DormaKaba (ISIN CH0011795959): Cheap enough after a -30% drop ?

In my initial post for Dom Security, I lined out why the Commercial Lock business is very attractive in my opinion. As a result, most businesses enjoy nice margins.

Kaba, the Swiss company was always the number 3 with some distance to market leader Assa Abbloy and allegion.

However in 2015 Kaba finally managed to merge with he German family owned Dorma in order become a much larger and diversified Group. In theory Dorma was a great fit for Kaba as they were specializing more in building access systems which should compliment Kaba’s locking systems nicely.

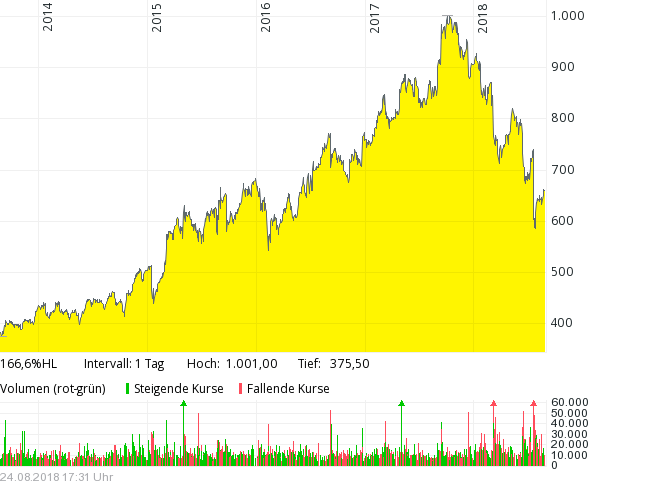

Looking at the stock price, investors liked the merger until end of last year:

What happened ?

Directly after the merger, DormaKaba announced that they target an EBITDA margin of 18% for the financial year 2018/2019. Until March this year they held up this plan despite having much more problems with the integration than they thought.

Then however, in July, DormaKaba admitted that based on the full year results of 2017/2018, they will not achieve their initial plan and postponed their 18% EBITDA target for 2 years.

Is the stock now cheap ?

When I first looked at Kaba after their -30% drop, I got super excited: with a market cap of ~2.8 bn Swiss franks, debt of 0.8 bn franks and an EBITDA of ~ 420 mn, an EV/EBITDA multiple of < 9 looked super cheap for such a high quality business.

However, I missed one important detail of the merger: The selling Dorma family shareholders didn’t actually get DormaKaba shares but a 47,5% share of the operating business, one level below the listed company.

This means that there is a significant minority position which has to be added to the EV. A rough calculation then shows an EV of (2,8/0,525)+0,8=6.1 bn and a resulting EV/EBITDA of around 15.

This is in line with the two big competitors Allegion and Assa Abbloy. So even if DormaKaba can grow faster than these two, I would not grant them a valuation premium at this point in time.

Summary:

Despite having dropped more than 30%, DormaKaba doesn’t look cheap. It looks like that at 1000 CHF at the end of last year, the stock was clearly overvalued.

For me the current valuation at 680 CHF/share looks fair, so I can see no undervaluation at this stage which for me would be required to justify an investment.

What I find interesting in this case is that some investors clearly anticipated the problems at a relatively early stage.

I do not understand your calculation for EV. In the staatement of changes in equity there is a column which accounts for profits, goodwill write-off, etc. so to get the proper EV the resulting minority value should be added to get enterprise value and is a lot less than the one calculated by you. Do you have any comment?

I am not sure that I understand your comment but the accounting value of the minority interest has nothing to do with how you calculate the EV. For the EV you need debt plus the market value of the equity. As the listed stock only represents 50% of the consolidated EBITDA, you have to double the market value to get to 100% market value of equity.

The way I calculate EV is the following:

EV = market value of common stock + market value of preferred equity + market value of debt + minority interest – cash and investments

Anyway take a look at the statement of changes in equity in the last Dormakaba annual report, you will understand what I am saying

I think your mistake is that you use the book value of the minority Interest. And again: there is nothing of relevance for calculating ev in the Statement of changes in equity.

There is a reason why they chose such a structure. Minority holders once again may get screwed.

https://www.fuw.ch/article/kaba-dorma-fusion-mit-tucken/

https://www.cnbc.com/video/2018/08/27/world-growth-the-best-is-behind-us-says-economist.html

Very good quick analysis. Unfortunately hunting for bargains is now very difficult. And many suggest best is behind us. Time to go protective / high quality ?