapidly. You know, like if 30% of drivers out there had a major accident the same year (picture a Godzilla movie where people, in feverish panic, crash cars into each other). Unlikely.

I think one might also consider the cashflows of the privately held businesses and the net worth of those businesses. By the way, AM Best journal has more regulatory disclosures just subscribe.

This has nothing to do with cashflows but with insurance regulation.

Wow, great stuff as always. Your ability to explain things so clearly will serve you well in life.

WEB always talks about keeping a spare 30-40 billion or so around for disasters, so I never take the 100bn cash numbers as available anyway, but what I didn’t fully appreciate is that he is not being necessarily conservative by doing that, he is just following the rules.

Great article, as ever, thanks!

I guess the implication of all this is that Buffett is actually fully invested in the ares where he has complete freedom and so therefore he does not consider the market wildly overpriced, something which he’s said directly a few times various places the past few months. Worth thinking about when deciding how much cash to hold. I tend to agree – most listed businesses offer a shareholder return in the 5% region, which is reasonable given where bonds/interest rates are – that this figure is unreasonable given history is I think irrelevant.

My views are that Buffet may perceive that the tradeoff market prices / risk is unattractive and he may not feel comfortable with it. Second is that the man is at the end of his (brilliant) career; and like athletes, he probably wants to retire on the winning side (which in his case means not taking unnecessary risks right now).

Just for clarification “net insurane liabilities” translates to actuarial reserves, and “rest of that money” (ie. money hold by insurers) should be linked to the risk capital hold to cover major events…

Not really. Net insurance liabilities equal gross insurance liabilities minus directly insurance related assets (recoverables, premium reserves). “Rest” is equity to cover capital requirements.

Thanks for clarifying!

What if he’s building up his cash position because he sees less opportunities to deploy it in the current market? An option to be able to buy more bargains in the future?

My argument is that from a regulatory point of view he will not be able to invest the existing insurance cash into stocks or even a complete company.

But I agree, the common opinion seems to be that he builds up cash fot a really big “lephant” deal, but as explained in the article, I think it is only an interest rate bet.

I am not sure but in case of BNSF, the insurance subsiderie’s(National Indemnity Co) cash was used to build an initial stake. In the case of final takeover, I am not sure if it was it done through insurance subsideries or not.

Any way some part of that 100 bln could be used to buy shares in secondary markets.

yes, many of his stock positions are held by insurance company. But my argument is that there is a limit for that and my rule of thumb stells me that he is actually very close to that limit (including listed stocks in secondary markets).

Good stuff. Thanks.