The return of the “Watch series”: Richemont (ISIN CH0210483332) – Better than Swatch ?

Within my “Watch series” last year (Swatch part 1, Swatch part 2, Hengdeli, Fossil part 1, Fossil part 2, Movado) I left out one company which also is one of the major players in the Watch space: Richemont.

Some might ask: Why didn’t you already buy Swatch ? I argued that 300 CHF would be a good entry point and the stock is now at 292. Well, at the time of writing the Swatch post, I implicitly assumed that 2015 would be the low point. As we can see now, this is most likely not the case. Sentiment at Swatch is clearly more negative than for Richemont but still not rock bottom.

Additionally, I think one should not overestimate the moat of expensive Watch brands. One example is a (German) article 2 weeks ago in Handelsblatt about luxury watch brand Richard Mille. Founded in the early 2000’s they went from zero to almost 600 mn EUR in sales of super luxury watches with a new brand. So the market entry seems to be possible, at least at the very top.

![]()

Background/Business

Originally founded in South Africa by Anton Rupert, Richemont has a quite colorful history.The Group among other activities was into Tobacco, Pay TV and jewelery. Then, in the early 2000s, they focused on luxury and increased their exposure to watches.

The founder Anton Rupert died in 2006 but he seems to have been a quite interesting biography, starting his business with 10 GBP in 1941. His son Johann was CEO from 2010-2013, since then an “external” CEO has been appointed. The Rupert family also controls South African based Remgro, a listed company with ~7 bn EUR market cap.

Today their most well-known brands are Cartier, IWC, Van Cleef, Mont Blanc just to name the most important ones. Around 50% of sales are watches, the rest is jewelery and others (leather, clothes, pens).

One could argue that Richemont has been a good capital allocator, over the last 17 years for instance, Richemont has clearly outperformed its competition with an annual shareholder return (in EUR) of +13,9% p.a. compared to Swatch (11,3% p.a.), LVMH (10,6%), Kering (1,8%). only super-exclusive Hermes has done better with 16,9% p.a. over that time period.

Current valuation:

Market cap: 33 bn CHF (share price 57 CHF)

P/E (2015): 17,3

P/B: 1,95

EV/EBIT: 13,3 (Bloomberg)

What I like:

+ The luxury business itself is a very good business to be in

+ Strong brands, especially Cartier is clearly a “Mega brand”

+ less Watch focused than Swatch

+ little exposure to lower priced watches (less risk of “disruption” via Apple Watch & Co)

+ conservatively run (net cash, little Goodwill)

+ underlying results often better than stated results

+ luxury sector seems getting attractive as contrarian opportunity

+ good capital allocation track record

What I didn’t like:

-non core brands (Dunhill, Chloé etc.) add little value

-relatively “hard to understand” numbers, lots of “one offs”

-clearly negative momentum, especially in watches & other (Diamond prices)

-A/B share structure with voting right control of founding family

-EM > 50% of sales (indirectly more likely much higher)

-Very highly compensated management, alignment with shareholders ?

-management change required (Co-CEO retired at age 69, CEO age 65)

-analyst sentiment still relatively positive

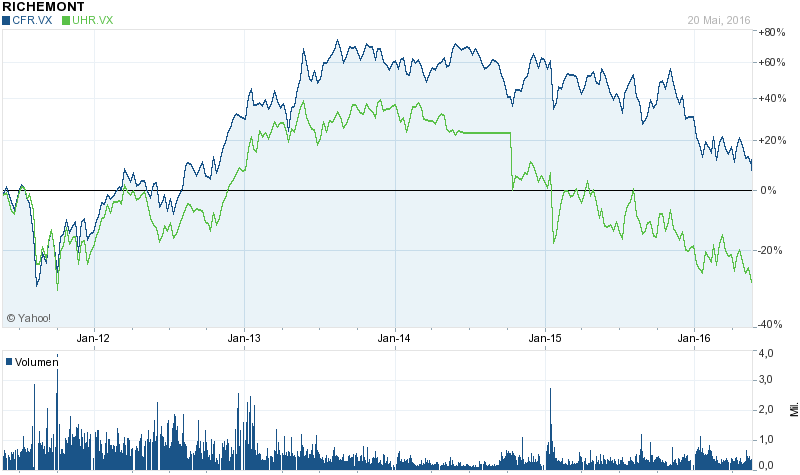

Stock chart

The stock price has held up better than Swatch over the last 5 years if we look at the comparison chart:

Early warning signs:

John Hempton pointed out the problems of Richemont (too) early in 2012. However I do think he indirectly made one mistake: You should never project your preferences (I hate expensive watches) on other people or even other people from other cultures. Jewelery for women for instance is a very old concept which has survived for thousands of years and will most likely survive a few more.

