Some thoughts on index funds & market efficiency (including some empirical material)

Currently there are a lot of articles in the financial press about the perceived “fight” between active and passive asset management styles.

The passive guys make the point that on average, after fees, active funds have to underperform against the index and low-cost index funds, which is difficult to counter. On top of that, “alpha” created by large active funds is not very persistent.

From the active side, there is the argument that if there is too much money invested in index funds, market efficiency will suffer and stocks will go up and down together because not enough people are analyzing single stocks. If stocks go up and down together without reflecting fundamentals, at some point in time “good stocks” should be too cheap and bad stocks to expensive. Which then should be some easy money for any good stock picker.

Is the market already inefficient ?

This argument reasonable at first but is there any evidence that the market is less efficient ? Let’s look for instance at the DAX 30, the major German index. It is hard to come up with good numbers but I do think that maybe between 10-15 % of the DAX is somehow invested via index funds with a clear trend towards more index ownership.

So let’s look how the DAX constituents have performed so far this year (as of Nov. 2nd). The Dax itself ytd is down -2,8% This is the YTD performance of the constituents:

| Perf. YTD | |

|---|---|

| ADIDAS AG | 63,44% |

| RWE AG | 19,47% |

| INFINEON TECHNOLOGIES AG | 16,14% |

| SIEMENS AG-REG | 13,32% |

| HEIDELBERGCEMENT AG | 12,09% |

| HENKEL AG & CO KGAA VORZUG | 11,72% |

| THYSSENKRUPP AG | 11,12% |

| BASF SE | 10,75% |

| VONOVIA SE | 10,74% |

| LINDE AG | 10,31% |

| DEUTSCHE POST AG-REG | 7,92% |

| SAP SE | 6,34% |

| MERCK KGAA | 3,86% |

| FRESENIUS SE & CO KGAA | 0,86% |

| DEUTSCHE BOERSE AG-TENDER | — |

| FRESENIUS MEDICAL CARE AG & | -4,70% |

| MUENCHENER RUECKVER AG-REG | -6,10% |

| BEIERSDORF AG | -6,26% |

| VOLKSWAGEN AG-PREF | -9,38% |

| DEUTSCHE TELEKOM AG-REG | -12,19% |

| ALLIANZ SE-REG | -15,01% |

| PROSIEBENSAT.1 MEDIA SE | -17,15% |

| E.ON SE | -17,95% |

| DAIMLER AG-REGISTERED SHARES | -18,97% |

| BAYERISCHE MOTOREN WERKE AG | -22,01% |

| BAYER AG-REG | -22,09% |

| DEUTSCHE LUFTHANSA-REG | -23,17% |

| CONTINENTAL AG | -23,98% |

| COMMERZBANK AG | -37,48% |

| DEUTSCHE BANK AG-REGISTERED | -45,08% |

So we can clearly see that the actual performance of the constituents is VERY different and interestingly almost no stock moves like the index.

However those numbers alone are not a proof. Theoretically, there could have been a much higher dispersion of returns in the past. So what one can do is to calculate the historic dispersion of the returns of the constituents vs. the return of the index. As a measure for dispersion, the standard deviations seems to be the appropriate measurement.

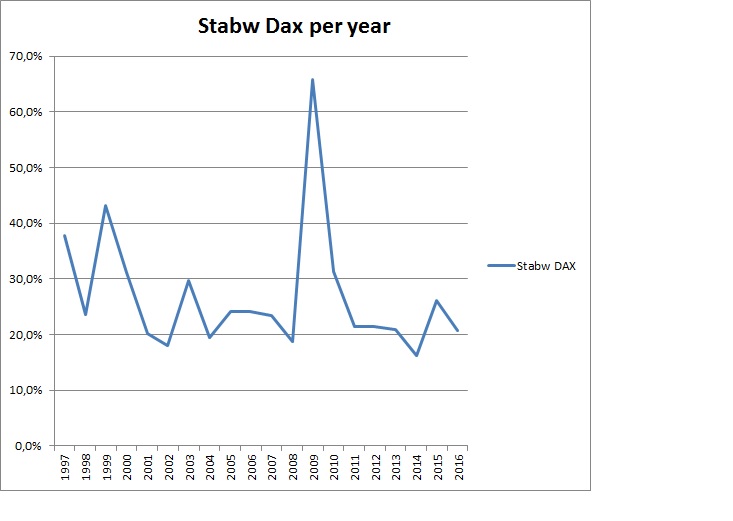

The following chart shows the dispersion of the Dax constituents for the last 20 years on an annual basis (annual performance, over 20 years):

Just by looking at the chart, at least for the last 10-15 years, I don’t see that there is a clear trend for less dispersion. However one big caveat here: The underlying data is a cheap “cut and paste” job. I did not have the correct constituents for every year, rather the older the data the less reliable. I also weighted the constituents equally and not according to their index weight.

