Banca Monte dei Paschi Siena (BMPS)- Another deeply discounted rights issue “Italo style”

Capital Raising in Italy is always worth looking into. Not always as an investment, but almost always in order to see interesting and unusal things. I didn’t have BMPS on my active radar screen, but reader Benny_m pointed out this interesting situation.

Banca Monte dei Paschi Siena, the over 600 year old Italian bank has been in trouble for quite some time. After receiving a government bailout, they were forced to do a large capital increase which they priced in the beginning of last week.

The big problem was that they have to issue 5 bn EUR based on a market cap of around 2,9 bn.

After a reverse 1:10 share split in April, BMPS shares traded at around 25 EUR before the announcement. In true “Italian job” style, BMPS did a subscription rights issue with 214 new shares per 5 old shares at 1 EUR per share, in theory a discount of more than 95%.

The intention here was relatively clear: The large discount should lead to a “valuable” subscription right which should prevent the market from just letting the subscription right expire. What one often sees, such as in the Unicredit case is the following:

– the old investors sell partly already before the capital increase in order to raise some cash for the new shares

– within the subscription right trading period, there will be pressure on the subscription right price as many investors will try to do a “operation blanche”, meaning seling enough subscription rights to fund the exercise of the remaininng rights. This often results in a certain discount for the subscription rights

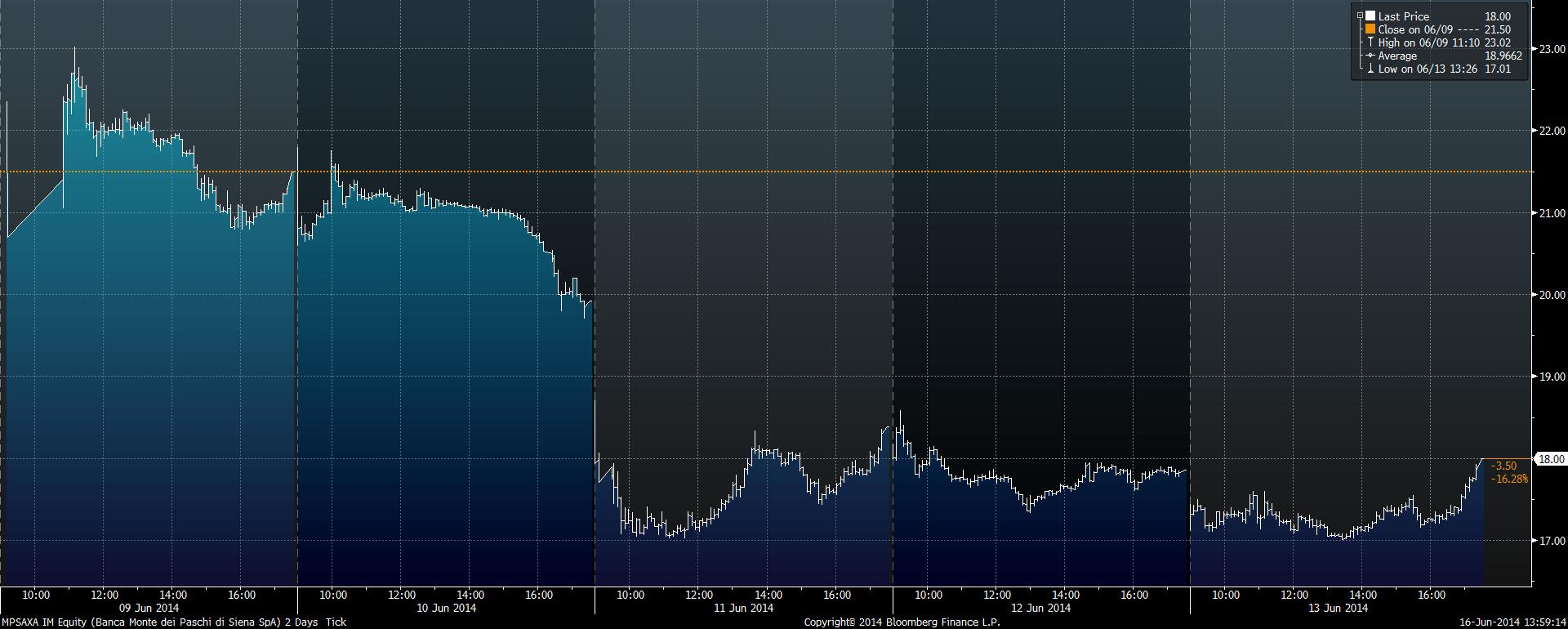

In BMPS’s case, the first strange thing ist the price of the underlying stock:

Adjusted for the subscription right, the stock gained more than 20% since the start of the subscription right trading period and it didn’t drop before, quite in contrast, the stock is up ~80% YTD. As a result of course, the subscription right should increase in value. But this is how the subscription rights have performed since they started trading:

It is not unusual that the subscription rights trade at a certain discount, as the “arbitrage deal”, shorting stocks and going long the subscription right is not always easy to implement.

At the current price however, the discount is enormous::

At 1,95 EUR per share, the subscription right should be worth (214/5)* (1,95-1,00)= 40,66 EUR against the current price of 18 EUR, a discount of more than 50%. The most I have seen so far was 10-15%. So is this the best arbitrage situation of the century ?

Not so fast.

First, it seems not to be possible to short the shares, at least not for retail investors. Secondly, different to other subscription right situations, the subscription right are trading extremely liquid. Since the start of trading on June 9th, around 560 mn EUR in subscription rights have been traded, roughly twice the value of the ordinary shares. The trading in the ordinary shares themselves however is also intersting, trading volume since June 9th has been higher than the market cap.

Thirdly, for a retail investors, the banks ususally require a very early notice of exercise. So one cannot wait until the trading period and decide if to exercise or not, some banks require 1 week advance notice or more. My own bank, Consors told me that I would need to advice them until June 19th 10 AM, which is pretty OK but prevents me from buying on the last day.

In general, in such a situation like this the question would be: What is the mispriced asset, the subscription right or the shares themselves ? Coming from the subscription right perspective, the implicit share price would be 1+ (18/((214/5)*1,95-1)))= 1,44 EUR. This is roughly where BMPS traded a week before the capital increase.

For me it is pretty hard to say which is now the “fair” price, the traded stock price at 1,95, the implict price from the rights at 1,44 or somewhere in between. As the rights almost always trade at a discount, even in non-Italian cases, one could argue that there might be some 10-15% upside in buying the shares via the rights. On the other hand, I find the Italian stock market rather overheated at the moment and the outstanding BMPS shares are quite easy to manipulate higher due to the low market cap of the “rump shares” at around 200-250 mn EUR.

The “sure thing” would be to short the Stock at 1,96 EUR, but that doens’t seem to be possible.

Summary:

Again, this “Italian right” capital raising creates a unique situation, this time with a price for the subscription right totally disconnected from the share price.

Nevertheless I am not quite sure at the moment what to to with this. One strategy would be to buy the subscription right now and then sell the new shares as quickly as possible, but it looks like that this is exactly what the “masterminds” behind this deal have actually want investors to do. They don’t care about the share price, they just want to bring in 5 bn EUR in fresh money and an ultra cheap subscription right is the best way to ensure an exercise. In this case we should expect a significant drop in the share price once the new shares become tradable. So for the time being am sitting on the sidelines and watch this with (great) interest as it is hard for me to “handicap” this special situation at the moment.