Also many succesful men want to show their wealth and expensive watches (or several of them) is a pretty good way to do so. Especially “new money” likes to show off and there is a lot of new money in Asia.

My personal experience tells me that especially value investors are mostly pretty “immune” against the lure of luxury brands as status symbols. However one should not confuse as I mentioned above personal preferences with the analysis of a company

Luckily I didn’t short Richemont back then but I tried my luck with Prada. Again too early.

Comparison to Swatch

Compared to Swatch, I do think that Richemont is both, better run and better strategically placed. With Harry Winston, Swatch seems to imitate Richemont, but I think it will take a very long time before they can even get into the vicinity of the Cartier brand which nowadays is even exhibited in museums around the world. Jewelry is good business but not a guarantee for sucess. Tiffany’s for instance just came out with pretty negative numbers:

Tiffany & Co’s quarterly sales fell 7.4 percent, the sixth straight quarter of decline, as a strong dollar discouraged tourists from buying its high-end jewelry and ate into revenue from markets outside the United States.

Sales at the jeweler’s stores open for more than a year fell 10 percent in the Americas region in the first quarter. Analysts on average had expected a 9.1 percent decline, according to research firm Consensus Metrix.

The Swatch brand itself is a lifestyle brand which I personally think has seen its best days long ago and a lot of the cheaper Swatch brands (Tissot, Rado; Hamilton) are not that strong in my opinion.

Within the watch sector, I guess that Richemont is missing a really “monster” brand like Omega. They do have very good brands but I think only IWC and Jaeger come close to the leaders Omega, Rolex and Patek Philipe. Interestingly, they bought their main brands from German conglomerate Mannesmann in 2000 for around 3 bn CHF. Back then, the acquisition multiples looked very expensive:

Over the three years to 31 December 1999, LMH’s sales have grown at a compound annual rate of 19 per cent to CHF 349.4 million. Operating profit before depreciation and amortisation (EBITDA) in 1999 amounted to CHF 80.4 million. Operating profit (EBIT) amounted to CHF 70.8 million.

Capital allocation

For companies like Richemont or Swatch with high margins and high free cash flows, capital allocation is important. The historic track record of the Rupert family is very good, they were active capital allocators with a very long-term perspective. Within Richemont, capital allocation looks smart as well.

For instance Net-a-porter, the fast growing online luxury retailer. According to this article, Richemont bought the company in 2010 for 392 mn EUR. Last year, the merged the company with Italian company YOOX and received a 50% stake in the combined listed entity which, at the time of writing is worth 1,6 bn EUR. So the quadrupled their money within 4 years which is not bad and turned an unlisted stake into a listed one. However a “behind the scenes” story I found indicates that they could have sold at an ever higher price.

At the moment they seem to be on the hunt for more Jewelery acquisitions , the timing looks relatively smart from the outside.

In 2008, Richemont made an interesting spin-off with the company Reinet Investments, which effectively was the Tobacco assets held by Richemont. At the time of the spin-off, the stock was worth 2,30 EUR, right now it trades around 17 EUR. For Richemont investors who kept the shares (for instance the Rupert family….) this clearly has been unlocking a lot of value.

One weakness in my opinion is that they carry a couple of brands which make no profit or losses. Accrding to the last annual report, acually 1.8 bn of sales (or 17% of total) contributed negatively for the second year in a row (adjusted for special charges).

I would subjectively judge that Richemont overall allocates capital significantly better than Swatch which is buying real estate in Zurich instead.

Management / founding family

The Rupert founding family owns all the unlisted B shares which gives them a 50% vote although they only own ~9% of the total capital. I do like to invest alongside families but all other things equal I prefer a “pari passu” structure.

Executive compensation looks very rich (fitting the name). The total compensation of the board (including non-executives) has been 50 mn CHF both in 2013/14 and 2014/2015. Swatch has similar levels of compensation (47 mn CHF in 2014, 42 mn CHF in 2015) but at least compensation went down with lower profits.

Johann Rupert pays himself “Only” ~1 mn CHF as Non-executive president of the board, this looks OK. Johann Rupert itself seems to be an interesting character. For instance here he gave a talk at FT conference. Also the Q&A of the 2015 results is quite interesting.

One of the issues is clearly that he turns 66 in June and no apparent heir from the family side is available at least for his role at Richemont. As a rule of thumb, for family businesses the jump from 2nd to 3rd generation always seems to be the hardest. I have no hard statistics on that but there is German saying which basically says: The fist generation creates, the second maintains and the third spends. Some family companies have solved this by bringing in external talent early and institutionalizing the ownership like Henkel, others have failed miserably.

