Amaysim (AU000000AYS5) – The “Freenet of Australia” ?

Business & Business model:

Amaysim is a 320 mn AUD market cap Australian company which went public in July 2015 and offers mobile subscription plans without owning the physical network in Australia. So they are effectively a reseller (like Freenet in Germany). As a specialty, they do not package the plans with “free” phones and long lock in periods, but offer “clean” and customer friendly contracts which can be canceled on a monthly basis.

Essentially, this is a distribution / billing service. Their value proposition both, for the networks and end clients is that they can offer this service better and cheaper than the networks. If they can do this, then it is “win win” for both sides.

They have a contract with the “Optus” network which is owned by Singapore Telecom and is the second largest in Australia (after Telstra but before Vodafone). Other than Freenet in Germany, they are bound exclusively to Optus. This is from the IPO prospectus:

ExclusivityIt is a condition of the NSA that amaysim and its “related corporations” do not acquire, sell, distribute, provide or otherwise supply a Competing Service (meaning similar or substitutable services to those provided by Optus to amaysim under the NSA)

History:

The history of Amaysim is quite interesting, as is was founded by Germans which most likely explains that Amaysim is popular with some German Value investors:

The origins of amaysim’s business model date back to 2005, when Thomas Enge, Rolf Hansen, Christian Magel and Andreas Perreiter (simyo Founders) launched the MVNO “simyo”, which pioneered the low-cost annual, online-led business model in Germany.

and:

In early 2010, the simyo Founders, together with Peter O’Connell (together, the amaysim Founders or Founders), identified an opportunity to introduce the subscription-based, online-led business model into the Australian market, which they believed was experiencing relatively high levels of customer dissatisfaction as a result of, for example, the complexity of mobile plan offer structuresand high prices, subsidised handset-led models with lock-in contracts, and primarily offshore-based customer care models.

Interestingly, the founders hold some remaining shares but only 2 of them are still members of the supervisory board.

More recent developments

Since the IPO, a couple of things happened:

- The Vaya acquisition

In January 2016, amaysim acquired Vaya, a low-cost mobile virtual network operator with approximately 140,000 subscribers at the time of the acquisition. The amaysim Group now has a dual brand strategy, with mobile plans and price-points to address broader segments of the Australian market. amaysim is the customer experience champion while Vaya is the price-fighter.

Buying a low price brand is clearly part of the “Freenet script” in Germany and can make sense, although in theory they could have created this on their own.

2. Broadband acquistion

In mid 2016, amaysim announced that they want to sell and offer broadband services. For this they acquired a small company which was already active in this field. Again, this is similar to what Freenet does in Germany. “Bundling” these services in theory should lower subscriber “churn” and lead to better profitability.

The interesting aspect of this is that it seems that broadband seems to undergo a big change in Australia. If I understand everything correctly, the government is building out a new network and then leaves it to resellers like Amaysim to sell plans to the ultimate customers. This clearly opens up business opportunities.

3. Take over of Click Energy

Just a few weeks ago then the announced their largest M&A transaction yet: they acquired Click Energy, They paid 120 mn AUD for an energy retailer. Again, this is something that Freenet offers in Germany as well with some success as I understand.

4. There will be a 4th mobile network in Australia

Just 2 weeks ago, Australian competitor TPG announced that they will build a 4th mobile network in Australia. TPG seems to have been a Vodafone reseller so far and thinks it might be a good idea to start a 4th network. From most other markets one knows that 3 networks are ok, but usually pricing gets much more competitive with a 4th one. So it is not a surprise that the stock prices of Telstra, TPG and Amaysim dropped when this was announced.

It’s not clear why they did this because Australia had 4 carriers, However Vodafone and Hutchinson merged in 2009 and are still struggling to break even.

From the supplier side, this is clearly not positive as lower prices mean lower profits for everyone. Lower general prices is one of the major risks Amaysim mentioned in their IPO prospectus as they are dependent on Optus:

Further, while the NSA contains a price review mechanism that expressly aims to ensure that wholesale prices continue to reflect a competitive offering in the Australian BYO Mobile Services market, this process may become drawn out. The outcome itself may not fully address the impact of the changed market conditions; be inadequate to deal with numerous or continual market changes; or result in an increase in amaysim’s wholesale costs.Any of these circumstances may adversely affect amaysim’s ability to maintain its gross margins, reduce amaysim’s Subscriber net additions and retention of existing Subscribers, and adversely affect its financial performance or position.

There is also an argument for increased opportunities for resellers but I think amaysim is somehow limited due to the exclusivity. This is clearly one of the major differences to Freenet: Freenet clearly has more opportunities to play the networks against each other.

It should be noted that the reseller market in general seems to become more crowded in Australia. There is no shortage of resellers, especially for the Optus network. Also competitors like Vocus/Dodo seem to be already a step ahead with regard to “new verticals”.

