AerCap Holdings N.V. part 2 – Less tangible at a second glance

So after my first look into David Einhorn’s long pick AerCap last week, I want to follow up with some more detailed analyis in a second step.

By the way, a big “thank you” for all the qualified comments and Emails I got already after the first post, that’s the best return on investment on a blog post I can get !!!

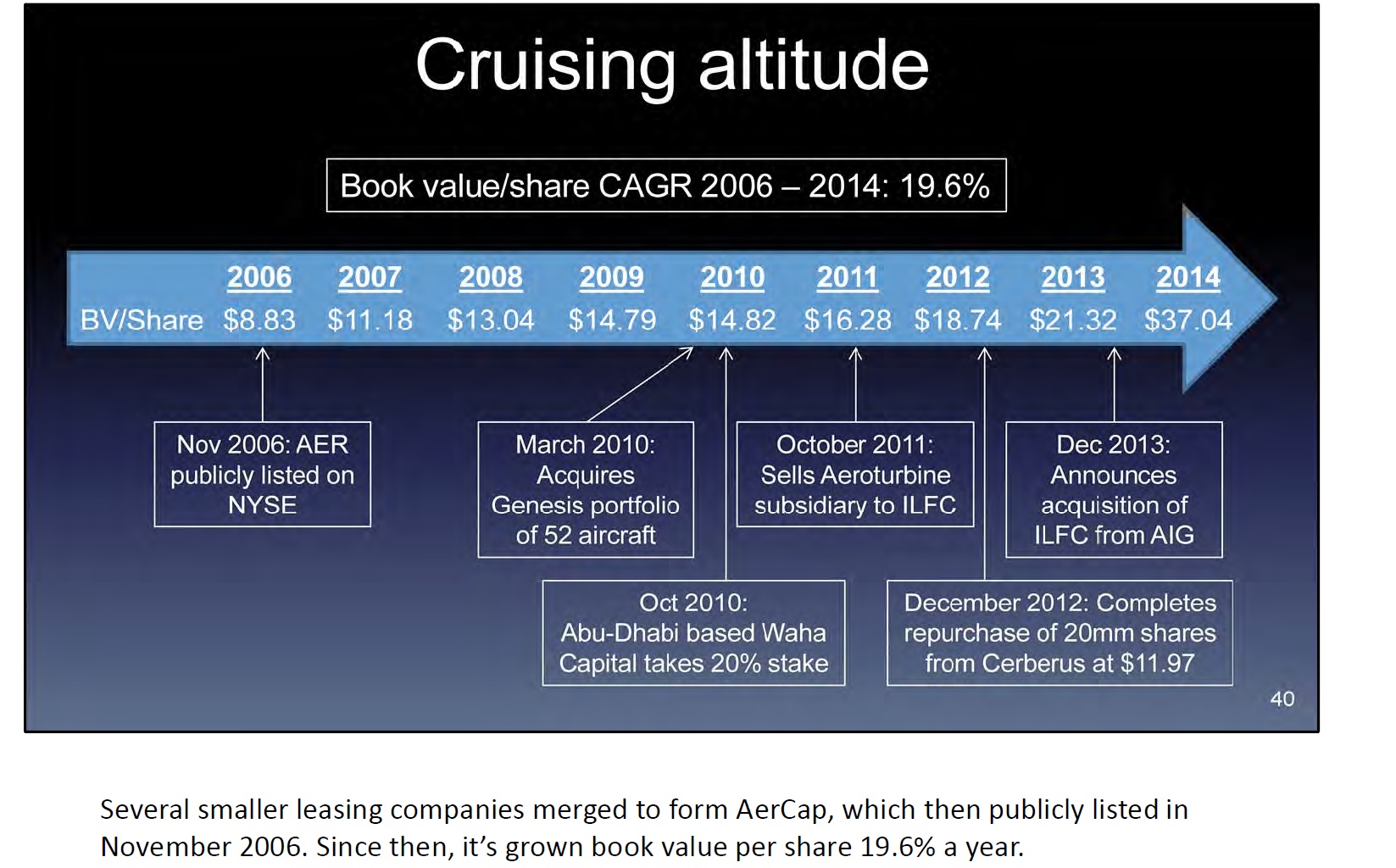

The book value story growth

This was for me one of the core slides of Einhorn’s deck:

I mean you don’t have to be a genius to understand this: A company which trades near book value and compounds 20% p.a. is pretty much a no brainer. However, if I look at the developement of book values for financial companies, I always look at both, stated and tangible book value per share.