Momentum (fundamental / stock analysts)

As I mentioned above, the underlying business, especially watches shows strong negative momentum. Clearly there are some special effects (terrorist attacks Paris) but for me it is not clear where the bottom is, both in sales and profit margins. When I looked at watch companies last year, everyone thought that this is the bottom, now however it seems to be 2016. But who knows ?

The question is clearly: What is priced into the stock ?

One indication for this is analyst consensus. Personally, I think it is very hard to gain any informational advantages on large and well researched stocks. The only but important advantage that I have vs. “the market” is that I can afford longer time horizons and that I can go against consensus for longer period of times.

Analyst consensus for Richemont is still surprisingly positive. From the 39 analysts that are covering Richemont, 18 still have buy recommendations. Overall consensus score is 3,65 (out of a max. 5) which puts it exactly into the middle of the Stoxx 600 index. So sell side analysts have not yet thrown in the towel. This could be an indication that the market still prices in too much optimism.

Valuation

Richemont clearly has experienced a boom from 2011 to 2015 which will be hard to repeat. One therefore should look at longer historic periods in time to estimate underlying margins.

If I look at the 17 year (1998-2014) average operating margin, this would be around 18%. Assuming (wild guess !!) 20% tax on a Group basis, this would mean 14,4% profit margin in the long run, across cycles (which, compared to many other industries is fantastic !!)

Based on current 11 bn EUR sales, this would mean ~1,6 bn EUR in average after tax profits. At a current market cap of 30 bn EUR (33 bn CHF) and and 5.8 bn cash and investments, Richemont trades at an implicit P/E of 15 over the cycle without growth.

Theoretically one could adjust further for the Yoox-Net-a-porter stake (1.5 bn EUR), then we would end up at around 14,2. Not bad but also not super attractive. For the inherent cyclicality I would require at least 10% return p.a. Within the next 2-3 years I don’t think profits will go up much, so this would be clearly a speculation on a multiple expansion.

For Swatch I thought a P/E of 16 would be fair, Richemont in comparison to Swatch clearly justifies a higher multiple. But even if we use 17 or 18, the stock doesn’t look like a bargain.

Summary:

I do think it is a good company and in direct comparison “better” than Swatch. On the other hand it is also more expensive and there are a couple of smaller issues like management change etc. which increase the risk.

Still I do think that there is a decent chance that one could buy the stock at some point in the future at a more attractive valuation, most likely when analysts as a whole more negative.

So for the time being I will do nothing. I don’t have a direct price where I would buy but I guess I would be more motivated (and take an even deeper look into) at prices around 50 CHF.

Better than expected results at Richemont:

Click to access company_announcement_06112020_w73nv7639xna67ysa8943b19_en.pdf

Especially China and Jewelery are doing well.

To hear Mr. Rupert on this last 9m results is really worth it and it gives real insight of how his personality is embedded within the organization.

Hi memy,

have you ever looked at Prada SpA. The stock went down from over 8 € to 2,7 €. The have a strong balance sheet, strong Brands (wide moat). Unfortunately the have a bad aquisition history. Nonetheless other hefge fund managers like David Herro (Oakmark International) are convinced that Prada is currently undervalued: “We think that while Prada may face some short-term obstacles, its long-term outlook is promising and it is trading at a meaningful discount to its intrinsic value.” Here another commentary from morningstar (08/26/2016): “We are lowering our fair value estimate for Prada to HKD 32 (3,69 €) from HKD 36 following a soft first-half report in which the firm missed our expectations on both sales growth and profitability. The results confirm our commentary after Prada’s Analyst Day that the company’s return to growth appears to be delayed until 2017. Nevertheless, we still rate Prada Group as a solid brand with a wide economic moat. Prada’s 100 years of history and design expertise is helping the firm maintain excess returns in invested capital despite losing some operational ground to competitors, and we believe Prada can retain its pricing power in the long run with some investment behind the brand.

First-half organic revenue fell 13%, driven by a 16% decline in retail sales. Europe, North America, and Asia all fell in the mid- to high-teens due to lower traffic in international traffic. Encouragingly, management said there had been signs of improvement in China early in the second half of the year, and we expect some improvement across the board in the second half. Nevertheless, global tourism is being impacted by geopolitical events, and this is likely to be a multiyear phenomenon, so we have tempered our near-term revenue assumptions. We now expect a 5% decline in sales this year, down from our previous forecast of flat sales, as we no longer believe favourable currency movements will offset the underlying decline. Despite the initiation of some rationalization measures, there was significant fixed cost deleveraging in the first half, with Prada’s EBIT margin slipping two percentage points to 14%.