Business summary:

From the business side, amaysim looks interesting. They run a capital light subscriber model which has been proven to work well in other countries. The combination of mobile, broadband and energy is also clearly something that seems to work elsewhere. However there also seems to be real pressure on the core mobile business.

What I don’t like at amaysim

Before getting to excited, I always try to “kill” the investment by looking explicitly at hings that I don’t like and I Have to admit there are a couple of issues, here are the major ones:

1. Founders are mostly out and management doesn’t own stock

From the initial founders, only two are the supervisory board and none has a really active role anymore. They still own some stock but sold most of it during or after the IPO. The current CEO which came in 2013 and sold his stocks in the IPO. As of now he only owns options that he received as bonus.

2. Management compensation relies on “so so” metrics

The key metrics for bonuses are “underlying” Earnings per share and Net promoter score. Both metrics in my opinion are not optimal, as EPS can easily be “juiced up” by acquiring businesses with a lot of debt. Some return on invested capital metrics would be much better in my opinion.

The long-term bonus depends solely on the “underlying EPS growth rate”.

Personally, I think one should be carefull here: The combination of a CEO with “options only” and EPS targets could in theory lead to a debt fuelled acquisition strategy. the higher the volatility the more valuable are the options.

This sentence that I found in the presentation for Quick Energy made my very cautious:

materially accretive with FY18F EPS accretion of 20%+ post-cost synergies (excluding transaction and integration costs)5

I hate it when acquisitions are justified by saying they are “accretive” if at the same time you leverage up the company significantly. It remains to be seen if they actually reduce the leverage going forward or if they continue to leverage up.

On the plus side, they do actually adjust down the EPS number for one offs.

3. Reporting is not very transparent

This is for instance what they write with regard to the Vaya transaction:

(v) Revenue and profit contributionAs the Vaya group has been integrated with amasyim and operates as one business and as one operating segment, it is impracticable to reliably determine the Vaya group revenues and profit contributed to the consolidated amaysim Group for the period since acquisition or to estimate the Vaya group revenue and profit as if it had been acquired at the beginning of the annual reporting period.

In German I would say that this is a “bodenlose Frechheit”, especially as they also do not adjust subscriber growth numbers which should really be pretty easy. In the half-year report issued a few weeks ago, the show y-oy subscriber growth of +34% which, excluding the Vaya transaction would only have been 15% or so. Still Ok, but not as good as shown.

Another thing I found strange is that one doesn’t find the Net Promoter score anymore in more recent reports. Although this is part of the management compensation targets.

There was a post at the “find the moat” blog which also focuses on the fact that Amaysim’s numbers are not “fullyy self explaining”.

4. The “Own software EBITDA game”

EBITDA is their major KPI in presentation to investors. However I detected something which is a relatively little known but often used trick:

You capitalize intangibles (instead of expensing them) and then write them off afterwords. Theoretically this should not make a big difference but due to the way EBITDA is calculated, this “pumps up” EBITDA.

In 2016 (page 64) of the annual report we can see that they started with around 3,5 mn book value of “Software developement” and added 4 mn new capitalized Software but amortized 2/3 of the existing ones, ending the year with 5 mn EUR. Although this looks like a wash, this has a positive impact on EBITDA. For clarification look at this example of 2 companies, which have the exact same profits etc. with one difference:

Company A expenses software, company B capitalizes software but writes it off completely in the next year. This is how this looks in numbers:

In the first year, clearly also the profit of company B is higher but in all the following years, profit, EBIT etc is exactly the same but EBITDA is higher. This is clearly not “illegal” but I think that one should adjust the EBITDA numbers in these cases.

What I also don’t understand why this doesn’t show up as negative line item in the Operating Cashflow /Net Income reconciliation on page 70 of the annual report. Amortization is added back but nothing is deducted for the (non-cash) capitalization.

Clearly this is not a big issue and the impact is low, but I would prefer a more conservative way of accounting.

5. Capital Management

One final point: Capital management is not great in my opinion so far. Why ? Paying a relatively large (unfranked) dividend and then issuing new shares to acquire a company within a few weeks is clearly not great capital allocation. I guess they were in negotiations already by the time they decided to pay around 10 mn in dividends. Of course many companies do just the same but clearly it is not “great”.

Quick valuation:

Amaysim has a market cap of ~320 mn AUD at the moment. They guide to 55 mn EBITDA for the full year, which I would adjust for the capitalisation of software.

With ~80 mn AUD net debt and 40 mn AUD new shares. this translates into 8,4x EV/EBITDA for 2018 (with a full year of click energy). Not expensive but not so cheap either.

