Silver Chef (ISIN AU000000SIV4) – The “Better Grenke” from Down Under ?

Following my previous posts on Australian stocks and Australian leasing companies in particular, it is not a big suprise that my first Australian investment is an Australian leasing/financing company called Silver Chef.

The company / the business

![]()

Silver Chef is an Australian company which according to the website “delivers equipment funding solutions that help small businesses reach their full potential.”

The company went public in 2005. Some key figures (at 9,20 AUD/stock)

Market cap: 323 mn AUD

P/E 2014/2015: 15,2,

P/B 3,11

Div. Yield 5,7%EV/EBIT 20,2

EV/EBITDA 4,9

Passing the first filters

When I did my “quick check filter”, there were a couple of aspects which I liked a lot:

+ the company is led by the founder who is also the biggest shareholder (~25%)

+ no goodwill, only (strong) organic growth

+ They have share bonus plans for employees, “great place to work” in Australia for many years

+ little analyst coverage, not in an index, almost no international shareholders

+ well written annual reports which clearly explain the business model and all relevant numbers. No or little “adjustments” within the results presentation.

The only 2 negatives at first sight:

– the growth has been funded with the issuance of new shares. However since 2012, the number of shares didn’t rise that much anymore, more or less in line with paid dividends. As I described in an earlier post, due to the franking credits, it could make sense in Australia to pay dividends and issue new share

– the CEO has not participated in the last capital increase

Business model:

Core business: Silver Chef offers flexible financing options for professional kitchen/restaurant appliances to founders/owners of restaurants.

For the clients, this saves upfront capital and reduces risk by contracting only for 1 year. If they choose to buy, they get 75% of their rental expense back. They also have the option of rolling into a cheaper leasing contract.

Silver Chef is actually a “start-up” business collateralized leasing/lending/renting company. Especially in the restaurant area, start-ups (people who want to open a restaurant) are often capital constraint. Other than technology start ups, someone who wants to open a restaurant with little or no capital does not have many places to go to for asking for money.

Offering expensive appliances with just one year lock-up can be attractive, especially when you get “cash back” after a purchase. At least in Germany, I am not aware of a similar offer. You can rent restaurant appliances for events but I haven’t seen any offerings for people who want to start a restaurant.

Opening a restaurant is risky business, many restaurants do not survive the first year. So Silver Chef’s offering really seems to be a very interesting way of keeping the risks manageable.

Competitive advantages

I don’t think that the business model is so easy to copy. Their business model does have a logistical aspect (reposession, sale of used appliances) and also the operating requirements (weekly cash collection etc). are not so easy to replicate. In the Australian hospitality business, they seem to cooperate with basically every vendor in that sector.

There is also a certain network effect in place, as they can more easily sell reposesssed equipment due to their large client base. Their offer also seems to be very attractive as a niche product between more expensive short-term rentals and more risky long-term leases.

One other competitive advantage is that they lend to businesses few other companies would lend. A “start-up “restaurant” is risky, but I guess after 30 years in the business they do have experience and a vast database.

They do so with very little requirements (1 page application) and a very short decision time (couple of hours) which might be hard to match from many competitors.

Founder/CEO/ Main shareholder: Allan English

I found an interesting interview with him here. He comes across as a genuinely interesting guy with a mission that is to enable people to start small companies. He even has donated half of his shares into a foundation which supports micro finance in poor countries:

His plan was then to use the dividend streams to fund micro finance programs for some of the world’spoorest entrepreneurs in developingcountries—giving a hand up, nota handout.In 2010, he formed the English Family Foundation, which he gave 50 per cent of his family shares, making it the largest shareholder in Silver Chef. This move gave employees satisfaction and purpose to be aligned with Allan’s charitable work; the more successful the company became, the more money would go into the foundation, and the more social good that could result.

Many companies talk about being “sustainable and responsible, but in my opinion Silver Chef is one of those companies where this is quite authentic.

Interestingly, Allan English stepped down from the CEO post in 2010, only to return in 2014. I tried to find out more, but i didn’t get that far. English is now 60 years old. This is 5 years younger than Wolfgang Grenke at Grenke Leasing.

