Some thoughts on (Australian) Leasing / Equipment rental companies

One very interesting aspect about Australian stocks is that there are many listed companies whose main activity is some sort of leasing. Those companies are all quite profitable and relatively cheap.

So far I only had looked at one leasing company, AerCap, the US based Aircraft leasing company.

Leasing business

The leasing business simply stated is asset based lending without a banking license. The client, instead of buying something outright and recieveing a loan from a bank, “leases” the good, pays installments and hands over the good after some time back to the lessor.

The leasing company therefore has the following main risks to bear:

- potential Defaults from clients

- value of goods depreciates more than planned

- funding risk

Compared to a bank, the funding risk and funding cost is often higher, also the direct exposure to the price of used goods is higher. Banks “only” have exposure to underlying prices if a borrower defaults.

On the other hand, people/businesses who lease things often seem to be less sensitive on implied interest rates then they would be with a stand-alone loan. That allows many leasing companies to earn quite decent margins. Plus, under current IFRS reporting rules, socalled “Operating leases” do not count as debt, therefore leasing is interesting for (small) companies who want to avoid reporting (too) much debt.

Similar to banks, a general economic downturn is usually a big risk. First of all, default rates go up and secondly, often the value of the returned goods (for instance cars) go down while the funding cost goes up. The best protection against this risk is both, a diversified product portfolio as well as a diversified client portfolio.

For AerCap for instance, in my opinion there is significant implicit risk because they only lease one type of products (planes) to one single industry (airlines).

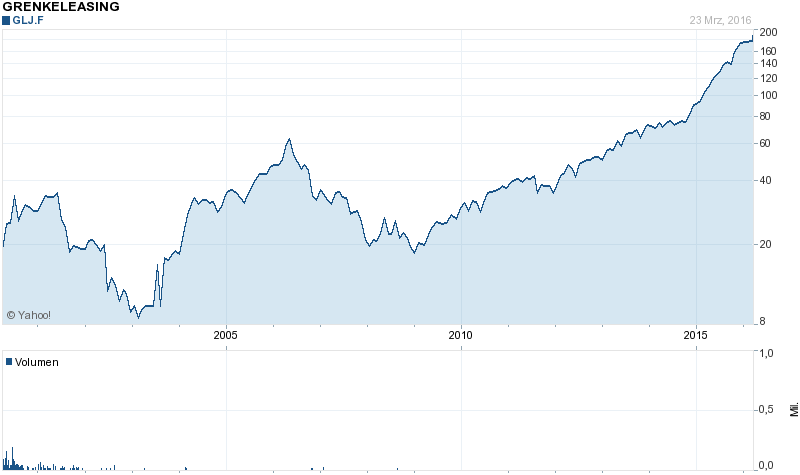

Grenke Leasing – German “Superstar” Leasing company

In Germany, the most well known and most succesful leasing company is Grenke Leasing. I often looked at them but always thought that they are too expensive (BIG mistake). This is how the stock price developed over the last 20 years:

Since it’s IPO in 2000, Grenke returned 16,7% p.a. vs. ~2% p.a. for the German DAX. The valuation of Grenke has nothing to do with any banks:

Market Cap 2.759 mn EUR

P/E 34

P/B 4,7

P/S 8

Grenke has very succesfully rolled out its business outside of Germany, starting in neighbouring Europe and then further into countries like Brazil and Turkey. The CEO and founder Wolfgang Grenke still owns 40% and has proven thatg he is a good capital allocator.

Grenkes “secret” for success in my opinion seem to be:

- they have an industrialized efficient workflow to procure small ticket IT leases very efficiently (small businesses are their main clients)

- they lease out fast depreciating assets with very little risk on asset values after a lease expires

- They grew organically

- The have a very diversified client base

At current prices, I would not want to own Grenke but the case clearly shoes that Leasing can be very good business if done right. What I am personally wondering is, why noone has yet started an online competitor yet. I think this might be more interesting than peer-to-peer lending.

