Kinder Morgan (KMI): Slow moving train wreck or Contrarian opportunity ?

In late 2014 I started looking into oil related companies. I have looked at a couple of energy related companies like explorer Peyto, LNG liquification terminal Cheniere , Consol Energy and Gaztransport. I only bought Gaztransport which I then sold 6 weeks later. As I am still interested in the Energy sector, I will cover some stocks from time to time.

Kinder Morgan, the US pipeline owner/operator looks like another typical potential contrarian “Value investment”.

![]()

What I liked at first sight:

- the overall sector is clearly out of favor and for some time now

- KMI lost more than 60% of its stock price over the last 6 months or so, mainly due to a dramatic reduction in dividends

- the underlying business (regulated pipelines) is solid and less exposed to oil prices than many related industries

- Natural gas as a subsector in my opinion is the only clear winner of fossil fuels

- the management is supposed to be good and aligned with shareholders

- Berkshire has been buying into it lately

What I don’t like:

- KMI is highly leveraged

- Lots of goodwill from previous acquisition/restructuringa

- extensive use of “adjusted numbers” / own metrics

- non-regulated pipeline assets

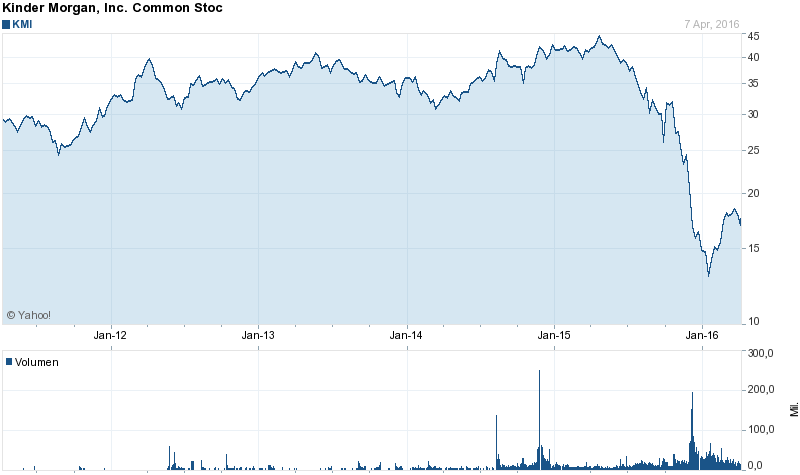

This is how the stock price looks like over the past 5 years:

Interestingly, the stock was still going strong until an all time high in April 2015. The drop in the share price however accelerated in December when they announced to cut ther dividend by about 75%.

The business

Oil and NatGas pipelines are very long living assets. I found this report about US Natgas pipelines which shows that around 60% of the US NatGas piplines are 45 years old or older. This implies that technological change seem seems not to be that fast, an important feature for any long term investor.

Pipelines are a typical “infrastructure” investment. Once there is the first one, it does make very little sense to put a second pipeline next to it. In many cases, the pipelines are regulated, especially with regard to required maintenance and safety standard but also with regard to the prices that can be charged.

The value of any single pipeline is not the (historic) cost to build it but the cashflows to be expected. Pipeline capacity is usually sold over many years to Energy companies and/or municipalities. So one could to a certain extent compare a pipeline to a commercial real estate plot with different tenants with the duration of the contratcs and the creditworthyness of the counterpart playing a significant role in how to value the assets.

This means however that similar to real estate, leverage is clearly part of the game. Like Warren Buffett does at Burlington or his utilities, relatively stable cashflows can be levered up to create higher ROEs.-

Trying to “kill” the investment case

As always, I try to “kill” the investment, which looks easy at KMI. Let’s walk through the points I don’t like:

1) Leverage

With enough leverage, you can transform any safe asset into a potential disaster. KMI has lots of debt. 41 bn USD net debt compared to a market cap of 40 bn USD. They currently have a BBB- rating (stable outlook).

