Silver Chef Update & “post mortem”

A few days ago, Silver Chef came out with their half-year update. There is the glossy half-year 2018 Investor Presentation and the 2018 half-year report.

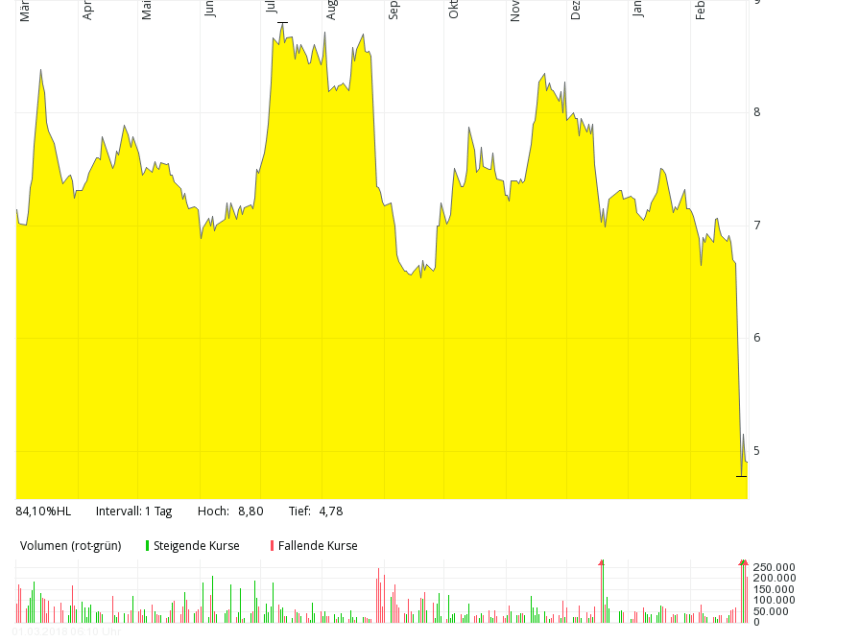

Looking at the stock price, the market clearly didn’t like the news very much:

So what happened ?

Silver Chef clearly surprised the market by announcing to exit their troubled GoGetta business. They will run down the existing book of business. The estimated restructuring cost is around 3 mn AUD, plus a “one time” charge off of 19,5 mn AUD. This will lead to a full year loss of -9 mn AUD.

Apart from that shocker, there were a few other not so nice surprises:

- Bad debts in the Australian Hospitality business increased significantly

- Estimated EBIT for the hospitality business is below 2016 levels

- Growth in Canada was relatively weak and local Management exchanged

- there seems to have been a loan covenant breach

Some points that are not clear to me are:

- why couldn’t they sell the Gogetta business ?

- Why exactly went bad debt up in the core business ? The explanation is not very convincing (preparing for growth….)

- Why did they still declare a 10 cent dividend ?

- Why didn’t they book the reorg cost directly in the first half ?

- Why did they exchange the Canadian management ?

- What amount of that “unallocated overhead costs” can be really reduced going forward ?

- Why do they announce a 500 mn CAD program in Canada but do not tell this their shareholders ?

How much could the “new” Silver Chef be worth ?

With GoGetta running off, all other things equal, going forward Silver Chef will only show the hospitality earnings. Just to illustrate the issue with a new profit estimate, let’s look how Silver Chef presents its earnings:

| 2017 | 2016 | |

|---|---|---|

| Hospitality EBT | 41,883 | 37,187 |

| GoGetta EBT | 12,815 | 16,270 |

| “unallocated” Cost | -26,356 | -21,617 |

| Total EBT | 28,342 | 31,840 |

| Tax | -8,097 | -9,484 |

| EAT | 20,245 | 22,356 |

| Tax rate | -28.57% | -29.79% |

Its easy just to exclude the GoGetta EBT, but what part of the unallocated cost remains with Silver Chef going forward ? On page 15 of the investor presentation, they split the unallocated overhead into continuing business and run-off. The continuing business gets allocated 16 mn (before tax) and the discontinued 11 mn USD. There is now way to verify this as they didn’t provide any explanation for this split.