In AerCap’s case, the comparison looks interesting:

| BV per share | TBV share | |

|---|---|---|

| 2006 | 8,83 | 8,3493 |

| 2007 | 11,18 | 10,6041 |

| 2008 | 13,04 | 12,4083 |

| 2009 | 14,79 | 14,3448 |

| 2010 | 14,82 | 14,3798 |

| 2011 | 15,26 | 15,0608 |

| 2012 | 18,72 | 18,5592 |

| 2013 | 21,32 | 21,2334 |

| 2014 | 37,04 | 16,174 |

| CAGR | 19,6% | 8,6% |

| CAGR 2006-2013 | 13,4% | 14,3% |

This table shows two things: Before the ILFC transaction, stated book values and tangible book values were pretty much the same and compounding around 13% p.a. Still pretty good but clearly not 20%. In 2014 however, with the ILFC deal something interesting happened: The book value per share doubled but tangible book value dropped.

The ILFC deal

So this is the right time to look into the ILFC deal. The two main questions for me are:

a) why did the book value per share increase so much ?

b) why did tangible book value per share actually decrease ?

This is how AerCap presents what and how they paid for ILFC:

So AerCap paid the majority of the purchase with own shares, 97,56 mn shares valued at 46,49 USD. Issuing new shares always has an impact on book value per share if the issue price is different from the book value. Let’s look at an example:

We have a company which has issued 100 Shares at 50 EUR book value per share and 100 EUR market value (P/B =2). So the total market value is 10.000, total book value is 5000. If the company now issues another 100 Shares at 100 EUR market value, we have 200 shares outstanding and 5000+10000 = 15.000 EUR total book value. Divided by 200 stocks we now have 75 EUR book value per share or a 50% increase in book value per share for the old shareholders. So issuing shares above book value increases book value per share automatically.

In AerCap’s case, it worked more or less the same way: AerCap had ~113 mn shares outstanding with a book value of around 21,30 USD per share. So issuing 97,56 mn share at a steep premium at 46,49 of course increased book value per share dramatically. The transaction alone would have increased the book value to ((113*21,30)+(97,56*46,49))/(113+97,56)= 32,97 USD per share or an increase of ~50%.

So how is this to be interpreted ? Well, clearly it was a smart move from AerCaps management to pay with its owns shares at such a nice price. On the other hand, one should clearly not mistake this a a recurring kind of thing. I would not use the historic 20% p.a. increase in ROE as expectation for the future but rather something like 13% or so in the past.

Intangibles

After looking into how much and in what form AerCap was paying, let’s look now what they actually got:

Yes, they got a lot of planes and debt. Interestingly they assumed more debt than book value of the planes. Altogether they did get a lot of intangible assets. All in, AerCap bought 4,6 bn intangibles which is around 80 mn more than equity created through the new shares. So at the end of the day, one could argue that the new shares have been exchanged more or less 1:1 against intangible assets.

The largest part of this is a 4 bn USD position called “Maintenance rights intangible” which for me is something new. This is what they say in their 20-F filing:

Maintenance rights intangible and lease premium, net

The maintenance rights intangible asset arose from the application of the acquisition method of accounting to aircraft and leases which were acquired in the ILFC Transaction, and represented the fair value of our contractual aircraft return rights under our leases at the Closing Date. The maintenance rights intangible asset represents the fair value of our contractual aircraft return right under our leases to receive the aircraft in a specified maintenance condition at the end of the lease (EOL contracts) or our right to an aircraft in better maintenance condition by virtue of our obligation to contribute towards the cost of the

maintenance events performed by the lessee either through reimbursement of maintenance deposit rents held (MR contracts), or through a lessor contribution to the lessee. The maintenance rights intangible arose from the application of the acquisition method of accounting to aircraft and leases which were acquired in the ILFC Transaction, and represented the fair value of our contractual aircraft return rights under our leases at the Closing Date. The maintenance rights represented the difference between the specified maintenance return condition in our leases and the actual physical condition of our aircraft at the Closing Date.For EOL contracts, maintenance rights expense is recognized upon lease termination, to the extent the lease end cash compensation paid to us is less than the maintenance rights intangible asset. Maintenance rights expense is included in Leasing expenses in our Consolidated Income Statement. To the extent the lease end cash compensation paid to us is more than the maintenance rights intangible asset, revenue is recognized in Lease revenue in our Consolidated Income Statement, upon lease termination. For MR contracts, maintenance rights expense is recognized at the time the lessee provides us with an invoice for reimbursement relating to the cost of a qualifying maintenance event that relates to pre-acquisition usage.

