Australia Updates: DWS & Silver Chef

DISCLAIMER: THIS IS NOT INVESTMENT ADVICE. DO YOUR OWN RESEARCH !!!!!!

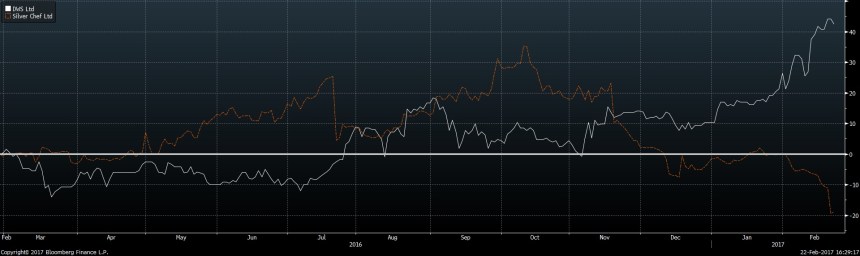

Almost exactly 1 year ago I started my exploration into the Australian stock market with DWS Ltd. and Silver Chef.

As some readers know, I didn’t buy DWS (I only put it on my watch list) and bought Silver Chef instead. Now, 1 year later it seems to be that I backed the “wrong horse”:

DWS is up +42,5%, SIV is down -19% (in AUD). So let’s look at DWS first.

DWS Ltd update

DWS released 6M numbers for 2016/2017 a couple of days ago. Overall things look good. EPS increased by +19%, and also margins, which were on a long downward trend, increased again.

For the time being it seems that they have integrated their acquisitions well. DWS currently trades at a 12,3 x earnings which doesn’t look expensive. However with currently around 1,68 AUD they are in the range of “fairly valued” if I believe what I have written last year:

The neutral case assumes stable margins, no growth but a multiple “adjustment” to a level of around 13x P/E which in my opinion would be reasonable. In that case we could double the H1 2016 result to an expected profit of 16 mn AUD times 13 = 208 mn AUD equity valuation, or 1,57 AUD per share.

One could now argue that we are maybe even in the positive case, as both profit and margins seem to have even increased:

Positive case:

In the positive case, I would assume the same margins but more growth and a P/E of 15. Assuming 5% growth p.a. for 3 years (and flat thereafter), I would then see a value of 2,10 AUD per share in that scenario.

But again, that “only” leaves a 20% upside based on my assumptions. Compared to Bouvet, the Norwegian IT consulting company I own, the upside would be higher based on their current multiples (like +50% or so). But maybe Bouvet is already over valued ?

So at current levels, I will not invest as the upside seems to depend on multiple expansion which in my opinion is risky. In the DWS case I was maybe just too slow.

Silver Chef

Silver Chef is a different story. After a strong rally of the stock price in Summer 2016 (and without apparent reason), suddenly in November 2016 they released a “shock” press release outlining a cyber fraud case in their quickly growing GoGetta business.

Silver Chef indicated that this would impact the expected profit negatively, both for the first 6 months:

On the basis that the Company intends to provide for the entire Fraud Event at 31 December 2016, statutory earnings is expected to be in the range of $4.0 to $5.0 million after tax, with underlying earnings in the range of $6.3 to $7.3 million after tax.

Consequently, statutory earnings is expected to be in the range of $21.0 to $23.0 million after tax, with underlying earnings in the range of $23.0 to $25.0 million after tax.

This pushed the stock price down from around 11 AUD to 8,40 in mid December. Clearly shareholders didn’t believe in a pure one-off event as the loss in market cap totaled around 94 mn AUD.

Then a few days ago Silver Chef released 6 months numbers and shareholders again were not happy.and the stock dropped close to 7 AUD.

What happened ? 6 month net profit was 4,6 mn, right in the middle of the range provided. Full year guidance remained unchanged:

There is no change to the Company’s full year after tax earnings forecast range of $21 million to $23million, with underlying earnings in the range of $23 million to $25 million, provided in November 2016 post the fraud event..

So let’s look at the information they provided in more detail:

- on a statutory basis, earnings in the first 6M decreased by more than -50% because of two effects: the -2,3 mn losses from the cyber fraud and a one-off positive effect in the last year. Nevertheless, even on an adjusted basis the profit would have been lower than last year

- topline growth was pretty good, especially Canada and New Zealand do well, but are still relatively small but approaching ~20% of total hospitality assets

- they lowered the 6M dividend from 0,17 AUD to 0,129 AUD per share which many investors might not like

The investor presentation provides some more details:

- bad debts increased in hospitality (3% of assets), but losses decreased

- Bad debt at Gogetta increased to ~7%

- overall bad debt is 5,2%

I think some people got spooked by those numbers. What is interesting however is the footnote on page 16:

Group bad debt increased to 5.2% -target range of 4-5%

So Silver Chef is clearly not a lender to high quality credits but rather a “small commercial subprime” lender and bad debt is part of the business. Clearly Go Getta has to improve and one now needs to look if the measures they announced are effective.

