The return of the Travel Series (9): Expedia (EXPE) – Cheaper than I thought

Disclaimer: This is not investment advise !!! Do your own research !!!!

The guy who wrote this post just lost a lot of money with his Silver Chef position. You might even consider shorting his recommendations 😉

Background:

When I looked at Expedia almost exactly one year ago as part of my 2017 Travel Series my key take negative aways were as follows:

– CEO has super high salary (90 mn USD in 2015)

– top line growth, operating profit stagnant

– expensive acquisitions in 2015/2016, number of shares and debt increased significantly

– reported growth numbers not adjusted for acquisitions in investor presentation

– lots of share options

Additionally, the stock looked expensive:

At 119 USD per share, Bloomberg tells me that they have a trailing P/E of 54, an expected 2017 P/E of 22,3 and an EV/EBITDA of ~16. This means that a lot of growth is already priced in.

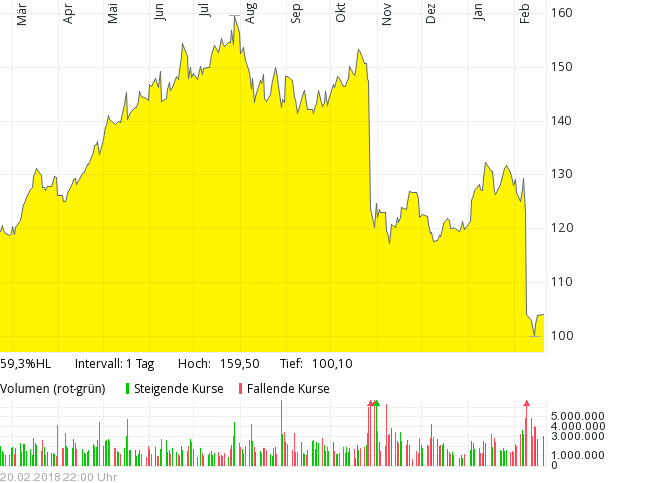

As we can see in the chart, the stock became at first even more expensive before dropping back to a level of around 100 USD / share:

What has changed ?

So the stock is now clearly cheaper than last year. Another problem has also been resolved: Super Star (and super expensive) CEO Dara Kosrowshahi left Expedia last year.

The new CEO is Mark Okerstrom:

Okerstrom is a longterm Expedia employee and was the CFO:

Prior to his appointment to the position of President and CEO in August 2017, Okerstrom served as Expedia’s Executive Vice President of Operations and Chief Financial Officer, overseeing all aspects of finance, corporate strategy, M&A, and Expedia’s eCommerce Platform Group. He first joined the company in 2006, and in 2009 he was appointed to the position of Senior Vice President and Head of Expedia Corporate Development and Strategy Group where he led Expedia’s global M&A activity around the world. In 2012 he was appointed Chief Financial Officer and added all Global Finance functions to his areas of responsibility. In 2014 he was elevated to the position of EVP of Operations and CFO, adding oversight of Expedia’s eCommerce Platform team to his remit.

Okerstrom receives 1 mn base salary. He also needs to do something for the share price to benefit from his newly granted stock options:

Overall, 2017 earnings were solid in my opinion. Around 13% top line growth translated into 6% adjusted EBITDA growth. The lower growth rate of EBITDA in comparison to top line is mostly a function of Trivago, which increased revenue by +40% but EBITDA actually declined. GAAP EPS increased significantly, adjusted EPS however slightly declined.

Interestingly, 2017 general and admin costs stayed flat. Maybe this was already the effect of the CEO change ?

Valuation & “Extra Assets”

Bloomberg now says that EV/EBITDA is 12,1, which is cheaper than last year however not that cheap.

Enterprise Value is estimated by Bloomberg at around 18.4 bn vs. the market cap of 15.8 bn. Interestingly, net debt of Expedia is only around 0.8 bn USD (down by ~0,5 bn USD vs. 2017). So where does the rest of the EV come from ?

