HP Enterprise (HPE) – Spinning-off its way to happiness ?

DISCLAIMER: THIS IS NOT INVESTMENT ADVICE. PLEASE DO YOUR OWN RESEARCH !!!!!

Management summary:

- HPE, the enterprise arm of the old HP looks attractive on a sum-of-part valuation

- following 3 spin-offs in 2 years, my model indicates an upside of ~40% in the base case and ~70% in an optimistic case

- Some “soft catalysts” are on the horizon such as the upcoming Software “spin -off merger”, further share buy backs and a “normal” financial year

- management acts shareholder friendly, has a clear strategy and has created significant shareholder value since 2011

- major risk is clearly a further detoriation of the Enterprise solution business which had a bad start into fiscal 2017

Background

I guess Hewlett-Packard doesn’t need a lot of introduction here. Founded in 1939 it was one of the predominant technology companies for many years but then somehow lost its mojo. Funnily enough a German CEO marked the end of a long buying spree by acquiring the more or less worthless UK Software company Autonomy in 2011 for 11 bn USD.

In 2011, Meg Whitman, the former CEO of Ebay took over and since then tried to consolidate the company.

Spin-offs seem to have become one of her favourite tools and HP actually already did 2 off them in the past and the third one will come up soon. Lets look at them in more detail:

- Spin-off HPE / HPQ

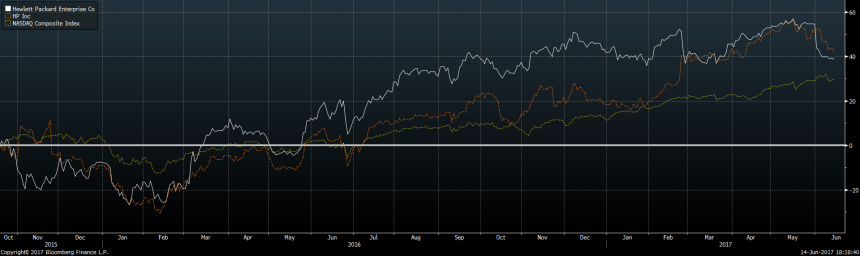

In late 2015, HP spun off the Enterprise business (HPE) form the consumer business (HPQ). Clearly, the enterprise business was seen as the more sexy one which is why Meg Whitman went with HPE.

Interestingly, both companies performed better than Nasdaq since then. HPQ actually slightly outperfomed HPE especially since the beginning of 2017 as we can see in the chart (HPE white, HPQ yellow, Nasdaq red):

2. Spin-off Merger CSC/DXC 2017

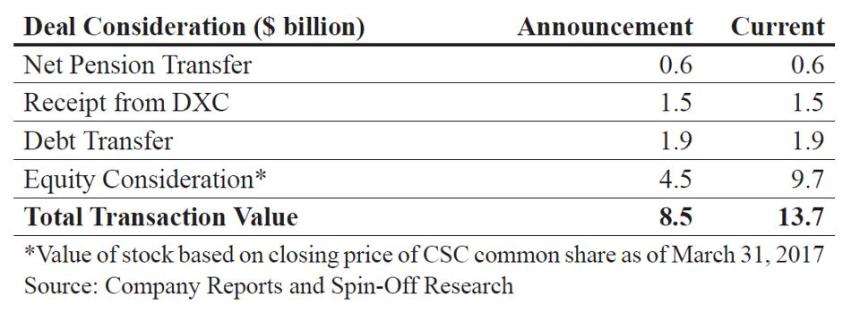

Just a few weeks ago, HPE spun off their “Enterprises Services” business and merged it with listed company CSC which then was renamed DXC. HPE shareholders received around 8,6 Shares of DXC for every 100 HPE shares they were holding.

The transaction was done as a “Reverse Morris Trust” which seems to be a very shareholder friendly structure as it is tax-free in the US if all conditions are met.

Interestingly, the DXC shares did relatively well after the spin-off merger , HPE shareholders didn’t dump the shares as one could have expected. It is also interesting to see that the value of the spin-off merger for HPE increased significantly between announcement and execution from this table:

So clearly this transaction made everyone happy, both CSC shareholders and HPE shareholders.