Track record

Silver Chef’s track record is very impressive as we can see in those 10 year numbers:

10 Year EPS CAGR +18,1%

10 Year Avg. ROE +22,8%

Stock performance p.a. since IPO in 2005: +25,9% (vs. 6,21% for the ASX 200)

All this has been achieved organically, without M&A activity.

What about Future growth opportunities ?

“Horizontal” Growth: GoGetta Australia

GoGetta seems to a similar story to the original “Silver Chef” offering. Instead of restaurants they target people who for instance want to be self-employed delivery drivers or Uber drivers. I think they occupy an interesting niche between just renting stuff which is flexible but expensive and leasing stuff which is cheaper and less flexible.

GoGetta grew incredibly strong over the last few years. They started it in 2008 from scratch and since then grew like crazy. Business doubled again over the last 3 years. Interestingly, despite growing so quickly, the new business is already very profitable. EBIT margins are at ~19% vs. 26% for the mature core hospitality business which is not bad for the short time they are actually doing this

International: New Zealand / Canada Hospitality

Silver Chef started in New Zealand in 2012 and Canada in 2014. Both countries show strong growth. Clearly, Canada is the much bigger market than New Zealand. If there business model would work in Canada, then there would be a lot of “growth runway” in front of them. The New Zealand business seems to have been profitable already ~2 years after starting it and the Canadian business had a “cash flow break even” in the first 6 months of 2015/2016.

Compared to Admiral and the insurance business, it seems to be an easier business model to roll out internationally.

Valuation

Silver Chef is an interesting case. In the 10 years the company is public, it was really a growth story. For some reason, the company was never valued as a growth company. On average, the market valued Silver Chef at around 11 x earnings despite the uninterrupted growth.

Lets look again at the past 10 years:

10 Year EPS CAGR +18,1%

10 Year Avg. ROE +22,8%

Compare hat for instance with Grenke:

10 Year EPS CAGR +9,3%

10 Year Avg. ROE +13,1%

Investors currently value Grenke at 36x 2015 earnings and ~30 x 2016 earnings vs. Silver Chefs 15 times trailing earnings and ~13x current earnings. Clearly, the higher interest rate level in Australia explains part of the difference in ROE but again, to me there is no real reason why Grenke trades so much higher than Silver Chef other than that it is much more well-known among international investors.

Based on the half year report, Silver Chef has guided towards a net profit of ~ 23-24 mn AUD. Based 35,2 mn shares, that would be an EPS of 0,70 AUD/share or a P/E of 13,2..

This is clearly not “super cheap”, on the other hand this clearly does not imply a lot of growth going forward. I would rather argue that the growth actually comes for free if you compare it to Grenke for instance.

If we compare Silver Chef for instance with DWS about which I wrote two weeks ago, we can clearly see that Silver Chef is more expensive, but on the other hand, Silver Chef’s margins are not in decline and they grow like crazy organically which clearly is less risky than M&A driven growth. In direct comparison, I don’t think that Silver Chef at the current price is both, the better company as well as the better investment due to the much larger upside.

Why is the stock (relatively) cheap ?

Normally, you don’t get many companies that are growing EPS at 20-30% p.a. and trade at a P/E of 13.

I think that there are several potential factors in play. Clearly, the outlook for the Australian economy is not that great, it seems that many investors think that growth will not last that much longer.. Steven Keen for instance expects 2017 to be the year Australia goes into recession.

Also I guess that many investors are concerned about a further decline in the AUD, after a -35% decline against the USD over the last 3 years or so.For me as an EUR based investor, this is clearly a risk but also a potential diversification opportunity. Looking at Australia from a EUR perspective, I would not want to go short AUD vs. EUR over the long-term. I do like the fact that there is some natural hedge between the hospitality business in Australia and a lower AUD.

I also think that Silver Chef is not a company which performs particularly well in a scoring model, as it carries a relatively high amount of debt and at first sight was always Free Cash flow negative. Based on EV/EBIT (magic formula) for instance the company looks expensive, as many other financial services companies do. Also the high P/B ratio will scare away many book value oriented investors.

