Update Gronlandsbanken – result and annual report 2014 & Danish interest rates

Gronlandsbanken

Gronlandsbanken has just released 2014 numbers and its 2014 annual report. 2014 results look solid: ~50 DKK profit per share, roughly 6% more than in 2013. The dividend remains at DKK 55 (dividend is paid out of pretax income). ROE has remained high at 16,3%. The result would have been even better if Gronlandsbanken would have not increased reserves. This is the quote from the annual report:

The result before value adjustments and write downs of DKK 148,6 million is the Bank’s best basis result so far. This is of course satisfactory. It is at the same time above the last announced results expectation of a result before value adjustments and write downs in the upper end of the range DKK 125 – 145 million. The result before tax returns 16.3% on year start equity after dividend.

This was achieved against a slight drop in Greenland’s GDP which I find quite remarkable. The stock market seemed to have “anticipated” those results to a certain extend as the stock price shows:

The balance sheet is still super rock solid with an equity ratio of 19% (of total balance sheet, not risk weighted assets or some similar shenanigans).

My initial investment thesis 2 years ago was the following:

– as it is the only bank in Greenland, its margins are around twice as high as the best global banks and the balance sheet is rock solid. One could call this a natural moat

– even based on the current state, current valuation implies significant upside to fair value

– the Greenland resource story could add significant growth going forward, even with maybe other banks entering Greenland

– finally, Management has started to buy shares after surprisingly good Q3 numbers

– although there is no direct catalyst, an indirect catalyst could be if some of the projects proceed well and Greenland will move into the spotlight. Gronlandsbanken is the easiest (and only) way to invest into Greenland without project specific risk

One of the issues of course is that most of the natural resources projects look a lot less likely to happen than 2,5 years ago.The annual report is as always a great resource to see what is going on in Greenland. Most projects seem to be on hold or cancelled, the only remaining interest is from China:

Among the larger projects, it has become obvious that virtually only Chinese investors continue to show a certain interest. The BANK of Greenland considers it likely and quite naturally, that the funding can come from China. Chinese enterprises are often the leaders in processing for further use in either Chinese, American, or European industry.

Especially the oil sector has been hit hard:

The prospects of the oil area are more dismal than of the mineral area. After Cairns test drilling in 2010 and 2011, oil exploration in Greenland is now greatly reduced, see Figure 8. The stagnation of the exploration in both the oil and the mineral area is expected to continue over the next few years, even though new licenses have been issued and the preparatory work is continuing in 2014 as well.

The declining interest in oil exploration is a.o. due to large oil and gas discoveries in other places, and the fall in the oil price . Of importance can possibly also be the administration and regulation of the area so far have not been regarded as sufficient by several persons in the industry.

So the bad news is that within my initial time frame of 3-5 years, I will not see any large mining or oil projects in Greenland. The upside might be that the incentive for other banks to enter Greenland will be most likely quite low.