One big advantage of Silver Chef is of course that thy can reprice their business quickly. With an average maturity of 22 months, margins should improve very quickly. This is different to a mortgage bank where mispricings on 30 year mortgages will remain on the books for a very long time.

Should they just stop GoGetta and concentrate purely on hospitality ?

Hospitality is clearly the better business. With their experience and their infrastructure they have a clear competitive advantage in Australia and in my opinion also a good chance to achieve this in New Zeeland and Canada. Margins and Returns on capital are higher in the core business.

From the comments and from discussions the major criticism of many investors is that with GoGetta Silver Chef is “diluting” its margins and returns and that this is clearly value destroying.

Without knowing if GoGetta ultimately succeeds I think the underlying argument is wrong. Why ?

If a company allocates capital, value for shareholders increases if the allocated capital earns more than cost of capital. From that perspective it is irrelevant if any new business is better or worse than the existing business. The only thing that counts if you earn your cost of capital plus a margin.

If I believe the above argument, Warren Buffett should not have invested in anything that generates lower returns than See’s Candy. But Buffett the master allocator clearly knows that the returns of your existing business only matters if you can allocate more capital into it. If this is not the case, than the only thing counts is your cost of capital or in Buffet’s case the opportunity cost when you allocate capital.

In Silver Chef’s case they clearly had exhausted to a certain extent their ability to invest much more into the Australian hospitality business and decided to start new businesses. Despite the current issues at GoGetta at the moment , there seems to be demand for their product and I think there is a decent chance to turn things around.

Also their other two growth options are looking promising despite being at an early stage.

In my opinion this shows that the company has a lot of entrepreneurial energy trying to grow those businesses organically. The easier and quicker way is clearly to do a lot of M&A. With M&A you can show success much more quickly but a lot of value creation is lost for paying out shareholders of the acquired companies.

Silver Chef summary:

Based on what I discussed above and despite the obvious issues, Silver Chef still looks like a great risk/return opportunity in my opinion due to the following reasons:

- the problems are known and in my opinion can be solved relatively quickly

- there are still significant potential growth opportunities for the company

- they seem to do the right things (reducing capital, focusing on the issues etc.)

So for the portfolio I decided (as I already mentioned in the comments of the original post) to double the stake from around 2% to almost 4%.

I could of course be wrong and I am far away from Australia, but I do think that the stock still offers the best risk/return potential of all my current holdings over the next 3-5 years.

DISCLAIMER: THIS IS NOT INVESTMENT ADVICE. DO YOUR OWN RESEARCH !!!!!!

The Silver Chef Limited (ASX: SIV) share price has plunged almost 11% to $7.59 after the commercial equipment rental and financing company released its full-year results. Although revenue increased 29.4% to $286 million, net profit tumbled a disappointing 9.8% to $20.2 million. I would suggest investors continue to stay well clear of this one. Source: Motley Fool

What do you think of the numbers? Update of the business case would be highly appreciated.

The point you make is the correct one. As long as the returns generated on GoGetta are sufficiently high it doesn’t matter that they are lower than the Hospitality segment’s returns, it is still adding real value for shareholders. Silver Chef does not provide enough detail to allow one to properly compute the underlying returns in both businesses but my back of the envelope analysis suggests GoGetta’s returns are roughly half the returns in the core hospitality business.

The overall group wide returns have managed to stay relatively flat (ROE > 20%) despite the increasing proportion of the asset base coming from GoGetta as the company has increased its use of leverage (simplistically, debt as a % of total assets has risen from 47% in FY12 to 63% as at 31-Dec-16). Whilst this is something to be conscious of I am not particularly worried by this – I have always thought this company could use more leverage and put in place some smarter financing.

Unfortunately, what the rapid growth and issues in GoGetta has demonstrated is that this company is overly focused on growth at the expense of underlying quality. They have a strong core product and a huge addressable market. I for one would have liked to see a more measured approach to growth by management balancing absolute growth with returns and credit quality (both of which have clearly deteriorated as they have aggressively pushed the GoGetta product).

I think this is a culture that comes from the top (i.e. the founder). Followers of the business may recall a couple of years ago that he kicked out the CEO for missing a lofty growth target. He then stepped in himself and aggressively grew the GoGetta business and the lower underwriting standards are now coming back to hurt the company (fraud, higher bad debts and impairments etc). This is the challenge with finance businesses – you can lower your credit quality, grow rapidly and have your P&L benefit today whilst the issues don’t come home to roost for some time (which can in turn motivate management to play accounting games in the future to cover this up).

