Banca Monte dei Paschi Siena (BMPS)- Another deeply discounted rights issue “Italo style”

Capital Raising in Italy is always worth looking into. Not always as an investment, but almost always in order to see interesting and unusal things. I didn’t have BMPS on my active radar screen, but reader Benny_m pointed out this interesting situation.

Banca Monte dei Paschi Siena, the over 600 year old Italian bank has been in trouble for quite some time. After receiving a government bailout, they were forced to do a large capital increase which they priced in the beginning of last week.

The big problem was that they have to issue 5 bn EUR based on a market cap of around 2,9 bn.

After a reverse 1:10 share split in April, BMPS shares traded at around 25 EUR before the announcement. In true “Italian job” style, BMPS did a subscription rights issue with 214 new shares per 5 old shares at 1 EUR per share, in theory a discount of more than 95%.

The intention here was relatively clear: The large discount should lead to a “valuable” subscription right which should prevent the market from just letting the subscription right expire. What one often sees, such as in the Unicredit case is the following:

– the old investors sell partly already before the capital increase in order to raise some cash for the new shares

– within the subscription right trading period, there will be pressure on the subscription right price as many investors will try to do a “operation blanche”, meaning seling enough subscription rights to fund the exercise of the remaininng rights. This often results in a certain discount for the subscription rights

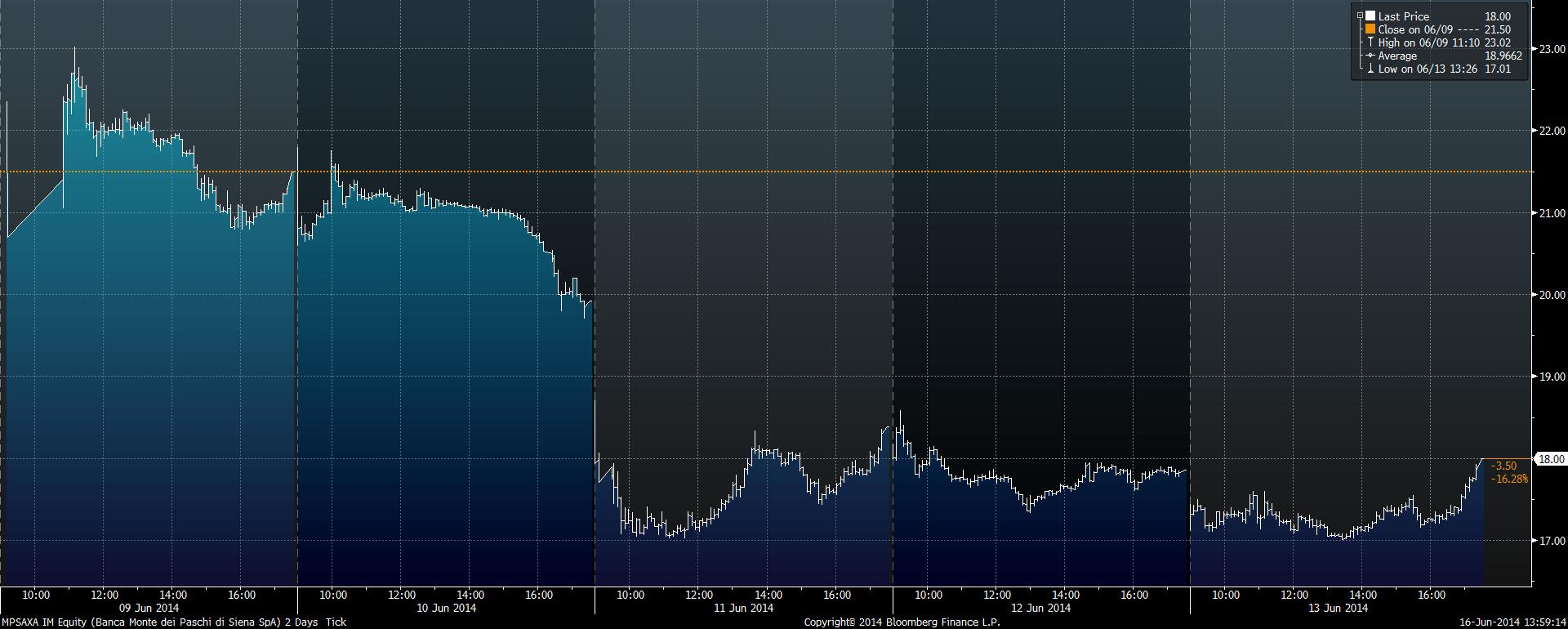

In BMPS’s case, the first strange thing ist the price of the underlying stock:

Adjusted for the subscription right, the stock gained more than 20% since the start of the subscription right trading period and it didn’t drop before, quite in contrast, the stock is up ~80% YTD. As a result of course, the subscription right should increase in value. But this is how the subscription rights have performed since they started trading:

It is not unusual that the subscription rights trade at a certain discount, as the “arbitrage deal”, shorting stocks and going long the subscription right is not always easy to implement.

At the current price however, the discount is enormous::

At 1,95 EUR per share, the subscription right should be worth (214/5)* (1,95-1,00)= 40,66 EUR against the current price of 18 EUR, a discount of more than 50%. The most I have seen so far was 10-15%. So is this the best arbitrage situation of the century ?

Not so fast.

First, it seems not to be possible to short the shares, at least not for retail investors. Secondly, different to other subscription right situations, the subscription right are trading extremely liquid. Since the start of trading on June 9th, around 560 mn EUR in subscription rights have been traded, roughly twice the value of the ordinary shares. The trading in the ordinary shares themselves however is also intersting, trading volume since June 9th has been higher than the market cap.

Thirdly, for a retail investors, the banks ususally require a very early notice of exercise. So one cannot wait until the trading period and decide if to exercise or not, some banks require 1 week advance notice or more. My own bank, Consors told me that I would need to advice them until June 19th 10 AM, which is pretty OK but prevents me from buying on the last day.

In general, in such a situation like this the question would be: What is the mispriced asset, the subscription right or the shares themselves ? Coming from the subscription right perspective, the implicit share price would be 1+ (18/((214/5)*1,95-1)))= 1,44 EUR. This is roughly where BMPS traded a week before the capital increase.

For me it is pretty hard to say which is now the “fair” price, the traded stock price at 1,95, the implict price from the rights at 1,44 or somewhere in between. As the rights almost always trade at a discount, even in non-Italian cases, one could argue that there might be some 10-15% upside in buying the shares via the rights. On the other hand, I find the Italian stock market rather overheated at the moment and the outstanding BMPS shares are quite easy to manipulate higher due to the low market cap of the “rump shares” at around 200-250 mn EUR.

The “sure thing” would be to short the Stock at 1,96 EUR, but that doens’t seem to be possible.

Summary:

Again, this “Italian right” capital raising creates a unique situation, this time with a price for the subscription right totally disconnected from the share price.

Nevertheless I am not quite sure at the moment what to to with this. One strategy would be to buy the subscription right now and then sell the new shares as quickly as possible, but it looks like that this is exactly what the “masterminds” behind this deal have actually want investors to do. They don’t care about the share price, they just want to bring in 5 bn EUR in fresh money and an ultra cheap subscription right is the best way to ensure an exercise. In this case we should expect a significant drop in the share price once the new shares become tradable. So for the time being am sitting on the sidelines and watch this with (great) interest as it is hard for me to “handicap” this special situation at the moment.

Curious, were people able to successfully execute the trade by shorting the CFDs?

Die Banken scheinen ihre Aktien bekommen zu haben.

Schon >150 mio Umsatz. Kurs bei 1,55 Euro.

Auch interessant, dass Aktionär nicht Aktionär ist 😀

nicht ganz überraschend. irgendwie müsssen die Hedgefonds ja ihre 2%+20% rechtfertigen.

Nunja… jeder der BZR kaufte sollte erstmal im plus sein. 1,55 Euro wären ein BZR-Kurs von 23,x Euro. Vllt gehts ja nach der Verkaufswelle wieder Richtung 1,70 Euro. Mir würde das vollkommen reichen

In Italy there is still the good old “t+3” settlement rule (but not for long: http://www.securitiesservices-newsletter.com/banks-and-brokers/article/bye-bye-t3-settlement-cycle). Instituationals started already selling today (Wed.). That also explains the almost 300 Mio shares traded today.

