Innoscripta SE: 60% EBIT margins & rapid growth but why did the 2025 IPO flop ?

Innoscripta is a young company. It was founded in 2012 and is headquartered in my hometown Munich.

Quick excursion: Young companies as “diversifier”ng companies as “diversifier”

Some months ago I listened to a podcast with Prof. Damodaran where he argued that the age of companies is an underestimated source of diversification, especially in the age of rapid fundamental changes. This is something that resonated with me a lot. The company age of my portfolio is quite old and based on personal experience, I do think that younger companies adapt more easily to fundamental changes.

That was one of the reasons that Innoscripta came onto my radar.

What does Innoscripta do & what problem do they solve ?

The business model is not too complex: Innoscripta offers a SaaS solution that allows companies to document and apply for a Tax refund in Germany for “Research & Development expenses”.

This Tax refund has been introduced in Germany in January 2020 and provides a tax refund of 25% to 35% of the expenses companies incur when researching and developing “qualified” purposes. The amount is capped at 10 mn expenses (2025) per company and the refund is between 25-35% of the expenses.

Those “qualified purposes” are mainly “new developments” not just incremental improvement of existing products and as one major feature, the economic outcome must be uncertain.

To get the refunds, the company must run through a 2 step process: First, they must get approval that the actual project qualifies for the refund. And then second, they must provide evidence how much that project has cost.

For step 2, the fiscal authority requires a detailed document in order as proof for the expenses which covers especially how much certain persons have contributed to the specific project. It also needs to be stored for eventual tax audits.

To my knowledge, so far, standard ERP software packages like SAP etc. do not provide this documentation. So you either have to do a lot of Excel stuff or use Innoscripta’s Software that helps you extract and document the data.

With Innoscripta’s web based software, users can upload all kinds of data, even unstructured data. Innoscripta then helps both with step 1 and step 2 of the process and seems to make it quite easy to apply for the refund. They also claim that they have a very high success rate.

Innovative revenue model: Success fees instead of software fees

Innoscripta’s innovative business approach is that they don’t charge upfront. Only when you get a refund as a company, you have to give Innoscripta a 20% share of that refund.

Before the change in 2020, companies had to apply for direct subsidies at various agencies. The budget for these subsidies was variable (first come first serve) and the application process extremely cumbersome.

One could argue that Innoscripta is not really a SaaS company but much more a “digitized consulting company”.

So the 2020 change was a game changer as it made the process much more uniform. Innoscripta seems to be the first (and only ?) company who offers a Software based solution. The competitors seem to work mostly on a consulting basis.

Other countries like the UK and France had tax reimbursement solutions already for a long time, France since 1984 and UK since 2000.

Founder led, bootstrapped and sales driven

Innoscripta is a relatively young company, still led and majority owned by its founder Michael Hohenester who according to my understanding is still quite young (maybe mid 40s or so. For some reason it is very hard to find a picture of him or even a video interview. He seems to be very keen on privacy.

As a bootstrapped company that was profitable early on, they didn’t really have outside capital and the growth has been very capital light which is quite remarkable.

From what one could read, as many other successful B2B companies, they have a strong sales focus. People who can sell the product can move up quickly and earn a lot of money after they have gone through a (most likely tough) Sales bootcamp.

This sales “pressure cooker” is clearly not a fit for everyone, which results in some not so good reviews on Glassdoor and Kununu.

Incredible margins & Growth

The stock with the highest margins that I have covered in the blog was GTT, a French monopolist for LNG ship insulation technology with net margins of 50%. I owned it twice but not long enough…

Innoscripta is approaching these levels quickly.

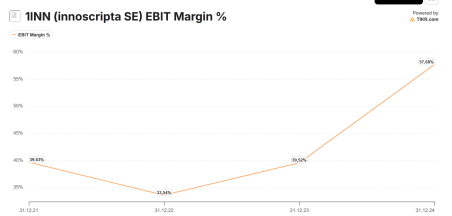

This is the EBIT margin development since 2021 and in 2025 the have increased the EBIT margin to 61%:

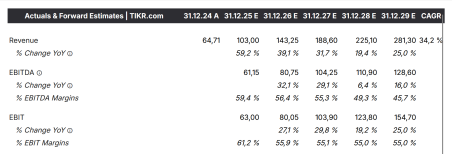

Sales growth and EBIT growth have been phenomenal. especially since the introduction of the tax credit scheme in 2020. More than 10x in sales since 2020 and 50x in EBIT is something you don’t see often:

Looking at the numbers for TIKR, the stock looks way too cheap based on these numbers:

A NTM P/E of ~20 for such a “monster” seems to be too good to be true. One argument could be that SaaS stocks have become quite unpopular lately, so maybe a general dislike towards SaaS stocks is part of the reason.