So let’s say we assume these credit quality issues are temporary and can be addressed (albeit with slower underlying growth going forward). Then it becomes a question of valuation. Here is where I think it gets tricky. For reasons the company does not fully explain, despite having an NPAT target of $23-25m in FY17, the business achieved only ~$7m in the first half of the year (all numbers exclude impact of the recent fraud). This is a very back-ended forecast and history does not suggest earnings are split so unevenly across the two halves of the year. How achievable is the FY17 forecast given, on an LTM basis to 31-Dec-16, the business produced only $13.7m NPAT (again, adjusted for the fraud)?

At the current market cap of ~$250m the business looks cheap if you assume they can hit their FY17 target (10-11x P/E) BUT this looks like an aggressive forecast and the Company is more expensive based on LTM NPAT (18.5x P/E).

The other issue impacting this analysis is the recent accounting change and the extremely large step-up in customer acquisition costs. This went from ~$11m in FY15 to ~$24m in FY16. Whereas Silver Chef previously expensed this through the P&L in the year incurred, they now amortize these costs over the course of 12 months (which effectively just pushes these costs 1 year forward). This is an acceptable approach but had Silver Chef stuck to its original accounting method the FY16 NPAT would have been $8m LOWER than reported and used in my numbers above. Perhaps the amortization of the large FY16 customer acquisition costs are producing the headwind on FY17 earnings? I would be interested to hear how you have thought about “normalized” earnings for the business today?

Sorry for taking up the comment board with such a long post…I didn’t even get a chance to share my view on the points raised in the Forager article!

Thank you for the long comment. With regard to the accounting changes: They explained the change last year. In my understanding this was a mandatory change. They were using a very conservative approach before and now must use the “normal” one. I don’t think that the impact is that big for the current year.

With regard to the expected profit in the second half: Yes, it looks ambitious, but they did stick to this target. They explain that they can reprice GoGetta rather quickly. Clearly this is a risk, but so far they seem to be consistent in delivering their promises. But we will see.

With regard to growth: I used to have the same approach but these days I see it a little bit differently. If you have the opportunity to grow profitably you should go for it even if it depresses profitability in the short term. But of course long term profitavility has to realize. However one of the advantages of strong growth is that you could also “grow out of your problems”….

But let’s see. Maybe I am overoptimistic but as I said I think the potential return if things work out in my opinion justifies the risk of a 4% position. And I do like to have some exposures to growth companies (at a reasonable price).

Agree there is still a lot to like. If they can re-create what they have in the Australian market in NZ and Canada the business could be a whole lot bigger in 3-6 years time. I am trying to work out what a reasonable level of earnings are today and then value that on the basis of more moderate growth in the coming years. I absolutely agree with everything you are saying regarding profitable growth even if it means a short term hit to earnings. My point was more that with finance businesses you can often achieve the growth WITHOUT a hit to short term earnings because the problems (i.e. poor credit quality) don’t show up until later.

I sent you a message on another Australian opportunity – CMI Limited. It is basically a net-net with a sustainable and consistently profitable (albeit volatile) business.

Thank you for the CMI opportunity, but I am not a good “net net” investor from a psychologically point of view……

I just noticed that this company has been rasing capital while making dividend payments… I wonder why they do this. They could avoid making shareholders paying tax on dividends.

Needless to say this destroys a bit of value.

I guess you haven’t read my previous posts. Due to the Australian tax system, paying “franked” dividends and reinvesting the proceeds as a capital increase does actually INCREASE shareholder value for Australian residents, especially if they invest via tax advantaged super annuation funds.

I was indeed not aware of “franked credits”… Thanks for highlighting it to me and my appologies for not having verified if you addressed it on previous comments.

Nevertheless, even though it makes sense from a domestic POV, this policy is value destructive for international investors – something that a non-Ausie resident should consider.

Good article. I’ve taken a look at Silver Chef as well.

I saw two main issues:

Bad debts are materially higher in GoGetta than in Hospitality. This issue can be adressed.

DSO are much higher (~90 days if memory serves correctly) in GoGetta. Hospitality is relatively fast turnover business, where cash is settled daily. GoGetta is the complete opposite. – This issue cannot be adressed.

-> I am of the opinion that GoGetta is a materially worse business. Additionally, if a downturn occurs, GoGetta will be materially affected and running the numbers shows that SilverChef might not survive it, at all.

well, that looks like a pesimistic view to me. Although your point is valid;: Australia didn’t have a real recession for the last 25 years or so. If there was one I do think many Australien businesses might get into trouble. However as a European investor, this is a risk I am happy to take. On our continent we are in recession now since 8 or 9 years….

Agree with L. Plus are you sure that as a “European investor, this is a risk you are happy to take”, taken into account the AUD/EUR exchange risk ?