Equipment rental companies

Equipment rental companies in my opinion are relatively similar to leasing companies with one big difference: The rental period is much shorter than with leasing contracts. This has two major implications:

Positive: The credit risk is lower

Negative: The business is much more directly exposed to the business cycle. Especially if a company rents out long living assets, this will create a significant mismatch risk between the financing of those assets and the volatility of cash inflows.

Interestingly, one of my own stocks, Aggreko could be actually considered to be an “equipment rental” business and the most recent development clearly shows the issues in those businesses. Aggreko has the big advantage that they have very little debt and are very flexible in moving their merchandise. If you compare that with leveraged owners of drilling rigs, the difference becomes quite clear.

So for an equipment rental company, I think it is even more important that the underlying assets have short useful lives and that there is a diverse customer base.

Australian Leasing/Equipment rental companies

This is a quick overview of companies I found up to now (and some valuation metrics compared to Grenke Leasing:

| Name | Mkt Cap (AUD) | P/E | P/B | P/S | Dvd Yld | 5Yr Avg ROE LF | Bas EPS 3Yr Gr | Debt/Com Eq LF |

|---|---|---|---|---|---|---|---|---|

| THORN GROUP LTD | 278,0 | 8,86 | 1,39 | 0,89 | 6,8 | 17,1 | 2,5 | 85,4 |

| SG FLEET GROUP LTD | 871,2 | 20,83 | 4,60 | 4,75 | 3,3 | #N/A N/A | 82,1 | |

| FLEXIGROUP LTD | 889,9 | 8,84 | 1,54 | 2,14 | 6,7 | 18,1 | 9,0 | 201,0 |

| SILVER CHEF LTD | 320,2 | 15,14 | 3,08 | 1,60 | 4,0 | 20,8 | 13,9 | 230,7 |

| GRENKELEASING AG | 4.073,1 | 34,17 | 4,63 | 7,91 | #N/A N/A | 14,5 | 21,6 | 396,7 |

| BOOM LOGISTICS LTD | 35,6 | #N/A N/A | 0,20 | 0,21 | 0,0 | -21,2 | #N/A N/A | 29,3 |

Quick scan:

Boom Logistics

Boom Logistics is an equipment rental company, renting out cranes. Forager has a 6,4% stake. This is clearly a “deep value asset play” which is not what I am looking for at the first place. There is also clearly a certain concentration risk with reghard to both, the leased goods as well as the sector they have as clients.

Flexigroup

This one looks actually quite attractive at first sight. The major part of the business seems to be IT leasing plus some consumer finance activities. On the other hand, the company made a lot of acquisitions in the past financed by new shares (share count increased +65% since IPO in 2006) and the old CEO was fired AFTER a large acquisition was made in NEw Zealand.

Thorn Group

Thorn Group seems to be a pure consumer leasing/financing company. At first sight it looks interesting, due to low gearing. Sharecount increased as well since IPO, but to a smaller extent. MAde some acquisitions in the past but smaller ones. Changed management in 2014/2015, CEO has only relatively small stake in company.

Silver Chef

Silver Chef looks much more expensive then Boom, Flexigroup or Thorn. It is essetially an equipment rental company, historically for kitchen apliances for restaurants. However it is also the company with the best profitability and the best growth. The CEO is also the founder and owns 25,6% of the company. As Id o like owner tun businesses, this is a clear plus.

SG Fleet Management

SG looks expensive and it is not obvious why. The seem to offer additional services on top of leasing but at first sight it doesn’t look that interesting.

Quick summary:

Grenke clearly shows taht leasing can be a very attractive business if done the right way. My first quick scan of Australian Leasing/rental equipment companies yielded some potentially interesting cases, with Silver Chef the most interesting, followed by Flexigroup and Thorn.

have you recently looked at flexigroup? Lost more than 30% in one month with a new low for the last couple of years.

no, but thanks for the heads up …

thanks for the suggestion. But If you would have read the first post, you would know that I am not so hot on the mining sector.

You may be interested in Ausdrill, a mining contractor in a related business mainly with gold exposure.