Metro update: Bad, but may be not so bad at all ?

A quick update on the Metro case. This is how I ended the Metro post from a few days ago:

For me, it is currently too early to do something. It is not clear to me if the stock price has overreacted or if more trouble is coming along especially from Russia.

Selling now would be clearly an uninformed decision as well as buying more. The next step will be the release of the 6M report next week. I think I will then still wait and see how Russia develops. If, for instance there would be a further profit warning because of Russia, then this would be a clear sell signal.

So let’s quickly check out the half-year report.

The good:

- Real, the German Supermarket chain is doing batter than last year. However the improvement in Q2 was smaller than in Q1 and might have been aided by early Easter holidays

- Delivery & Real Online do well, but are small

- Asia stable despite negative FX impact

The bad:

- Metro Germany is still losing money

- Eastern Europe less profitable despite good growth

- FCF Q2 lower by -130 mn (reason given: Store openings)

- Restructuring charges at Real of up to -40 mn EUR (over 2 years if I understood correctly)

The ugly:

- EBITDA in Russia in Q2 dropped -50%, Like for like sales by almost -9%

Russia / Metro’s competition

For Metro, Like-for-like (Lfl) sales were -8,9% which is clearly “Super bad”. However also some competitors seem to have problem. Magnit for instance still showed top line growth but Lfl decreases:

Krasnodar, Russia (April 20, 2018): Magnit PJSC, one of Russia’s leading retailers (MOEX and LSE: MGNT) announces its unaudited 1Q 2018 results prepared in accordance with IFRS[1].

During 1Q 2018 Magnit added (net) 275 stores. The total store base as of March 31, 2018reached 16,625 stores (12,283 convenience stores, 242 hypermarkets, 210 “Magnit Family” stores and 3,890 drogerie stores). Selling space increased by 13.24% in comparison to 1Q 2017 from 5.15 million sq. m. to 5.83 million sq. m.

Revenue increased by 8.08% from 266.98 billion RUR in 1Q 2017 to 288.56 billion RUR in 1Q 2018.

This looks like -5% Lfl sales at Magnit although they do not report the number explicitly. This clearly does not make Metro’s number any better but I think it explains the context that it is maybe not a Metro individual problem.

Lenta, another competitor actually did a little bit better:

1Q 2018 Operating Highlights:

Total sales grew 19.9% in 1Q 2018 to Rub 93.4bn (1Q 2017: Rub 77.9bn);

Like-for-like (“LFL”)[1] sales growth of 6.1% vs. 1Q 2017;

LFL traffic growth of 0.6% combined with a 5.5% increase in LFL ticket;One new hypermarket and nine new supermarkets opened during the first

quarter of 2018;Total store count reached 338 stores as at 31 March 2018, comprising 232

hypermarkets and 106 supermarkets;Total selling space increased to 1,392,973 sq.m as at 31 March 2018

(+19.3% vs. 31 March 2017); and

Interestingly Lenta’s numbers don’t make that much sense: They added 19,3% floor space, increased sales by 19,9% and claim +6,1% LfL sales increase.

Edit:

Some readers claimed that I should not compare additional floor space in the quarter with the increase in sales. I am aware that this is a simplification. The better metric would be to use the increase in floor space 1 year ago to adjust for the treatment of new stores. On that basis, Lenta actually looks (much) worse. Lenta increased floorspace at a rate of +30% a year ago which then translated into 20% sales increase a year later. This shows even more that Lenta’s Lfl numbers seem to be comletely bogus and that their LfL should rather be -10%.

Another of the big Russian retailers, Dixy Group had already very weak results in Q4 2017:

4Q 2017 Operational Highlights:

o Revenue amounted to 73 billion RUB, demonstrating -7% yoy;

o LFL sales declined by 7.9%;

o 6 new stores opened and 7 stores closed.

Market leader X5 finally claims to have flat LfL sales in Q1 with a top line growth of 20%, but similar to lenta the numbers don’t really add up at selling space increased by 26%.

What’s clear is that the large Russian competitors of Metro added floor space like crazy over the last 12 months and I guess that this, combined with weaker than expected GDP growth then led to the observed waek Lfl numbers.