Also are you sure that bad debt are not in uptrend ? I am saying that as I guess bad debt increased since 2015/16. I am seeing this trend (the oil slip) to resume sonner or later.

Please note my comments are more brainstorming. Hope your investment will go well..

no worries, your comments are appreciated.

Regarding the AUD/EUR risk: As a EUR based investor, the AUD rather looks like an additional opportunity to me. As far as I know, the Australian Central bank is not buying bilions of Junk debt every day 😉

The DWS name tickled my mind until a few seconds later I realized I took a look at it in 2012. It is not a very good business so I passed it. However, on the HotCopper board, someone did mention a company called Nearmap, which is the current name before they changed it. I bought into it around 0.04 and sold it in around a month for a 70% gain. However, now, every time I check the price of it, it makes me cry:

https://www.google.com/finance?q=nearmap&ei=XyW-WICLJoKJ2Aboj7WICw

I have paid a deep price for being impatient. Same story here for AMA.ax. I bought them at around 4 cents too, and sold out at around 12 cents:

https://www.google.com/finance?q=ASX%3AAMA&ei=Jie-WKmkNc7U2AbT8pvQDQ

11-12 is probably the best time to look for deeeeeeeeep value stuff in AU, but things are not cheap anymore. NZM is still worth a look since the merger might not be as dead as people assume.

isn’t it expensive in Consorsbank to invest in AUD? Are they competitive in the FX commissions ?

that’s why I opened a new account with a different broker (Sbroker).

Hi,

Ist Sbroker zu empfehlen? Kann mir nicht vorstellen dass etwas mit dem roten “S” preiswert ist … Erfahrung vom Giro.

Konnte SilverChef bei ihrem “Aktienfinder” auch nicht finden. Funktioniert der Handel im Realdepot?

Funktioniert wunderbar. Sbroker hat gerade eine Sonderaktion: Man bekommt 300 EUR Orderguthaben (auf 6 Monate limitiert) wenn man bis 31.03. ein Depot aufmacht. Das gilt nicht für Fremdspesen, aber macht den Handel doch recht günstig. Ich bin soweit zufrieden.

ValueTraderBlog,

Meinst du DeGiro. Ich habe gerade ein Konto geöffnet. Empfehlst du es nicht ?

Danke

Hi Charles,

nein ich meine das Giro Konto bei der ansässigen Stadtsparkasse (Rotes “S”).

Kontoführungsgebühren, Gebüren bei Online-Überweisungen, langsam …

DeGiro höhre ich zum ersten mal – die Preisliste sieht jedoch sehr interessant aus. Deine Eindrücke zum Broker würden mich interessieren.

Ok, danke. Es ist nur 2 woche ich habe das Konto geöffnet. Also ein bisschen zu früh zu sagen…

jetzt auf English als mein Deutsch nicht so gut ist:

What striked me is that the account bei DeGiro can only have one currency i.e CHF for me. Then all transaction in securities in other currency than the account’s currency would need to go through a fx (and of course a small commission on the fx). All in all this is still cheaper for me than any other broker. Will keep you updated..

Thank you for answering. Does that mean that if you buy … lets say IBM (USD) on SIX Swiss Exchange you have to pay FX-commission?

How much is the FX-commission on USD-dividends?

Again thank you!

HetGiro zieht interessant und preiswert aus, aber leider es zieht auch ein bisschen kaötisch. Oder, nicht zu orderntlich (und das ist nicht akzpetabel).

Deshalb bevor eine Konto dort zu öffen, warte ich auf weitere Empfelungen…. , und ich höre gern weiter auf unseres schweizeres Korrespondent ! 😉

I’ve just checked and you have both possibilities : buying on the SWX in CHF (or in USD) or buying on NYSE in USD. Concerning fx commission on dividend please check their fees document on their website as I am not sure about that.

See you

And also an old link from forager funds https://foragerfunds.com/bristlemouth/bristlemouthrent-try-buy-youre-better-loan-sharks/. There has been some activity recently in relation to payday lenders and consumer leases, the government is planning to increase regulation.

Silver chef does neither do payday lending nor provides consumer loans.

I read the Forager post as well. Two points: Silver Chef has eliminated the misleading numbers. And Silver Chef is a Business-to-business company. I don’t know that much about Australian consumer protection, but Silever Chef’s clients are all businesses.

If you want some scuttlebutt, have a look at the gogetta reviews on http://www.productreview.com.au

The reviews do not look very sophisticated.

Good analysis on the Silver Chef case. I entered my first position in the last weeks and came to the same conclusion after I did my research. It’s to be seen whether the new CEO is up to the job, but based on his work experience in the company the likelihood that this is the case is high in my opinion.