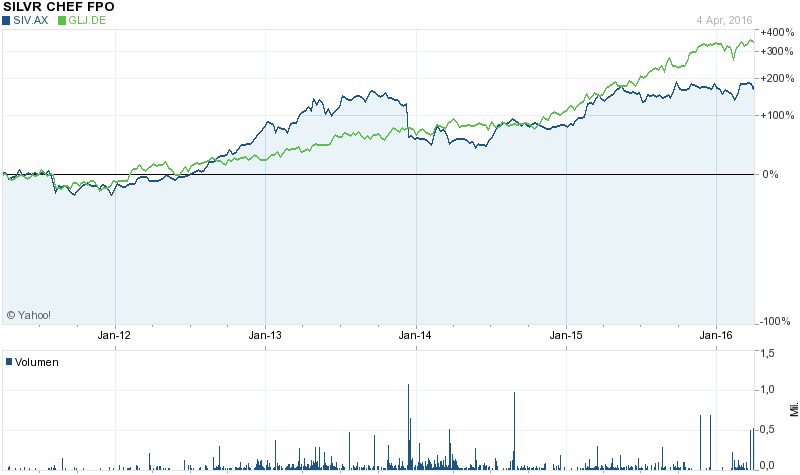

Although I am not a chartist, the stock chart also looks a little bit like it lost momentum over the last few years, especially when you compare it to a “Momentum superstar” like Grenke who goes from top to top:

Also, I think maybe with the exception of Grenke, financial services companies still have the “stigma” from the financial crisis that they are dangerous businesses and need to be valued differently (i.e. lower) than “Normal” businesses.

Finally, one could also argue that Silver Chef is more risky because they lend (or rent) to relatively risky customers. They do have higher write-offs than other financial companies. According to their last presentation, annualized writ-offs are currently at around 3% annualized relative to total assets compared to for instance Grenke at around 1,7% for 2015. On the other hand, margins seem to be high enough to compensate for that and from a leverage perspective, they are relatively conservatively financed. With an 31% equity ratio they have almost twice as much equity compared to Grenke with 17%. So taking into account the balance sheet I would say that Silver Chef is not clearly riskier than Grenke.

Summary:

Silver Chef to me looks like a very interesting company, maybe similar to Grenke a couple of years ago. They seem to have an interesting business model, occupying a niche between pure rental and leasing, which is not that easy to copy successfully. They expanded their business model within Australia into other sectors and now go international.

If they are succesful, this would mean that there is would be a lot of “growth runway” in the future. Compared to DWS, the Australian IT consultant, I would rank Silver Chef clearly before DWS.

I also like that the company and the CEO approach things “differently” to a certain extent than other companies, both by offering a rather unique product as well as having a “Mission” to support entrepreneurs.

Within my investment categories; i do think Silver Chef is a company similar to Admiral, Thermador or Handelsbanken. A company which does things differently which up until now lead them to great success. Even if they grow slower than in the past, at current prices the company still has a lot of upside.

I will therefore allocate a first 2% position at 9,80 AUD/share into Silver Chef. As this is my first Australian investment, I think it makes sense to start very carefully, as I might have missed one aspect or another.

Perhaps it’s time to revisit the original thesis on this one – I personally will not be holding it in 2018.

Is this because the announcement today ?

Amongst other things – this is showing the classical flags of a slowly eroding value trap

Increased my Silverchef Portfolio from around 2,1% of my portfolio to around 3,9%, making it a “top 10” position. Average purchase price of this piece was 7,23 AUD.

Thanks for the disclosure. This is what I would call “conviction in your own analysis”. Now I will definitely take a deeper look at the company.

Good luck,

Tom

Time to add?

not sure, need to look at the number in more details.

What are your comments on this?

http://findthemoat.com/2016/12/01/silver-chef/

Thank you. Before I answer: Waht is your comment to start with ?

Well, just to be clear: I am not a shareholder but I have analyzed the company and I’m following it with interest. I think the post I linked is very worrying and he makes a quite strong case. But on the other hand, no measures are “sub-par” so far but if the ROA would go substantially below 10 % I would start to become very worried. The deterioration is a very bad sign and the quality of the GoGetta business seems to be far below that of the Silver Chef hospitality business, but I haven’t looked into the measures in any high detail (eg. I guess his ROCE is based on his own calculations).

