The return of the “Freedom Energy basket”: ABO Wind vs Energiekontor (BUY)

Dislaimer: This is not investment advice. PLEASE DO YOUR OWN RESEARCH !!!!

Background:

Some of my readers might remember, that I bought into a “Freedom energy” basket in March 2022 in order to “hedge” against potentially catastrophic effects from the Russia/Ukraine war. After a first nice run, I sold 3 out of the initial 4 (7C Solar, PNE, Energiekontor and ABO Wind) and only kept ABO Wind because I considered it the most undervalued stock.

Looking at the chart we can see that for some of the stocks of that basket, not so much happened, only PNE is still significant above the level of March 2022 (ABO Wind is the solid Yellow chart):

ABO Wind is my remaining Renewable Energy investment with a weight of 3%. The basis of the thesis was, that the stock is relatively cheap and that due to a significant ownership stake of its founders, long term interests of Management and shareholders should be well aligned.

In addition, I do think that the value creation potential for developers in the current environment is significantly higher than for pure “operators” such as 7C or Encavis.

Germany: Something is happening here

Some might remember the Speeches of German politician, calling renewable Energy “freedom Energy” from last year. A lot of stuff was announced, especially lofty targets for more Renewable energy, but initially little or nothing happened. However now, after almost 1,5 years, things in Germany are moving. One thing in particular stands out: It really looks like that Onshore Wind permits, that used to be very cumbersome to obtain, seem now to move much faster than a year ago. I have heard this from several sources, that the speed of permitting etc. finally has been greatly improved and that developers now can develop and build especially Windparks much faster.

Who is to profit most from this ? Of course Developers with a big presence (and pipeline) in Germany. From my basket, the ones with the biggest German development exposures is clearly Energiekontor (~50% share Germany~ 4GW). ABO Wind has around 2GW German pipeline (10%). PNE has a similar sized German development pipeline but also some more exotic countries like Vietnam and South Africa. So Energiekontor is clearly the most German focused developer.

Faster speed also creates problems: Capital

Developing (and owning) Windfarms is a very capital intensive business. If, for an existing pipeline, the speed of development gets higher, this means higher returns on Capital but also a requirement for (a lot) more capital.

Interestingly, Energiekontor, which is one of the pioneers of “developing and owning” business model has a very different apporach to ABO Wind.

The ABO WInd approach: Mo’ Capital

On June 1st, ABO Wind dropped a bombshell by announcing that they plan to change their corporate structure from a “normal” German stock cooperation (AG) to a KGaA. The KGaA also has listed shares, but due to a different Goevrnance, the public sharehiolders have only a very limited say in how the company is run.

On June 13th, ABO Wind released a Webcast where one of the founders together with the IR guy tried to explain why they are doing it. The main reason is that they want to raise more capital in order to grow faster, but the founders, who currently own 52% do not want to be diluted below 50%. The KGaA structure would enable them to go below 50% in ownership but keep control.

In a subsequent call with the IR guy, he mentioned that they need the capital both, for faster project approvals but also in order to be able to hold projects longer until they are “turnkey” ready. So far, ABO often sold projects earlier, for instance at the “ready to build” stage. The reason for this is that they want to keep more of the developer margin.

I think especially especially for the KGaA attempt, ABO Wind was pummeled heavily, I am not sure if they will get the required votes for this.

The Energiekontor approach:

Energiekontor interestingly has the exact opposite approach. They actually plan to sell projects earlier than in the past in order to use capital more efficiently:

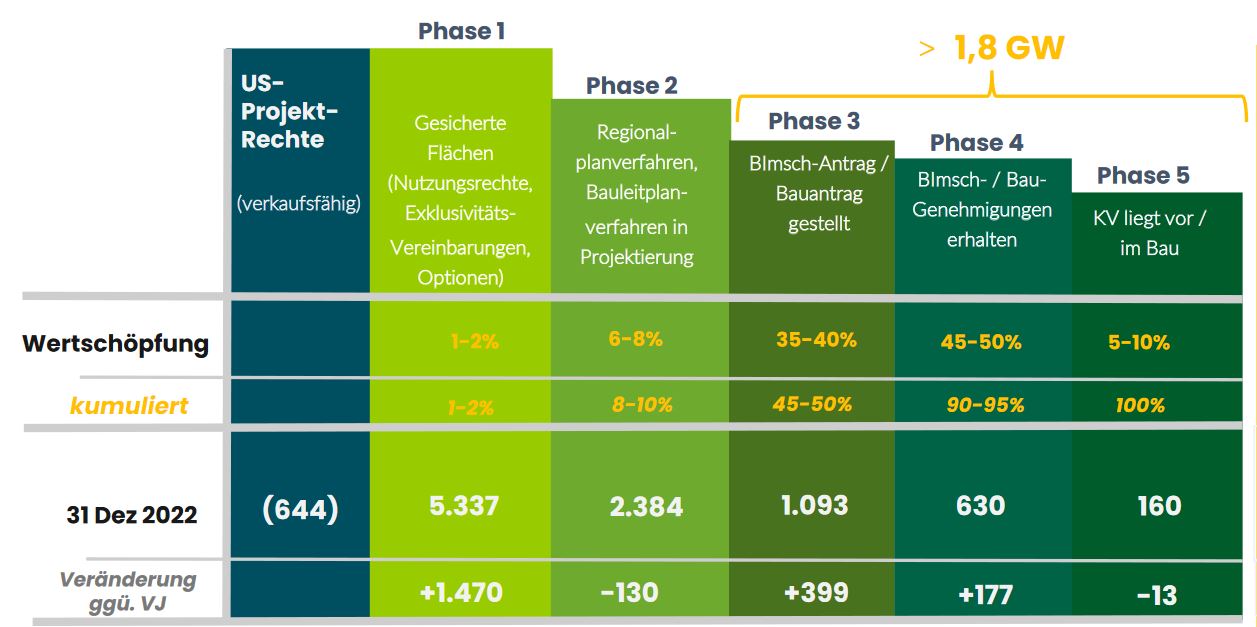

Looking into this chart from the Energiekontor investor presentation clearly shows that 90%-95% of the value creation happens up until a plant is “ready to build”:

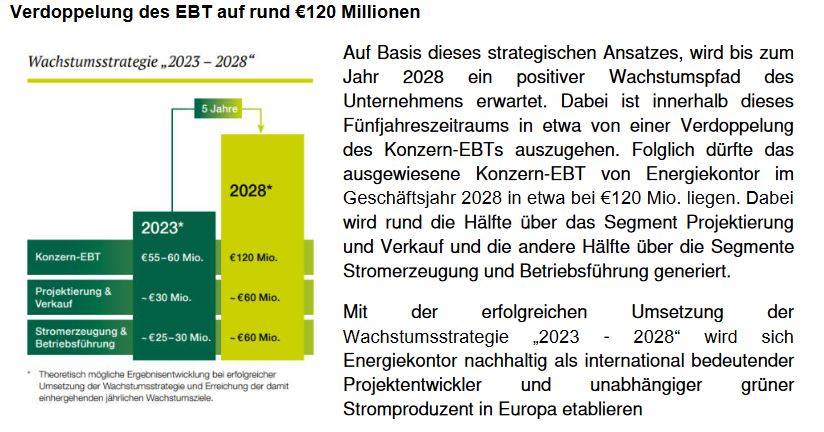

So from a capital allocation perspective, Energiekontor’s strategy looks a lot more shareholder friendly than ABO Wind. Interestingly, Energiekontor has published a quite aggressive forecast for 2028:

So Energiekontor plans to double EBIT by 2028 based on 2023, which itself is 15-20% higher than 2022.

Before I write myself tired, I reference the excellent new (German language) Energiekontor write-up from Jon Neuscherler on Abilitato.

To summarize the attraction of Energiekontor in a few points:

- most exposure to strongly growing German on-shore Wind reneweables market

- founder owned/run

- shareholder friendly strategy focused on capital efficiency

- relatively conservative Balance sheet (Net debt ~2,5x EBITDA)

- Significant upside if forecast is hit

- represents a certain hedge against Energy price shocks

- The increase in speed in German On Shore wind permit doesn’t seem to have been realized by the market so far

Overall, at the current valuation, one is underwriting a return of 15-17% p.a. which I think is highly attractive considered the relatively limited downside risk.

Of course there are risks, such as rising costs for wind parks, further rising interest rates, execution risks and political risks. But overall, I consider this as a very attractive risk/return profile and allocated 3% of my portfolio into Energiekontor at ~74,50 EUR per share. (For the record: In 2022, I bought them at 63 EUR and sold at 91 EUR).

What about ABO Wind, PNE, 7C and Encavis ?

Via the Active Ownership Fund, I already have exposure to PNE. ABO Wind is a company that I still like from a fundamental perspective and is attractively valued, despite the less shareholder friendly startegy.

I do think that the stock is currently a kind of “special situation”. If the KGaA issue resolves itself one way otr the other, the share price could benefit. So I will keep the ABO Wind position for the time being.

Dislaimer: This is not investment advice. PLEASE DO YOUR OWN RESEARCH !!!!

Although I should have done that much earlier, I sold ABO Enrgy over the last days, with the remainder today.

Do you see renewables in general more critically after the Trump election or are you specifically concerned about the KGaA transition at Abo?

Both, I think the next few years could be more difficult and I think the startegy of ABO Energy specifically is not consistent. German election might have more impact than Trump.

Vielen Dank für deinen Write-Up, immer sehr interessant. Bist du im Rahmen deiner Norwegen-Suche einmal auf die Firma Cloudberry gestoßen? Nach meinem Verständnis ebenfalls wie bspw. Energiekontor sowohl Bestandshalter als auch Entwickler. Möglicherweise spannend, mich würde deine Meinung dazu interessieren!

Nein, Cloudberry hat der Zufallsgenerator noch nicht ausgewählt.