3. The upcoming Spin-off merger software business & Micro Focus

The third spin-off is again structured as a Reverse Morris Trust and will happen at some point in the next few months. This time, the “non core” software business (incl. the infamous Autonomy) will be spun off and merged with UK company Micro Focus. At announcement, the deal was worth 8,8 bn USD, which consists of 2,5 bn USD in cash and 50,1% of the new combine company as “spin-off” dividend for HPE share holders. As the Micro Focus stock price increased further, at the time of writing, the stock component would be worth almost 7 bn USD at current prices.

A few words on Micro Focus

Micro Focus itself is an interesting company, specializing in buying troubled software companies with “Mission critical” software products and “milking” them by slashing costs etc. This passage from the last annual report sums up their philosophy quite well:

Each year the world of IT gets another year older (and we should remember that IT is still a relatively young industry). Whilst the vast majority of companies will chose to focus on the “new and exciting”; we believe that there will be an increasing opportunity to help clients derive value from their existing and often highly complex IT investments.

The company seems to be very shareholder return oriented which shows in their fantastic results since they went public in 2005:

The Company was listed on the London Stock Exchange on 12 May 2005 at a price of 130 pence and in the year ended 30 April 2006 Diluted Adjusted EPS was 14.23 cents and total dividends for the year of 6 cents per share were declared. In the year ended 30 April 2016 Diluted Adjusted EPS is 146.70 cents and the proposed full

year dividend is 66.68 cents representing a compound annual growth rate of 26.3% and 27.2% respectively.

I guess that one would call a serious compounder. For them, the HPE deal is a huge one and clearly a risk. However if the manage to bring this business close to their own profitability, the upside would still be very significant. All in all I think that this could be a similar accretive deal as the CSC/DXC deal for HPE share holders.

Other divestitures

On top of those listed spin-offs, HPE has sold/merged 51% of its Chinese business into a 49% stake of a company called H§C (deal value ~2,3 bn USD). Another 0,8 bn were realized by selling their stake in Indian IT services company Mphasis to Blackstone last year.

Management and will HPE “shrink to greatness ?”

Personally I do like the “slimming down” and think a more focused strategy promoted by CEO Meg Whitman is a good one:

“The bigger you are the harder it is to be fast, because you’ve got so many people involved in every decision. Our view was – given the backdrop of the technology industry – [being] smaller [and] more focused was going to be important,” she says.

HP got into trouble because the previous CEOs followed the mantra of bigger is better. So I think it might be a good idea to focus on the core of the company. It needs to be seen if Dells strategy to take on 57 bn USD of debt to go private and then combine with EMC is better. As a CEO of a public company and especially right now, the easier strategy would actually be to do many big acquisition funded by cheap debt. HPE does the complete opposite which I find quite compelling. In my definition of “Outsider company” which means doing things differently than anyone else, this comes quite close to being an “outsider old school tech company”.

So far Meg Whitman (herself a billionaire after running Ebay from 1998 to 2008) in my opinion did a very good job to create value for shareholders. Spinning off companies to shareholders allows the shareholders o decide if they want to keep that part or sell it and the previous “spin-off merger” definitely created value for all parties involved.

But not everything is about shrinking. HPE did some acquisitions as well which so far seem to have been OK or even good. More recent ones were:

- Nimble Storage (800~900 mn USD)

- Simplivity (650 mn USD)

- SGI

- Aruba (2,8 bn)

Especially the Aruba acquisition seems to have been quite smart according to several articles I read.

Overall I would give her and HPE very good grades for capital allocation. On top of the spin-offs, they have been buying back stock at reasonable levels and the acquisitions so far look strategic and reasonable.

The remaining business: Enterprise solutions / data centre infrastructure

I don’t claim to be a big expert on their “enterprise” business. From what I understand, they provide servers, storage and network hardware plus services (incl. financing) for big data centers either for companies or other large institutions.