Still trading above 2.5x book. I wouldn’t bottom pick the stock unless I had a very good understanding of why incremental returns are dropping like a rock and conviction that its temporary. Otherwise its long way down to 1.0-1.5x book.

Well, anyone is entitled to his own opinion. However I find you analysis a little bit “superficial”……

One hint: If you try to grow 3 new businesses organically in parallel, it would be a real suprise if returns would stay constant. Clearly the risk is there but I don’t see why book value is a relavnt metric here, unless mental anchors are important.

1) Book value is always a relevant metric for finance / lease businesses. If you don’t believe that, we wont agree on much

2) My comment was not analysis. It was a warning not to fall into the “value” investor trap without being aware of a potential change in the business. If you want to pick up shares, that change needs to be understood. The lower the book value multiple, the higher the margin of safety in these businesses. Fact.

3) Yes they are growing 3 new businesses. But the cost value of GoGetta rental assets is already almost the size of SilverChef if not exceeding it already. So you’d hope they would have started seeing some scale benefits already. Grenke expanded its product range continuously. They also expanded into new countries continuously. They did this while maintaining their return profile which is obviously better.

I guess we don’t agree on much then. admiral trades at 7 times book value and is nevertheless my favorite insurance stock. Just as one example.

That’s fine. High P/BV does not always equal bad IRR and vice versa. It depends on the ROE and reinvestment opps

any thoughts on the recent bad news? much appreciated!

I will leave you with a stock tip: read the analysis on Dart group plc on VIC from mip14.

thanks. I used to own Dart Group. My own first analysis is here:

https://valueandopportunity.com/2012/06/08/boss-score-harvest-part-1-dart-group-plc-isin-gb00b1722w11/

Silver Chef: I think the stock is still attractive.

Cyber fraud attack hits Silver Chef shares

By Carrie LaFrenz

Nov. 18 (Financial Review) — Silver Chef chief executive Damian Guivarra has laid the blame for a fraud attack that sparked a write-down and a plunge in the lender’s shares on cyber criminals.

The Brisbane-based company, which provides equipment funding to small to medium sized businesses predominantly in the hospitality and fitness sectors, revealed on Friday that a fraud involving fake customers and equipment vendors would impact earnings.

“What makes this unique is financial services fraud and cyber crime,” Mr Guivarra told AFR Weekend. “This was a coordinated sophisticated attack.”

The fraud came in the form of about 60 small contracts originating from Victoria and NSW, with an average of less than $65,000 per contact. The crime involved someone applying with a fraudulent identity and using a fake vendor.

Silver Chef has two operating segments: Hospitality and GoGetta. Fraudulent customers and equipment vendors had targeted the GoGetta division, which provides equipment rental finance to other industries outside hospitality such as fitness and agriculture.

The fraud was targeted to financing for fitness equipment and believed to be over a three-month period. Silver Chef’s collections department first identified multiple payments in arrears two weeks ago, and alerted management. At first the irregularities weren’t picked up because they were linked to a long-time equipment broking partner, who is not involved in the fraud.

The stock tumbled as much as 18 per cent following the news, but finished the session down 10 per cent, or $1.11 to $9.96. Silver Chef founder and executive chairman Allan English is the group’s biggest shareholder, and suffered nearly $10 million in paper losses in the rout.

Mr Guivarra – who was appointed just two weeks ago – said the business was achieving its acquisition targets and performing in line with expectations in the first quarter, despite the setback.

“We have got confidence we can deliver for our shareholders,” he said. “Despite this event, the company is in a strong position. We are hitting our numbers for the year.”

The fraud forced the company to write down the value of rental equipment to the tune of $3.3 million. Silver Chef also flagged a one-off impairment charge of $2.2 million in its half-year accounts, with statutory earnings tipped to be in the range of $4 million to $5 million after tax. Underlying earnings are expected to be in the range of $6.3 million to $7.3 million.