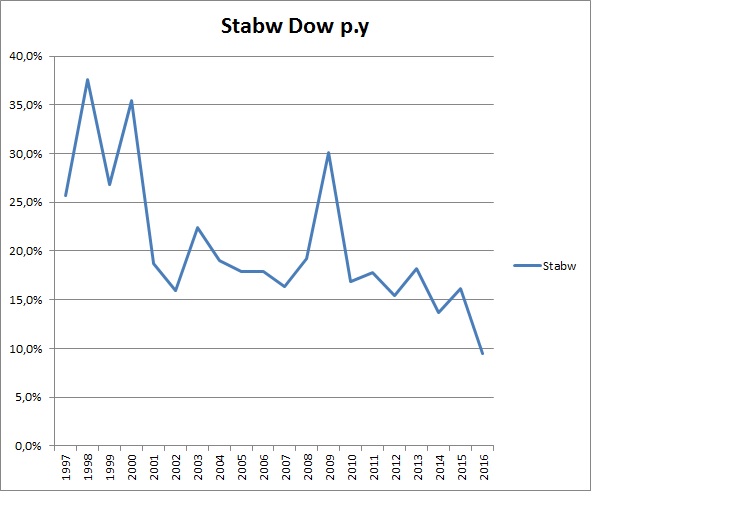

Just for fun I did the same (crappy cut & paste) analysis for the Dow and there it looks more interesting:

h

Here it there seems to be a certain trend, especially the current year looks weirdly “narrow”. So for the US we might see some preliminary evidence that returns have become narrower around the index return in the last years, although this can quickly change if we run into a crisis scenario.

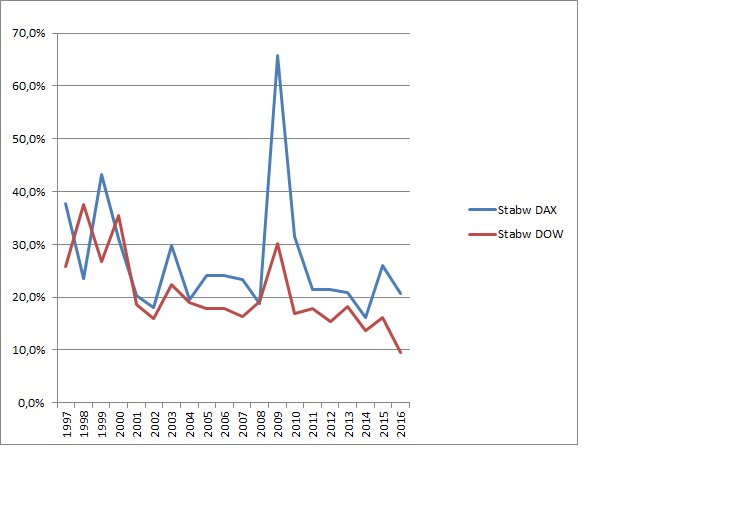

Finally, if we compare the DAX and the DOW, we can see that in the past 20 years, the 30 Dow constituents did trade in narrower bands around the index than the 30 DAX constituents:

Overall it looks that at least with regard to this measure, the US market seems to be more efficient than the German one which in my opinion should not come as a big surprise. Especially in times of crisis, US stocks seem to be more stable than German ones.

So what does that tell us ?

I think especially for the US market there seems to be a certain effect in play which reduces the dispersion of returns of the large stocks around the index return. One reason could be that more and more money goes into index funds, however it is always hard to really prove this. It could also be that for some reason the fundamental development of the index constituents is more connected than it was in the past.

If index funds would explain all this, then in my opinion, stock picking could become interesting again in the future.

For the German DAX so far the effect doesn’t seem to be observable. As my data is not very good, this could be a problem of my data or index ownership in Germany is behind the US.

Nevertheless I do think that keeping an eye on return dispersion within indices is something very useful in order to find out if structural opportunities might arise at some point in time.

I think there is much more to write about active vs. passive but that will fill a couple of posts in the future.