The biggest short-term danger for this model danger is clearly the cloud. Companies like Amazon seem to use “No name” hardware because its cheaper but 85% of the business is still traditional business and I am not sure that everyone wants to migrate to Amazon or Microsoft. HPE claims that big companies will eventually implement a “hybrid cloud” solution which means a private cloud with own machines within a company and usage of a public cloud for less sensitive issues. In general, moving everything into one central cloud is also legally not as easy as it looks.

Some people who are way smarter than I am, like this guy from Andresen Horowitz actually think that cloud computing as we know it doesn’t have a bright future. The same guy also sees a very bleak future for data centers in general:

The point is not about startups challenging Intel (though that may happen). It’s about startups leveraging different hardware (ARM processors, flash storage, and networking) to build systems that are largely software enabled — thus bypassing legacy models, where the value was in fat margins on hardware and in on-premise installations.

Those guys are clearly talking their book but its clear that the data center business might undergo significant change in the (near) future.

HPE’s biggest competitor is clearly Dell which recently acquired EMC and targets the same markets plus maybe IBM. However, with such big changes on the horizon, I am not sure if it is a good idea to be leveraged up to your neck like Dell.

Very recently HPE seems to have lost a lot of business from their biggest customers, most likely Microsoft. So there are clear headwinds even in the current model. On the other hand, more focus on the core business might help.

There is a pretty detailed post on VIC about HPE from last year which in general is still relevant (although sales have clearly done worse than expected.

The financial services business

The financial services business (financing the equipment for clients) seems to do good at the moment with still increasing sales and profit, however financing value seems to have been stable.

For valuation purposes, the debt of the FS segment should not be added to EV as there are corresponding financial assets. According to the Q2 presentation, FS net debt is around 10,3 bn USD, leaving HPE with a net cash balance of 4,4 bn USD at the end of Q2.

Bringing it all together: Valuation

After all the mentioned spin-offs and disposals, HPE will have a healthy cash balance plus HPE shareholders will own either directly or indirectly a lot of “extra assets”.

So therefore a “sum of parts” valuation makes a lot of sense. I have created a table with 3 scenarios (base case, bad case, good case) which of course contains a lot of critical assumptions:

A few explanations:

- the “bad” case is clearly not a worst case. It assumes discounts to some assets (MF shares, H3C) and lower multiples

- the “Good” case includes a full 4,4 bn share repurchase at current prices

- all cases assume stable profits for the remaining “core” profits based on the first 6M of FY 2017.

- all cases show that the Enterprise business is implicitly valued at very low single digit P/Es (between 4-6 times earnings”. Whatever multiple we assume here drives the investment case

Clearly one can challenge any single assumption here but overall I think the cases could be realistic. Based on my assumption, the results are clearly interesting: a +43% upside in the base case, more or less fair value in the downside scenario and a healthy +68% upside in a good scenario.

For me this looks attractive. Maybe not a “grand slam home run” but importantly: Good enough and could return 20% p.a. over the next 2 years in the base case.

“Soft catalysts”

Just being attractive based on a sum-of-part basis alone often is not so compelling. However in HPE’s case I think there are a couple of catalysts which could affect a significant revaluation at some not so far point in the future:

- The spin-off merger with Micro Focus

- Further share buy backs

- “normalized” earnings in FY 2018

So all in all one could expect that the discount to the “sum of parts” valuation could be closed within the next 1-2 years which would be my time horizon for this “special situation”.

Major risks

Tha biggest risk is clearly that the core business continues to deteriorate fast. I am inclined to believe management that this will not be the case but there is clearly a risk. If the business really deteriorates more than management indicated, I think one clearly needs to “eat any loss” and sell because then the downside is hard to quantify.

Plus, Meg Whitman will not run HPE forever. She is no 61 years old and had ambitions in the past to get into politics. My expectation is that she will stay at least until HPE can show the numbers for a “normal” year which would mean FY 2018. If she leaves then there clearly would be the risk that someone else thinks that going on a buying spree might be a good idea.

There is also the risk that for some reason, HPE shareholders would dump MF shares after the spin-off. Plus, as always, HPE could make a big (and dumb) acquisition and destroy value like they did in the past. This would also be a reason to sell the stock if that happens.

