Trisura (TSU) – Interesting spin-off opportunity or intransparent minority mess ?

A friendly reader had mentioned Trisura as a potential Spin-off opportunity in the comments and the stockspinoffinvesting blog mentioned it a few days ago and linked to a Seeking Alpha write-up.

At first sight, Trisura indeed looks interesting:

- it’s a small cap specialty insurer currently mainly active in Canada

- it hasn’t been “discovered” by sell side analysts yet

- only mini spin-off dividend for Brookfield holders (1 Trisura stock for 170 Brookfield stock(~0,3%)

- the company has been growing very quickly over the last few years

This is from the listing prospectus:

In 2006, Brookfield Asset Management capitalized Trisura Guarantee, holding ownership through its private equity group. Trisura Guarantee is a niche property and casualty (‘‘P&C’’) insurance company with a primary focus on the Canadian surety, professional and executive liability and warranty markets. Trisura Guarantee has been a successful investment, with a strong partnership between its management team and Brookfield Asset Management. Trisura International, founded by Brookfield Asset Management in 2001, has provided specialty insurance and reinsurance products to the global insurance and reinsurance markets since its

inception in 2001. Trisura International ceased writing new business at the end of 2008. Trisura US is expected to utilize a fee-based business model focused on specialty non-admitted insurance premiums in the U.S. Together, these businesses write specialty insurance policies that are not otherwise easily secured by companies, making them interesting businesses with potential for growth. Collectively, these businesses comprise Brookfield Asset Management’s specialty insurance entities, a small component of Brookfield Asset Management’s overall asset management franchise.

Business model

As outlined above, Trisura is currently active in 3 main “specialty insurance” lines:

Surety

Surety bonds are used to guarantee contractors’ completion of contractual obligations and the payment to suppliers and sub-contractors, and in a wide variety of other circumstances to guarantee an entity’s compliance with legal or fiduciary obligations

Surety is an interesting business. Especially for Government buildings etc. the owner requires construction companies to provide a 3rd party guarantee if they fail to complete the project. Compared to other insurance business, surety has significant exposure to economic cycles and especially the real estate sector. So depending on how optimistic one is about Canada’s real estate sector this might be a good bet or not. The last years looked quite good from a combined ratio perspective: Combined Ratios have been between 83% and 94% in 2014-2016. However if there would be a real estate crisis in Canada, loss ratios could go up dramatically. This report for instance shows historical combined ratios of Surey Insurers in the US went up to peaks of 170% in the 1980s.

“Risk solution”: Warranty

Risk Solutions includes specialty insurance contracts managed by program administrators. These specialty insurance contracts are structured insurance solutions to meet the specific requirements of program administrators, Managing General Agencies, captive insurance companies, affinity groups and reinsurers.

Historically, our Risk Solutions business has consisted primarily of warranty programs.

(Extended) Warranty insurance is a tricky product. Usually this is sold in connection with a car manufacturer. The manufacturer covers the first 2 years and then the extended warranty covers the next 3 years. However insurance premiums are calculated and paid already in the beginning. This means for the first 2 years there are obviously no claims but they start to show up in year 3. So a portfolio of quickly growing warranty insurance covers always looks good in the beginning but if growth slows, claims can catch up.

In Trisura’s case, this already raises some concerns. Risk solution is growing extremely fast but looks VERY volatile. Combined ratios for 2016/2015/2014 were 139,4%/86,7%/111,0% which raises some questions on underwriting standards. In 2017 YTD premiums in this segment have grown by almost 50% which in my opinion could already be a red flag. If you grow so quickly in insurance, then in 9 out of 10 cases the risk has been underpriced.

Corporate: D&O, E&O liability

The major products offered by this business are: directors’ and officers’ insurance for public, private and non-profit enterprises; errors and omissions liability

insurance for both enterprises and professionals; business office package insurance for both enterprises and professionals; and fidelity insurance for both commercial and financial institutions

This kind of liability insurance is often described as “long tail” meaning that claims can come many years later. Again a business where quick growth can mask a lot of troubles for some time but in Trisura’s case this segment is stable.

Other business activities

They also talk about expanding in the US and in international Reinsurance which I don’t think is such a good idea as those markets are much more competitive than the Canadian markets.

Commissions /cost ratio

One interesting aspect of their business model is that they have a very high cost ratio. The cost ratio is around 70% leaving little space for actual losses. In the first 6M 2017, the loss ratio was only ~20% after reserve releases. From the outside and without a longer term “claims triangle” it is very difficult to say if this is sustainable or not.