So wie ich dich verstehe, sehen wir ein erwähnenswertes Anwachsen von Anlagegeldern in kostengünstigen, passiven ETFs, die stumpf Indizes wie den DAX oder den Eurostoxx 50 nachbilden, also alle Aktien in einem Index anteilig kaufen. Voraussichtlich geht ein überproportional großer Anteil dieser Gelder in große und bekannte Indizes oder aber in Indizes für aktuelle Hype-Themen wie Biotecs oder web 4.0 / IoT….

Für mich stellt sich allerdings die Frage, ob das dazu führt, dass jetzt anteilig mehr Geld stumpf diesen Indizes folgt oder ob wir nur eine Kapitalverlagerung weg von teureren, pseudoaktiven Fonds sehen, die auch schon bisher zu 80 – 90% ihre Vergleichsindizes nachbildeten.

Eigentlich sollte sich das empirisch recht gut ermitteln lassen, indem man Aktien betrachtet, die in stark durch ETFs geprägten Indezes auf- oder abgestiegen sind. Da einige Anleger schon etwas früher darauf aufmerksam werden, würde mich ein Vergleich interessieren, bei dem die Aktienkurse jeweils ein komplettes Jahr vor wie auch nach der Indexaufnahme betrachtet werden im Vergleich zu anderen Aktien (Einerseits ähnlichen Aktien, die nicht in den jeweiligen Index sprangen und andererseits mit Aktien, die bereits im Index sind.)

Dabei würde mich zweierlei interessieren:

a: Lohnt es sich im Mittel, in Aufstiegkandidaten zu investieren? Bringt dieses gemittelt eine solide Outperformance, oder ist der Bereich schon “too crowded”? So ganz neu ist diese Idee ja nicht gerade…

b: Hat sich der Kurseffekt durch einen Indexaufstieg in den letzten Jahren verändert? Sofern der Anteil der passiven “ich kaufe den kompletten Index”-Investoren gestiegen ist, sollte das den Aufstiegswerten ja einen stärkeren Schub als früher geben. Falls dieser Effekt nicht zu sehen ist, erleben wir vielleicht nur ein “Umlabeln” von pseudoaktiven Fonds zu wahrhaft passiven Fonds, wobei nur etwas weniger Gebühren in der Finanzwirtschaft hängen bleiben.

Kennen du, MMI, oder einige der Mitleser belastbare Analysen zu diesem Thema?

zu a) Das ist schon ein alter Hut, die Strategie gibts schon lange

b) hat mit a) zu tun

In der Praxis gibt es m.E. mittlerweile Geschäftsmodelle die nur das Ziel haben sich in den Index zu fusionieren wie z.B. Vonovia.

mmi

As you say this is a huge topic, perhaps I should write more about it on my own blog too, but I prefer right now to concentrate my efforts to build a better portfolio of stocks to be invested in. I will throw in a few cents here..

One have to take a step back and ask what is active investing (let’s call it alpha from now on)? If you go 16 years back and you applied a strategy of sorting out the stocks which ranked well on Value metrics out of broad benchmarks. Then you invested according to that. That might have made you a very successful investor for a number of years, greatly beating the benchmark. Why? Because Value outperformed massively after the IT-collapse. Was that alpha? Back then, yes! And many big fund managers made their careers on being loaded on the Value factor. Is it regarded alpha today? One would say yes, you beat the standard benchmark therefor it is alpha. Another more sophisticated investors says no. They would argue you just loaded up on a smart beta factor which we call Value. A third person would say it depends, did you constantly tilt in the same way to Value, or did you rotate into Value at the peak of year 2000, if the later, you have alpha in terms of market timing the factor.

If you on the other hand had a Value approach and you outperformed a comparable Value benchmark, then you also added alpha on-top of your Value tilt, by choosing the right Value stocks. So a pointer to mmi would be to change his benchmark to something more Value oriented (you seem to go to some length to actually find an appropriate benchmark by mixing several indices).

One can do the same analogy with for example Sectors instead of the Value factor. Healthcare stocks have for example outperformed now for a long time, is it alpha or not choosing to be over-allocate to Healthcare stocks. Again, it perhaps depends, if it is a constant tilt, it’s hardly alpha..

So back to my original question, what is alpha? The answer is, it depends how you view the world of investing. Given that we now can buy smart beta strategies almost as cheaply as MCAP weighted index funds, they have commoditized something that most people used to call alpha and transformed it into beta. That leaves a smaller pool of alpha, but a alpha that is more pure.