Summary:

Overall, I do like the case. There is a clear upside in my opinion combined with some “soft catalysts” that makes the stock attractive for my “special situation” bucket. I also like to retain some USD exposure as my Actelion position got closed out last week.

Pros/Cons summary

+ Sum of parts attractive

+ “soft” catalyst MF spin merger

+ good management / capital allocation

+ contrarian/outsider aspect

– remaining business under pressure (shrinking sales)

– high volatility of stock

– little visibility in current numbers (spin- offs etc.)

I will therefore initiate a 3,3% position at current prices at around 16,50 USD / per share for the “special situation” bucket.

P.S.: A big “Thank you” for the friend and reader who mentioned HPE to me as a potential idea !!!

Wow, 40% lower today…

https://www.ft.com/content/77c9291e-2b44-11e8-a34a-7e7563b0b0f4

:-s !

For the record: Overall result of the HPE “trade”: 5,6% in EUR.

Sold 1/2 of my remaining HPE position at around 11,90 EUR /14,15 USD per share.

😦 !

In adverse conditions better earlier than later…

Sold the rest at around 11,80 EUR / 14 USD.

Meg Whitman is stepping down as CEO:

http://fortune.com/2017/11/21/hpe-meg-whitman-ceo/

This somehow weakens my investment case.

10% drop today! she is capable but certainly not worth that much

But your model needs rebuilding from scratch to take into consideration the massive Capex on R+D that the new guy is planning….

I don`t know about “massive” R&D spend. On the call they repeated the 2bn USD FCF target. I am also not sure if Meg Whitman is such a big loss at the current state of the company.

The fun part with all the spin offs, deals and strategic initiatives is over. Now its down to good old and maybe boring execution. Perhaps someone else at the helm is better at that?

Well, the biggest risk in my opinion is that they start doing large acquisitions again. Under MEg Whitman, I would have been confident that HPE has at least some discipline. With new managment this is more risky. The cash pile is clearly alluring for any tech company CEO.

I second that point – the worry is about capital allocation. Yahoo is still fresh on everybody’s mind.

Just read your post on GE: I remember reading somewhere 15 years ago that fund returns are 96% from asset allocation and 4% from market timing (BCG study at the time I believe). I view corporate share buybacks as the same: they should not be judged on their timing (i.e. share price drop after a buyback) but on the use of cash – was GE better off distributing cash to shareholders via a special dividend instead? doing a more ambitious acquisition? investing in emerging ideas? or piling cash in high ROE business segment (Aerospace and medical imaging)?

Judging management on their poor timing skills is less relevant in my opinion.

Thanks for the comment. However my intention was not to say that GE was stupid. That’s easy to say aftrrwards. The point I wanted to make is that huge share buybacks as such are not always positive. And if GE now needs to sell assets in order to survive, it is not only bad timing but bad capital allocation.

Personally, i do think that “keeping some powder dry” is much better than debt financed share buy backs at high prices.

No need to say that HPE looks to me more like an IBM than a spin-off case now. I got you yesterday.

Will stay clear of GE until it gets much cheaper. I will not speculate on a Berkshire takeover at all (sorry Seeking Alpha)

*errata: I got out yesterday

One of my good friends at GE said he sold all he had long long ago, as he had big question marks with management strategy…

I don’t understand this (from the quarterly report):

“Non-GAAP diluted EPS [for 2018] is expected to be $1.15 to $1.25. GAAP diluted EPS is expected to be approximately $0.43 to $0.53.”

I am also not sure whether I like the large sum that is going into share repurchases (2.6 billion USD) compared to dividends (0.4 billion USD). Given that they have a share count of approx. 1.6 billion, paying a dividend of 1 to 1.5 USD/share would boost the share price much more than buying back shares on the market, as dividends are the new interest. On the other hand, the book value of HPE shares was 17.87 USD in July, so maybe it is more cost efficient to buy back shares.