Interest rates

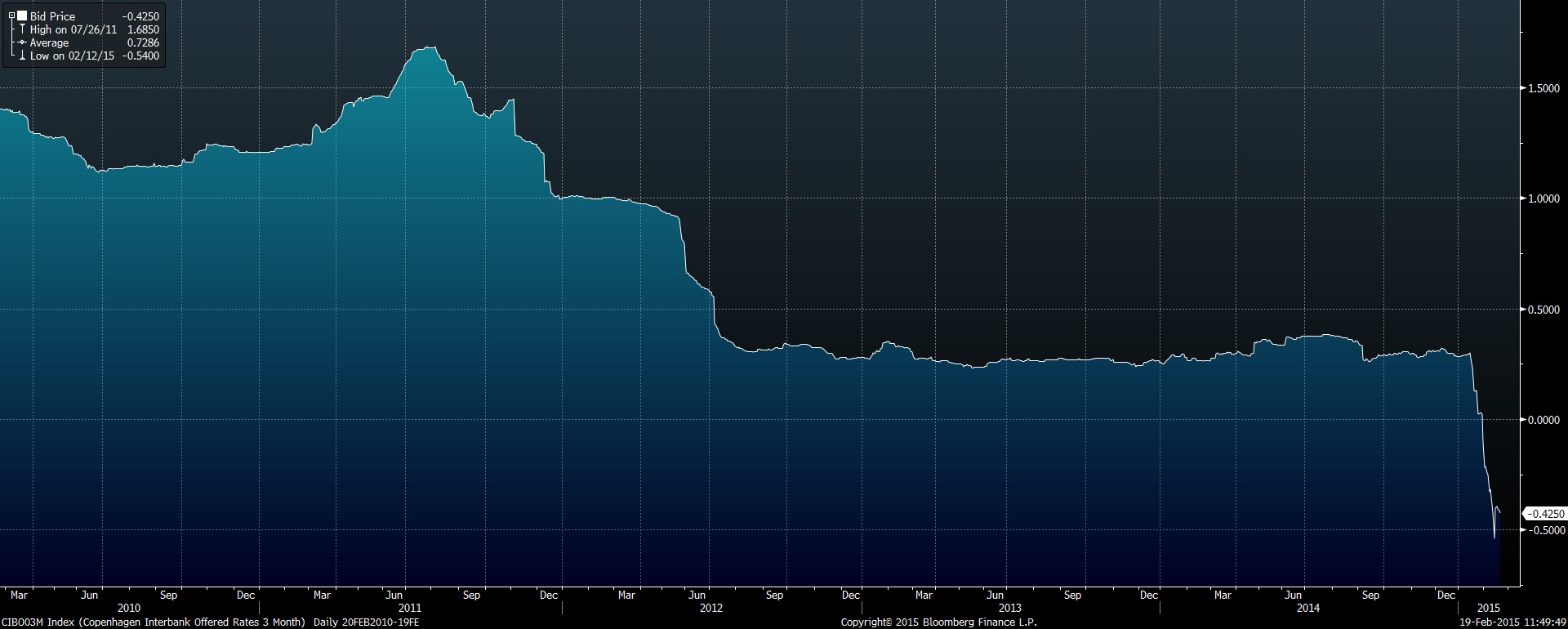

However, another thing happened which was not on my radar screen: Denmark went from having low-interest rates to negative interest rates. This is how 3 month local swap rates developed:

