Update Gronlandsbanken – result and annual report 2014 & Danish interest rates

Gronlandsbanken

Gronlandsbanken has just released 2014 numbers and its 2014 annual report. 2014 results look solid: ~50 DKK profit per share, roughly 6% more than in 2013. The dividend remains at DKK 55 (dividend is paid out of pretax income). ROE has remained high at 16,3%. The result would have been even better if Gronlandsbanken would have not increased reserves. This is the quote from the annual report:

The result before value adjustments and write downs of DKK 148,6 million is the Bank’s best basis result so far. This is of course satisfactory. It is at the same time above the last announced results expectation of a result before value adjustments and write downs in the upper end of the range DKK 125 – 145 million. The result before tax returns 16.3% on year start equity after dividend.

This was achieved against a slight drop in Greenland’s GDP which I find quite remarkable. The stock market seemed to have “anticipated” those results to a certain extend as the stock price shows:

The balance sheet is still super rock solid with an equity ratio of 19% (of total balance sheet, not risk weighted assets or some similar shenanigans).

My initial investment thesis 2 years ago was the following:

– as it is the only bank in Greenland, its margins are around twice as high as the best global banks and the balance sheet is rock solid. One could call this a natural moat

– even based on the current state, current valuation implies significant upside to fair value

– the Greenland resource story could add significant growth going forward, even with maybe other banks entering Greenland

– finally, Management has started to buy shares after surprisingly good Q3 numbers

– although there is no direct catalyst, an indirect catalyst could be if some of the projects proceed well and Greenland will move into the spotlight. Gronlandsbanken is the easiest (and only) way to invest into Greenland without project specific risk

One of the issues of course is that most of the natural resources projects look a lot less likely to happen than 2,5 years ago.The annual report is as always a great resource to see what is going on in Greenland. Most projects seem to be on hold or cancelled, the only remaining interest is from China:

Among the larger projects, it has become obvious that virtually only Chinese investors continue to show a certain interest. The BANK of Greenland considers it likely and quite naturally, that the funding can come from China. Chinese enterprises are often the leaders in processing for further use in either Chinese, American, or European industry.

Especially the oil sector has been hit hard:

The prospects of the oil area are more dismal than of the mineral area. After Cairns test drilling in 2010 and 2011, oil exploration in Greenland is now greatly reduced, see Figure 8. The stagnation of the exploration in both the oil and the mineral area is expected to continue over the next few years, even though new licenses have been issued and the preparatory work is continuing in 2014 as well.

The declining interest in oil exploration is a.o. due to large oil and gas discoveries in other places, and the fall in the oil price . Of importance can possibly also be the administration and regulation of the area so far have not been regarded as sufficient by several persons in the industry.

So the bad news is that within my initial time frame of 3-5 years, I will not see any large mining or oil projects in Greenland. The upside might be that the incentive for other banks to enter Greenland will be most likely quite low.