The next table shows how this looks like based on the historic results, but also includes an alternative case where only 50% of management’s expense reduction is taken into account:

| Management Case | 50% Case | |||

|---|---|---|---|---|

| 2017 | 2016 | 2017 | 2016 | |

| Hospitality EBT | 41.883 | 37.187 | 41.883 | 37.187 |

| “unallocated” Cost | -16.000 | -16.000 | -21.178 | -18.808.5 |

| Total EBT | 25883 | 21187 | 20705 | 18378.5 |

| Tax | -7394 | -6311 | -5915 | -5474 |

| EAT | 18489 | 14876 | 14790 | 12904 |

| impl. PE | 10.3 | 12.8 | 12.9 | 14.7 |

This table tells us, if Silver Chef can indeed reach Management’s overhead cost reduction goals and profitability remains at or regains 2017 levels, the stock would relatively cheap at current prices (4,75 AUD) at the time of writing.

However if I use my 50% adjustment, the stock looks only priced “OK”.

Taken into account that at least for the current year, the hospitality business EBT will be around 35 mn only, this means that the stock based on “normalized” 2018 earnings is not cheap if we use this as calculation basis (AUD 4,75 / share):

| Management Case | 50% case | |

|---|---|---|

| 2018 | 2018 | |

| Hospitality EBT | 35.000 | 35.000 |

| “unallocated” Cost | -16.000 | -21.178 |

| Total EBT | 19.000 | 13.822 |

| Tax | -5.428 | -3.949 |

| EAT | 13.572 | 9.873 |

| impl. PE | 14.0 | 19.3 |

So we can see that based on current year’s estimate, the stock looks rather expensive, despite the huge drop in price last week. The reason is both, the exit of the Gogetta business and the significantly reduced hospitality EBIT which is now below 2016 levels.

Now the question is: How likely and how quickly will reach Silver Chef’s hospitality business the old levels ? My honest answer is: I don’t know. Plus, in my eyes, Silver Chef now requires a significant discount for me as I don’t trust the Management’s ability that much. Management claims that the GoGetta book run-off will return the book value of the assets, but after the last 12 months or so I would say there is a lot of uncertainty around that estimate.

Therefore I sold my existing Silver CHef position at current prices (~4,40 AUD/share) as I think that the shares are not undervalued despite the recent big drop in the share price.

If I have calculated correctly (including Dividends), this is a loss of around -47% for the remaining part and a total loss of -40% (including the part sold last year) or a negative impact of around -2% for the overall portfolio.

Post mortem analysis: Mistakes made & lessons learned

One of the good things about blogging is that I can look back to see how I reacted to news.

Silver Chef was part of my “extending the circle of competence” effort when I started looking at Australian stocks in early 2016. These were the posts that I wrote about Silver Chef:

Looking at my initial thesis, I guess the main reasons for buying were:

- founder led business

- strong organic growth in the past

- reasonable valuation

- the “corporate culture” seemed to be positive and somehow different

This is what I wrote about GoGetta inititally:

“Horizontal” Growth: GoGetta Australia

GoGetta seems to a similar story to the original “Silver Chef” offering. Instead of restaurants they target people who for instance want to be self-employed delivery drivers or Uber drivers. I think they occupy an interesting niche between just renting stuff which is flexible but expensive and leasing stuff which is cheaper and less flexible.

GoGetta grew incredibly strong over the last few years. They started it in 2008 from scratch and since then grew like crazy. Business doubled again over the last 3 years. Interestingly, despite growing so quickly, the new business is already very profitable. EBIT margins are at ~19% vs. 26% for the mature core hospitality business which is not bad for the short time they are actually doing this

In May 2016, GoGetta indeed looked like “THE” big growth story for Silver Chef. However some early warning signs surfaced already in my first update:

In setting the FY17 budget, the Company has also taken a more conservative position in respect of provisioning for bad debts in the GoGetta business given its significant growth and stage of maturity.

But the prospect of huge growth in Canada seemed to have compensated for this. However things only got worse from that on.

In my next update I mentioned the “Cyber Fraud” case:

Silver Chef is a different story. After a strong rally of the stock price in Summer 2016 (and without apparent reason), suddenly in November 2016 they released a “shock” press release outlining a cyber fraud case in their quickly growing GoGetta business.