Around 1,7 bn of the EV is some kind of “Minority interest”. Looking at the 2017 10-k, we find the following:

Page 39:

On December 16, 2016, our majority owned subsidiary, trivago, completed its IPO. In conjunction with the IPO, Expedia and trivago’s founders entered into an Amended and Restated Shareholders’ Agreement under which the original put/call rights were no longer effective and, as such, we reclassified the

redeemable non-controlling interest into non-redeemable non-controlling interest on the consolidated balance sheet. See NOTE 12 — Redeemable Noncontrolling

In connection with the acquisition of our majority ownership interests in trivago in 2013, we entered into a shareholders agreement with trivago’s founders

that contains certain put/call rights whereby we could cause the founders to sell to us, and the founders could cause us to acquire from them, up to 50% and 100%

of the trivago shares held by them at fair value during two windows. The first window would have closed during the first half of 2016. However, during the second

quarter of 2016, we and the founders agreed not to exercise our respective put/call rights during that window and instead to postpone the window while the parties

explored the feasibility of an IPO of trivago shares. On December 16, 2016, trivago completed its IPO for proceeds of approximately $210 million after deducting

discounts, commissions and offering expenses and became a separately listed company on the NASDAQ. Prior to the initial public offering, we owned 63.5% of

trivago. In conjunction with the initial public offering, Expedia and trivago’s founders entered into an Amended and Restated Shareholders’ Agreement under

which the original put/call rights were no longer effective and were replaced with a contingent founder held put right whereby Expedia would be obligated to buy

all, but not less than all, of a founder’s shares in the event a founder is removed from trivago’s management board under certain circumstances which are within the

control of Expedia. Immediately prior to the offering and the effective date of the newly Amended and Restated Shareholders’ Agreement, we adjusted the fair value of our redeemable non-controlling

interest to reflect the estimated fair value immediately prior to the offering. We then subsequently reclassified the redeemable non-controlling interest into nonredeemable

non-controlling interest on the consolidated balance sheet as the non-controlling interest was no longer redeemable pursuant to the Amended and

Restated Shareholders’ Agreement. Post offering, and as of December 31, 2016, our ownership interest and voting interest was approximately 59.7% and 64.7% of

So to cut a long story short: If I understand it correctly, the minority interest shown is the market value of the Trivago shares of the founders at the IPO of Trivago. This itself is interesting as the current share price of Trivago (8 USD) is around 30% lower that the IPO price, so “mark to market” minority interest (and EV) should go be at leat 0,5bn USD lower.

But that brings as to a more interesting point:

How would Expedia look like if they would spin-off Trivago ? Expedia is not a newcomer to spin-offs. As I have mentioned, they spun off TripAdvisor in 2013.

Trivago in 2017 contributed around 750 mn in sales but only 5 mn in EBITDA. So EBITDA would remain unchanged. However from a shareholder perspective, EV would change as follows:

- Minority interest would decrease by 1,3 bn USD

- Expedia Shareholders would receive 1,7 bn worth of Trivago shares (or around 13,40 USD in trivago shares per Expedia shares

So in total, such a spin-off would “unlock” 3 bn in EV without changing EBITDA.

Additional “extra assets”

Expedia holds 2 other “extra assets” for which EV should be adjusted:

- a 13.9% interest in listed Despegar, worth 275 mn USD

- a recently purchased ~30% stake in Indonesian travel site Traveloka, worth 350 mn

Again thos assets could be seen as extra assets that so far do not contribute to EBITDA.

As a summary, here is a short table how I would adjust EV/EBITDA for Expedia:

| Expedia | |

|---|---|

| Equity value | 15.6 |

| Net debt | 0.94 |

| minority interest | 1.62 |

| Total EV | 18.16 |

| Cash & ST Inv | 3.31 |

| Gross debt | 4.25 |

| Free cashflow | 1.1 |

| EBITDA (adj.) | 1.712 |

| EV/EBITDA | 10.6 |

| Extra Assets | |

| Despegar | 0.26 |

| Traveloka | 0.35 |

| Trivago | 1.72 |

| Total | 2.34 |

| Adjusted EV | |

| Gross EV | 18.16 |

| Adjusted extra Assets | -2.34 |

| minus MI Trivago | -1.3 |

| Adjusted | 14.52 |

| Adjusted EV/EBITDA | 8.5 |

So suddenly, we have moved for an expensive 16x EV/EBITDA in 2017 to a rather interesting EV/EBITDA of 8,5, reflecting the extra assets and special effects of the Trivago stake.