Looking at TIKR’s analyst estimates, we can see that “the street” assumes 40% growth in 2026 with a slightly lower profitability, stabilizing at 55%:

But, and this is a big BUT, on a quarterly basis, sales has been slowing in 2025 from quarter to quarter as we can see in this graph that NotebookLM created for me:

The big question here is of course: What’s going on and how will this continue ? Are competitors already taking a bite of Innoscripta’s business or are companies “vibe coding” their applications already with Gemini and ChatGPT ?

Unfortunately, Innoscripta does not give any guidance, at least I haven’t seen one for the coming years.

Competition:

Current competition seems to be at the moment mostly Consulting companies and Full service Auditors. Innoscripta mentions these companies in the IPO prospectus:

Leyton, Ayming, FI Group, AF Project GmbH, EURA, GovGrant, Ryan, Grantify, Alliant Group (which acquired ForrestBrown), Auditex, and ABGi Group

In addition, they mention that some software companies that specialize in Workforce planning could become potential competitors:

Generic technology solutions providers. These companies in Europe primarily include servicenow, monday.com, workday, ATLASSIAN, ATOSS, Jira, Docusign, Planisware, Fortnox and smartsheet. They focus primarily on unspecialized management capabilities and documentation services.

Another “competitor” could be a simplification of the whole process. There seems to be already a discussion going on that the process should be simplified. Not sure if I can believe this, but it would make sense. From a tax payers perspective, paying 20% of the money to a service provider with astronomical margins might not be the best solution.

For Innoscripta the most painful initiative would most likely be a discussed “Fast track” process for companies that have already successfully applied for a Tax credit in the past. This could increase churn rates potentially, especially for larger clients where more money is at stake.

Opportunities

– so for, only a relative small percentage of companies has actively requested the Tax credit (19K application as of Summer 2025), so there are many companies that could become clients in the future

– The scope and size of the credits have been extended and increased. In 2026 for instance, companies can apply for an additional 20% of non specific expenses

– expansion into R&D project management software already started

– eventually opportunities in other European countries with similar products. Innoscripta mentions that they have opened branches in France and the UK. The claim is that Innoscripta’s software can be adjusted without additional coding to apply and document under foreign rules

AI

To my understanding, the Software from Innoscripta looks for the required data in operating systems (SAP, HR Systems etc) and then processes it in a way that fulfills the requirements of the German Fiscal authorities.

So I would describe this as a “one way processing” which is most likely done once or a few times per year. Maybe there is some feedback looking into the systems but Innoscripta Software is clearly not something employees use on a daily basis.

This is for instance two screenshots of the Software from their homepage:

It doesn’t look extremely complicated, but of course a screenshot does not say anything about the complexity etc.

As mentioned above, the know-how of how to do this and also some kind of track record is existing at other places, mostly consultants and auditors.

With the help of AI coding tools, I guess it should be possible to create a solution similar to Innoscripta for at least some of the players. I do not believe that many SMEs will “vibe code” their own tool, but I think especially the consulting arms of the auditors could become veritable competitors as their distribution power is quite significant.

AI clearly helps Innoscripta to become even more efficient but net, I do hink that AI is a threat to Innoscripta’s “fat” margins that will attract competitors.

The one thing that is extremely hard for me to judge, as with almost all other software stocks is something I have already mentioned on Twitter/X:

In order to be able to judge if and how AI will be a threat to especially a Software business model requires to have a view on how AI will develop over the next 1,3,5 or 10 years if you are a longer term oriented investor.

I think it is a big mistake to judge based just on current capabilities of LLM models. For me, this is impossible, so I am very cautious in these cases especially if the valuation is higher than the average market which is of course also facing disruption through AI.

