Synchrony Financial (SYF) – a Spin-off that is better than its Parent GE ?

While looking at General Electric some days ago, I remembered that I had the IPO/Spin-off GE Capital Credit Cards which is now Synchrony Financial on my research list for quite some time.

![]()

Company Background

This is from the 2016 annual report explaining how Synchrony was separated from GE:

The Company was previously an indirectly wholly-owned subsidiary of General Electric Capital Corporation (“GECC”) until the closing of the initial public offering of our common stock (“IPO”) in 2014, which reduced GECC’s ownership in the Company to approximately 84.6% of our common stock. In November 2015, Synchrony

Financial became a stand-alone savings and loan holding company following the completion of GE’s exchange offer, in which GE exchanged shares of GE common stock for all the remaining shares of our common stock it owned (the “Separation”)

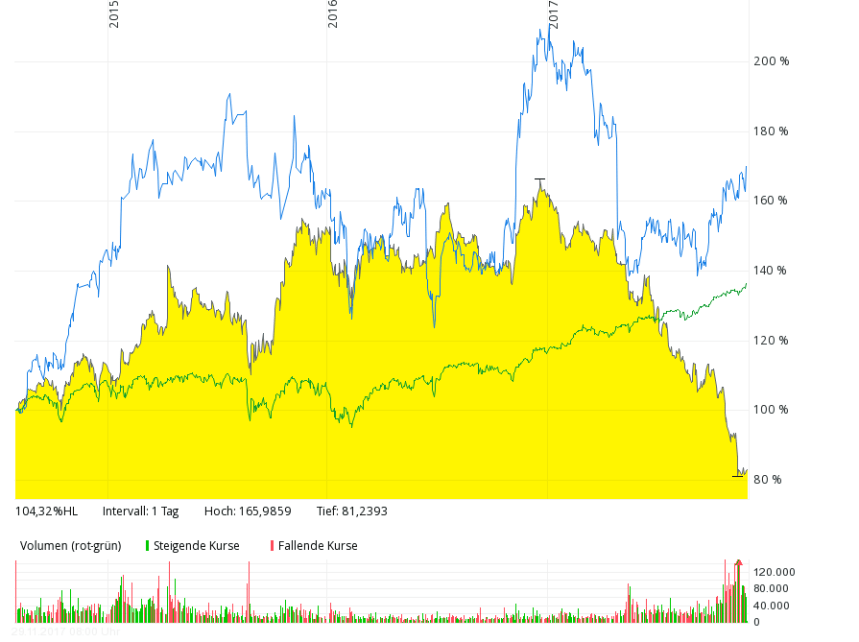

Back then in 2014, Jeff Immelt thought that in order to increase the share price of GE, it is better to dispose as much of the financial business of GE as possible and concentrate on the industrial business. Looking at the stock charts, so far it doesn’t look like such a great idea as Synchrony has done a lot better than both, GE and the S&P 500 (Synchrony in blue):

A few numbers (at ~37,50 USD/Share):

Market cap: 29,3 bn USD

P/E 2017: 14,4

P/B 2,0

ROE: 15%

Div. yield 1,60%

The business model:

The business model is nicely explained in the annual report:

“Our business benefits from longstanding and collaborative relationships with our partners, including some of the nation’s leading retailers and manufacturers with well-known consumer brands, such as Lowe’s, Walmart, Amazon and Ashley Furniture HomeStore. We believe our partner-centric business model has been successful because it aligns our interests with those of our partners and provides substantial value to both our partners and our customers. Our partners promote our credit products because they generate increased sales and strengthen customer loyalty. Our customers benefit from instant access to credit, discounts and promotional offers. We seek to differentiate ourselves through deep partner integration and our extensive marketing expertise. “

Synchrony offers credit cards in the form of so-called “store cards”: These are credit cards which can be used in certain stores only. The advantage for the stores is that they don’t have to pay the typical credit card fees on each purchase which are usually around 2-3% for normal credit cards. On top of that, the stores even participate in the money made from extending credit to consumers who pay for the card.

For many retailers with razor-sharp margins, not paying credit card fees has a significant impact on the bottom line and so they are happy to promote those cards as much as possible by offering discounts on their merchandise which then again in theory should attract customers to use those cards.