These results confirm our belief that Prada lags its competitors on a number of metrics including e-commerce, CRM, and inventory management. Slower global travel does not explain Prada’s relative underperformance. However, with strong execution in these areas, and improved store productivity following a period of rapid expansion, we believe Prada can close the efficiency gaps to competitors.”

I would be glad to hear your opinion, although I already build up a small position at 2,65 €.

Best regards,

Boogie

Hi Boogie,

if you search the blog, you will see that I was actually short Prade 3-4 years ago but didn’t hold it through. At the current level, Prada is interesting but I have yet to look into it in more detail….

mmi

Hi,

I also did take a closer look at Richemont. Here are the things I noted while reading the annual report. My notes are in German, sorry for that, but couldn’t be bothered to translate. Hope it’s ok to post them anyway:

Richemont macht 55% Umsatz mit seinen Juweliermarken (Cartier, Can Cleef & Arpels, Giampiero Bodino), 29% mit reinen Uhrenmarken (Jaeger Le Coultre, IWC Schaffhausen, Lang und Söhne, Piaget, Panerai etc.) und 16% des Umsatzes mit Kleidung, Accessoires etc. (Mont Blanc, Chloe, Dunhill, Lancel etc.)

Johann Rupert ist Großaktionäre, Vorsitz im Aufsichtsrat und Gründer des Unternehmens. 2010 hat er bei Richemont wieder die Führung übernommen. Rupert hat die Stimmrechtsmehrheit von über 50% an dem Unternehmen. Er ist 66 Jahre alt.

4000 Mitarbeiter weltweit.

Die IT für Internethandel ist für alle Häuser (“Maisons”) gebündelt. Auch die Immobilienverwaltung geschieht zentral für die verschiedenen Häuser.

2016 sind die Umsätze währungsbereinigt ungefähr gleich zum Vorjahr geblieben. Der Bruttogewinn ist 4% gestiegen, trotz erhöhter Umsatzkosten aufgrund des starken schweizer Franken. Das Betriebsergebnis vor Steuern und Zinsen (EBIT) sank um 23%, was an gestiegenen Ausgaben für Verwaltung und Vertrieb liegt, sowie stärkeren Abschreibungen aus Käufen von Boutiquen im Vorjahr. Auch der starke Franken hatte hierauf einen Einfluss. Aufgrund stark negativer Währungseffekte im Vorjahr und eines Einmaleffekts aus einer Geschäftskonsolidierung ist der Gewinn unter dem Strich um 67% gestiegen.. Der operative Cashflow ist ungefähr auf Höhe des Vorjahrs.

Die Umsätze sind am höchsten in Europa und Asien, wobei Asien der mit Abstand größte Teil ist, wenn man Japan mitzählt (zusammen 45% der Umsätze). Im letzten Geschäftsjahr sind die Umsätze in Europa um 10%, i Japan 20% gestiegen, dagegen in Asien/China um 13% gesunken. Der starke Anstieg in Japan hat auch mit dem Tourismus und dem günstigen Währungsverhältnis zu tun. Die Schwäche in China wiederum mit der bekannten Nachfrageschwäche aus Hongkong und Macau. China Mainland hingegen hat einen Anstieg verzeichnet. Die Schwäche war insbesondere im Uhrensegment und im Großhandel zu spüren. Insgesamt ist der Großhandel eher schwach, das Endkundengeschäft dafür stark gewesen.

Das Schmucksegment lieferte den mit Abstand höchsten Beitrag zum operativen Ergebnis. Das Uhrengeschäft war demgegenüber eher schwach und der Restfuhr sogar ein leicht negatives Ergebnis ein, was hauptsächlich an der schlechten Performance von Dunhill und Lancel lag.

Richemont ist Gründungsmitglied in der RJC (Responsible Jewellery Council), welches die Nachhaltigkeit bis hin zu den Rohstoffen (Edelmetall, Edelsteine) zu gewährleisten versucht. Mitglieder sind große Bergbauunternehmen sowie Schmuckanbieter.

Die drei Geschäftsbereiche, Schmuck, Uhren und Rest sind jeweils einem eigenen CEO unterstellt und werden relativ autark geführt.

Richemont hält Anteile an der italienischen Yoox Net-A-Porter Group.

Rupert hält die Richemont B-Shares mit 9,1% des Eigenkapitals und 50% der Stimmrechte. Er kontrolliert also das Unternehmen.

Die A-Shares sind an der schweizer Börse und in Südafrika gelistet.