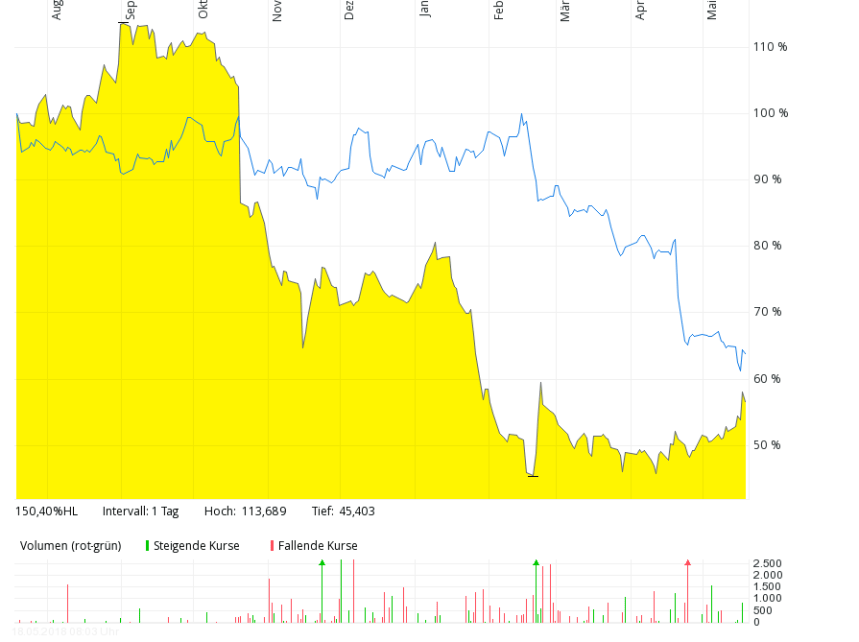

Looking at the stock chart we can see that for instance Magnit also suffered with its stock price along side Metro:

So one of my worst case scenarios from last time might (hopefully) not be the reason for Metro’s problems:

- Metro is active in Russia & Turkey. These are countries where irregularities are rather common –> is the bad outlook in Russia maybe related to a fraud case ?

Again, this doesn’t make Metro’s numbers better but for me it supports my decision to hold the shares as it doesn’t look like a pure individual problem of Metro.

I am clearly not a macro expert, but I do think if Oil prices stay where they are, this is not bad for the Russian economy and maybe we will see some recovery later in the year.

Other things

Olaf Koch, the CEO bought shares last week in a value of 1 mn EUR. For a guy who earned 1.9 mn gross (and maybe 1 mn net) last year, this is quite a statement. However he also bought shares for 1 mn in July last year, so his timing capabilities are not perfect.

In any case it is a good signal but it should not be overestimated.

Behavioural aspects – is this just regret aversion

In my last post, some people commented that not selling might be a form of “regret aversion”, which means that one is not acting although one should because of the fear that the decision will turn out to be wrong.

As a first defense I would argue that writing already the second post on my “Hold” decision clearly shows that I didn’t make it too easy for myself.

I think that I am very well aware that not selling in this case is an active decision. Actually writing these posts is for me an important exercise in order to avoid specifically these kind of biases. I think also the track record on this blog shows that I have no problems selling a losing position when I think that the situation has deteriorated so much that a recovery is not very likely (Silver Chef).

Of course I could be totally wrong and Metro will do very poorly going forward, but this is a risk I am currently actively prepared to take.

Summary:

As mentioned last time, I do think that for me selling Metro now doesn’t make sense. Clearly; i have underestimated the issues in Russia and I should have done more research into the competitors at an earlier stage. However it looks like that this is not solely a Metro problem but a market wide problem, which at least for me is a big difference.

There is no guarantee that Metro will make its reduced forecast and clearly there are other issues, but for me, at the current valuation risk vs. potential return looks pretty attractive.

I have now sold my Metro shares at an average price of around 12,30 EUR /share. Major reason are the issues in Turkey which in my opinion will make it very hard for Metro to reach their targets,

A more detailed “post mortem” will follow.

How interesting.

I added at 11 actually! Looking forward for the post mortem

LON:DPEU is the better play on the lira recovery by the way, but metro is still an interesting story in my view.

So you are already 5 EUR/ smarter than i am. Congratulations !!

Are you looking at Bayer at all?

Not really. Toi difficult dir me.

Seems too difficult from Bronte as well

Very much looking forward to the post mortem as well. Within C&C Eastern Europe, Turkey is ’only‘ the fourth biggest country in store count behind Poland, Ukraine and Romania – plus food should be more or less natural hedged (in contrast to consumer electronics over at Ceconomy for example).

But even if Turkey would drag down Metro to make them miss their targets, why does this consequently mean that Metro is still not attractively valued anymore? Their target would mean a EV/EBITDA of about 5…

Does your EV/EBITDA calculation include all the operating leases ?

I think so – here is what I used, so decide yourself:

(4.2 bn € Market Cap + 3.2 bn € expected ye Net Debt + 4 bn € PV operating leases) / (1.6 bn € EBITDA + 0.5 bn € adjustment for rent expenses)

I‘ve taken the 4 bn € from the anual report, there is a paragraph on the results of their impact analysis regarding the implementation of IFRS 16 (I have taken the worst case).

The leasing expenses I have adjusted in the EBITDA could be lower or higher: For the 0.5 bn € I have taken the difference between last years EBITDAR and EBITDA. The problem is of course, that this difference includes non-leasing rent expenses as well as non-leasing rent income – I have estimated that both add up to zero, but who knows.

Thanks. Howere I don’t think that they will manage to generate 1.6 bn operating EBITDA in the current years. 9M EBITDA was ~1.070 mn. vs. 1250 last year. So full year EBITDA will clearly not be 1.6 bn. Maybe 1.4? I would not include RE gains.

And you shoul include 0.6 bn (+ ~20%) of pension liabilities to debt.