The lease premium represents the value of an acquired lease where the contractual rent payments are above the market rate. We amortize the lease premium on a straight-line bases over the term of the lease as a reduction of Lease revenue.

This sounds quite complicated and for some reason part of the sentences seem to have been duplicated. If I understand correctly, they assume that the underlying value of the aircraft is higher than the book value of the acquired planes. To be honest: I do not have any clue if this is justified or not.

However, as those intangibles are significant (more than 50% of book value), the case gets a lot less interesting for me. Intangibles created via M&A activity are in my experience always difficult, especially if it is esoteric stuff like this. It’s also a big change to the past of AerCap. Historically, they were carrying very little intangibles.

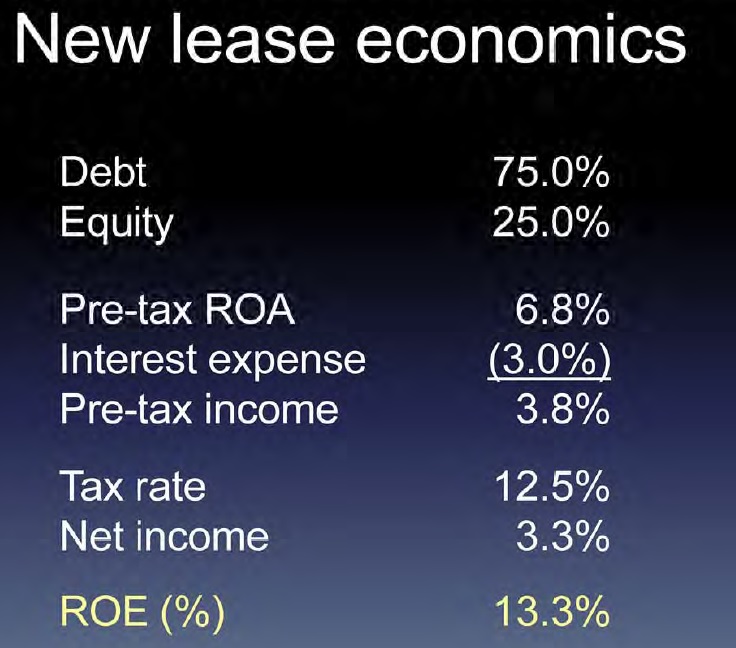

Funding cost & ROE

This was Einhorn’s prospective ROE calculation:

One of the key assumptions is a 3% funding cost. So let’s do a reality check and look at the expected pricing of AerCaps new bond issue. This is from Bloomberg:

Aercap $750m TLB Talk L+275, 99.75, 0.75%; Due April 30

By Krista Giovacco

(Bloomberg) — Commits due April 30 by 12pm ET.

Borrower: Flying Fortress Holdings LLC, a subsidiary of AerCap Holdings and International Lease Finance Corp., largest independent aircraft lessor

$750m TLB due 2020 (5 yr extended)

Price Talk: L+275

OID: 99.75

Libor Floor: 0.75%

Call: 101 SC (6 mos)

Fin. Covenants: Max LTV test

Existing Ratings: Ba2/BB+ (corp.); Ba1/BBB-, RR2 (TLB)

So AerCap is funding at a spread of 2,75% vs. LIBOR. With the 10 year USD LIBOR at 2,00%, funding would be way more expensive than the 3% assumed by Einhorn. Maybe the fund floating rate, but then the whole company would rather be a bet against rising interest rates than anything else. On a “like for like” basis without structural interest rate risk, I don’t think AerCap will generate a double-digit ROE at current spreads.

Business case & competitive environment

Within the comments of the first post, some people argued that the company is not a financing company but that the access to Aircraft is the value driver. Buying cheap aircraft from manufacturers and then selling (or leasing) them with a mark-up to clients then looks like some kind of Aircraft trading business.