Management /Ownership

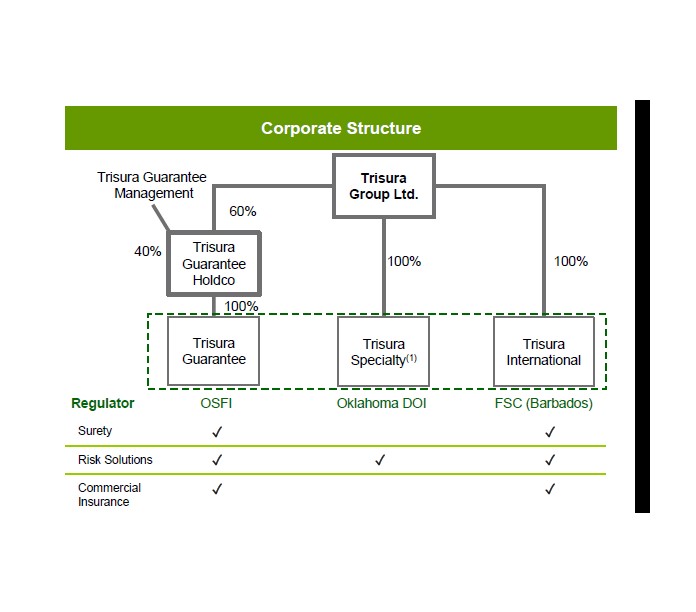

For a really interesting spin-off situation, the goals of management and shareholders should be well aligned. This is however the point where it gets messy with Trisura. Yes, there is management participation but unfortunately at the wrong level of the corporate structure as we can see in the chart from the corporate presentation:

The main operating insurance company Trisura Guarantee is only owned by 60% by the listed company, 40% belong to the management of the subsidiary. So this is clearly not an ideal alignment of interest between management and shareholders at TopCo level.

The 40% minority shareholders (=Trisura Guarantee management) have pretty far-reaching rights. On top of that they have a quite unusual put right:

As a result of the spin-off, the TG Management Group will have the right to exercise this put during the one-month period following the 18-month anniversary of the spin-off. In other circumstances, including retirement or the termination of employment of a member of the TG Management Group, TG Holdco will berequired to purchase all of the shares of TG Holdco held by such member of the TG Management Group and Trisura Group will be required, at TG Holdco’s request, to lend to TG Holdco some or all of the funds required to repurchase these shares. If Trisura Group is obligated to make, directly or indirectly through TG Holdco, anysignificant payments to members of the TG Management Group under the TG Holdco Unanimous Shareholder Agreement, then there could be an adverse effect on our financial condition and cash flows.

This put feature leads to a relatively complicated accounting treatment:

The unanimous shareholder agreement of TG Holdco (the ‘‘Unanimous Shareholder Agreement’’) among each of the shareholders of TG Holdco includes terms with a puttable feature for the common shares of TG Holdco issued to certain members of the management team of Trisura Guarantee Insurance Company (‘‘TGI’’), a wholly-owned subsidiary of TG Holdco. This puttable feature results in the common shares of TG Holdco held by TGI management being classified as a financial liability in accordance with IAS 32 — Financial Instrument: Presentation. These financial liabilities are carried at fair value in the unaudited pro forma statement of financial position of the Company which represents the put value ascribed to such common shares under the Unanimous Shareholder Agreement. As at December 31, 2016, the fair value of the liability in relation to the common shares of TG Holdco held by TGI management was $16,008 (Dec 31, 2015 — $15,812).

It is also interesting that the value of this put is so low. Trisura guarantee made 4.6 mn USD net income in 2016 which would mean that the put is valued at around 8,7 times earnings.

Where I am also struggling is the treatment of the minorities in the P&L. If I understand everything correctly, due to the liability treatment of the minority share, the change in implicit value of this put is a one line item which for instance turned a 5 mn pretax income into a 2 mn after tax loss as the put has been revalued. Unfortunately it is not explained how they value the put option.

In the 6M report they say the following:

Accounting rules require the Company to account for the Trisura Guarantee minority interests as a liability as a result of a puttable feature included within the terms of a shareholder agreement between the Company and management

shareholders (the “Shareholder Agreement”). The minority interests are revalued annually each January 1 as required by the Shareholder Agreement. While accounting rules require us to fair value this 40% minority interests, we are not able to record a fair value increase on our 60% ownership interest. Therefore, while the value of our share of Trisura Guarantee has similarly increased, we do not reflect this increase in our financial results.

Personally i think this statement is misleading. Why ? Because they show 100% of premium, underwriting income etc. although they own only 60%. So normally, without the put they would need to show “normal” minority interest which would also dilute the result for shareholders.

