Homework: Electrica SA update

Electrica is the only remaining “Emerging Market” stock in my portfolio. I bought the stock in December 2014 and now after 3 year and some months it maybe time to assess how the situation looks against my initial expectations.

Including dividends, the stock is up ~18% in total since then, in my portfolio however the stock is flat because I bought more of Electrica at higher prices. Compared to a +53% performance of the portfolio in the same period, the stock is clearly a underperformer and the question is clearly if I should keep the stock.

My initial thesis relied on the following assumptions:

- the stock was cheap for a grid company with guaranteed returns on invested capital

- Romania was supposed to grow significantly and Electrica as well

- As a former Government owned company, I expected significant cost savings potential

- I had expected After Tax / After minority Earnings of around 442 mn RON in 2017

What happened ?

In the beginning, everything looked great, especially 2015 was a knock-out year. But as this table shows, already 2016 profit was stagnating but still in line with my expectations, before 2017 profits then fell significantly short of expectations, despite having purchased the minority stakes from Fondul at a reasonable price:

| 2014 | 2015 | 2016 | 2017 | |

|---|---|---|---|---|

| Exp. Profit a.M. | 252.6 | 311 | 376.9 | 441 |

| Act. Profit a.M. | 296.8 | 362.4 | 356.6 | 192 |

| 117.50% | 116.53% | 94.61% | 43.54% |

The result presentation from 2 weeks ago now tries to explain this very unfavourable outcome.

One factor is an incentive programs for people to leave the workforce. As a prior Government entity, it is pretty clear that the company was quite overstaffed and adjusting the workforce makes clearly a lot of sense in the long-term. For 2019, this was supposed to be a 59 mn RON (pretax) expense which explains a little bit less than 50 mn RON after tax. The mention around 37 mn RON (pre tax) for other one-offs, which leaves a lot more to explain.

Electricity prices

The bigger problem seems to be the unexpected strong growth of the country and as a consequence sky rocketing electricity prices. For some reason, electricity production in Romania did shrink, while Elctricity consumption increased due to the current economic boom. Already in the initial assessment I pointed out that the legacy electricity supply business could be vulnerable:

– business is partly electricity distribution, no pure “grid” play (no guarantees for distribution)

As prior Government entity, Electrica has to carry old retail contracts where former clients can get electricity at guaranteed prices. This means that Electrica could not pass through the significantly rising wholesale prices to most of its customers.

Instead of a ~174 mn RON pre-tax profit for the supply division that I had projected for 2017, the segment only made a profit of 1 (!) mn RON, leaving a gap of 173 mn RON pre tax to my estimates. It looks like that the situation is improving a little bit but I guess my initial estimates for the supply segment were clearly to optimistic,

In the distribution segment, investments are ramping up a little bit slower than I thought. However, unexpected for me, the distribution part has also hit by the rapidly increasing electricity prices.

The problem ist that Electrica has around 11,3% “network losses”, i.e. electricity that gets into their grid but does not reach the customer. It looks like that Electrica is responsible for buying the electricity on the market to compensate these losses and it seems that they didn’t hedge their purchases. Overall this seems to have been a negative effect of around 94 mn RON pre tax. Without this effect and the personnel reduction program, distribution profits would have been higher in 2017 than in 2016.

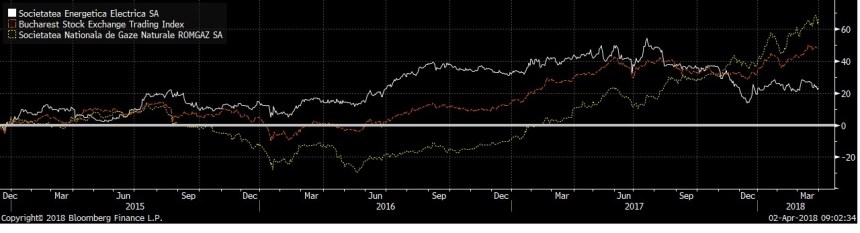

Looking at the stock chart, one can easily see how this has impacted the stock price negatively, especially in comparison to the overall index and my other previous stock Romgaz:

Electrica has been a outperformer until electricity prices rose in 2017. Since then, especially Romgaz who is an (accidental) electricity producer gained strongly whereas Electrica had to give up most of its gains. Looking back I should have kept Romgaz as a kind of “Hedge”.

Summary & what to do now ?

One of the lessons learned in the Electrica case is clearly that high GDP growth is not always good for businesses, especially if prices increases for inputs cannot be passed fully to customers.

Operationally I think Electrica is on track but I think I have underestimated the vulnerability towards volatile electricity prices.

Including the services business, I think the distribution business currently should produce ~350 mn RON in annual profit when electricity prices normalize which translates into a P/E of around 11,5. Assuming that the can grow this by 5-10% over the next years I do think that the stock ist still attractive, even if the supply segment is valued at zero.

So for me the stock is clearly a “hold”. The case might take longer as I thought, but compared to any other alternative I still think the stock is attractive at the current share price.

I don’t question the “one-off” character of the losses due to the spike in energy prices in 2017. LTM EBITDA in Q3 2018 is close to 50% up YoY and not far off the levels of 2015 and 2016. So I do expect (very) good results for 2018.