It was a profitable trade if you assume rights bought at around 19 EUR (gives you an entry at 1.45 EUR) and sold today at 1.55 EUR for a nice profit of 10cts per share. 7% before any fees is not that bad.

Interesting to see the price developing over the next few days when others are allowed to sell. My guess is around 1.60 EUR (just a guess).

caute,

thanks for the comment. I didn’t know that Italy take one day more to settle….

mmi

If I look at the current shareprice, it seems to be “glued” to the 1,50 EUR….very “natural” intraday chart.

why are the shares still trading so high?, maybe the rights were eventually underpriced and the stock as such wasn’t overpriced? or should one expect a sharp drop next week and why is it not priced in today?..

I would expect shares to drop to their theoretical after issue price, of around 1.55. This is also indicated by the futures markets (the August future was yesterday trading with a bid-ask of around 1.45/1.55). I guess the reason for the high price of the share is technical nature. Short squeeze or perhaps some problems that people who have to follow indices have to buy shares ahead of the trading of new shares? After all, its a massive increase in the number of new shares, and this may cause some problems. Newspaper articles also refer to “techical issues”…

I think it will be interesting to see when the price drops. If shares are delviered on Monday,June 30th, then institutional clients will be already start selling 2 business days before, which will be Thursday 26th. As shares settle t+2, institutional investors will most likely have this 2 day advantage against private investors who most likely will be able to enter orders only on monday.

why are they able to start selling 2 days before the delivery? the shorting is still not allowed(?)

does anyone know, when do they allocate the new shares, if one has exercised the rights?

According to IB, June 30!

thanks.

Even if the costs for borrowing are around 300% – it would still make sense to borrow at this level.

So in case you can find me a lending happy to take it, also for 300%.

I entered a position in the rights and bot Puts strike 1,5 july @ 0,115 (hard to get, spread is enormous, the only option series where a reasonable price was available), so i have a maximum risk of round about 3%…

Even if you could sell short (which I can assure you, you cannot) the borrowing cost is currently 300%. That is why the price rallied. -recalls.

Falls noch eine Story zum untersuchen brauchst. Third Avenue Real Estate Value Fonds hat scheinbar auch falsch gepreiste Bezugsrechte bei einer spanischen Immo-Firma in Q1 erworben. Kurs der Firma hat sich jedenfalls verdoppelt.

Click to access TAREX-Letter-2Q-2014.pdf

http://www.bloomberg.com/quote/COL:SM

Heute mal fetter Einbruch zu Beginn und jetzt gleich wieder hoch 😀

Die Anrechte scheints kaum zu interessieren 😀

Bin mal gespannt, ob Freitag noch ein großes Finale bei der Story kommt

this is also an output of the new short selling rules that where implemented over the last two years in the EU.

This kind of exaggeration is what happens when you limit short selling in the market.

Theoretical market cap of BMPS is now at 13,5 bn. Not bad after like 2 bn 8 weeks ago plus the 5 bn new cash….

BTW, short borrow not available and borrow rate 246%. So prayers to the god of market efficiency are definitely required.

Short in the money calls, buy the rights and pray…

The few prices on futures and options that are available indicate that market expects sharp drop in price of underlying (ask on August future is 1.58). News articles (googling) also indicate technical issues and demand for stock by shorts that drive up price. So my bet for the fair value for the stock would be around the theoretical ex price of around 1.55 (=(25+1*214/5)/(1+214/5) where 25 is price of stock before the rights were issued).

Ich versteh nur die Logik nicht. Eine Woche lang wurde recht liquide zu 1,70-1,80 gehandelt und manche konnten sich nicht eindecken?

Hast dir mal die Übernahmschlacht um deine R.Stahl angeschaut. Da hat Scherzer jetzt einen öffentlichen Brief ans Management geschrieben 😀 Auch ne lustige Geschichte.

Maybe I should have titled the post “the great Italian Squeeze” or “The Italian Corner”…..this looks like some investors really get burned here. Thank god, there were no shorts available….

Aktie bei 2,51 euro und BZR inzwischen bei 20 Euro … Vllt geht das BZR ja doch noch Richtung fairen Wert bis zum Freitag …

Are the rights exerciseable on every day up to the 27th July?

sorry, i meant June.