Regarding your comments on Lenta and X5 “Market leader X5 finally claims to have flat LfL sales in Q1 with a top-line growth of 20%, but similar to Lenta the numbers don’t really add up at selling space increased by 26%”

Let me explain how this works:

>Let’s say that X5 has 100 stores last year selling $100m in total

>They claim they had +0% Like-for-Likes, so these 100 stores sold exactly the same amount, $100

>They added space by 26%. For simplicity, we assume all stores are the same size, which means they have now 126 stores.

>New stores don’t count in like-for-likes until they are one year old, and new stores are always lower sales than older stores, as it takes time to ramp-up operations

>As we know that X5 grew sales by 20% to $120, these 26 new stores sold the incremental $20, therefore the sales per store are lower than older stores at $20/26 million per store.

>This is common when you have high growth rates, as new stores dilute somewhat your margins and sales densities

On Metro in Russia, I am really worried as all competitors are aggressively investing and fighting for market share, and this was one (still is) of the profit engines of Metro. We just need to see what happened in Poland a few years ago, from double-digit EBITDA margins to losses in just a few years…

What is the value of Metro is Russia is loss-making?

Javier, first of all I think one important aspect of your comment is in my opinion at least partially wrong: New stores don’t have alaways lower sales than old ones, rather the opposite. Usually new stores have higher sales because of the novelty effect, “Grand Openings”, promotions etc. Margins are usually lower but again, claiming that new stores have lower comparable sales is nonsense-

The “formula” I was implicitly using is actually the normal way of how to check “non GAAP” numbers like same store sales for potential issues. See here: http://www.aaii.com/journal/article/financial-metric-shenanigans.touch

My expereince with Russia is: If there is any doubt than there is an issue. And I think there are issues especially for Lenta.

In any case, with so many people deeply worried about Metro at the moment, there is a high probability that the share price might have overreacted 😉

P.S.: I didn’t understand your last question.

Well in most cases this is the norm. When you open a new store, you usually need to drive traffic, customers don’t know it is there, there is a time to learn for new employees, etc.

Best in class retailers have 60/70% sales productivity in new stores compared with old fleet, it usually takes 18 months to ramp-up to steady state.

Just check their financials or transcripts, it is there. For instance, Inditex mentions 67%, similar rate for Ross Stores in the US.

My last question is, what happens to your value of Metro if Russia behaves like Poland (LSD EBIT margins)?

I am not sure if Inditex and Ross stores are a good comparison for Russian SUpermarkets.

Lenta’s store space increase includes also a significant amount of acquisitions which obviously have a lot less lead time to ramp up if what you are saying is relevant in Russia. And as I mentioned before, the further you go back in Lenta’s numbers, the worse “adjusted” Lfl sales look like. There it rather looks like -10% Lfl and then very similar to Metro and Dixy which in my opinion makes a lot more sense than reported numbers.

Well, with regard to your last question: This is the 100 EUR qeustion. How much is already priced in and what is not priced in ? We will see how it developes. “My value of Metro” assumes further profit contraction, although not to Polish levels. Plus there is upside in other regions. Or are you assuming Metro Germany will run at a loss permanently ?

And by the way, Lenta had even higher growth rates in store space a year ago (+30%). SO the 20% increase in sales a year later actually points to LFL sales of ~-10% than the 0% that I have estimated with my simplified approach.

Thanks for the hint 😉

Would be interested to know if Ennismore still holds it – are there positions published or do we have to wait for the interim/annual report?

The equation LfL = Rev – Selling space – rev is erronous. Rev is annualised (12 months) and store addition is discrete. A store can be added 1 day before the end of the financial year: extra space factored in but 12 months of revenues not collected.

I know that my Lfl “approximation” is not perfect. On the other hand it is well known that new stores usually generate more sales in the first few weeks(months than old stores (opening offers etc.) before they then turn into “Normal” stores. If topline growth diverges significantly (downwards) from increase in floor space, then a retail chain has ALWAYS big problems.

And please refer to my comments to Javier: It seems that the Lfl growth numbers for Lenta look even more bogus when you compare the rate of sales growth now (+20%) with the rate of floor space increase 1 year ago (+30).

To me it looks like that only Dixy seems to be somehow reliable in reporting Lfl numbers.

I’m not sure where you learned that “it is well know that new stores generally generate more sales in the first few weeks (months) than old stores.” A quick look at Magnit’s presentation below will show you that it takes between 6 and 15 months for new stores to mature, depending on the format.

Click to access Magnit_FY20171.pdf

Having worked on/met with grocery retailers all over the world, I can confirm Javier’s logic.

What is well known though is that as markets mature, EBITDA margins for grocery retailers tend to settle in the mid to high single digits. Walmex is the one major outlier but this can be explained by its dominant market share.

Well, maybe I overgeneralized it but I know this from High Street Retailers that do “Grand openings”. However in Magnit’s case “maturity” can mean anything from sales to margins. Interestingly, the deck that you have linked to shows that magnit had already -3,1% ifn lfl sales for the first half year 2017.

If your unversal margin rule would be true, than Metro woudl have a huge upside in Germany 😉