System1 (ISIN B00B1GVQH21) – Warren Buffett “Collateral Damage” or Structural Headwinds ?

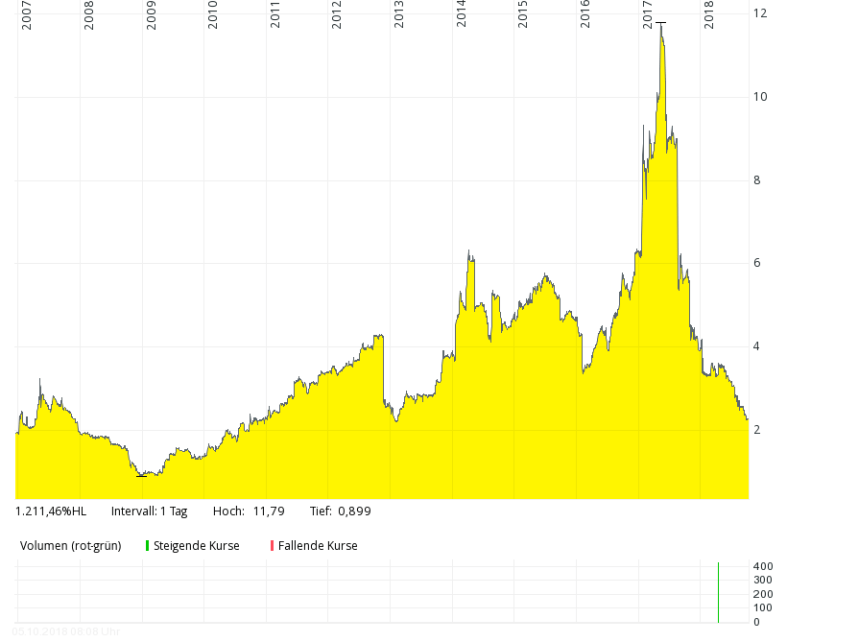

System1 (or under its old name Braijuicer) is a good example for a stock where it didn’t pay off to hold if we look at the chart:

I had looked briefly at them when Ben from Wertart bought them in early 2016 but back then didn’t take the time understand what the company was all about. After the huge drop I decided to have a deeper lok at the company.

The business

To understand the business, Ben’s 2016 post includes everything one needs to know which is great because then I don’t have to reproduce anything.

In short, System1 is mainly a market research company which tries to predict if and how market campaigns are performing based on how the campaign effects the emotion of the audience (i.e. how it effects System 1 according to Kahnemann). To measure this, they developed some quantitative measures which they seem to have sold quite succesful to mostly large consumer companies.

This approach went well for some time, the company grew from 3 mn GBP sales in 2005 (pre IPO) more than 10 times to 32 mn GBP in 2016/17.

Back then the company looked like a sure winner:

- led by a charismatic CEO with a significant share in the company

- cash generative, asset light business with a solid balance sheet (net cash)

- “cutting edge” products with good growth potential

- great investor communication (amybe no surprise for an advertising company)

- Great investors on board (Ennismore etc.)

Maybe for these reasons, the stock then went on a meteoric rise in 2017 as one could see in the chart above only then to drop equally fast until now.

What happened ?

In the FY 2017/2018, sales suddenly dropped by .-18% and profit by -73%.

Management itself seem to have been totally surprised by this and (other than the stock market) only slowly realized the issue. In early 2017, management seemed to have no clue how the next financial year would look like and predicted that 2017/2018 would more or less look like the year before (in terms of growth).

In their trading update, they saw some slow down but nothing compared to what actually happened:

As of now, we anticipate a little over break-even in Profit Before Tax in H1 (prior year: £2.8m) and a decline in full year Profit Before Tax of approximately 10-15% from the £6.3m achieved last year.

So it is pretty clear that the business as such has not a very good visibility on even the near future. The business to a large degree seems to be “lumpy” consulting business.

Blaming Warren Buffett (sort of)

In the annual report 2017/2018 they explain this the following way:

On Friday 17th February last year, Unilever received and immediately rejected a £115bn bid from Kraft Heinz Co., backed by their controlling investors, Warren Buffet and 3G Capital. Although Unilever successfully fought off the bid, the following months saw a number of the World’s largest consumer goods companies announce significant reductions in marketing spend, helping to bolster their short term profits and share price against hostile bids.

Unfortunately, these events had a more painful effect on our business than on many of our larger competitors, but also gave us the necessary insight for how to match the dramatic market changes with a dramatically more competitive offering, capable of building a far bigger, more resilient business.

So interestingly, one of the culprits seems to be Warren Buffett in this story. However a quick fact check shows that this story has some holes in it:

In reality, above mentioned Unilever had actually increased its marketing expenses in this period:

Speaking on a press call this morning (1 February), Unilever’s CFO Graeme Pitkethly said the company’s ‘brand and marketing’ spend was up slightly in absolute terms in 2017. It invested €250m (£220m) more in media and in-store in 2017 than 2016, offsetting that investment with efficiencies in ad production brought about by zero-based budgeting.

but they have been reducing the number of agencies they have been working with

Unilever has previously pledged to make efficiency savings of €2bn in its brand and marketing investment, in particular by cutting production costs and the number of agencies it works with. While the company did not detail the specific savings it has made in brand and marketing so far, it did say it will reinvest two-thirds of the savings into “capacity building and in the competitiveness of our brands”.