Just tried to sell the CFDs through Saxo and they take you all the way to klick “Place Order”, before they tell you that “shorting for this security has been disabled”. Does anyone have a view, whether there is value in the rights stand alone? The capital increase takes their CET1 to 13.3% and according to their Q1 presentation, their core business is relatively stable

mrt, I don’t want to sound arrogant, but if you have no experience with subscription rights, then this might be not a good first investment.

Of course they ar NOT exerciseable until 27th of June. It depends on your bank, most banks will already cut off early this week.

When you say ‘this is roughly where it traded a week before’ with regards to implicit value of rights, do you mean in terms of price to book?

I meant adjusted for the subscription right

I think it’s a safe bet that the right side of this trade is the side you can’t take: shorting the common. If you have a broker that offers CFD’s on this name I wouldn’t hesitate to build a long/short position. Pretty awesome if you would be able to pull that off. I’ve checked my broker and while they have CFDs on this name you can only do closing transactions.

What do you mean by “do closing transactions”? I am with IB and they offer CFDs. They also offer futures, which I am considering as well.

With IB, when you try to make the short on the CFD, it doesn’t allow you to do it because of being only able to close positions. This was just confirmed by IB that they can’t clear the trades in which you’d open a new position, i.e. short sell the CFD. Don’t know whether this could be done with futures or options.

i dont really get it, here (http://english.mps.it/NR/rdonlyres/FBA3E79F-206E-40FB-AD49-70923D65FEC7/72641/PressReleaseMPSFinaltermsandsupplementapprovalENG.pdf) it says “at a ratio of 214 new BMPS shares for 5 BMPS shares held.” so you need to buy the 1 subscription-right-share (+ 5 old ordinary shares?) to get to buy 214 new ordinary shares for 1eur ?

You need 5 rights (@18,29 euro) to buy 214 “new” shares (@1 euro) ==> (5×18,29 + 214×1)/214 =1,427 euro. Shares currently@2,21 euro ==> Discount= 35,5 %. Or the rights should be at 52 Euro.

The problem is ” short share/CFD”. If you/we would find an opportunity to short the shares it would maybe the “best arbitrage situation of the century “. Currently: Shares @2,21 euro and so the rights “should” be @52 euro

At Eurex you could find some put-options. But strike price minus price of the put-options is about price of the rights.

What exactly is a CFD? And does the CFD trade in line with the stock such that it would make sense to short the CFD against the rights?

http://en.wikipedia.org/wiki/Contract_for_difference

Interesting case, thanks for bringing it up! Did I understand correctly, that if I buy 5 rights issues and exercise them, I get to buy 214 shares of BMPS at 1EUR? So assuming one can go long rights issue and short share/CFD, one would want to exercise the rights (unless the price of them rises, when it’d make sense to sell them) and then afterwards sell the new shares and buyback the shorted shares/CFDs?

very interesting article! Price currently up 15%, one can’t help but wonder whether the deep-pocketed bookrunners (JPM, GS, MS) are not pulling the old trick Milken did with junk bonds, moving shares from the right hand to the left giving the illusion of a price increase and of liquidity.

Does anyone have a link to the prospectus? I’ve been digging on their site but can’t seem to find it.

Also, what do you mean by “rump shares” when referring to the market cap?

Es ist übrigens die älteste Bank der Welt und m.W. auch im ES500. Also nichts kleines oder unbekanntes oder so 🙂

Heute ging der Kurs ganz entspannt 15% auf 2,10 Euro hoch (bei +20% wird wieder ausgesetzt), und das BZR, außer am Anfang, quasi unverändert. 2,10 Euro sind 47 Euro BZR. Damit 61 % Discount im Augenblick.

Der primitive CFD-Handel von comdirect hat nichts zu Monte dei Paschi. Und auch nichts zu Adler/Estavis, da hatte ich damals auch schon geschaut.

Ich bin mir nicht sicher, wie die Bezugsrechte in den Indizes berücksichtigt sind…evtl gibt es da auch Arbitragemöglichkeiten.

Interesting. Short sale of the shares via CFDs seems to be possible. Regards, Matthias

at which bank ?

I can trade them through IB…