Bei der Mangement-Vergütung wird angestrebt im Mittel des Wertes einer Vergleichsgruppe aus über 50 Unternehmen verwandter Branchen zu liegen. Bei der variablen Vergütung wird eine überdurchschnittliche Vergütung bei überdurchschnittlichen Ergebnissen angestrebt.

Johann Rupert erhält für seine Arbeit jährlich 3 Mio, ohne variable Vergütung (letztere ist ohnehin schon durch die große Teilhabe gewährleistet). Der Wert ist dreimal so hoch wie im Vorjahr (da hatte er glaube ich ein sabbatical year).

Aktienoptionen erhalten nur die obersten Führungskräfte (executive Directors). Vorstand erhält 60% der Vergütung als Optionen. 30% für kurzfristige Ziele, 30% für langfristige. Das Maximum der variablen Vergütung liegt dabei bei dem doppelten Basisgehalt. Es werden quantitative sowie qualitative Ziele bewertet. Bei den quantitativen sind es Umsatz, operatives Ergebnis und (bereinigter) Free Cashflow gegenüber dem Budget und dem Vorjahreswert.

Bilanz: 2016 sind die Investitionen in andere Gesellschaften deutlich angestiegen. Cash ist leicht gesunken. Die Verschuldung ist gegenüber 2015 auch gesunken. Die Pensionsverbindlichkeiten sind fast so hoch wie die Verschuldung selbst.

GuV: Gestiegener Umsatz aber auch gestiegene Umsatzkosten. Vertriebskosten recht stark gestiegen (vermutlich wegen starkem Franken). Verwaltungskosten sind auch gestiegen. Das operative Ergebnis dementsprechend gesunken, also insbesondere aufgrund der gestiegenen Kosten. Durch ein vergleichsweise positives Finanzergebnis ist das Vorsteuerergebnis höher als im Vorjahr. Das Finanzergebnis war im Vorjahr durch starke Währungsverluste geprägt, insofern Einmaleffekt. Ohne wäre diesen wäre das Jahresergebnis aufgrund der gestiegenen Kosten niedriger gewesen.

Ein guter Gewinnanteil kommt aus nicht mehr weitergeführter Geschäftstätigkeit von Net-a-Porter. Dieser wurde an die Yoox über einen Aktientausch vergeben. Da das Geschäft nun in den Investitionen wiederfindet sollte es sich direkt (über Ausschüttungen, Dividenden) und indirekt (über Wertsteigerungen des Goodwill) auf das Ergebnis bzw. die Bilanz auswirken. Insofern kann man diesen (positiven) Einmaleffekt nicht wirklich als solchen Werten. Auch künftig sollte dieses Geschäft positive Auswirkungen auf die Ergebnisse von Richemont haben.

Comprehensive Income ist deutlich schlechter als im Vorjahr, aber immer noch deutlich positiv. Der Hauptgrund sind die nicht so positiven Währungsänderungen an Bilanzposten (-500 statt + 1900). Rechnet man sie raus, dann ist das Ergebnis 2016 besser als 2015, wobei man dann fairerweise 2015 auch die negativen Effekte im versteuerten Gewinn rausrechnen müsste (Hedges im Finanzergebnis).

Der operative Cashflow spiegelt das in etwa wider, was ein gutes Zeichen ist. Der Cashflow 2016 ist höher als in 2015, was überwiegend an geringeren Steuern, geringerem Anstieg des Inventars, etwas höheren Abschreibungen und geringeren Verlusten aus der Veräußerung von Wertpapieren lag, trotz des eigentlich niedrigeren operativen Ergebnisses.

Capex ist marginal höher als im Vorjahr, was zu einem deutlich positiven Free-Cashflow (wie im Vorjahr auch) führt. Tendenz seit 2014 aber fallend. Aufgrund höherer Rückzahlungen von Schulden und Dividenden, sowie erstandenen Minderheitsanteilen und anderer Geschäfte, ist der Cashbestand gegenüber dem Vorjahr etwas niedriger.

ca. 45% des Umsatzes werden mit Uhren gemacht, 35% mit Schmuck.Die restlichen 20% werden überwiegend mit Lederwaren, Kleidung und Schreibgeräten erwirtschaftet.

Fast 70% der Kapitalanlagen (jetzt hauptsächlich Anteile an Yoox) sind Goodwill! Yoox hatte 2016 gerade mal eine Profitmarge von 4%. Fraglich, ob das die hohe Bewertung des Goodwill rechtfertigt (hängt vom Wachstum ab und dem Profit nach Zusammenschluss mit Net-a-Porter).