For me however there is one big problem with such a business model. Retailing or wholesaling any merchandise is then most attractive as a business when 3 criteria are met:

– there are a lot of suppliers

– there are a lot of clients

– you can create a competitive advantage via physical distribution networks

In AerCap’s case, the biggest problem is clearly that there are not that many suppliers but only 2, Boeing and Airbus. Both don’t have much incentive to let any intermediary become too large so they will most likely encourage competition between Aircraft buyers.

Secondly, as far as I understand, there is no physical distribution network etc. behind AerCap’s business. So entering the market and competing with AerCap in the future doesn’t look so difficult for anyone with access to cheap capital.

Clearly, as in any opaque trading business, an extremely smart trader can always make money but it is important to understand that at least in my understanding there are no LONG TERM competitive advantages besides the purchase order flow from ILFC.

That the barrier to entry the business is not that high is proven by no other than Steven Udvar-Hazy the initial founder of ILFC and his new company Air Lease.

IPO’ed in 2010 and now the company is already a 4 bn USD market company 5 years later. Interestingly, AIG sued Air Lease in 2012 because they

were able “to effectively steal a business,” and reap a windfall at the expense of ILFC, the world’s second-largest aircraft lessor by fleet size. It described how some employees, while still working at ILFC, downloaded confidential files and allegedly diverted deals with certain ILFC customers to Air Lease, before leaving to join that firm. The companies are in the business of buying aircraft and leasing them to commercial airlines all over the world.

So to me it’s not clear what AerCap actually bought. It seems the “secret sauce” of ILFC seems to have been transferred to competitor Air Lease already. Interestingly, the lawsuit was settled a few days ago at a sum of 72 mn USD. I found that quote from Udvar-Hazy interesting:

“I want to make it clear that there is no secret sauce in the aircraft leasing business,” Hazy told analysts on a conference call. “ALC’s success is a result of a strong management team with extensive experience and solid industry relationships.”

Summary:

My problem with AerCap is the following: The financial part of the company, which I feel that I can judge to a certain extent, does not look attractive but rather risky to me. The Aircraft “buying and trading” segment on the other hand seems to be the more attractive part but for me too hard to judge in a reasonable way.

So for the time being, this is clearly not an investment for me. To look further into AerCap, two things need to happen: First they need to regain their investment grade rating and funding cost will need to drop to the 3% that Einhorn is assuming and secondly, there should be a clear impact on the share price from a potential sale from AIG.

In the current market environment clearly anything can happen and a multiple expansion could bring nice profits but personally, in a direct comparison I prefer the LLoyd’s case.

If the debt lowers the return on assets by 3%, would the cost not be 3/0,75= 4%?

“this December, we have raised $1.9 billion of funding at a blended cost of 3.6% and we expect to close approximately $1 billion of additional long-term funding”

They target 30% secured 70% unsecured. I would like more deleveraging than buy-back, but the market seems to like buy-backs more.

wow, Aercap is down 1/3 since my post. Even Lloyd banking did better 😉

I believe the decline is a function of the huge debt portion of the total EV. With less leverage the company could be a great buy here. But who knows.

For now they are still earning money despite continually writing down the maintenance intangibles from the ILFC transaction:

“Our leasing expenses increased by $329.4 million, or 494%, to $396.1 million during the nine months ended September 30,

2015 from $66.7 million during the nine months ended September 30, 2014. The increase is primarily due to $255.5 million higher maintenance rights expense recognized during the nine months ended September 30, 2015 and $47.8 million higher regular aircraft transition costs, lessor maintenance contributions and other leasing expenses recognized during the nine months ended September 30, 2015 as compared to the nine months ended September 30, 2014. These increases were primarily related to the ILFC Transaction.”

already more defaults, but low base rate:

” In addition, we recognized expenses of $34.9 million relating to airline defaults and restructurings during the nine months ended September 30, 2015 as compared to $8.8 million during the nine months ended September 30, 2014.”

I think their biggest problem is the funding costs. Their 10 year CDS spread for instance “exploded” form 250 bps p.a. to 400 in the last 2 weeks. At that level, they are not competitive. As a “shadow bank” you cannot do business if you have to pay 400 bps spread.

Additionally, their EM exposure is significant.

Do you think AER is now a buy at under 30 (USD) or would you continue to avoid the stock?

I don’t know. It’s not the type of business I would want to own right now.