Procter and Gamble for instance kept its budget more or less constant in 2017 and the same holds for instance for Nestle.

So management’s explanation in my opinion is not 100% credible.

What else could be going on ?

I don’t claim to be a marketing expert, but there is one very obvious trend going on which more and more reaches the branded consumer product sector:

For more than a 100 years, John Wanamaker’s claim was true:

“Half the money I spend on advertising is wasted; the trouble is I don’t know which half.”

This was the main problem of classical advertising: How can you measure that a certain TV spot etc. is actually triggering purchase or not ? There are a lot of other factors in play, such as how the retailers were positioning the product etc. etc.

But things are changing and a new very significant trend is emerging:

Direct-to-consumer selling and marketing. For instance at Unilever:

Unilever’s direct-to-consumer drive

Unilever is also putting an increasing focus on going direct to consumer as it looks to build direct relationships with its customers. Its ecommerce sales nearly doubled to €2bn (£1.7bn) last year, helped in part by acquisitions such as Dollar Shave Club but also by “investments made in building capability”.

CEO Paul Polman cited the example of the laundry bundles it now sells on Amazon as a sign of its focus on new channels. “By understanding the Amazon search algorithm we can win in search and give a more tailored and valuable offering.

There always have been Direct-to Consumer companies in the past but this was rather the exception like the German company Vorwerk or Multi-Level-Marketing companies like Avon etc. With the internet and especially mobile, it is now much easier to reach many customers than before.

However this direct connection also allows a new form of marketing:

Direct Digital Marketing

This is from a Medium post about digital consumer start-ups and how they do their marketing:

If you wanted to advertise using old-school methods, you (at best) had a limited idea of the ROI of your advertising investment. Perhaps if you had customers return coupons to a store then you can do some primitive sort of tracking, or if they opted to tell you where they heard about you first.

Now, you have programmatic ads. In simple terms, programmatic means that ads are served to you specifically based on certain criteria. Remember when you started searching for restaurants in Cancun and all of a sudden you’re seeing ads for hotel deals? Your interests are known and stored in databases all over the world, and then you are served ads based on those interests. Or you’re served ads based on your search queries. Either way, for the first time in history, you can have extremely specific targeting preferences for advertising campaigns. This means that instead of paying to advertise to 10,000 people, then having 9,000 of those people not be interested, you can directly target the 1,000 relevant individuals that you wanted in the first place. While that’s an oversimplification, the result is the same: you pay dramatically less to target much higher-quality audiences.

This opened the floodgates for reaching customers with ridiculously specific preferences, and made it cheap to do so. You also had an unprecedented amount of data collected and can further integrate your campaigns with your on-site analytics system to truly understand the numbers and behavior involved in people coming to purchase. That means you can iterate at lightning speed instead of waiting for sales figures from stores, and then seeing how many coupons came in, and so on.

Compare this to System1: They had carved out a niche for them by offering some kind of predictive quantitative forecast on how traditional ads will reach specific persons. In the new age of direct digital marketing,g companies don’t need this anymore or to a much less extent.

Consumer are targeted directly and the success or failure of a campaign can be seen in real-time and reacted to in real time. This mostly happens fully automated this day. So there is very little requirement to do long forecasts anymore.

Clearly there will always be some general brand management which requires System1 like capabilities but at the moment at least, a significant part of marketing budgets is shifting into this new world of direct digital marketing.

Implications for System1:

I n my opinion, System1 is facing a big structural headwind: although they seem to have an innovative approach within traditional advertising, their whole market seems to be shrinking.

They try to counter this with some innovative approaches like a subscription like tool, but the problem in my opinion remains that they are stuck in a shrinking market.

Summary:

For me, it is time to stop at this stage. I am not a (digital) marketing expert, but for me the risk of a company in a secular shrinking market with no clear way out is too high. Maybe they can grab a bigger share in the traditional advertising market but other than for instance at FitBit, I don’t see how they could actually move into real new growth areas. So for me System1 is clearly not an investment, even at a lower price.

For those who seek different opinions, there are a surpisingly large amount of more positive analysis online. Some examples (most from 2016/2017):

http://latticework.com/why-we-initiated-a-position-in-brainjuicer-group/

https://www.moneyobserver.com/our-analysis/share-sleuth-brainjuicer-nailed-buy-and-hold-investment

Do you have had a look at MutuiOnline ? IT0004195308

One red flag was the rebranding. The management lost focus because they were changing their name for no tangible benefit.

I seem to remember tbere were others but travelling so don’t have my notes…

Thanks for sharing this article, I have been interested in this company recently, and it’s interesting to hear your opinion.

Not sure if you have seen this post, but in the comments you can see some notes from the AGM which are useful:

https://maynardpaton.com/2018/06/08/system1-boss-blames-buffett-backed-bid-for-client-cutbacks-and-72-profit-crash/

It does seem that if the new subscription product really took off it could be transformative for the company (apparently director talk of potentially 2,000 clients, priced at £12,000 per year per advert category), and apparently this is much cheaper than competitors – see the AGM notes. They have been investing quite heavily in this product, but I don’t know whether it will be successful or not, clearly a key question!

Thanks for the comment. Let’s wait and See if and when they will reach this goal.