Stock price:

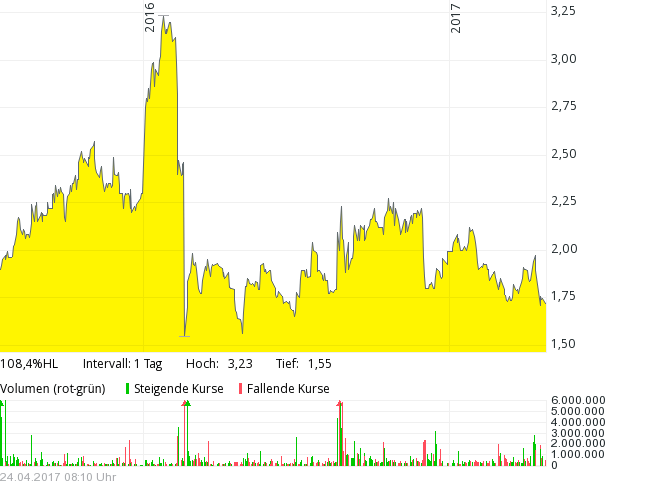

We can see that amaysim trades now below the IPO price of 1,80 AUD from around 2 years ago:

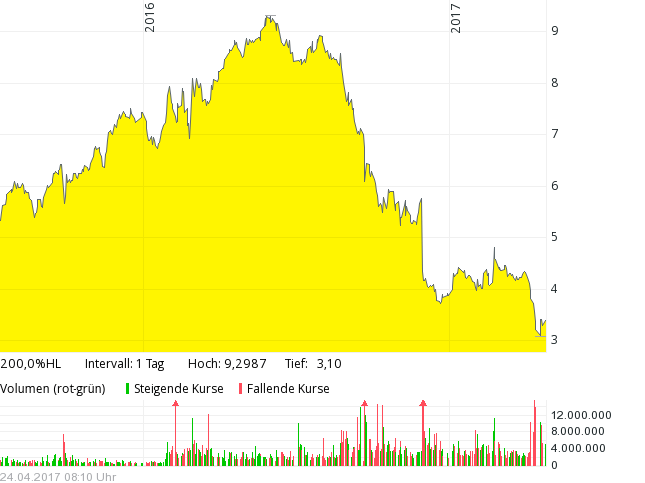

The latest drop was most likely a reaction on the news that TPG is building a 4th network. Other TelCos in Australia have done worse, like Vocus:

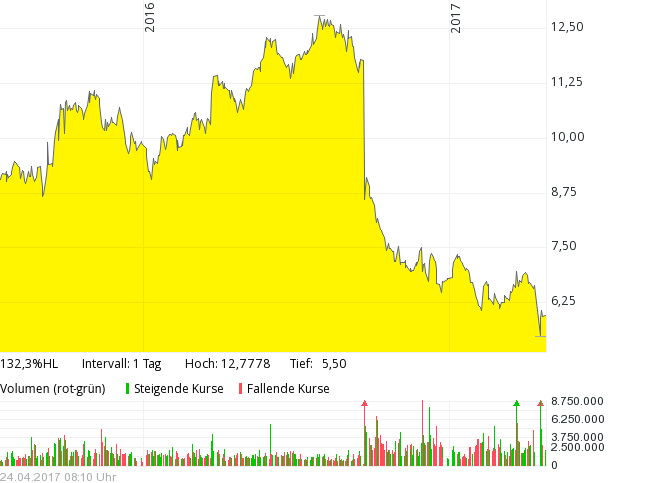

or TPG:

Summary:

I am a little bit torn here. I like the business model, the strategy and what they achieved so far. On the other side I see some issues like the reporting, the KPIs for the management and the lack of ownership among the executives.

They clearly have good growth options, but there is also a lot of pressure in the core business.

I think amaysim is clearly a case where I as an armchair investor have a disadvantage at this stage. There is very little written history to analyze and the success clearly depends on how well this is being executed, which, from my “armchair” I cannot judge very well at the moment. On top of that, I do not have much experience with the TelCo industry and Australia.Australian stock

For the time being, I will therefore stay away and watch this one closely.

What could change my opinion ? I think the following (at least 2 of them) items could change my mind:

- they reduce leverage (or adjust KPIs for management) significantly (or maybe even reduce the dividend)

- they improve their reporting and introduce a segment view especially after the acquisition of click energy (and clearly explain what amount of the earnings increase comes from acquisitions)

- the pressure on the core business is not as big as I assume

- management is actually buying shares with own money in a significant amount

- the share price becomes even cheaper

- I manage to look at more TelCo companies (in Australia)

- They do not increase the amount of capitalized Software significantly

Amaysim got hammered today.The trading update looks oK from the top line but EBITDA, even on an adjusted basis looks weak:

https://investor.amaysim.com.au/irm/PDF/1485_0/amaysim39sfirsthalf2018tradingupdate

What I don’t like is that they now even try to adjust the adjusted EBITDA;

Statutory EBITDA of approximately $10 – $11 million (vs. $17.3 million)

• Underlying EBITDA of approximately $17 – $18 million (vs. $17.3 million) after adding back costs

incurred in connection with the integration of Click, investment in new mobile products and the

launch of a new vertical, amaysim devices

• An additional $6 million receivable relating to the first half will be reported as a subsequent event in

the 2018 half year accounts. If this subsequent receivable were included, adjusted statutory EBITDA

would be approximately $16 – $17 million and underlying EBITDA would be approximately $23 – $24

million

This is without doubt your biggest strength.