Die Steuerquote war 2016 vor allem wegen geringerer “unrealised gross margin elimination” geringer als 2015 – was immer das auch heißen mag …

Die Abschreibungen auf das Inventar betrugen 2016 232 Millionen gegenüber 159 Millionen in 2015 – Tendenz also schon deutlich steigend.

Abschreibungen auf Verbindlichkeiten aus LuL waren 2016 geringfügig niedriger als 2015, offenbar also keine verschlechternde Zahlungsmoral der Kunden/Geschäfte.

Die ungedeckten Pensionsverbdinlichkeiten sind 2016 gegenüber 2015 merklich gestiegen. Grund ist hauptsächlich der gesunkene Wert der Geldanlagen. Der Diskontsatz ist mit 0,6 in der Schweiz und 3,5% in UK angesetzt.

Das operative Leasing ist mit 124 Millionen nicht gerade gering. Diese sollten, zusammen mit den Pensionsverbindlichkeiten, in die Verschuldung (und EV) mit einberechnet werden.

Die Vergütung des Key-Managements (Board und Senior Executives) beträgt insgesamt 38 Mio, gleicher Wert wie im Vorjahr.

In general, I like this company. I didn’t value it yet but I’ll collect the numbers of the last decade and perform a DCF on that data. The big unknown here is how the luxury watch industry is going to develop in the future, which is difficult to tell. I see luxury watches for men as the male counterpart to jewellery for women: As a way to show status, wealth and fashion. For men, a watch often is basically the only accessory which stands for this. In rich arabic countries, for instance, men even don’t display their status via clothing, since they all wear the same dresses. The watch is therefore the ultimate accessory for them to display their status, which may explain why this market is so strong for watch sellers.

Since smartwatches seem to be in decline already, I don’t think this will threaten the luxury watch business in particular. The big question is more that of a change of attitude: Will the rich young generation in the future still wear expensive watches to show their social status? I am not sure about it, but in the mid term, this may not be a deciding factor for Richemont and others.

I have less of a doubt about jewellery and that’s what I am really bullish about when it comes to Richemont. I’d expect women to continue to wear expensive jewellery, also younger women to a certain extent. New generations may change their attitude on this, though.

If you wish, I can update you with the analysis of the numbers, once I collected them, and the result of my valuation, too.

Hi thanks for the notes. And yes, please let me know about your valuation, too !!!

Cheers,

MMI

Hi,

sorry, being a bit late, but I have finished my valuation. I try to be conservative about a DCF, especially regarding the assumption for Terminal Value and perpetual growth.

Anyway, here’s what I have noted from the numbers (now in english). It looks like I can’t upload the Excel file containing the calcluation and all the multiples from the past 11 years. If you’re interested, I can send them or post them here if you tell me how. Here are my notes:

Revenue (9%) and operating Cashflow (7%) only grew modestly over the past decade. Profit also grew only around 7% a year, similar to operating Cashflow. Not a high growth company, at least in the past decade.

Depreciation and Capex grew stronger than Cashflow, with about 11% per year – not a good sign for quality of capital allocation. Expenses grew a bit stronger than income, but slightly below Revenue.

Market cap growth below growth of Revenue/Cashflow/Income (5.5%). Should indicate better valuation today (market cap as end of calendar year) than ten years ago.

Pensions and operating leasing grew stronger than Revenue (19/13%). Same for Inventory (11,4%), and current assets (12,3%) as well as current liabilities (10%). Non current assets, on the contrary, grew only 2% while current liabilities grew 8% per year.

Management compensation actually fell, with a peak in 2012/2013. Good sign that management gets incentives according to company results.

EBIT, EBITDA, Free Cashflow, as well as Free Cashflow to the firm, Free cashflow to Equity grew between 5-7% per year in the last decade.

Borrowings, including unfunded pensions and operating leasing grew with 13%.

Regarding growth, liabilities, expenses and Capex/Depreciation grew stronger than earnings, revenues and cashflow.

Costs of goods sold in relation to revenue stayed pretty constant at 36% over the last 10 years and can be considered pretty low (indicates good gross margin in general). Distribution expenses in relation to revenue grew slightly where as administrative costs shrunk slightly over the last decade.

Tax ratio increased over the last decade but seems too low to mantain at around 16% on average.

Margins look ok but have mainly shrunken where it matters. EBIT and EBITDA margin look very strong, with around 25-28 percent, RoCE and RoI look good with 15 and 11%. Cashflow margin looks also good at around 17%. So, in general, margins are a strong point at Richemont, though shrinking a bit.

Gearing is negative, so basically no debt. Interest coverage ratio looks very solid.