So this is a very different business model to Amex (or Visa or Mastercard): For instance, Amex tries to win customers by offering significant rewards for using the card but the stores accepting Amex have to pay for those rewards by the significant fee Amex pays on each purchase. An additional advantage for the stores lies in the fact that they gain access to all the data from the store card whereas they have zero access to the data of normal credit cards.

The disadvantage for a store card provider like Synchrony is clearly that they have to live off interest charged for the actual credit only. There is no transaction fee income like for instance at Amex or Visa or Mastercard.

There is a much better comparison of the business models at Punchcard Blog, I highly recommend to read it.

Some KPI Data:

If we compare 2016 with 2013 (last year under full GE control), top line growth was quite nice but bottom line growth was almost non-existent. What looks especially bad is the fact that Return on assets decreased significantly. However this is a result of a much larger capital requirement as stand-alone company. During GE, the business had only minimal capital and benefited from the strong GE rating.

Cost of debt clearly increased since the separation. Synchrony is now a BBB- credit and needs to pay up. We can also see that the amount of credit losses has been increasing.

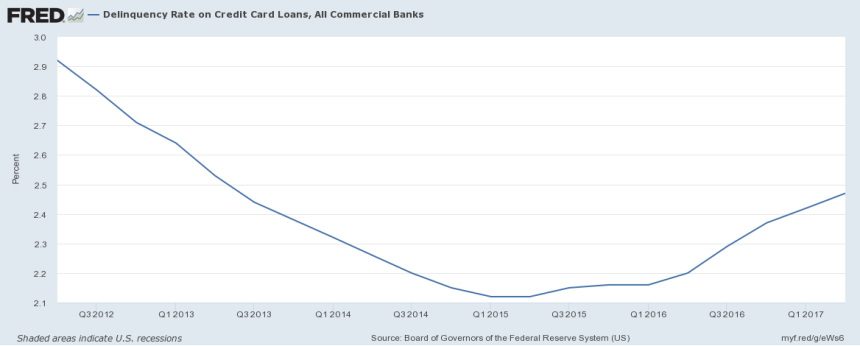

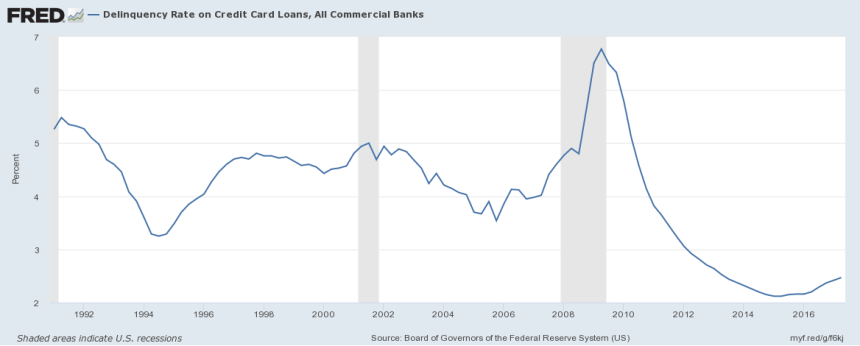

However this si not a Synchrony specific problem but a problem in the US in general as this graphs show:

Longterm it looks like that there is still room for things to get worse.

Synchrony’s store cards contain a significant amount of “sub prime” credit and loss rates are in general “above average” for US credit card companies.

So this is clearly an issue to watch out if and how delinquencies in the US develop.

Shareholders:

Synchrony has some famous Value Investors as shareholders. Baupost owns 3,7%, Berkshire 2,7% and Frist Eagle around 2,3%. Berkshire increased it’s Synchrony stake just recently.

Pro’s / Cons

As always I do a Pro and Con summary from my side at this stage:

Pros

+ relatively cheap and good underlying growth potential

+ business model different from AMEX, Visa (retailer driven)

+ hosts among others, Amazon’s credit card

+ recession hedge via reduced “kick backs” to stores

+ business model (credit) less vulnerable to financial disruption

+ good and transparent reporting

+ reasonable capital allocation policy

+ cheap deposit funding

+ still unloved industry

+ GE “genes” should mean good management culture

+ As an US based company, the potential decline in corporate tax would directly increase after tax profit

Cons

- high yielding consumer debt

- Charge offs increase

- risk of programs not being extended (high concentration on Walmart)

- low bottom line growth since separation

- loss normalization or deterioration ?

So all in all a lot of fundamental pro’s vs. a few con’s.