I didnt find what is interest rate of their long term liabilities and if it is fixed. And duration…

You know MMI?

Gut ausgearbeitete Punkte und spannendes Unternehmen.

War keine Stromerzeugung aber ein Erzeuger für Strom und Wärme über ein BHKW wäre 2G Energy. Die Energiewende wird ein Zusammenspiel aus vielen Faktoren und Technologien. Leider wird die Wärmeerzeugung oft vergessen.

Hast du dir 2G Energy schon einmal angesehen?

Du deckst ja Stromerzeugung und Gebäudeisolierung (zwei große Treiber) bereits ab.

Ich frage mich ernsthaft wer sich in Zukunft ein BHKW in den Keller stellen soll. Um grünen Wasserstoff herzustellen wird man eine Menge Wind- und Solar-Energie benötigen, hat Wirkungsgradverluste, muss man erst einmal eine Infrastruktur bauen, da die Gasleitungen nicht viel Wasserstoff abkönnen und BHKWs sind teuer und reparaturanfällig.

Da heize ich doch lieber mit einer Wärmepumpe, die die Windenergie direkt nutzen kann, zusätzlich noch die kostenlose Energie aus der Umluft nutzt und die entgegen der ganzen politischen Debatte auch heute schon günstig zu bekommen ist, da Wärmepumpen in Asien und sehr bald auch in Europa in Massenfertigung produziert werden.

Wenn es im Winter mal sehr kalt und windstill ist, ist es viel effizienter durch Spitzenlastgaskraftwerke die fehlende Energie zu decken, als dass sich jeder sein eigenes Kraftwerk in den Keller stellt.

Okay, mein Fehler. 2G Energy ist eher im Bereich Industrie-BHKW unterwegs. Aber auch hier sprechen im Grunde die gleichen Argumente für Industriewärmepumpen.

2G Energy ist der einzige Hersteller mit H2 readiness. Ob Wasserstoff wirklich in großen Mengen kommt, das ist ein anderes Thema. Trotzdem wird der Bedarf an Grundlaststrom groß sein. Die Einsatzgebiet können hier von kleinen Dörfern, Industrieunternehmen, Krankenhäuser (welche alle Versorgungssicherheit benötigen) aber auch im Verbund mit Biogas betrieben werden.

Der Wärmebedarf besteht auch in der Industrie. Außerdem muss die Grundlast des Stromes und auch der Bedarf der Wärme mittelfristig gedeckt werden. Das Thema Wärmepumpe und die breiter Abdeckung ist eher ein langfristiges Vorhaben.

Am Ende entscheiden jedoch der Markt und die politischen Entscheidungsträger. Grundsätzlich haben die Staatssekretäre die Verantwortung, die Energiewende und Versorgungssicherheit zu garantieren. Sonne und Wind wird die Versorgungssicherheit nur mit einem erhöhten Ausbau gekoppelt mit einer wirtschaftlichen und möglichst verlustfreien Speichertechnologie bewerkstelligen

Wie groß ist denn der Anteil von BHKW für Biogasanlagen bei 2G? Und wie sehen da überhaupt die Aussichten von Biogas aus?

BHKW mit Erdgas hat keine lange Zukunft denke ich. Und mit Wassestoff ist das natürlich auch Quatsch (auch wenn sich H2-ready sicher gut verkauft).

Sehe ich in der Tat anders. Biogas aus erneuerbaren Quellen hat seinen Platz und in der Kombination mit einem Wäremnetz hat das langristig Zukunft. Kann man Live schon gut z.B. in Däemark ankucken. Die sind da schon 5-10 Jahre weiter.

Mit Biogas bin ich dabei. Deshalb frage ich mich ja, wieviel mehr Biogas wird es denn geben? Es gibt ja nicht nur die Problematik bezüglich Anbaufläche für Nahrungsmittel.

Auch für den ganzen Bioabfall der zu Gas umgewandelt wird, gibt es möglicherweise zukünftig auch ander zahlungskräftige Nachfrager. Mir fällt da auf jeden Fall SAF, also Biosprit für Luftfahrt, ein. Die werden da erstmal außer den noch teureren e-Fuels keine großartige CO2-freie Alternative haben.

Vielleicht ist das aber auch noch etwas zu weit in die Zukunft gedacht. Luftfahrt will ja erst 2050 Klimaneutral sein.

Dass man auf der gleichen Fläche mit Photovoltaik mindestens die 30-fache Energieausbeute hat wie mit Energiepflanzen, lässt mich daran zweifeln. Aber vielleicht machen die Förderungen es irgendwie attraktiv. Und Elektrolyseure und Großwärmepumpen werden noch nicht in ausreichenden Stückzahlen hergestellt.

2G steht auf meiner “Priority To do “liste…..

@Flo: Backup zur Versorgungssicherheit ist tatsächlich ein gutes Argument. Dafür könnte auch Erdgas weiter eine Rolle spielen. Denn hohe Brennstoffkosten sind im Notfall akzeptabel. Danke.