The biggest risks in my opinion with leverage are the following:

a) lumpy maturities which can create liquidity issues

b) covenants which can force early maturities

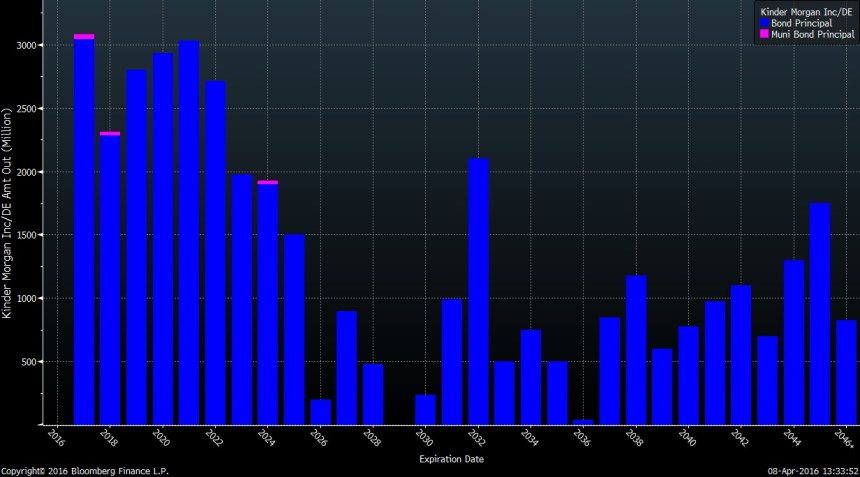

Let’s look at the maturity profile of KMI:

What we see is a pretty evenly spread out maturity profile. With Free cashflow of around 4-5 bn USD p.a. (after maintenance Capex), KMI theoretically could pay down the debt as it becomes due if it doesn’t pay dividends and keeps new investments to a minimum. This is a very good position despite the high debt load and in my opinion a sign for good Capital Management. This is actually what they are doing in 2016. They communciated that after cutting the dividend, they have no need to access the capital market in 2016.

It is also important to know that the outstanding debt is all “non covenant” senior debt. Looking into their 10-K the only covenants are to be found in a 4 bn revolving credit line:

Debt Covenants

As of December 31, 2015, we were in compliance with all required financial covenants. Our credit facility included the following restrictive covenants as of December 31, 2015:

• total debt divided by earnings before interest, income taxes, depreciation and amortization may not exceed:

• 6.50: 1.00, for the period ended on or prior to December 31, 2017; or

• 6.25: 1.00, for the period ended after December 31, 2017 and on or prior to December 31, 2018; or

• 6.00: 1.00, for the period ended after December 31, 2018;

• certain limitations on indebtedness, including payments and amendments;

• certain limitations on entering into mergers, consolidations, sales of assets and investments;

• limitations on granting liens; and

• prohibitions on making any dividend to shareholders if an event of default exists or would exist upon making such dividend.As of December 31, 2015, we had no borrowings outstanding under our five-year $4.0 billion revolving credit facility, no borrowings outstanding under our $4.0 billion commercial paper program and $115 million in letters of credit. Our availability under this facility as of December 31, 2015 was $3,885 million.

So they do have some covenants but as they haven’t actually drawn the line (and not issued any CP either), so a covenant breach would have zero impact. By the way, it is much easier to renegotiate covenants if you have not drwan the line….

Overall I find that their debt load is relatively appropriate and manageable, especially after cutting their dividend (more on the dividend cut later).

2) Goodwill

Goodwill as of 12/2015 was ~ 24 bn. Based on common equity of 35 bn, this leaves only 11 bn “tangible” equity.

Looking into the 10k on page 105 we can see that the majority of Goodwill is allocated to regulated assets (16 bn). Goodwill for regulated assets in my opinion is less problematic as cashflows are relatively safe.

They give a pretty detailed picture how they test goodwill, the most relevant in order to have a basis for the valuation is this quote:

Based on the weighted-average cost of capital of the peer group, we determined the appropriate rate at which to discount the cash flows is 8%. Each 100 basis points change in the discount rate changes the estimated fair value by approximately 5%

The sustained decrease and the long-term outlook in commodity prices have adversely impacted our customers and their future capital and operating plans.Acontinued or prolonged period of lower commodity prices could result in furtherdeterioration of market multiples, comparable sales transactions prices, weighted average costs of capital, and our cash flow estimates.Asignificant change to any one or combination of these factors would result in a change to the reporting unit fair values discussed above which could lead to further impairment charges.