Full-year earnings expectations were lowered also due to fraud. Statutory earnings is now expected to be in the range of $21 million to $23 million after tax, with underlying earnings in the range of $23 million to $25 million after tax.

The group previously guided net profit after tax of $23 million to $25 million for the 2017 financial year.

Increased my Silver Chef position to 3%. Reinvestment of part of Hornbach sales proceeds.

I think an additional explanation for Grenke being more expensive than Silver Chef, can be once Grenke acquires a new customer it becomes a recurrent stream of revenues ie Grenke can lease another computer once the old one becomes obsolete or can lease a different product within the same company. Meanwhile Silver chef has to be constantly looking for new customers in order to keep the same level of business. So the life time value of the customer per customer acquisition cost is higher for Grenke than Silver Chef.

Did anyone figure out why it dropped yesterday?

Maybe some people are disappointed that “Headline” NPAT in 2017 is forecasted “flat” against 2016 ? Who konws, I think fundamentally nothing changed.

Agreed.They equally took a credit break free charge, which is a bottomline positive event really!

https://www.silverchefgroup.com.au/irm/PDF/1719/BusinessUpdate

Ok, understood your perspective.

Surely SIV growth will not collapse as Valeant when access to equity market is more restricted but the multiple can easily de-rate if this happens, and 14x seems to price a status quo from access to capital perspective

So key to SIV thesis to me is sustainability of ROE. To answer this, I think we need to look at evolution of SIV leasing rates, at what portion of residual value they can re-lease if clients do not purchase? How this evolved historically? I could not find this from SIV disclosures…

Alex

In the world of negative interest rates, access to capital is not the issue. The problem is more if you can deploy capital profitably.

Silver Chef is currently buidling up two new businesses, Silver Chef Canada and GoGetta. Both “start ups” are less profitable than the core business and there is clearly the risk that they will never be as profitable. On the other hand. in my opinion this is also the reason why the stock is relatively cheap. I don’t know that many businesses with a 20% ROE, 10%+ growth rates and a P/E of 14. If you know any, please let me know.

mmi

Once again: I was irritated as well at first why Silver Cehf has been raising equity several times. But as I have explained, it makes a lot of sense in Australia to pay out dividends and issue new shares, as investors get a full rebate on Corporate tax paid by the company (Franking Credit).

Thank you re. Franking Credit. This is something I was not aware of, as we haven’t invested in Australia before. To extend this discussion further, I have unearthed sell-side initiation report from Macquarie from 2013, see a link below

What’s interesting about it is p4, where they show CFs over the time of the typical lease (table one on that page)

My quick calculation shows ROIC of 17-18% when lease is for 12months and over 50% (annualised) if lease is for 29 months (average lease as per macquirie).

This obviously does not match the actual ROIC they have been achieving over the last 3-4 years. Among possible explanations 1) residual value for the equipment has been dropping (due to competition, demand, etc) 2) new projects you mention do indeed have inferior economics

That’s why I think it is critical to understand historical evolution of their leasing rates and economics of new projects to be able to make a call on SIV

https://www.dropbox.com/s/ose6mmmc5e4zo2i/SIV_2015_macq_ini.pdf?dl=0

Let me know what you think

Alex

I think it is the latter. GoGetta currently is clearly less profitable for the time being but growing veryy strongly. I doubt that they will reach the same profitability as the kitchen equipment, but it still could be a decent business.

if you read the annual report, you will see that Silkver Chef reports the losses on sale of equipment compared to book value.

Ok, given I did some more digging on SIV today, here are some more findings:

1. As we suspected, decline in GoGetta’s leasing rates is primarily responsible for lower ROIC/ROE over the last few years. I define Leasing rate = rental income/cost of leasing assets.

If we isolate leasing rates for Hospitality and GoGetta, Hospitality Leasing rates remained very healthy, actually increasing from 50.3% in 2010 to 51% in 2015. However, GoGetta leasing rates declined from 55% to 47% during the same period. This may reflect more competitive environment, lack of moat for SIV in leasing equipment other than kitchen appliances.