It is not the quarterly you are looking at. It is the Analyst meeting from yesterday. The gap between GAAP and non-GAAP relates to restructuring (Next program).

Buybacks are more tax efficient than dividends. If they ask me, I would like them to cancel the dividend completely and buy back shares for 6.5 bn USD (that is the current net cash position at holding level after the MCRO spin). The book value is more or less irrelevant when it comes to buybacks. If you like dividends (and enjoy paying taxes) then you can simply sell some shares.

Yes, buybacks are more tax efficient that dividends.

But there are other, IMHO bigger problems with share buybacks.

They are used much more procyclical than dividends, and they are better usable to manipulate the share price, helping the management to hit the share prices required to free higher bonus levels.

Over a whole market cycle buybacks are quite often destroying a lot of shareholder value, pulling it especially at high share prices, (high price-book-value), preferencially debt financed. In bad time the money often has to be brought back by capital increases in the worst of all times.

Dividends instead are much more difficult to be misused by a procyclical management for self-enrichment. So in my experience dividends are less tax efficient, but still the much better deal for the shareholders over a whole.market cycle.

I really wonder why so many value investors are in praise of share buybacks.

PS:Please excuse my little rant.

I don’t agree that the book value is irrelevant with regard to buybacks. When a company buys back shares below book value and cancels them, the book value of the remaining shares will increase. When a company buys back shares above book value and cancels them, the book value of the remaining shares will decrease and thus, value is destroyed.

I am aware that buybacks are more tax-efficient than dividends, but in my opinion, buying back 5% of the shares will have less impact on the price than announcing a 5% dividend in the current low-interest environment (even though this is not logical). Maybe I am wrong.

Fughettabout book value, start thinking about intrinsic value! Berkshire buys back shares above bookvalue. According to your thinking WEB destroys value each time he does this. Really?

to be honest: i don’t think that dividend or sharebuy back contribute significantly over the longer term. Topdanmark is a very good example that it doesn’t seem to matter that much if you buy back or pay dividend.

Book value is relatively easy to calculate, Intrinsic value is ery hard to evaluate.

Hence intrinsic value is good word to fog alues, a nice PR-Bubble.

I believe Buffet as he has proven his value again and again, but with nearly everyone else I prefer a comparison toward book value in the way cktest did. I the share price is lower than book value I like share buybacks, otherwise I prefer dividends.

I can’t help it, that’s just the conservative and sceptical value guy inside me.

By the way, quite often I saw jumps of the share price following buyback announcements. Bigger than following dividend announcements. Share buybacks are fashionable in these days of expensive shares.

MMI, Thanks for the posting on HPE.

What drove your decision to buy HPE before the spinoff instead of buying it after the spinoff? Based on your valuation, it seems cheap even before the spinoff. My thought on this kind of situation would be to buy it post-spinoff because: 1. you don’t have to hold Microfocus and worry about selling it after; it’s hard to know what price it would be trading at. 2. sometimes right after the spinoff, there’s a sell-off that gives you the opportunity to buy HPE at a lower price before it rebounds.

I am just wondering what’s your thought on this – buying before vs. post spinoff.

Thanks,

Sold my Micro Focus shares today. Main reason: My retail broker needed 3 weeks to actually book them in a way that I could trade. Lucky me as the shares increased nicely in between.

Luck helps those that work after it

If the short history of HPE spinoffs is any guide, it would have made sense to keep the Micro Focus shares a little longer…

HPE should spin off the Software business (MCRO shares) tomorrow (Sept.1). As I understand it, we get NYSE-listed ADS. Let`s see where both shares will trade, but I am keen to “recycle” MCRO proceeds back into HPE.

Yes, it will be interesting to see what happens today.

Que pasa?

Spin off ?

Looks like David Einhorn has jumped onto the HPE train as well:

https://www.gurufocus.com/news/554132/david-einhorn-starts-hewlett-packard-enterprise-position-in-2nd-quarter

Too risky for my taste MMI. Obviously you could catch up with a nice rebound that diminishes the gap between expected value and price but there are tectonic shifts in this sector that are long term in nature and I do not think that those movements are favorable to HP.

