Special Situation “Quickies”: EasyJet, Nagarro & BioNTech

Castlelake vs. Easyjet

The UK is a fertile hunting ground for Private Equity these days. I had written about KKR wanting to buy DCC and EQT going for Intertek.

Another potentially interesting story is Easyjet, where a US investor with the name Castlelake is trying to buy Easyjet and has increased the bid price now for a fourth time.

Easyjet’s board however seems to be less keen to sell compared to DCC and has not accepted the fourth offer, but allowed Castlelake a look into its books to motivate them to potentially pay an even higher price.

As other Airlines, Easyjet was hit hard by the Iran War due to rising fuel costs:

Castlelake had started with a bid of 4,03 GPB/Share on the first of June. And then increased via 5,60 GBP, 6,25 GBP to now 6,50 GBP.

According to some sources, the board might be willing to sell for 7 GBP.

At the time of writing, the shares trade at 5,72 GBP, a discount of more than 18% to the potential “clearing price” of 7 GBP and 12% to the last offer from Castlelake.

This is a pretty wide spread, but maybe justified because the case as such is not super easy.

For instance, in order to maintain its EU landing rights (which are essential for Easyjet), non-EU ownership is capped at 49%. To circumvent this, Castlelake seems to have teamed up with certain European individuals to restrict their ownership as US institution, put this structure will be heavily scrutinized if it comes to a bid.

What I also find interesting is that Castlelake has no track record in Private Equity. However, since 2024, they seem to be majority owned by Brookfield. But so far they have been focusing on Asset based lending, not Private Equity.

To me it is also not 100% clear which fund is sourcing this quite substantial deal.

Finally, at Easyjet, the founder is still owning 15% and he might have a lot of influence if and how this company gets sold.

Looking at the long term chart we can also see that as many other airline stocks, it was not such a great long term investment after all:

So overall, at least for me it is really difficult to “handicap” the risk of the deal not happening. Therefore I will stay away from this one despite the rather “juicy” spread.

Nagarro

Nagarro is a company I followed loosely over the years. It is a spin-off from German IT services company Allgeier and mostly considered to be a “Indian IT Outsourcing” shop.

Initially, the company became a “spin-off superstar” and went up to almost 200 EUR per share in 2022, before trending down the last 4 years to around 33 EUR:

There wer always some questions around the company and those outsourcing business models these days seem to be vulnerable to Ai Agentic coding.

Pretty much out of the blue, last Friday night came a take over offer from an Indian Competitor at a close to 100% premium equalling 81 EUR per share in cash.

There are a few interesting details here:

For instance, the share price already increased by +20% on Friday, so it seems that some insiders were already front running the news.

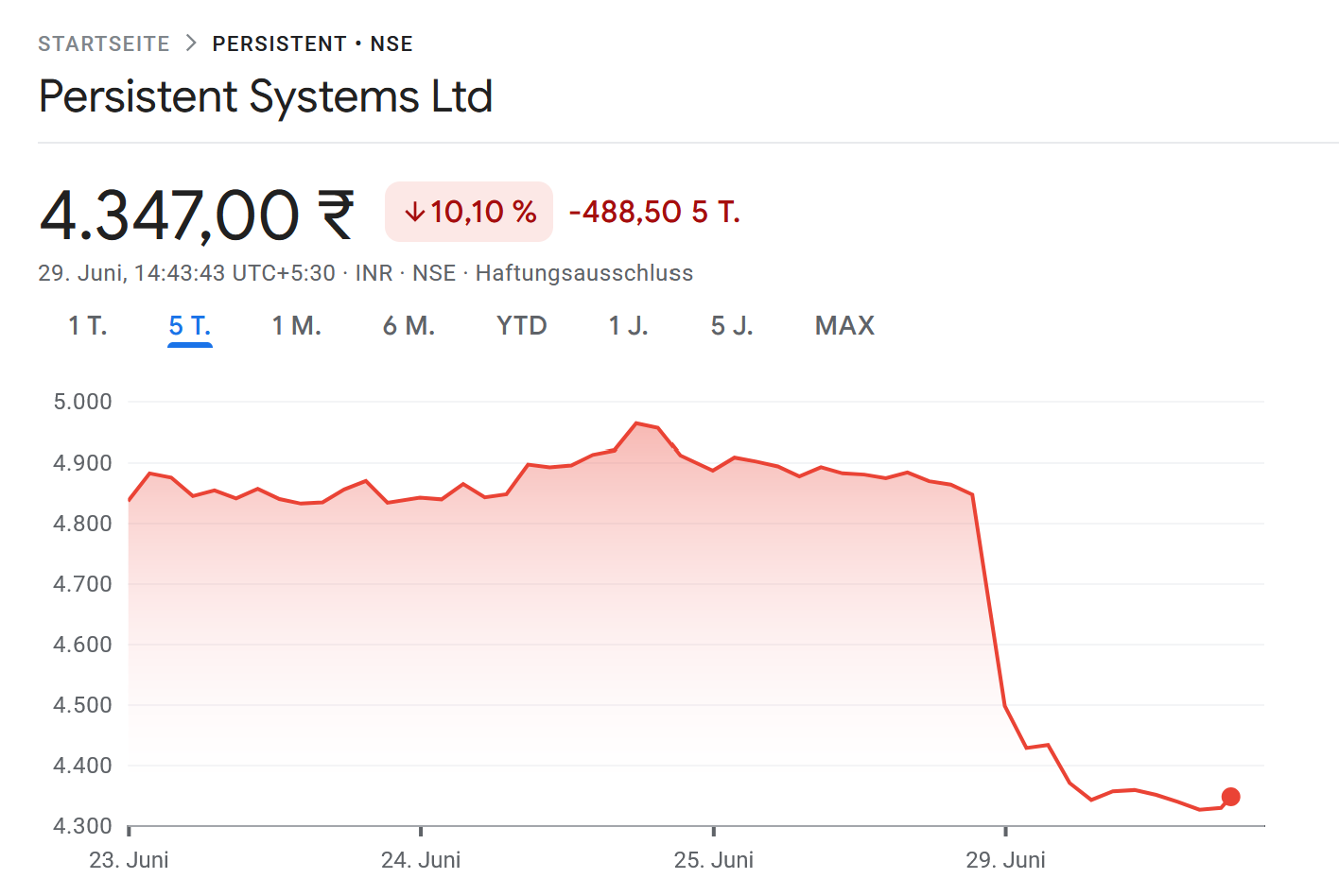

I also find it quite curious that the take over premium is so high. The bidder, Persistent Systems which is listed in India dropped by -10% today:

At the current price of 77 EUR, the discount is only 5%. There will be a dividend on July 2 nd of 1 EUR and record day is tomorrow, so this could be added to the discount, but still, something does not feel 100% right here from my perspective.

BioNTech:

Tomorrow is the day when BioNTech is supposed to announce how the separation between the founders and the company will look like.

As I mentioned in my post from 3 months ago, not announcing this tomorrow would be a really bad sign.

The stock price has stabilized since the sudden news of the potential departure in March and traded sideways, although with some volatility:

For the time being, I am watching here.