2. I did some sensitivity analysis to understand what’s priced-in in the current consensus in terms of GoGetta’s leasing rates. Seems that consensus implies the following:

a) Legacy assets grow by 12–15% YoY in 2016–17, while GoGetta’s leasing assets grow by 30–35% YOY

b) Leasing rates for legacy business are stable at 51% of asset cost, while leasing rates for GoGetta improve from 47% to 50%

Under these assumptions, we get to the consensus revenues. Assuming expenses will remain in line with historical ratios (bad debt and salaries as % of revenue), we get to EBIT and Net Income in line with consensus. Under these assumptions, EBIT margin rebounds to 23% roughly in line with consensus and ROE is 29% (consensus is only 25%)

3.

– All else equal, if GoGetta’s leasing rate remains at the level of 2015, EBIT margin is at 21–22%, while ROE is 26% (slightly above consensus)

– If GoGetta’s leasing rate declines from 47% in 2015 to 43% in 2016, EBIT margin is down to 20% and ROE is 23% (slightly below consensus but still quite high)

Based on this, it seems that current consensus seems reasonable: even if new business is incrementally less profitable, SIV is able to maintain its ROE of more than 20% provided 30-35% asset growth in GoGetta.

Hope this helps

Alex

Agree that this looks very interesting: high ROE, ROIC, impressive increase in BVPS.

The biggest problem is negative FCF. Since 2004, SIV did not have a single year with a positive FCF(!!!). If the growth model is predicated on SIV constantly raising equity to deliver dividend and growth in BV, how is this not a ponzi scheme similar to what was happening in US MLPs over the last 3-4 years?

When the company is trading at 3x-4x EV/EBITDA as they used to during 2008-13, funding growth via equity issuance might not be a problem, provided they effectively ‘get a higher multiple’ on invested capital from investing in growth projects. However, this is not the same as issuing equity when company is at 5-6x EV/EBITDA

You keep comparing SIV to Grenke, but Grenke does have positive FCF

Dear Alex,

thanks for the comment. As I have mentioned several times, Free cashflow is not a very useful concept for financial companies especially when they are growing.

For Grenke specifically, please refer to my other post “Free cashflow reporting: Doing it “Grenke style” (Grenke, Silver Chef)”. Then you will understand that Grenke’s Free cashflow is the result of some pretty “creative” cash flow reporting.

Same for same, Silver Chef Looks much better.

MMI

mmi

Thank you on correction re. Grenke FCF, duly noted.

Let me disagree with your ‘FCF is not a useful concept for financial companies’. Please expand on your logic here, mine is below:

Let’s look at it from another perspective:

Company (financial or otherwise) creates value for the shareholders via compounding BV (by earning returns in excess of its cost of equity) or returning FCF to the shareholders as a dividend. In SIV case, dividend is funded via equity issuance, and debt, because FCF (Operating CF- Capex) is negative.

As a matter of fact, since 2004 SIV issued equity in every year except 2004, 2007-08. If company’s prospects are predicated on constant access to equity markets, how is this not a ponzi scheme: company uses new equity investors as a cash machine to fund its dividends to the existing investors?

In case of SIV, I think equity issuance was historically ‘accretive’ to the book value only because of low multiples in the past (PE multiple re-rated from 5x to 14x since 2009, P/BV re-rated from 1x to 3x over the same period) so that the new equity earned returns higher than their cost of equity.

However, as multiple re-rated, newly issued equity started to be less and less ‘accretive’ for the overall ROE and ROIC: ROE declined from 25-26% in 2008-09 to 20% in 2015. ROIC declined from 19-20% in 2008-09 to just 8% in 2015. So we have a company which earns below its wacc and has negative FCF, hence I don’t see how it will continue compounding BV

What would make FCF positive if SIV keeps growing? Not many things. SIV will keep needing more capex in order to expand, and this capex will be funded by equity earning lower and lower returns as history shows.

If you are buying it now, you inherently hope that newly raised equity will earn higher ROE/ROIC than over the last couple of years, while the opposite occurred despite being in a cheap debt environment. Other ways for SIV to actually create value for shareholders is to re-lever the company a lot more to be able to fund growth and dividend solely via debt.

Do they intend to do it? probably not.