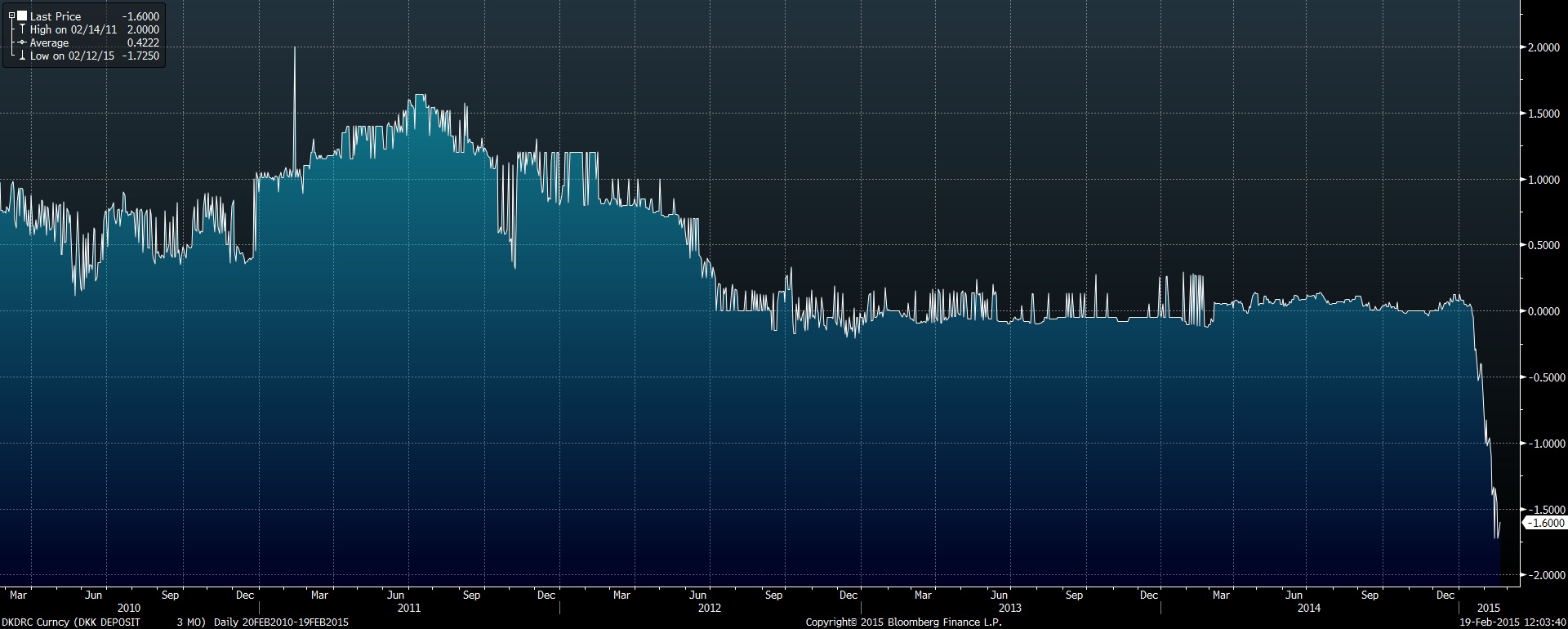

Just as a reminder: Swap rates are “unfunded”, that means based on contracts where no principal changes hands. If we look at “funded” rates, so how much money Danish banks pay for actual deposits, the situation is much more dramatic:

So just to put this in context: If you want to deposit money for 3 months at a Danish bank for 3 months in DKK, they charge you -1,6% p.a. for this “service” !!!!

Impact on Gronlandsbanken:

One thing about Gronlandsbanken which I liked initially but what could be a problem going forward is the following: Gronlandsbanken has a significantly higher deposit base than loans outstanding. While this is good from a liquidity and risk point of view, it is bad because those excess funds have to be invested somewhere and in local currency.

I am not sure if Gronlandsbanken could actually charge for deposits locally, so the risk is there that they get squeezed on the amounts not loaned out to customers. They seem to have anticipated this and increased their bond holdings, but still, at year end 2014, roughly 20% of the balance sheet is potentially exposed to this potential “Negative carry” problem.

On the other hand, as a EUR investor being invested into a DKK security exposes me to a “positive Black Swan” similar to the CHF/EUR move in January. If something goes horribly wrong in the EUR zone, there might be some upside in holding DKK denominated securities.

Addtitionally, any Danish pension fund and Insurance company will struggle to find income producing assets in DKK. With a dividend yield of (gross) of around 8%, Grondlandsbanken should be not unattractive and therefore support the share price in the short term.

Summary:

The underlying business of Gronlandsbanken has done surprisingly well in 2014 despite a lackluster economy. Due to the carnage in natural resource prices, the implied “resource option” has been postponed some years into the future, making the investment case less attractive compared to 2,5 years ago.

Ultra low and negative interest rates could make it more difficult for deposit-rich banks like Gronlandsbanken to maintain their interest margins. As there are not that many alternatives at the moment I will continue to hold the stock for the time being, as it also functions as a kind of “Euro Black Swan” hedge. If I find other interesting finaincial service stocks, Gronlandsbanken would be the first one to be replaced as I think that my other financial holdings (Kasbank, Van Lanschot, NN, Admiral) have a better risk/return ratio.

I will also monitor closely if and how the negative rates will feed through Grondlandsbanken’s Q1 results.

I found a quite cheap (in my opinion) stock in the French market: DLSI (FR0010404368).

This is a HR/recruitment company with amazing low multiples and low debt (near zero).

The unemployment rate in france may be a concern (or not), though the company released quite good results in 2014.

what do you think about this stock?

good spot. It seems to be an amazing stock to invest, cheers mate

Can you give a brief opion about that stock, DLSI. Thank you

Dear Kirsten,

I don not know the company at all, so I can’t give a qualified opinion.

mmi

I would like to share with you this research

http://www.groupedlsi.com/GetDocument?id=446031

to be honest, this sell side one pager doesn’t motivate me to look into the company….