Concentration risk:

If we look at their customer list, the largest 5 account for 54% of their business. 2 of the 5 are actually Walmart. So I would assume that Walmart really is the biggest client with a significant percentage of their business:

Our five largest programs are with Retail Card partners: Gap, JCPenney, Lowe’s, Sam’s Club and Walmart. These programs accounted in aggregate for 54% of our total interest and fees on loans for the year ended December 31, 2016 and 50% of loan receivables at December 31, 2016. Our programs with JCPenney, Lowe’s and Walmart each accounted for more than 10% of our total interest and fees on loans for the year ended December 31, 2016. Sam’s Club is a subsidiary of Walmart that is a separate contracting entity with its own program agreement with us, which

we report separately from the Walmart program. For purposes of the information provided in this paragraph with respect to Walmart, the interest and fees on loans from the Sam’s Club program have not been included.

The length of our relationship with each of these five Retail Card partners is over 17 years, and in the case of Lowe’s, 37 years. All of these program agreements have been renewed in recent years and expire in 2019 or beyond

Valuation:

As I like to keep things simple, therefore my valuation model looks also quite simple. For me a P/E of 15 would be a long-term “fair” P/E for a company like Synchrony which I would consider a “quality financial” firm. With a current P/E of around 14,4, there is little room for multiple expansion.

So any return needs to come from growth. They seem to be able to grow the topline by around 9-10% growth but so far this has not flown to the bottom line. If losses do not deteriorate much further, top line growth should translate into bottom line growth as some point in time. As a financial company, growth requires profit retention, so my total expected return going forward would be the growth rate (9-10%) plus the dividend yield which is currently 1,6% plus maybe some share count reduction. Overall this results in something like a 10-12% return per annum which for me is unfortunately not enough, especially compared to the risk of further deteriorating credit quality.

For me, Synchrony would be more interesting at a price of around 30 USD (all other things equal).

Summary:

Synchrony Financial is an interesting company. They have a good business model and seem to be well-managed. On the other hand there are also fundamental headwinds like increasing default rates and reliance on a few big customers.

For me the stock at the moment looks too expensive. If for some reason the price would come down 20% or so I would be a buyer.

Pretty bad news:

https://www.wsj.com/articles/the-10-billion-tussle-over-walmarts-credit-cards-1540378800

For the time being, “OFF watch list”…..

Are you now a buyer?

No. They just lost their biggest account with Walmart:

https://www.bloomberg.com/news/articles/2018-07-26/synchrony-falls-on-report-capital-one-wins-walmart-card-business

I think this is not an easy case and I will pass as it is too difficult for me and the stock is too “high maintenance”.

Why do you think that Berkshire and Baupost invested if you are only expecting 10-12% return? Do you think that return is enough for them, or that they see more upside somewhere?

maybe because they are smarter than I am ?

Also, how would a new retailer decide which card issuer to go with? How do they choose between Synchrony or ADS or somebody else?

Is there anything that prevents their business from being commoditized?

I guess they need to be either better or cheaper than the competition. With around 40% market share they seem to do something right.

hi,thanx for your post.

what do you mean by “As a financial company, growth requires profit retention…” ? what do you mean by profit retention and why the grow requires it in financial company and not other company ?

and why you assume the return equals to growth plus dividends ?

thank you.

The issue is that for regulatory reasons, a regulated company like Synchrony needs to maintain a certain amount of “hard” equity capital as a percentage of their loans. The higher their loans the higher the requirement. And this has to be funded upfront in “hard cash”. Other companies can spend whatever cash they are earning to finance growth but regulated financials cannot.

My assumption that return equals growth plus dividends is maybe conservative but I think not unrealistic.. As I said, I like to keep things simple.

but still you didn’t explain why you assume that the down line (which was over the 6 years- 1.5%) growth will be the same as the top line growth (9-10%) ?

Well, at least Synchrony processes the Amazon card as well….

From a recent Wall Street Journal article store cards have two growing problems. As more shopping is done on Amazon.com the store cards will see less and less use since they generally can only be used at the named store. Second, with many subprime customers, delinquencies will increase as customers no longer visit those stores (probably because the nearby one has closed) they will not see the need to pay off a balance. Also in spite of a growing economy and low unemployment bad card debts are increasing; what happens when the economy is not doing so well ? Today’s WSJ also has an article on discount chain Dollar General chain; they are finding more and more opportunities in communities where people no longer have any spare cash.