Canada Mortgage banking follow up: Home Capital group (2) & Equitable

Quick Home Capital Group follow-up:

After my first post about Home Capital Group, a reader recommended to look at the KPMG report on Home Capital Group. This document can be easily obtained via a dedicated Home Capital Short Seller website hcgexposed.com which seems to be run by “famed” short seller Mark Cohodes.

I am a big fan of actually reading documents so I did read it fully (its only 20 pages).

My summary is as follows: Yes, there were serious deficiencies in HCG’s underwriting process. At its core, management emphasized volume growth above anything else and controls were not adequate.

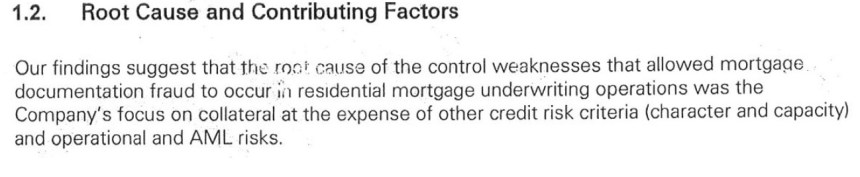

The core issues of the “documentation fraud” is summarized as follows:

Personally, I don’t think that this is such a big issue in this case. Home Capital’s “niche” was to lend to people who don’t qualify for “normal” mortgages because they are for instance self-employed:

The Toronto-based lender primarily offers uninsured mortgages to clients who are turned away from traditional banks, for reasons such as an uneven credit history or because they’re self employed. These residential mortgages account for roughly 90 per cent of Home Capital’s business.

If you explicitly lend into this niche, the collateral is of course much more critical than for standard mortgages. I didn’t fully research this but I guess what was Ok for non-standard mortgages was not OK for standard (insured) mortgages. A lot of the “Missing control” stuff can be found in any other financial organization

So I have to say it again (and taking the risk that I will be called an idiot again in the comments): Overall the KPMG report doesn’t look good but at the end, the issue was “only” documentation. There has been no proof of any fraud with regard the loans themselves (like personal kick backs to the underwriter, fraudulent payments etc.) or fraudulent accounting. Of course, management’s behaviour and the attempt to lie about all this is really bad.

At the end of the day, I am not a big fan of investing into hotly contested stocks unless I have a really high conviction, so I will take a pass on Home Equity Group for the time being.

Short look at Equitable Group

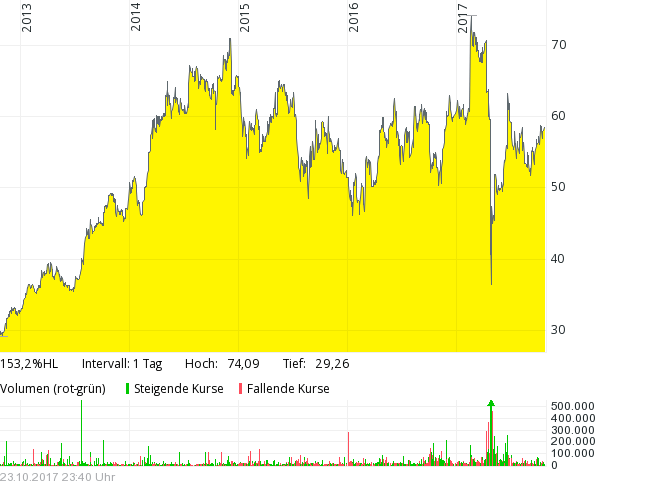

Equitable Group is a direct competitor to Home Capital Group. The stock got hammered following the Home Capital “crisis” as well but recovered to a large extent:

Interestingly, despite recovering nicely, Equitable Group still looks dirt cheap:

Market Cap: 960 mn CAD

P/B 0,97

P/E 6,1

If we look at historic numbers, they look really great for a bank:

CAGR Net Income 2010-2016: +16,9%

Avg ROE 2010-2016: +17,7%

(remark: in 2010 Equitable changed their accounts from Canadian GAAP to IFRS, so earlier years are difficult to compare)

With fast growing banks the issue is often that they increase their balance sheet much quicker than their equity, i.e. they generate earnings growth and ROE via an increase in leverage. So let’s look how this looks like for Equitable

| Equity in % | Return on assets | ROE | Credit losses/loans | Gross margin/assets | |

|---|---|---|---|---|---|

| 2016 | 4.70% | 0.80% | 17.22% | 0.015% | 1.73% |

| 2015 | 4.60% | 0.84% | 18.69% | 0.027% | 1.80% |

| 2014 | 4.39% | 0.78% | 18.23% | 0.022% | 1.75% |

| 2013 | 4.21% | 0.77% | 18.85% | 0.062% | 1.61% |

| 2012 | 3.90% | 0.74% | 19.57% | 0.022% | 1.55% |

| 2011 | 3.64% | 0.65% | 16.54% | 0.021% | 1.51% |

| 2010 | 4.22% | 0.61% | 14.50% | 0.190% | 1.14% |

So this is interesting. Equitable managed to grow while simultaneously increasing equity as % of total balance sheet. Based on this measure, the company became less risky while growing strongly, which is uncommon for financial companies,

How do they do it ?