Taking FCF issues aside, if this is a finance company, let’s look at P/BV and PE rather than EV/EBITDA (4-5x EV/EBITDA looks cheap but it is really meaningless if we think this is a finance business)

SIV is at c. 3x.P/BV and 14x PE. For a company which earns 20% ROE and has highly capital-intensive business, this does not seem cheap. When you compliment this with a business model dependent on a constant access to equity market, it does not seem cheap at all.

Please let me know what I am missing here.

Alex

Hi Alex K,

I dont mean to jump into your conversation but wanted to make a comment.

You are conflating several issues that obscure the argument. Let’s stick to FCF before talking about ROE / ROIC.

Re FCF: any capital intensive business requires capital to grow, this is widely known and accepted. In non-financial companies, this is called growth capex or any capex above and beyond maintenance capex. The faster you want to grow, the more you need to spend. If you start a restaurant and then open a new restaurant every year, you’re also unlikely to generate any FCF for the first 5 years or more. Doesnt mean you’re not incredibly successful at each restaurant. And if you grow as fast as SIV, its completely normal not to have any FCF. This really is not controversial.

Note, this is neither good or bad. This is just a fact of life. Whether it is good depends on if the ROIC / ROE generated is satisfactory. Therefore looking at the incremental returns SIV has generated over the recent years is indeed very important as you allude to.

Another small distinction, this is not a Valeant type or MF Global type situation i.e. the business does not collapse when access to growth capital is taken away. When equity markets close on SIV, they can just stop growing but they wouldn’t implode. The underlying business would not be impacted solely from equity markets shutting (NB: I am not sure what their debt structure / maturity schedule looks like)

And lastly, a capital intensive business that has access to capital and can put it to work at 20% ROE is incredibly valuable. I would say far more valuable than 14x PE. Question is whether the incremental returns will stay at 20%.

Cheers

Hi mate, great post on SilverChef, I think digging in the UK can unearth bargains in the same rental sector, like Lavendon and Northgate, both trading very close to the Bookvalue, which theoretically offers some ‘margin of safety;

http://seekingalpha.co.uk/2016/05/26/silverchef-vs-lavendon/

thanks for the comment. Pure rental in my opinion is a little bit different to what Silver Chef does.

Not possible to buy thru my broker. Which broker do you use?

DAB Bank

Got really excited with The company and considering investing. I have some worries I need to understand: It’s hard to know if depreciation charges are correct, and given the amount of capital employed it’s very relevant. For example, I can see that they had equipment disposals in 14′ and 15′ at a loss (10-15% loss over book value of equipment sold). This could mean nothing important or could mean that depreciation charges are not enough. I’m also worried about what happens if in a ciclical downturn they end up with a lot of un-leased equipment.

I’m a weekly follower of the blog. Thank you for your good reasoning and ideas.

For your own safety you shpuld assume that in a critical downturn they will end up with losses on returned stuff. And yes, they do have losses on equipment sold, but if you look at longer term numbers, this averages out over the years.

The company is clearly exposed to cyclicality and that is in my opinion one of the reasons why it is trading at a 13x P/E and not at 25x.

Hm… I looked it up back to 2008: there are always losses on equipment sold, so I don’t understand what you mean when you say that this averages out longer term. There are definetly no gains on equipment sold. ?

This does not necessarily mean that depreciation is too low: could it be that there is a connection between these losses and this:

“If they choose to buy, they get 75% of their rental expense back. They also have the option of rolling into a cheaper leasing contract.”

If customers get a rebate when buying, this would explain the losses and could indicate a really strong business model. If, on the other hand, depreciation is too low, this should cause some headache.

But then, I always get headache when thinking about rental or leasing companies 😉

Thanks for the article,

Tom

What I meant is that it averages out in total over the cycle at a rate of around 2-3% on assets including bad debt. Lossen on sales were in some years 0,1% of total assets, in the worst year 3,5% (2008).

Silver Chef clearly shos higher losses than Grneke but clearly their business is riskier as restaurants go bankrupt more often. But again this is in my opinion one of the compeitive advantages as very few institutions would lend to a newly openend restaurant.