Steven Romick is not well known but a splendid investor and, judging by his presentations, also a very fine and humble person.

His latest presentation makes an interesting read. http://www.fpafunds.com/docs/special-commentaries/cfa-society-of-chicago-june-2015-final1.pdf?sfvrsn=2

He comes to the same conclusion about the aircraft leasing business but touching upon different things.

Thanks for the link. I do read the FPA reports from time to time but I haven’t seen that one.

Very interesing article, thanks!

I am invested in the company and wrote about it on my blog. For those of you who are interested (and understand the german language): http://value-student.de/investment-thesis-aercap/

I think my arguments are similar to those of David Einhorn. My ROA & ROE calculation looks very similar as well. But I cited my sources. That might be a good starting point to get a better understanding of the underlying economics of the business.

I think your evaluation of the competitive environment is to simple. IATA used the 5 Forces Model to provide insights regarding the industry in “Profitability and the air transport value chain”.

Furthermore I think you are overestimating the power of Boing and Airbus. AerCap is a significant customer. ILFC was an important launch customer of some recently developed airplanes.

Your arguments on the ILFC transaction are very interesting. Nerver heard of the lawsuit.

well, if we would have the same opinion, the stock market would be very boring…..

One additonal remark: In a “hedge fund hotel” stock you should be careful that you are not the one wh needs to switch the light off at the end….

mittlerweile tummeln sich immer mehr bei Aercap herum. Auch Leo Cooperman hat Aercap bei der letzten IRA Veranstaltung vorgestellt.

http://www.gurufocus.com/news/334343/leon-cooperman-suggests-buying-aercap-holdings

Die Jungs von Profitlich haben sich auch in Q1 mit Aercap eingedeckt.

Eventuell “crowded”?

MMI. Great analysis. Another problem with the aercap recommendation is the fact that there are multiple signs of oversupply of aircraft in the market. American Airlines talked about it in their most recent call and many others have pointed to it. This certainly can not be positive for an aircraft leasing company that is effectively long these assets.

A cheap stock in this sector I came across is a Lithuanian company listed in Warsaw: http://www.aviaam.com/en/page/reports

Unfortunately it is not in my circle of competence as I don’t know what their assets are really worth and don’t know if the related party loans are at arm’s length.

$$

cash 37m (35m in USD)

PPE 37m

Loans granted to related parties 23m

Loans granted to third parties 12m

tangible equity 93m

finance lease liabilities 14m

mcap 74m

net profit 22m

dividend in 2014|2015: 3.5m|4m

Events after the balance sheet date

In March 2015 the Group entered into the Letter of Intent in respect to sale of one Boeing 737-‐‑000 airframe.

Maybe it is worth a look for you?

Was the TLB you mentioned really to finance leasing operations?

I’d imagine that a secured loan against the specific collateral could, in fact, earn 3% in the current environment.

I think Einhorn may be closer to the truth in regards to borrowing cost over the next 5 yrs, or so. But I don’t really disagree with anything else you’ve written!

I am not sure for wht they use the TLB, I just saw that on Bloomberg. Clearly, secured financing is cheaper but it also has less flexibility. With unsecured financing, you can much more easily sell aircraft etc.

For me it is also quite optimistic to assume current conditions for the future, especially regarding the significant amounts which have to be rolled each year and the new Aircraft to be purchased.

Einhorn’s new lease economics are based on income (ROA) and interest expense on his stylised capital structure of 75% debt / 25% equity. So, the assumed 3% interest actually corresponds to 4% cost of debt and 0% cost of equity. That cost of debt is in line, even above, what you say their current bonds are priced at.

The intangibles point and absence of long-terms barriers to entry are still interesting.

David,

thanks for the comment. However I do not know where Einhorn takes the 25% Equity. If you look at the ILFC acquistion, the newly raised quity only financed goodwill, the actual aircraft assets were 1:1 backed by debt plus some working capital.

mmi

Do you think you could share some of the lessons you learnt from those who emailed you, in detail? I am always trying to learn new things myself and would be grateful!

part of what I learned is in the post 😉

Thanks, really interesting stuff.

For me it was ultimately the capital intensity that made me to not looking further on this, but it’s always great to read well-reasoned text on why not to invest in a popular idea. Also goes to show how important it’s to do ones own due diligence.

I guess Einhorns idea shows how hard it is to come up with something enticing in this market.

The search continues.