You don’t make big mistakes.

Kudos!

“subsequent receivable”?? I will add this to the Red Flags from below. It become quite clear that the company does not suffer from too few Red Flags.

That’s actually quite creative.

Hi,

I very much enjoyed reading your post and was particularly interested in the parallels you draw with Freenet, a company that you seem to have studied quite in detail although I do not see it covered in your blog (maybe it is somewhere but I missed it). I myself consider Freenet as a business appealing to “value” investors and I am quite enthousiastic about the rather bold move they made last year on Sunrise. I would be very interested to learn your view on this company.

Unfortunately, I do not have a qualified opinion (yet) on Freenet.

Interesting company; nevertheless would not a mere two year operationg history as a public company make somebody who considers herself a value investor wary? Please have a peek e.g. at Bulletproof (ASX: BPF) which had phantastic metrics in (business years) 2015 and 2016; what has happened since?

well, I don’t know that much about bulletproof, but the business model of amaysim has worked elsewhere (Germany) and the founders had a pretty decent track record.

But clearly, a longer track record would make it easier to invest. That’s one of the reasons why I didn’t…..

“Other TelCos in Australia have done worse” ==> die hatten sich aber vorher auch verfünffacht in 3-4 Jahren

Streng genommen hat sich amaysim in den Jahren zuvor “verhundertmillionenfacht”, da sie 2010 bei null komma null angefangen haben. Der Exit war im Nachhinein natürlich Glück. Deshalb macht es m.E. schon Sinn die Perfomance seit IPO zu vergleichen und da schauen sie relativ gesehen gut aus.

Natürlich macht es Sinn.

Aber es erweckt den Anschein, dass die Telekoms in Australien vollkommen gefallen sind. Vorher waren das x-bagger in 3-4 Jahren.

Es ist halt die Frage wann ist es eine Übertreibung nach unten.

guter Punkt.

What are you looking for in the NI/CFFO reconciliation? The capitalization games take place in CF from Investing. There you find it. Also, the structure of their 2016 acquisition gives them leeway to prop up profits in future periods.

That company looks more interesting from a short perspective (if it weren`t so small and valuation would be higher)…

I would disaggree that amaysim is a short candidate. I think they have a good track record from an entrepreneurial side. If they execute well then in my opinion there is more upside than downside.

Very competitive no-growth industry with commodity-type products, no entry barriers, no switching costs, now venturing into another commodity industry via acquisition, heavy use of adjustments, flawed incentive structure, management partly sold-out, agressive (acquisition) accounting, deteriorating balance sheet, opaque reporting…enough for me….but time will tell…

well, as I said in the post: If they can offer better customer service at a lower cost, then this business model could translate well into similar sector. if they can’t, then there will be problems. Therefore it would be interesting to knwo how good their service really is.

“Hindsight Capital” was probably right on this one. If it looks like a duck, quacks like a duck,…

Thanks for sharing your direct experience. Why is the energy acquisition a bad move ?

Again, Click are just a reseller of energy. I also think it was not a cheap acquisition, I think it works out to about $750 per customer that they bought. There are also a lot of competitors in this space too, though I have not yet bothered to shop around for cheaper electricity, so I can’t comment on how easy or difficult it is to switch.

My two cents. I used to be an amaysim customer and recently moved all my family onto AldiMobile. The main reason was that the amaysim network was not reliable, in some cases it was taking hours to receive SMS messages. Aldi are also a reseller, buy they use the Telstra network which is the best and their plans were also cheaper. So my personal experience with Aldi dissuades me from investing in them! I think the energy acquisition is also a bad move.

and how quick and easy is it to switch between suppliers ?

It’s actually very easy. You simply sign up to your new provider online, put in your existing mobile number and tell them who your existing provider is. They then arrange for the number to be transferred. Takes a couple of hours usually. Took a little bit longer in my case because it was over a public holiday.

Another company, TPG Telecom will be directly entering the mobile space. Currently they are a vodaphone reseller, in future they will have their own mobile infrastructure, so it will make it more competitive. TPG Is quite well known and has very competitive home Phone and broadband deals.

yes; i have mentioned this in the post. This might make life more difficult for all of the existing players. Although it might take time until they reach the same availability levels as the other players.