Valuation:

At currently ~1,5 times book value and > 20 times earnings, Trisura doesn’t look cheap either. I would have thought that the stock would trade with a larger discount to the above mentioned issues.

Summary:

Overall I don’t think Trisura is interesting at the moment. It is difficult to say how good Trisura underwrites with only 3 years of published history. Plus, the minority issue looks quite messy and is not well explained.

Combined with an already quite ambitious valuation, I think at the moment the stock doesn’t look promising. Let’s see if in 18 months the minority issue can be resolved.

Clearly Trisura will show significant premium growth over the next years but it is unclear for me if this is creating any real value for shareholders.

Valuation of put option is explained in the shareholder agreement (was part of the original prospectus filings; Article 7 says it’s the higher of either 8 times trailing earnings or of book value); management incentives (ESOP amounting to about 6.5% of shares outstanding) to be established at special meeting of shareholders on 11 Dec 2017

Ah ok. Thanks. I guess they won’t put then…

Trisura Group Ltd just bought out the minority shareholders in Trisura Guarantee – establishing 100% ownership

Thanks. Need to lool that up.

I have looked at this company and my view is about the same — though i didn’t spot all the issues you did. I received some from BAM and then tried to buy some more right at the spin off at i think around CAD 21 or 22 and the price quickly moved away. I don’t think at the current price Trisura is at all interesting. My view is that in general insurance companies are interesting at book or a discount to book. At this kind of premium to book I cant imagine finding any insurance company interesting.

DId you by the way see what happened at Nacco / Hamilton Beach spin-off? It’s still below the pre spin-off price as far as I can see.

wow, I missed that one. Overall Market cap of the 2 stocks is significantly higher than before the spin off if I am not mistaken.

Well, one of us isn’t getting it (and it might well be me). My understanding was that each NC share got given a single HBB share. The week before the spin-off NC was at 80-84 – let’s say 82. Today if I have a share of NC at 36.25, and HBB at 36.32, I’m only getting about $73. Am I being stupid?

I have to admit that I just looked at the adjusted Bloomberg chart and both stocks there look like great performers. But looking at HBB Bloomebrg seems to have something wrong here as the list HBB with 12 mn shares in total. strange.

But honestly, I haven’t looked into this company at all.

Do I understand this correctly and every Nacco shareholder actually got 2 shares of ABB ?

http://www.prnewswire.com/news-releases/nacco-industries-declares-hamilton-beach-brands-holding-stock-dividend-300521260.html

CLEVELAND, Sept. 18, 2017 /PRNewswire/ — NACCO Industries, Inc. (NYSE: NC) today announced that the Board of Directors declared a stock dividend of one share of Hamilton Beach Brands Holding Company (“Hamilton Beach Holding”) Class A common stock and one share of Hamilton Beach Holding Class B common stock for each share of NACCO Industries, Inc. Class A or Class B common stock outstanding on the record date.

I don’t think that’s what it means (but I could be wrong). I think they literally doubled the cap table class for class and then handed each shareholder an additional share of the relevant class. As you’d only hold a single class, you’ve only got 1 new share for each share you held.

Actually, scratch that last comment. Reading this http://s2.q4cdn.com/648240483/files/doc_downloads/spin_off/Stockholder-Tax-Basis-Information-Statement-for-HBB-Spinoff-FINAL.pdf shows that you got effectively two HBB shares for every Nacco share. Damn! That’s a nice profit missed! Good spot on the detail.

I guess you will not get puts for Trisura. I am not sure how much time I used, maybe 2-3 hours ? Why do you ask ?

Let’ ask the management if they sell us some 😉

I ask for the time, because I like to see how much other investors (and especially my favourites, like you) spend on such an analysis.

I think one should as well keep an eye on ROTI (Return On Time Invested) and develop something like a “bull shit radar” to avoid spending huge amounts of time on a complicated stock without any benefit.

Do you agree?

hmm, no I don’t agree. I think any stock analysis should be considered as beneficial as long as you learn something new. I t doesn’t really matter in my opinion if you actaully then decide to invest or not. You can learn a lot by looking at bad companies as well.

Fair enough. You have a point.

Physikus What is your average ROTI?

It strongly depends. I have stocks, where I spend hours and found it out of my circle of confidence or have bought them and they blew up. I have stocks were I spent 5 min and had a solid return.

So I am embarassed to say I can give no straight answer. But that’s why I want to improve there.

Maybe we should also buy some puts. I have been waiting for the typical “company gets smashed after the spin off moment”. But that didn’t happen and managment is ill insentivized. So the spin off argument is out of the window.

Thanks for your analysis, how much time did you spend?