First time customer effect & lack of cohort data

New customers, especially now will have the opportunity to apply for tax refunds for the previous 4 years. That means that the initial revenue that Innoscripta is booking for such a client is very high.

But if nothing changes and the client stays, this client will have only ¼ of the initial volume and sales going forward which translates into a -75% churn in revenue for such a client in year 2. That means that current cohorts could see significant churn rates simply because of this effect depending on how much of the current revenue consists of multiple year refunds.

This effect was less severe in the first years as the maximum look back for the credit is 1.1.2020. So a new client in 2021 could only apply for 1 year, in 2022 for 2 years etc. but know this really can distort growth numbers if a larger number of new clients applies retroactively for the full 4 years (which is only possible from 2025 on).

In any case, applying typical SaaS KPIs in this case clearly makes no sense as it is not a SaaS revenue model.

A quick look at the valuation:

63,4 mn EBIT should translate into roughly 43 mn EAT or an EPS 4,3 EUR or a P/E of ~21 for 2025.

This is not that much for a company that has been growing 60% in 2025 and is earning 60% EBIT margins and 100% plus in ROIC/ROCE.

However, and this is the big however, I really struggle to have any idea how the future path of both, revenue growth and EBIT margin development is.

One could argue that very little growth is priced in at this level. On the other hand, in my opinion, there is a “non-zero” probability that EPS is maybe lower in 2026 or 2027 than in 2025. I just don’t know. I just have no real feeling how this is going to develop. Which for me is not a good basis for a longer term investment.

Other considerations

A typical German feature is that there is also very little dilution through option programs. Employees can buy shares by transferring the bonus into shares but so far, Innoscripta made little use of granting options like all the US startups do.

One negative point is that Innoscripta only trades in the Scale segment on the Frankfurt exchange which has a lot lower requirements than the regulated markets. For instance, Innoscripta does report only according to German GAAP, not IFRS.

Another “risk factor” is that the current business model depends on one regulatory regime in one country.

At the moment, there is clearly a tailwind for these credits but you never know what happens if for instance the, after an election the Government changes. Or if the Government decides to change the rules.

As mentioned above, paradoxically the biggest risk would most likely be a radical simplification of the process as such.

Summary

Innoscripta is clearly a very interesting company with an outstanding growth trajectory over the last 5 years. However, based on several factors, I am not sure if and how to project the future trajectory of this relatively young business even for 2026 or even further out.

Especially the rapid growth deceleration in 2025 is something that has not been explained.

As a consequence, I will not invest now, but keep a close watch on the stock, especially to see how the next 1 or 2 quarters look like. Even if they manage only 10 or 15% growth, then it could be worth an investment. Otherwise, maybe not.

If someone has better insights on how to model future revenue, I am very much open to discuss this.

I dont like the business model as it depends on the regulatory dschungle of german burocracy.

There might be several headwinds:

I would agree mostly. Only exception is that R&D funding / credits might increase for a while.

Danke, sehr lesenswert! Haben Sie sich CTS Eventim angeschaut? 10x EV/EBIT, 1 Milliarde Net Cash. Marktführer.

I looked at them last tiem 5 years ago…

Have you looked at CTS EVENTIM? Great company back under 70 EUR per share.

Looked at them last time 5 years ago….

yeah – it is a consulting company, i do not understand what saas is there or needed ther.

There are a lot of (very small to very big) consulting companies offering the same service, what differentiated (and probably still does) Innoscripta during my time was there very aggressive aproach on acquiring „customers“…

Well, aggressive customer acquisition is not bad per se if the product is good and sticky.

it used to be a well organized, aggressive sales business trying to convince companies to tab the federal budgets for [Forschungszulagen]. innoscripta was helping with the application for the funding and got a revenue share in exchange for that service. free money for companies who often did not know these government funds existed. No software at all historically but maybe this has changed now. well done by founders to get the software saas multiple for this. financials are very strong and maybe the have an opportunity to build that SaaS business people are talking about.

Thanks for the insight “Bill”. They do have a Software but the question is if it really is an enduring competitive advantage or not.

Back to basics: I have not seen any granular PnL breakdown to understand the cost base and incremental margin. The margins look way off for what is a consulting biz at the end of the day.

Why IPO to begin with with such a tiny float? And now mgt buy some shares in the market?