Why is the stock cheap ?

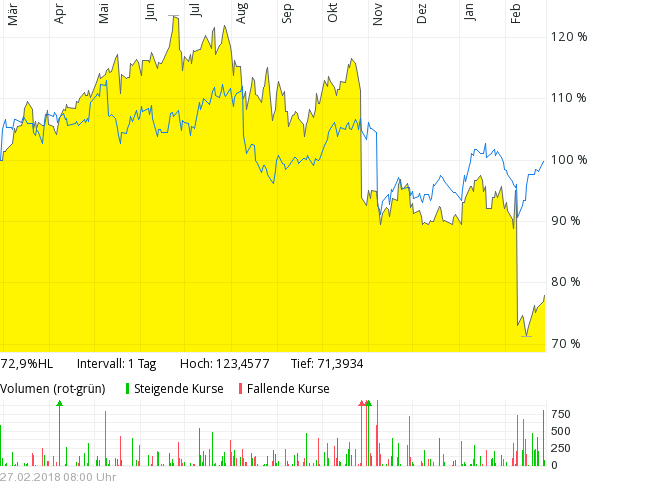

Despite the change of the CEO, Q3 2017 was in general not good for any travel stock. Analysts seem to have expected better from the sector. If we compare Expedia with Priceline, we can see that Priceline dropped as well after Q3 2017 but since then has been fairly stable:

Maybe it has to do with the cautious outlook Okerstrom gave in the Q4 press conference. This quote seems to summarize it well:

“Under new management, Expedia is more aggressively investing in tech and marketing to scale its global footprint and catch up to industry leader Priceline Group Inc , which currently has approximately 2x the inventory and room nights sold as Expedia,” RBC Capital Markets analyst Mark Mahaney said.

Mahaney lowered his price target for Expedia’s shares to $141 from $155

I find this quite interesting, that investing more into one’s business directly leads to a downgrade from an analyst. All other things equal, I actually prefer a company that invests into it longterm prospects compared to a company that just harvests its current market position.

I don’t find it too surprising that a new CEO doesn’t come out swinging and promising aggressive profit growth targets. I think it would be very natural that he politely (and indirectly) criticizes that under the old management, Expedia didn’t invest enough in organic growth and instead only focused on M&A.

Summary:

As the post has gotten already quite long, a quick summary:

- Online travel is still a growth industry with a long runway of growth

- Expedia as the global number 2 has a good chance to participate in this long-term growth trend

- The stock price has corrected significantly because the market seems to be disappointed about the new CEO and his “Back to organic growth” strategy

- I think the organic growth strategy makes a lot of sense

- Adjusted for “extra assets”, the stock looks relatively cheap on many metrics

Putting it al together, I do like the risk/return profile of Expedia at its current price. I think that it is not unlikely that Okerstrom will meet his vesting target of 200 USD/share in 3 1/2 years.

Therefore I initiated a 3% position for the portfolio at around 104 USD/share.

Disclaimer: This is not investment advise !!! Do your own research !!!!

The guy who wrote this post just lost a lot of money with his Silver Chef position. You might even consider shorting his recommendations 😉

https://www.reuters.com/article/us-usa-leisure-antitrust/u-s-state-ags-looking-into-expedia-group-hotel-practices-in-antitrust-probe-idUSKCN1SF2NY?utm_medium=Social&utm_source=twitter

That looks shitt*…

to m e that looks like a pretty standard comlaint against any online aggregator

Hi, I really really like your blog! thanks for sharing and keep up with the amazing job your are doing!