Thank you as usual for sharing, and good luck!

By the way, coming to a more industrial part of the business, Nordex in Germany is getting hit hard. Obviously is a turnaround situation, that falls well behind the best in class (Vestas) but in this case the long term nature of demand and business is favorable in my opinion. An interesting case to follow in my view (I dont expect operating growth till 2019 though).

Take care.

Dave,

thanks for the comment. Interestinlgy I still wait for a single positive comment on HPE. I haven’t ever looked at Nordex though.

mmi

My problem with Nordex (and in general with all wind turbine producers) is: you may be right that the long term nature of demand and business is favorable, but it is purely politically driven. And politics is in my opinion unpredictable.

As for the product: who really wants a power source where you don’t know in advance when it is actually producing power? For solar power you know at least that the sun does not shine at night and that most days the sun will shine.

Well, I guess everything is in the end more or less subtly politically driven BUT the important thing is, in my opinion, that economics for wind are sounded and this technology is really competitive (the grid parity is getting closer –depending on what is the prevailing marginal technology: the higher the cost of the marginal, the easier it is for wind to match it without subsidies-). PV, at the current stage of technology, is a different story and with a lower efficiency factor, the technology is clearly less competitive (cost MWh wise).

Actually, you are wrong, utilities know in advance how much wind will blow on a yearly basis in a specific area with a high degree of probability (thorough wind studies are developed before the location of the windfarm is decided).

Currently the technology allows for rotor/turbine increase in size which is good for modest economy of scale.

But in order not to hijack the conversation of mmi in relation to HP, I suggest we leave it here.

Superspannend. Bin besonders fasziniert von Microfocus. Das erscheint mir ein großartiges Geschäftsmodell zu sein. Werde einen Einstieg dort prüfen und dabei bewerten, ob ein indirekter Erwerb über HPE die bessere Variante ist.

Bzgl. Datacenter-Business der ‘alten’ Player a la HPE bin ich aber recht skeptisch und würde hier durchaus ein erhebliches Risiko sehen. Da wandert einerseits viel Geschäft in die Cloud ab, andererseits schrumpfen die Margen immer weiter und aktuell gibt es wohl noch ein spezielles Problem mit dem extrem gestiegenen Preis für Speicher.

jupp, das sind alles die bekannten Problem. Die frage ist: wieviel davon ist im Preis reflektiert ?

die haben alles an Share- oder Stakeholder gegeben und 0 investiert.

Das wird ein Problem. Schwindende Margen und Cloud Services werden sicher durch exponentielle Bedarfsteigerung Rechenleistung kompensiert. Da sind wir noch sehr am Anfang. Nur ohne Innovation wird das nix und die kann man sich nicht dazukaufen, jedenfalls nicht kontrollierbar, höchstens glücklich …

You’re right on the major risks…couple quick notes:

– I think your assumption of “core profits based on the first 6M of FY 2017” is optimistic at best. HPE is heavily bleeding server sales to low-cost Asian ODMs and even Dell/EMC has been taking share recently. They will most likely completely exit the “Tier 1” (sales to cloud providers like MSFT) server business in the next year which will continue to hit their top line.

– With their core EG business deteriorating they WILL do more acquisitions. Meg commented at the recent Discover conference that “I think you will see acquisitions become a bigger part of our strategy.” No doubt they’re going to have to acquire growth, so the question will turn into who they decide to acquire at what price. We’ll see what the market thinks…

– Starboard Value started a stake recently which could be a catalyst if they get heavily involved.

Think this is one the market has right for now…unless their core business stabilizes this will continue to be a value trap IMO. Definitely some upside if someone outside gets involved.

Thanks for the insightfull comment.

2 things:

According to management in the last call, profits are to some extent seasonal and the later quarters are ususally better than the first so I am not sure if my estimate for the current FY is so optimistic.

Interestingly almost everyone thinks that their business can only deteriorate. Of course everyone could be right, but it also explains why the stock is cheap. For valuation purposes, they wouldn’t even need to grow, they would just need to stabilize.

But we will see how much downside is already priced in.