When one looks at Kinder Morgan’s presentations over the year 2015, one can see that they seem to have underestimated to a certain extent the impact of the low energy prices and the reactions of Rating agencies, in particular Moody’s.

Until September, they had a slide in each investor presentation which still claimed the following:

Greater dividend growth and visibility — 2015 budgeted dividend of $2.00 (15% growth over 2014) — 10% annual growth expected through 2020 — Expect substantial dividend coverage, even in lower commodity price environment

Funnily enough, at a Barclay’s investor meeting at the same day, that slide was already missing. And it never reappeared thereafter.

The first indication that there were bigger isssues with the rating agencies was the issuance of the mandatory convertible in October. They mention that one of the reasons for issuing these securities was:

Maintain investment grade credit rating

and that:

S&P, Moody’s and Fitch will provide 100% equity treatment to this mandatory convertible security

In November then, they still guided for the following:

Preliminary 2016 dividend per share growth projection of 6-10% over 2015

Then however, despite the Mandatory Convertible, Moody’s threatened to downgrade them in the beginning of December 2015. This clearly put pressure on Management as this Forbes article well explains.

Very shortly thereafter they cut their dividend down to 50 cents for 2016. According to the article, Moody’s directly reacted:

Moody’s Investors Service upgraded its outlook to stable from negative, reversing a Dec. 1 warning that Kinder Morgan’s debt could be headed for non-investment grade.

For anyone with some experience with rating agencies (as an issuer) it is not that difficult to understand the timeline of those events. Rating Agencies are notoriously bad in plain communication and change their view quite rapidly if the overall environment deteriorates.

The major mistake of KMI in that regard was that they were maybe a little bit to close at non-investment grade and didn’t want to risk a down grade to “junk”.

Personally, I think it was right to defend the investment grade rating but communication was clearly not optimal for a shareholder oriented company.

It seems that the stock was owned mostly by “dividend investors” who got sppoked by this. Here for instance someone

is complaining that not paying dividends hurts shareholders. Or here a write up and valuation from 2014 with dividend yield being the sole factor in the valuation.

I think there is one very good lesson there for everyone: Paying or not paying dividends does not have a lot of impact on intrisic value but it seems to be that sometimes there is a big impact on price.

From a value investor perspective however, that makes the case interesting. If The dividend cut is truly the case for much of the share price drop, then this could be an excellent opportunity for a potential value investmetn.

Summary:

To my own surprise, the first attempt at “killing” Kinder Morgan as an investment was not successful. Both, leverage and Goodwill are not a big problem in my opinion and the underlying business looks very solid. The use of adjusted numbers seems to be OK considering the characteristics of the business.

This clearly justifies a deeper look into the company to see how the potential upside looks like.

TO BE CONTINTUED SOON……

Hi mmi,

You might be interested in reading this:

https://punchcardresearch.com/2016/06/07/mlps-be-cautious-when-the-boring-is-made-exciting/

cheers! Seb

After reading your article I started to look into KMI myself. Usually I just ignore Goodwill when analyzing a balance sheet but after you wrote “Looking into the 10k on page 105 we can see that the majority of Goodwill is allocated to regulated assets (16 bn). Goodwill for regulated assets in my opinion is less problematic as cashflows are relatively safe.” I was wiling to consider to take in the Goodwill.

On the other hand the company descripes Goodwill as “After measuring all of the identifiable tangible and intangible assets acquired and liabilities assumed at fair value on the acquisition date, goodwill is an intangible asset representing the future economic benefits expected to be derived from an acquisition that are not assigned to other identifiable, separately recognizable assets. We believe the primary items that generated our goodwill are both the value of the synergies created between the acquired assets and our pre-existing assets, and our expected ability to grow the business we acquired by leveraging our pre-existing business experience. ”

Doens’t that mean that the relatively safe cash flows have nothing to do with the Goodwill as they wlll be represented in the fair value of the pipelines at the acquisition date? I understand that the Goodwill soleley depends on KMI’s ability to create synergies and grow the business. Although that is not necessarily unlikely I don’t really see why this is more likely than Goodwill created from other companies also hoping for synergies and extra growth.

Could you elaborate a bit more why you think that Goodwill is not so much of an issue in this case? To me it still seens to signal that optimistic prices have been paid in the past and a fair share of that equity could be lost.