“You have to turn over a lot of rocks to find those little anomalies. You have to find the companies that are off the map”

Warren Buffett

good point. However I have so many interesting rocks lying in front of me that I have to prioritize 😉

One thought on the negative interest rate in DKK.

Are you sure this is a negative for Danish banks? The way I see it is, that Danish banks have the possibility to deposit their cash with the central bank at the current account rate which stands at 0%.

If I’m correct here, there is no negative effect on customer deposits which likely carry a 0% interest rate.

However, there’s one huge upside available – apparently Danish banks can take money (via cross currency swaps and similar instruments) at a negative rate (ie they are being paid to take money) and deposit that money at the current account rate of 0%.

I’m not 100% sure that’s how it is in Denmark, but it quite certainly works that way in Switzerland.

Yes, Danish Banks can deposit at the current account rate but only up to a certain limit.Above that it gets automaticallytransformed into a -0,75% deposit account.

http://www.nationalbanken.dk/en/marketinfo/official_interestrates/Pages/default.aspx

If you look at the net positions,you cann decide yourself if there is aproblem for Danish banksor not:

http://www.nationalbanken.dk/en/marketinfo/netposition/Pages/default.aspx

I would say there is a problem. a BIG problem.

Danish Banks in general – yes, a problem at the moment – no doubt.

As for Gronlandsbanken – their current account limit is 250 mln DKK. They have deposits with central banks of roughly 550 mln DKK. That means a maximum of 300 mln DKK are charged with 0.75% (assuming their balance on December 31st as ongoing). Would cost them about 2.25 mln DKK a year (or 2.5% of their net earnings after tax). I would not consider that a big problem.

Also, what motivation would the Danish central bank have to crumple their own banks? I’m 100% certain, that should the negative deposit rate become a major problem, the central bank will find a solution in favour of their commerical banks (same as in Switzerland).

the problem for Gronlandsbanken is not the amount at the central bank but the deposit/laon ratio. Unless the situation reverts quickly. Gronlandsbanken will get a problem with the total amount of excess deposits. This is a specific Gronlandsbankne problem.

“The result before tax returns 16.3% on year start equity after dividend.” Why isn’t ROE lower than 16.3%, as net income should be lower than EBT and why deduct the dividend?

I have read an interesting article in the FAZ recently, which states the central bank is not allowed to change interest rate DKK/EUR. A parlamentary vote would be required. This is a higher hurdle. http://www.faz.net/aktuell/finanzen/devisen-rohstoffe/euro-bindung-daenemark-kaempft-gegen-die-spekulanten-13432468.html

mhm. der value tüpi, siehe unten: negative black swan und DKK hedge gegen eur risk. glaube der denkt bisschen zuviel nach.

ich werde die jedenfalls glaub verkaufen, vor der dividenden zahlung. die wird so hoch besteuert, und man muss das dann irgendwie beantragen. weil die nicht im doppelbest.abkommen sind. habe 6-7% mit denen gemacht. invest so 7000.- EUR denke nach der div. am 25.3. gehts die 55DKK runter. also alles ein brei. der geschaeftsbericht ist jedenfalls interessant. positiv: ueber die zeit habe ich mich ein bisschen mit groenland beschaeftigft. schon sehr interessant alles. im sueden ist es etwa so wie in oslo klimatisch. die bauen einen neuen hafen. 120mio und einen neuen knast. fuer 150 mio oder so. auftraggeeber die daenische krone bzw. republik. also so heile welt ist da wohl dann auch nicht. also zum auswandern mein ich. 😉

sonst habe ich einen dax put seit gestern und goldposition neu heute nicht ausgefuert. ETF in stuttgart euwax gold. reine preisspekulationen. kauf ich mir mal was.

eine (fast) gratis unicredit option long auch neu. aber nur (noch) kleingeld. denke auch mario denkt zuerst an die seinen.

>