So if we use a very stricts definition of alpha, neutralizing country, sector and factor tilts, you can pick down almost any investor and explain they have zero alpha. What was seen as alpha was actually just a country tilt, or sector tilt, or an investment style (Value, Quality, Momentum, High Dividend, Net-Nets, etc) which happened to work during the evaluated time period.

Now that we have taken this step back to understand what we are talking about. Your question is: is there any point to try and pick stocks, can we generate meaningful alpha as individual investors, or should we just give up and invest according to either standard MCAP weighted indices, or even smart beta indices?

Well I would argue, without scientific proof, for about 95-99% of all individual investors out there, they won’t be able to generate meaningful alpha over time. And more-or-less the same goes for professional investors.

I have met many fund managers, and had as my job to find those that generated alpha, without giving away all secrets in the business I conclude that there are managers that after adjusting for the above mentioned factors, do generate consistent outperformance, year after year. It was very encouraging for me to see that it actually can be done. For long-only managers we are here talking about 3% yearly alpha before fees, for the very best out there. That’s how much you can expect if you really belong to the elite.

As private individuals we do have a few aces up our sleeve, which makes it easier for us to generate alpha compared to a professional fund manager. The main ace to play being that we can invest in small companies with too low liquidity for any professional investor to touch. I believe this effect if used correctly, can compensate for that we are not as professional as the very best full time fund managers, so perhaps we can also strive to achieve 3% yearly alpha? I believe it can be done, for a few of us, that work hard enough and have enough knowledge.

“I have nothing to add” 😉

Hehe 🙂

Although somewhat disappointing to not get any push-back or feed-back from all the clever people commenting on your blog, when I for once tried to write a serious comment.

As always mmi thanks for the efforts on your great blog.

The great Jesse Livermore (of the Philosophical Economics blog) put up four awesome posts covering the active vs. passive debate in May. Would highly recommend reading them in order…

http://www.philosophicaleconomics.com/2016/05/passive/

http://www.philosophicaleconomics.com/2016/05/followup/

http://www.philosophicaleconomics.com/2016/05/indexville/

http://www.philosophicaleconomics.com/2016/05/passiveactive/

My own $0.02…

1) Best strategy for 99% of equity investors is go passive and stay passive (particularly during severe market drawdowns).

2) History suggests significant % of “passive” investors in fact “actively” rotate out of equity during drawdowns (creates mkt timing opps).

3) These “passive” investors expand the ranks of the active and lower average skill at the precise time skill matters most.

4) As always on active side: small, long-term oriented, absolute return focused “owner” investors are advantaged over the alternatives.

5) Add’l thought: 99.999% passive investors disaster for capitalism / economic efficiency as mgmt’s would run roughshod over shareholders.

mmi,

Thank you for your thoughts on passive investing.

1. Do no academic studies exist which used more detailed data?

2. Would not a large active investing company pay for research showing the disadvantages of index funds? Does the lack of such research prove anything?

3. Can a threshold be calculated in advance, when passive investing will be inefficient, e.g. 50% of market capitalization? Due to the difficulty of forecasting the financial results of companies, will the threshold be much higher, e.g. 80%?

4. With some large funds resembling indices and private investors preferring large, well known companies, was passive investing not around for a long time? Adding this capital to the index funds, how large is the actual passive invested capital?

5. Does it matter that different index funds use different indices – like FTSE, MSCI etc – for the same market?

6. Is the principal agent problem amplified by index funds? Will this counterbalance the advantage of passive investing?

7. Are capital weighted indices some sort of trend following system, because successful companies make up the greater part of the index?

8. What alternatives to passive investing has a person who does not possess the necessary knowledge, talent or inclination to invest actively in securities? Active security funds, real estate, agriculture, timberland, resources, collector items and gold appear to be even more difficult than index funds.

Regards

malt

wow, many good questions. Please find some answers here

1. I do not know. I didn’t find any at least for the DAX

2. Good question. However for large active companies I am afraid the situation is not good anyway

3. I have no idea….a good question for a PHD thesis maybe ?

4. Good questions, a lot of “active” is actually quite passive. I have no numbers on this.

5. Could be but in my opinion not the big driver (the big ones are in every index)

6. Not more than currently with “active” funds in my opinion

7. Yes, they are to a large extent

8. For rpivate investors, cheap index funds is still the best option. One could allocate a small portion to “real active” funds like the TGV Partner.

Good writing. Thank you for that idea.

Do you think, that the eroding interest levels have influence on the observed changes in standard deviation?

I honestly don’t know. I think overall marekt volatility was the strongest driver in the past….