I am not sure if I understand your question fully. Goodwill is created when you buy an asset above its “book value” or tangible net assets. In the case of a pipeline purchase, this means the price above the “tangible cost” to build the pipeline minus depreciation. As the value of a regulated pipeline does not relate to the cost to build it, but the ability to charge (monopoly) fees, I feel more or less comfortable with such a kind of goodwill. What KMI says is that they can create even more value on top of the Goodwill created at acquisition by realizing synergies etc.

I see your point if you assume that Goodwill is created if the purchase price is above book value but KMI states that Goodwill is created when they buy an asset above its “fair value” not its book value. According to IFRS 13 the fair value is basically the market value. If that is the case the Goodwill can only be valuable if KMI can do something with the asset nobody else can…

No I think you are reading this wrongly or the explanation is not precise. I wouldn’t get hung up on book value anyway. Cash generation is much more important.

Are you sure the debt/bonds don’t have a Cross Default clause and would be due after a covenant breach of the RCF facility?

If you breach the covenant and nothing is drawn then there is no cross default.

how are bonds structured junior / senior / maturities and where do they trade price-wise ?

I would want to add two points to your thoughts on potential risks to the investment:

1. The demand for pipeline transportation is reasonably static. While this is probably generally true, shifts in the main locations of supply (for example a sizable shift in shale production in areas not covered by the KM network) or even different price differentials can render certain pipelines obsolete. I have not looked at this specific case, but it might be worth thinking about.

2. Customers continue to pay the agreed tariffs and are not able to renegotiate their contracts or simply default. Given the pressure faced by many oil and gas companies at the moment, this could be an issue. There is most likely a link to point 1. If KMs pipeline network is still needed in the current environment, they will be able to resell if someone defaults (potentially at lower prices), if not such a situation would be much worse.

thanks for the comment. Indeed single pipelines can become less atttractive for the mentioned reasons. KMI in my opinion (but I am not an expert) however has a good portfolio and Rich Kinder has a pretty good track record buying/building the right pipelines.

Lots of ink on KM spent by various contributors of Seeking Alpha… have a look.

I looked at a few oif them but didn’t see anything interesting. Most were pretty much focused on dividends.

have you though about looking at the best of bread in this sector? (i believe they are Magellan and Enterprise)

Why do you consider them “the best” ?

That’s common knowledge among the industry ( I am not a part of it) I think they are both mange Thierry debt load more readably and do not dilute their partners. Kmi used to pay lots of dividends and at the same time issue more shares which reminded some of a Ponzi scheme. Do you know Kevin Kaiser from Headgeeye?

QUOTE: Overall the situation reminds me a little bit what I read abouth John Malone and Liberty. If you run a company gathering long term assets, it is actually a pretty clever strategy not to show high GAAP earnings and pay a lot of taxes, but to depreciate aggresively in order to reinvest “before tax”.

———————————

GAAP accounting has nothing to do with the tax they pay to the IRS. (With the exception of weird situations like LIFO / FIFO inventory accounting, where GAAP rules force the company to match the LIFO/FIFO choice used for IRS accounting.)

I don’t fully understand your post. Yes, KMI has due to the merger a different tax basis than GAAP book values. But for any new projects, GAAP will be the starting point for taxes. KMI will clearly try to depreciate any asset as quickly as possible to lower the tax bureden. This has nithing to do with FiFo/Lifo investory accounting.

GAAP is not the starting point for taxes.

GAAP accounting and IRS accounting are generally two different things. You can depreciate things differently for the GAAP set of books versus the IRS set of books.

I hope that makes more sense.

Point taken. let me rephrase my initial statement the following way: I guess the clearly write down everything as quickly as they can within the IRS books and don’t care that much about GAAP earnings.

Are you sure that free cash flow is 4-5bln? I see it at 1.4bln in 2015 after 0.85bln in 2014. Operating CF is at around 4-5bln but that doesn’t really help much in terms of servicing debt, does it?

It depends how you define Free cashflow. Free cashflow after maintenance capex is around 4 to 4,5 bn. the number you stated is after expansion capex. This is something they have under control. They can invest less and pay back some debt if they want.

Will you consider looking at the warrants, too?

which warrants ?

May ’17, $40 strike. While you should not follow others, Tepper purchased some KMI stock, along with warrants.