Management compensation is a bit high, with 3.5% on average, but ok for 2015 (1.7%).

Company is growing (CAPEX higher than Depreciation) but Capex as percentage of operating cashflow is higher than it was in the past (indicates bad capital allocation).

Goodwill is not an issue.

Working capital management looks mainly solid, with liquidity solid at all grades and cash conversion cycle pretty stable at 340 days on average (though seems a bit long in principle). In general, company pays its bills much faster than it gets paid (may be related to business model – retail etc.). Percentage of inventory on total Assets grew significantly (i.e. capital is bound stronger to the company).

Payout ratio for dividends is solid, but in relation to free Cashflow already high (60%). In general, it was higher in 2015 than it was on average in the last decade.

Valuations (all end of calender year in relation to numbers at end of fiscal year) have been lower at end of 2015 than they were on average over the past decade, with a PE of 18, PB of 2.7, EV/EBITDA of 12 and EV/EBIT of 14 not looking all to cheap. Also EV/FCFF looks not cheap with a number of 18.

EV/EBIT growth in the past 5 years and PEG (5 past years) also are a bit higher than 1. Therefore, slow growth doesn’t seem to be adequately reflected in valuations.

For the DCF-Valution, I assumed 2% riskless interest rate, an unlevered Beta of 0,8, which is according to Damodaran’s pages and which is the market default, since I couldn’t find an appropriate sector. I set the risk premium to 5% which gives me costs for Equity of 7.1%. Due to the low leverage, the WACC is close to this at 6.3%.

For the Terminal Value, I assumed perpetual growth of 2%, a tax rate of 25% and WACC of 8% (assuming a bit highter WACC in the future due to normalizing interest rates).

Regarding the coming 5 years, I assumed that EBIT will be lower in 2016, at 2000 instead of 2740 million, with a slow recovery to the 2015 value of around 2800 until year 2020. For the tax rate, I have chosen a higher value of 25% than the average of 15%, which I consider too low and not sustainable. I expect CAPEX to be slightly lower than 2015 and slowly approaching that level again. This in total leads to Free Cashflow to the Firm of 1090 (2015) up to 1560 (2020), which would be still lower than in 2015 (this value is changing a lot and 2015 actually was pretty high, same in 2013).

So, with all this, I end up with a fair market value of around 26 billion, still lower than the current 30+. This is certainly highly dependent on my assumptions, especially the Terminal Value which itself contributes about 2/3 to the valuation.

Overall, I would say that this is a decent company and business but taking into account the tendency of compressing margins, low growth and the issues with the watch business in general, not knowing where the smartwatch impact is leading to, the stock seems still to be overvalued a bit (according to my assumptions). Personally, I would wait for the stock price to reach levels in the low-mid 40ies. I do like the brands and especially the jewellery business, which I think are great.

Dan, thank you. In which reporting currency did you calculate your historic growth rates ? If it is in CHF, then I would adjust your numbers to USD. The CHF numbers are distorted due to the Swiss Franc movement.

All numbers in EUR, as stated in the official reports of Richemont (they report in Euro). Market cap is calculated as end of calender year stock price in CHF and calculated back into EUR with the corresponding end of calender year exchange rates CHF->EUR. Converting EUR->USD wouldn’t add value I guess. I typically keep USD and EUR reporting and convert reporting of all other currencies into EUR.

If you want to have a look into the numbers and change some of the inputs for the DCF, I can hand out the xls if you wish (not using macros, no worry).

I had time to look into your assumptions. I think most assumptions are oK. I am not sure about your normalized tax rate, as a Swiss based company ususally has pretty low tax rates. But I aggree, without assuming significant growth, the company doesn’t look cheap.

As I mentioned several times, I do not think Smart Watches are an issue.

Hello. I think there is a mistake on the market cap. Only A shares are listed and their market cap is about at your calculation but there are also the B shares which have same rigths as the As but for the dividend. The B share number exactly the same as the As so they should be taken into account so the whole company seems to me as very expensive at current prices

Nope.

There are 522 mn A shares out. At around 58 CHF this results ~ 30 bn market cap

There are another 522 mn B shares, which however have only 1/10 of nominal value than the A shares, so on an “apple to apple” basis you have 52,2 mn “equivalent” B shares.

Together we then have 574 mn shares which sum up to ~33 bn market cap, if one uses the same share price. One could discuss that the voting rights would justify a higher price but in other cases (Henkel etc.) liquidity seems to be the more important issue.

So to sum it up: the 33 bn market cap (and the ratios) are correct.