Interest rates

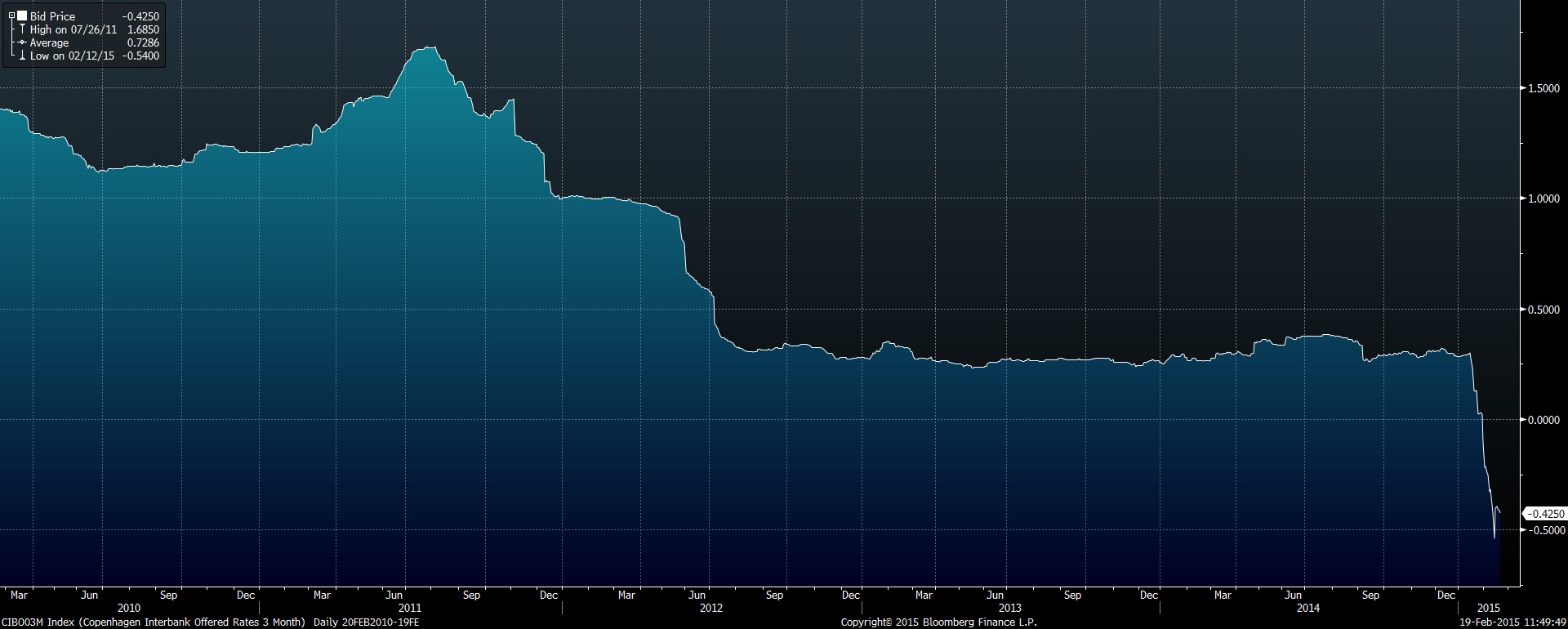

However, another thing happened which was not on my radar screen: Denmark went from having low-interest rates to negative interest rates. This is how 3 month local swap rates developed:

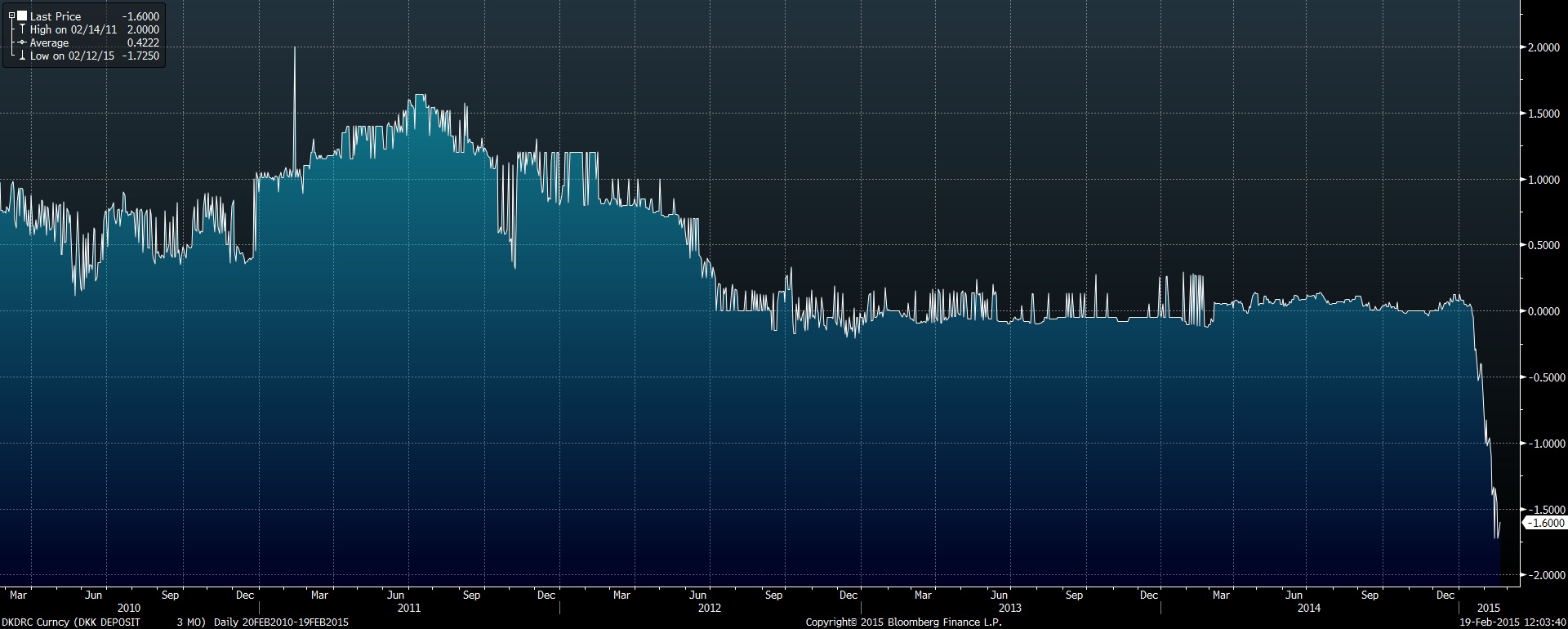

Just as a reminder: Swap rates are “unfunded”, that means based on contracts where no principal changes hands. If we look at “funded” rates, so how much money Danish banks pay for actual deposits, the situation is much more dramatic:

So just to put this in context: If you want to deposit money for 3 months at a Danish bank for 3 months in DKK, they charge you -1,6% p.a. for this “service” !!!!

Impact on Gronlandsbanken:

One thing about Gronlandsbanken which I liked initially but what could be a problem going forward is the following: Gronlandsbanken has a significantly higher deposit base than loans outstanding. While this is good from a liquidity and risk point of view, it is bad because those excess funds have to be invested somewhere and in local currency.

I am not sure if Gronlandsbanken could actually charge for deposits locally, so the risk is there that they get squeezed on the amounts not loaned out to customers. They seem to have anticipated this and increased their bond holdings, but still, at year end 2014, roughly 20% of the balance sheet is potentially exposed to this potential “Negative carry” problem.

On the other hand, as a EUR investor being invested into a DKK security exposes me to a “positive Black Swan” similar to the CHF/EUR move in January. If something goes horribly wrong in the EUR zone, there might be some upside in holding DKK denominated securities.

Addtitionally, any Danish pension fund and Insurance company will struggle to find income producing assets in DKK. With a dividend yield of (gross) of around 8%, Grondlandsbanken should be not unattractive and therefore support the share price in the short term.

Summary:

The underlying business of Gronlandsbanken has done surprisingly well in 2014 despite a lackluster economy. Due to the carnage in natural resource prices, the implied “resource option” has been postponed some years into the future, making the investment case less attractive compared to 2,5 years ago.

Ultra low and negative interest rates could make it more difficult for deposit-rich banks like Gronlandsbanken to maintain their interest margins. As there are not that many alternatives at the moment I will continue to hold the stock for the time being, as it also functions as a kind of “Euro Black Swan” hedge. If I find other interesting finaincial service stocks, Gronlandsbanken would be the first one to be replaced as I think that my other financial holdings (Kasbank, Van Lanschot, NN, Admiral) have a better risk/return ratio.

I will also monitor closely if and how the negative rates will feed through Grondlandsbanken’s Q1 results.