As you mentioned a year ago, EXPE operates (mostly) in the merchant business model. This results in negative working capital (= free money to grow). So: 1. As far as I understand it, you can’t deduct cash from debt. the $3.3B of cash and short-term investments (assets) are offsets by the $3.2B deferred merchant bookings (liabilities) and $0.3B deferred revenue, not by the long-term debt. So you have to adjust the EV. 2. Because of the negative working capital, I’m not sure that free cash flow is a good proxy for “earnings power” – if and when growth will stop for some reason, it will be a cash drain so FCF will converge into net income and not the opposite. It’s probably a long way to go but it’s important to notice. 3. I think that hotel suppliers (and even travelers) prefer the agency business model over the merchant (while shareholders of course should prefer the opposite) for obvious reasons (better cash cycle) and that’s another reason why booking.com has much better organic growth. If that’s true, EXPE will have to change from merchant to agency and it won’t be pretty – negative to positive working capital will be a huge cash drain.

What do you think?

Thanks for the comment. Maybe a few facts upfront:

– the merchant business is silghtly more than 50% of 2017 revenues

– I do not adjust EV by negative working capital. if a company has negative working capital in my opinion this is a positive but of course anyone can adjust whatever he/she wants

– the merchant business is still growing healthy (+11% in 2017, mostly organic)

You are right, Booking is growing faster but that’s why they are more than 2x as expensive,

Overall I do not follow your conclusion. I think the merchant modell will not go away and I don’t think that a business with negative working capital is something negative. Rather the opposite.

– I agree that negative working capital is good in general.

– It is also a risk if growth stops for some reason because the business is more leveraged.

– I don’t know if the merchant model will decline relative to the agency model. But it’s a tail risk (because of the leverage)

What do you think about analysts talking about Amazon entering the OTA market once again. Just Amazon pumping stories or do you consider it a real possibility? What’s your take on a possible competition from Amazon?

Good point. I would be surprised if they do so because they would then directly compete with their main ad costumers. The additional profit pool available in my opinion is much smaller than what they are currently earning from Expedia & Co.

Did you just mixed up amazon and google?

Nice One

Analysts fear that a more aggressive EXPE vs PCLN will hurt margins for both players (EXPE bidding up google keyword pricing for example).

Long term, I do not think the juicy 10-15pc commission per online hotel booking is sustainable, as users become more sophisticated. End customers will gradually learn how much their booking is “worth” to a platform, and that there are sites that let you share in that (through miles, free nights, whatever). Even smaller accomodation providers will use inexpensive channel management software that lists inventory on all sites, reducing Booking.com’s uniqueness. Large hotels will try to chip away on OTA’s dominance on the legal front.

Expedia and Booking are distribution platforms.

The question is, if Hotels (and Hotel Chains) can do distribution more efficiently than the aggregators. Of, course, every Hotel will tell you: Sure no problem. but in Internet economics, size (and network effects) does matter and people want to be able to compare.

Thanks for the write-up and spotting the extra assets! I also think the OTA space is very attractive.

Have you looked into the quality of the “Adj. EBITDA”?

It includes c150m in stock-based compensation (SBC). Some (tech) companies already came to the conclusion that these are real costs (who would have thought?). Other adjusted costs (legal costs, occupancy tax,…) look regular to me. The 625m EBIT looks like a better metric to me. The stable G&A costs you observed is only due to the heavy decline in SBC.

thanks for the comment. and yes, SBC most likely declined becasue of the exit of the “Super CEO”.

I agree that the adjustment for SBC is not justified. One should adjust the adjustment ;-). I think it is still Ok to compare the stock relatively to players like Priceline and Tripadvisor.

Abut EXPEDIA: their ROE went as: 20.3 (2014), 23.0 (2015), 6.3 (2016), 8.7 (2017). To the question: “what happened?”, you already gave the answer: ‘expensive acquisitions in 2015/2016, number of shares and debt increased significantly’.

Question is: can they go back to those figures? And equally important question what is the growth potential ?

In any case your bet in Expedia seems better than that of Silverchef (which to me was a bit like consumer credit for McDonalds competitors)…. and maybe the story is not over and manage a good reverse…

It is always easier to assess the attractiveness in hindsight.

“A priori” I think the Silverchef idea was not worse (or better) than all the others. But more on that a later point in time.