Some hard evidence that the watch industry is under a significant correction, especially in the high end:

Jaeger LeCoultre Master Perpetual Pink Gold in the company website, shipped to the UK: GBP23,200. Same watch second hand at reputable website Watchfinder, 1 year old, still under guarantee (but without the original box, granted): GBP13,950, almost a 40% discount. Links below:

http://www.jaeger-lecoultre.com/eu/en/watches/master/master-ultra-thin-perpetual/1302520.html

http://watchfinder.co.uk/Jaeger-LeCoultre/Master%20Ultra%20Thin%20Perpetual/1302520/27203/item/64320

So while great brands like Rolex and Patek may retain value, secondary brands will have a very hard time adjusting to the new times of less Nouveau Riche from emerging markets. And Richemont only has secondary brands – I tend to agree with the author that Cartier is not big among man and big on selling “cheaper” quartz watches to women.

Sales can only go down at Richmont in the short term. It is incredible that the sell side remains so positive. I hope to see the tide turning at some stage. As the author points out, this is an absolutely great company at a still terrible price.

I would not say that Richemont has secondary brands. A. Lange, Vacheron or Jaeger are actually top brands for “conneseurs”. They miss however a big brand with several billion of sales. Those big brands make more money because of the cost effect for advertisement.

Hi,

Great article, thank you.

3 points:

1. Richemont actually does have a mega watch brand: Cartier, with iconic models such as the Cartier Tank Watch and the Santos; unfortunately, CFR does not report any numbers on the Cartier watches, which are part of the âJewellery Maisonsâ segment; our estimate is that Cartier watchesâ sales amount to about 2.3bn USD, making it the third largest luxury watch brand in the world after Rolex and Omega.

2. Richemontâs jewellery business is growing fast (8% in FY 2016, will slow down a bit, but historic growth rates are > 10%)) and even if softer for a while, will gradually change the sales mix of the company; EBIT margins (not disclosed) of the jewellery business (Cartier jewellery excl the watches, van Cleef & Arpels, Piaget) is estimated at about 35-40%. So, over time you get margin uplift for the Company as a whole.

3. Forward integration: Richemont watch business is rapidly forward integrating, i.e. the company sells increasingly through its own stores and online platforms; this is accretive for both sales and margins in the watch business. So, another upwards drift here.

I think Richemont is worth a detailed look by you now. I would not be surprised if you said 60-70 per shere is value.

Best,

Peter

Peter,

thanks for the comment.

I agree that Cartier is a Mega brand, but at least for male watch buyers, Cartier is not a Mega watch brand.

I would also be carefull with growth projections. This is what they said for April:

“April sales declined by 18% and 15% on a reported and constant rates basis. All regions reported a decline in sales.

At constant exchange rates, only the Middle East & Africa posted growth. This performance was largely

anticipated. Asia Pacific remained weak due to no recovery in Hong Kong and Macau, only partially offset by

continued improvement in mainland China, which was up 26% on a constant rate basis. Retail sales continued to

outperform the wholesale channel. The challenging comparatives will persist through September. ”

But let’s wait and see….

mmi

Have you thought about a hedged entry, e.g. short Swatch long Richemont? I am wondering as you have done similar things in the past, but I admit that Swatch and Richemont are probably less correlated than Dräger and their Genussscheine.

hmm, I think at the current level, Swatch is not a short. Don’t get me wrong, I am not saying that Swatch is a bad company, I just think Richemont is the better one.

thanks for an interesting read! I like your valuation based on normalised profitability.

Although the sell-side is usually focused on the wrong metrics (and horizon), this report could be useful in your analysis: http://discussions.ft.com/longroom/tables/the-wall-of-worry/euro-luxury

I congratulate you on this good article on richement.Have you thought about Fossil. recently after the last earnings release the stock has come down a lot. Do you have any opinion on fossil/kors at current prices.

I would love to know if you have already researched Bolloré (familly owned french conglomerate). In last on year the stock has come down a lot due to commodities slowdown and other company related issues.

I haven’t looked at Kors. Kor is fashion and fashin is too difficult. Fossil: Also too difficult for me. They are in a very difficult position, squeezed from all sides. I personally would prefer Movado if I had to buy in this segment.

Bollore: On my “to do” list, but quite a difficult subject.

Thanks for your remarks. I have difficult time understanding the demand for campanies like fossil. Their watch should not be considered luxury . Then why suddenly sales are deteriorating even though watch for medium priced watches should not be too cyclical on the first impression. May be I am missing something.

Fossil is not luxury but fashion. The problems for Fossil come from many sides: Fitness trackers, new market entrants and the weakness of the license system (higher license fees if somethin is succesfull). Add to this the problems of the traditional sales channels (Department stores) and you get the picture.