Interestingly enough, within this company update, the company states the following:

The overall credit quality of the GoGetta customer base continues to improve based on changes to our underwriting policy and deal approval processes.

I think that led me to increase my initial 2% position into a 4% position, as I clearly believed that the Gogetta issues were only temporary.

Then in the August 2017 update, I decided to even further increase my position as the management gave a quite positive outlook into the current business year and the GoGetta problems seemed to have passed:

In EPS this translates into a range from 0,64 to 0,69 AUD per share or a P/E somewhere between 10-11. For me this looks (too) cheap. Therefore I increase my position from currently 3,5% to ~5% of the portfolio at around 7,30 AUD/share.

I guess this was my first really big mistake: I mostly looked at the investor presentation and not at the actual annual report.

Fortunately, a very nice reader of the blog send me an Email which pointed out that there was something strange going on: Overdue receivables had exploded without an appropriate increase in reserves for bad debt. This was only reported in the report, not in the investor presentation.

After verifying this information, I reversed my initial decision to increase my stake:

For the record: I sold the additional Silver Chef shares that I bought 2 weeks again. Why ? Well, I missed one specific issue when I looked at the numbers: Overdue receivables increased significantly, but provisioning against defaults did not increase in the same amount. Management seems to have explanations for this, but I am not 100% convinced.

I am still not giving up on Silver Chef, but my position increase seems to have been premature and I decided to reverse it (at a loss).

This move clearly limited the damage to a certain extent but I think I made my second mistake here: This issue was so grave that I should have sold my complete position. Looking back why I didn’t do so I have to say that I maybe over relied on (indirect) communication with management which had good explanations for everything.

Lessons learned from my side:

- Extremely fast growth in financial businesses should always be treated carefully. Providing credit is a competitive business and rapid, far above market growth often implies that there is wrong pricing or that you lend to the wrong people (or both)

- If problems surface, act quickly and don’t trust management’s explanations. Due to the leverage in financial companies, problems will be amplified significantly

- Read the actual exports before reading the analyst presentations. Analyst presentations often show a too rosy picture and does not mention the really critical staff

- When entering new markets such as Australia, don’t over concentrate positions. Stay small and try to learn.

So overall, I think I did not react optimally to the deteriorating situation and I could have limited my losses if I had reacted better.

this is a brilliant piece.

Ackmann, Einhorn, Woodford, etc… should learn from you.

learn what exactly? the mea culpa?

Curb your enthusiasm mate, it’s just a post mortem. All serious investors do that….

Maybe one lesson could be not to average down…

I personally have always made mistakes when averaging down

Financial forensics of own investments is not fun. A -2% is not fun either… but as the russian proverb says: no matter what it can always go worse. And a -2% you will easily survive. 😉 And it creates room for a new investment position that we will happily read very soon !

Great post-mortem mmi, we all make mistakes. As always really appreciate your thoughts.

Nice post mortem and sorry for the loss,i booked similar percentage losses from Carillion in 2017 although my position was only 1%,you are much more analytical of the reasons leading to being wrong on the company than me.

Onwards an upwards.

Congrats to your self-critical analysis. … I am sure you will be a better investor coming out of this Silver Chef transaction. I believe this is the hardest part to admit a mistake to yourself (and the readers of course).

The open and honest way you share these critical thoughts and your learnings is fantastic and extremely beneficial for yourself and your readers. I just had a similar negative experience investing into another financial business (Lending Club) and had to do the same exercise just a few weeks ago (see https://www.high-tech-investing.de/single-post/2018/02/26/Lending-Club—Ende-mit-Schrecken-oder-Schrecken-ohne-Ende ) – so I probably know how you felt writing these lines.

Thx Stefan

Kudos for doing a detailed post mortem

“Fortunately, a very nice reader of the blog send me an Email which pointed out that there was something strange going on: Overdue receivables had exploded”

That’s when the blog works at its best and you “the blogger” reap the benefit of its efforts.

It’s perhaps time to revisit Northgate now with the lessons learned from Silver Chef?

It is a different in ways, but similar in others – and getting repriced.