I have noch headaches with depreciations. Annual rental income is around 50% of the average rental asset base, this means assets turn around every 2 years. So any mistake in deprectaion will realise very quickly. This is very different for instance from Airplane leasing, where problems can build up for a very long period.

I find Silver Chef more and more intriguing. The share have had a 10 year CAGR of about 20 %, BVPS for the same period have had a CAGR of 18 %, revenue since 2010 have grown 28 % CAGR, it sure looks interesting.

Any thoughts on the longer depreciation times within the GoGetta segment? I think the increasing importance of that segment raises the risk substantially, but maybe you’re right and it’s an equally attractive nische that has the same lack of competition as the core restaurant business.

Pingback: Omaha 2016: More than a Gloriously Capitalistic Weekend – Frank Weippert – Value Investing

A very interesting discovery. I always read your posts the moment they hit my inbox.

I think the “don’t” does not belong in the conclusion – otherwise I would be confused: “I ‘don’t’ think that Silver Chef at the current price is both, the better company as well as the better investment due to the much larger upside.”

Interesting company!! But isn’t booked profits overstating the real profitability? If they can’t finance growth with FCF, I guess more shares will be sold in the market, which will dilute current shareholders? What is a sustainable growth rate with positive FCF? Thanks for a very interesting write-up.

I am not sure if I understand the question. Capital intensive business need capital to grow. You can model this any way you want. The safest bet would be to use the current capital structure and then make your assumptions on growth trates and calculate what additonal equity is reuired.

However this has no impact on stated profits.

I guess I’m just a bit suspicious about companies with a sustained negative FCF. It makes me wonder if depreciation times etc. behind the EPS numbers are unreasonable too, which could risk make earnings totally unrelated to the business’ real, underlying profitability. But it sure looks like a good company, so I’m probably just overly sceptical!

“Free cash flow” in the classical sense is not a very usefull concept for financial companies.

Neither banks nor insurance companies or other “asset based” companies will create free cash flows when the are growing strongly. As I have described, Grenke triued to tackle this with a “non IFRS compliant” adjustment.

Now one could argue: That is teh reason why they performed so badly, but this is wrong in my opinion and one of the reasons why I think that finanical companies are at the moment significantly undervalued compared to non-finanical companies.

“Assets funded by Silver Chef are more stable…Kitchen appliances or vans can be used longer than computers”.

I disagree with this implication. Longer life assets are amortized less quickly and therefore carry more residual price risk. In addition, a surplus of these assets takes much longer to work through i.e. think about offshore drilling platforms / cargo ships etc and what those markets are doing. Book value of those long lived assets are written down 50% and more. Shorter life assets are amortized quickly and the fast decay rate means supply / demand imbalances work themselves out much quicker.

In theory you are right, in reality not.

If you look at Silver Chefs accounts, you will see that the asset turnover (annual lease payments compared to total lease assets) is much faster at Silver Chef than Grenke. The reason is most likley that Silver Chef charges higher rates (rental rates are higher than lease rates) and doesn’t only lease out new equipment but also a lot of second hand stuff.

They do clearly have wirte offs and losses on sales but the gross margin is much higher.

thanks for the write-up

Regarding the cyclical risk, how did their leasing book perform during 08-09 or other downturns? Yes Grenke has less equity but they also have half the loan provisions and their loan provisions went from a low of 1.76% of receivables in 2007 to peaking at 2.74% in 2009-2010. Hardly a disaster given 6-7% interest margins and a 50% ish efficiency ratio. They have much more diversified exposure too (e.g. 20% of restaurants closed in the US during the GFC and if you take out the chains, its probably a much higher level of independents).

NB: I’m not advocating buying Grenke, insane valuation. Just want to dig more into macro / cyclical risk

In the GFC, Australia was not hit that hard so their book performed actually pretty well.

One reason could also be that the underlying assets funded by Silver Chef are more stable than Grenke’s IT assets. Kitchen appliances or vans can be used longer than computers.

But we will see. Interestingly, for most restaurants that close, a new one is opened. A high “turn around” in restaurants should be good for business as they need to cook something, too.