Compared to other banks, Equitable doesn’t pay a lot of dividends. They retain ~90% of their profits. They don’t own branches so the cost/efficiency ratio is quite low.

Another factor clearly is that they show almost zero losses. The delinquency rate in Canada seems to be pretty low in general

The delinquency rate in Toronto was just 0.12 per cent, and 0.15 per cent in Vancouver, compared to a national average of 0.34 per cent.

At the same time, mortgage delinquency rates were above the national average in Prairie cities hit hardest by the slump in resource prices, including Calgary (0.35 per cent), Edmonton (0.52 per cent), Regina (0.47 per cent), and Saskatoon (0.51 per cent).

A group of East Coast cities also had above-average mortgage delinquency rates during the fourth quarter: Charlottetown (0.55 per cent), Halifax (0.54 per cent) and Moncton, N.B. (0.71 per cent).

Saint John, N.B., had the highest delinquency rate of any Canadian metropolitan area during the quarter, at 0.86 per cent. Guelph, Ont., had the lowest rate of mortgage delinquencies, at just 0.1 per cent.

The 0.34 per cent national average delinquency rate for the end of 2016 was little changed from the 0.35 per cent rate observed at the end of 2015 and the end of 2014.

Nevertheless it is interesting that they really have only 1/10th of the national delinquency rate.

Reading through a few annual reports (2016), however I couldn’t find anything special about the company. At Handelsbanken for instance it is pretty easy to find out that the culture of the bank leads to very cautious underwriting. If your pension depends on the stock price in 20 years, then you tend to think more long-term.

For Equitable, I haven’t been able to dig really deep into it. Glasdoor reviews sometimes really look enthusiastic, sometimes not. They score well on some “top places to work” rankings but not on all of them.

The CEO is there since 10 years and has reasonable equity exposure with a position of around 6 mn CAD but he seems to be quite wealthy and Equitable only is 50% of his personal net worth. The CEO before him was CEO for 17 years so from that perspective they seem to be no “Hire and fire” shop. Moor doesn’t really think highly of Home Capital which is no surprise as it is its prime competitor.

Other stuff

What I find interesting is the largest shareholder of Equitable: A guy called Stephen Smith who is also the CEO of another Canadian Mortgage company First National Financial Corporation. First National has a larger Market Cap (1,7 bn) but trades at 3 times book value. Smith has been buying more this year which is interesting as he is clearly an industry insider.

Summary:

To sum it up at this stage: There is still a lot to learn for me about the Canadian Mortgage market. With Home Capital Group I do have a problem. Not because the KPMG report was so bad, but ultimately that they lied to shareholders. Although the old management is gone, somehow this does not make me confident into the banks culture which in my opinion is one of the most important factors when looking at financial institutions.

Equitable looks like a much more interesting company. The track record looks extremely good, however at this stage i do not really understand how they achieve their ultra low loss ratios. If the Canadian Real estate market does not collapse, than equitable would be an extremely interesting stock to own. But more research is needed..

Maybe some of my Canadian readers have an opinion on Equitable and Canadian Mortgages ?

I have been an Equitable Investor for over 7 years and am a Canadian. I have been very impressed with how Equitable’s management has run the company and with their level of integrity. It has been a great stock for me. I know people keep talking about how hot or expensive the market is but really I think that is concentrated in two geographic areas: metro Vancouver and Toronto. The Canadian government has been putting in measures to cool down the market and to avoid an mortgage meltdown. I actually bought more EQB shares when all the crap went down with Home Capital Group in the spring.

Thanks for the comment. Good timing on your side 😉

Home Capital also reported low delinquencies like Equitable.

The shorts are probably looking at it this way. If you lend to less creditworthy customers, your loan losses will almost certainly be higher than lending to prime customers. Rising home prices, collateral, character, capacity, etc. all affect loan losses. If Home Capital isn’t verifying incomes (the phantom ticking described in the OSC document), then their underwriting is not good. So you would expect that their loan losses would be higher than their peers. (For what it’s worth I am short HCG. The borrow on EQB is expensive; I am not short it.)

The Friendly Bear on seeking alpha has an explanation about Home Capital’s low loan loss reserves. That author describes an instance where delinquent borrowers were able to obtain bridge loans (from a company that you wouldn’t expect to be in the lending business) before the loan was rolled over again. I can’t say whether or not that explanation is true.

thanks for the (qualified) comment. Just for reference: Home Capital’s loss ratios are in line with the country average. Equitable’s however are much much lower.

It is alos interesting that the short is expensive. I would have assumed that due to the low dividend yield, Equitable would be attractive to short if you don’t like the Canadian Mortgage market.

I am neither Canadian nor an expert, but in my opinion the Canadian housing market is clearly at a cyclical peak. Is it good to invest at a cyclical peak? Commoditiy businesses also look cheap at the top…

To be clear, I am not predicting a crash or whatever, however taking a long term perspective, one should keep this in mind.

Yes, that is a valid concern. However the stock price might already include this. Interestingly I would have expected many more defaults in Canadian housing with the slump in energy and commodity pricing.

This is why i find this interesting: Everyone seems to think/know that Canadian Housing is at a peak and will drop soon.

You can only make money against the consensus but you have to be right. Which is difficult.