It just looks like any recovery in profits is targeted by ANRE/government by increasing requirements regarding network losses, reducing RRR, increasing taxes, …

After having bought out the minorities from Fondul Prop, Electrica should enjoy substantially higher profits on a net income to commons basis. But while 2018 looks to be a good year, I’m much less positive for 2019 (due to the reasons stated in the comments above). At the same time the net cash position of Electrica has reduced from something like 2.4bn RON at the end of 2016 to 600m RON in Q3 2018. For a Utilitiy in a benign regulatory environment, one would expect these investments to produce decent profit growth.

I’m still holding some Electrica shares and I believe the assets are worth more than current market prices imply, but it is tough to hold on when the government seems to view these companies as “enemies of the state”.

Anyway… no hard feelings, best of luck and Merry Christmas!

rumors than ANRE wants to reduce the allowed rate of return to 5.07%

https://economie.hotnews.ro/stiri-energie-22418968-anre-reduce-rata-reglementata-rentabilitate-distribuitorilor-energie-7-7-5-07.htm

Banca Translivania commented recently on the planned regulatory changes by ANRE:

Distribution tariff calculation methodology under review /negative

ANRE plans to change the methodology applicable for the fourth

regulatory period, with proposals including: RAB corrections,

investments to be grouped into categories, some expenditures to be

subject to a lower RRR (-300 b.p.), penalties for unrealized planned

investments, passing efficiency gains mostly to customers (75%

customer, 25% DSO), cap elimination for regulated inflation, royalties

and monopoly tax to be excluded from uncontrollable costs,

comparative analyses between DSOs to be used for setting the

regulated levels of controllable costs and own technological

consumption.

The Federation of Associations of Energy Utility Companies disagrees

with most of ANRE proposed items for lack of clarity.

In my opinion, by far the biggest risk for Electrica, which wasn’t mentioned in the update (but in the original post), is the political risk. There are constant (unfavourable) changes to the regulatory framework (see comment in April) and inexistent rule of law. The shocking tax plan announced this week by the socialist government puts Romania in the same category as Venezuela.

https://www.icis.com/explore/resources/news/2018/12/19/10297460/fury-as-romanian-ministers-seek-to-pass-gas-price-caps-tax/

While I can’t see that these taxes can be maintained for long (as they would likely lead to an investment freeze, bankruptcies, rising funding costs for the government, …) it is nevertheless shocking to see these things happening in Europe.

With the resignation of Willelm Schoeber from Electrica’s board (chairing the strategy and corporate governance committee), the only non-Romanian board member will leave the company early next year. He probaly had enough of it.

It would be wonderful to see the socialist government being kicked out in the near future, but with its populist agenda targeting pensioners and state employees, these seems very unlikely.

This last minute tax change comes on top of the massively reduced regulated rate of return which has been at 7.7% for the last 4 years (2014-2018) and will drop by 26.5% to 5.66% for the next 4 years.

http://business-review.eu/energy/the-regulated-profitability-rate-of-electricity-dealers-will-drop-to-5-66-percent-from-7-7-percent-in-2019-184480

I conclude that Electrica will be faced with massively falling net profits in the coming year(s).

maybe you should actually read the links that you post:

“The approved RRR to be applied from January 1, 2019 is 5.66 percent, expressed in real terms, before tax. We also note that, in order to stimulate new investments, ANRE considers supplementary remuneration, with a percentage point above the value previously mentioned, of the investments made in the energy capacities in the fourth regulatory period (2019-2023),” show the press release.

This is still a pretty generous renumeration in a European context. As this only refers to NEW investments it is also wrong to assume massively falling earnings. They will only grow slower.I guess this is the reason why the stock price actually performed quite well before the Decemeber announcement. It was also not toally unexpected.

well, if that’s true, then why hasn’t the stock price reacted back then ? Are you the only one who did read it ? I guess you are then the smartest one. Congratulations.

And by the way, Electrica has filed complaints against ANRE quite frequently, actually directly after the IPO.

Actually, both Poland and Hungary have done similar things in the past. This is not an excuse but political risk is always there.

“maybe you should actually read the links that you post”

Well sorry my friend, but I actually did and also read a few other articles related to the issue. As far as I understand the ANRE order, the 5.66% relates to OLD investments. But in order to incentivize NEW investment, these would be subject to a 1 percentage point higher rate of 6.66%. As a result, my assumption of massively falling profits (if the order is not overturned) still stands.

Electrica has filed a complaint for the annulement of ANRE’s order.

https://www.londonstockexchange.com/exchange/news/market-news/market-news-detail/ELSA/13839648.html

Maybe my first answer yesterday was a little bit harsh. But if you actually look in more details into Electrica’s account you will see that the supply businesses created large (unexpected) losses as the electricity prices spiked and Electrica had to distribute for a fixed price. if this normalizes, then earnings will get a large boost independent of the pure distribution returns.

If I read correctly, the 5,5% are still a “real return”, i.e. above inflation. Including leverage this allows still very decent ROE’s for Electrica in theory. But of course many things can happen in Romania.

A decisive factor I have not seen mentioned is Electrica’s WACC. If wacc ~ or > real return, I would run away. Only if real return >> wacc would I bear the risks embedded.

And yes mmi007 is often very harsh…

And if someone adressesd the wacc factor, then skip my comment and focus on Christmas celebrations!

Just one comment: “real return” should mean after Inflation. Wacc is pre-inflation. So don’t compare Apple to oranges.

Italgas in my opinion has little to no direct gasprice exposre.

Interestingly ITALGAS (also utility) still sports a nice ROE / ROCE, and gas prices are favourable…