All German Shares part 14 (Nr. 251-275)

This week there are as always a couple of “zombies”, some hyped real estate companies but also some interesting watch candidates and two former portfolio companies. Enjoy !!

251. Atoss Software AG

Atoss is a 620 mn market cap Enterprise Software company specializing in HR software solutions. As many Software companies, the stock has performed very well over the past few years:

The company has net cash of around 30 mn and is currently growing at ~15% p.a. and has decent EBIT margins of ~25%. However a lot of that growth seems to be priced in with a P/E >50 and a valuation of around 8-9 times sales that include a significant amount of consulting revenues. For me a “Pass” at these price levels.

252. DEFAM Deutsche Fachmarkt Ag

DEFAMA is an interesting company. It has been founded only a few years ago (2014) and is run by a former stock journalist (or “Blogger”) Mathias Schrade. The company specializes in regional small scale shopping centers. The company is valued curently at 66 mn EUR, however book equity is only 25 mn and has significant leverage (Equity before capital raise was less than 20%). To make things worse, the company pays dividends and at the same time is doing regular capital increases. As many other real estate players, DEFAMA aggressively revalues their property and shows “NAVs” significantly above their acquisition price which then enables them to take on more loans as the banks seem to be willing to play along. As far as I have seen however, they haven’t sold anything to justify their valuations. This reminds me a lot to the same game played by open ended real estate funds before the financial crisis. For me the company would be a potential short candidate, however as it is difficult to time the end of the current real estate cycle, I just “Pass” on this one.

253. Pro DV AG

1.3 mn EUR Market cap nano cap, active as IT consultant. Another Hyped Dotcom IPO. Very small business with high personell expense ratio. “pass”.

254. GFT Technologies SE

GFT is a 310 mn market cap IT service provider for the financial industry. As far as I understand they specialize in implementing third party software. The P&L looks like a “Normal” IT consulting company with >50% expenses for wages. The company had net debt and topline has been stagnating as they are losing business with their top 2 clients (Barclays, Deutsche Bank). They seem to be able to replace the business with new clients, however the bottom line has been suffering which can be seen in the stock price:

In 2018 they acquired a Canadian company that specializes in implementing Guidewire, the leading standard software for insurance companies.

For me GFT is a “watch” candidate for a later analysis.

255. Aixtron SE

Aixtron SE is a 937 mn EUR market cap machinery comoany that manufactures machines for the semiconductor industry. As the semiconductor industry, Aixtron is very cyclical which can be seen in the stock chart:

I actually “played” an attempted Chinese take-over attempt in 2016, just before the next up-cycle kicked in. The Q3 2019 numbers showed stable sales, increasing EBIT but drastically falling order backlog, so it seems the next downswing is already underway. Too cyclical for me, pass.

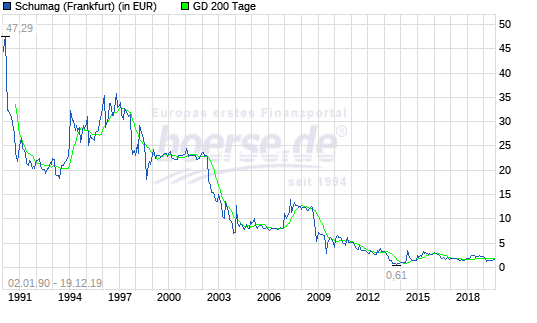

256. Schumag AG

Schumag is a 6,3 mn EUR market cap machinery company. I actually owned the stock a long time ago when the company was in much better shape. As the chart shows, this has been a long way down over the last 25 years or so:

The company went thorugh bad majority shareholders and bad management. In the recent years it looked like a turnaround had finally happened, but the first 6M of the current FY again showed significant losses. A clear “pass” for me.

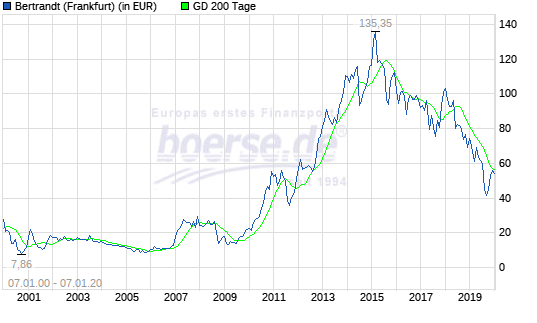

257. Betrandt AG

Bertrand AG is a 600 mn market cap automotive company which has been seen better days:

The company is an Engineering Service/outsourcing partner for mainly German car manufacturers. Looking into their annual report we can see that profitability peaked in 2015/2016. Despite stable topline, profits since then went down more than 1/3, mostly driven by increasing personell costs which account now for around 75% of the top line. My guess is that this is a combination of lower rates that can be charged to the OEMs and the pressure in the current employment sector for skilled engineers.

The French competiros like Akka or Altran seemed to have managed the last few years much better. Nevertheless, I’ll put the stock on “watch”.

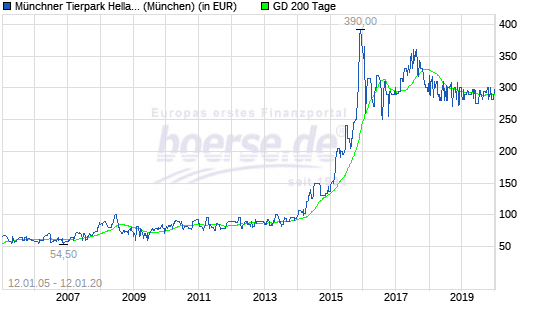

258. Muenchener Tierpark Hellabrunn AG

This is a very interesting case. Although I knew that the local Munich Zooo is stock listed, I never looked at the stock which currently has a market cap of 87 mn EUR

. Interestingly, the stock had a huge run up in 2015/2016 as we can see in the chart:

The company is majority owned by the City of Munich (93%). I am not sure what triggered that increase. The company makes a small profit but mainly driven by transfers from the city. Yes, they own ultra prime real estate in Munich, but this will never be used for any other purpose. And if I read the annual report correctly, shareholders have no profit participation rights. It used to be that sharholders got free entry but that seems to be over. “Pass”.

259. Marna Beteiligungs AG

1.5 mn Nanocap. in its previous life before restructuring, the company used to won and run some ships. “pass”.

260. 11880 Solutions AG

A 33 mn EUR market cap company that started its life as a telephone information service under the name “telegate”. The stock price chart shows that the company was a brief superstar during the dot.com bubble:

The overview on the company web page shows that the company is burning its cash since years into a shrinking business. In 2019, the business seemed to have stabilized and they actually received a take-over offer from their largest shareholder at 1,87 EUR per share. Subsequent actions (announcement of capital increase) have hurt the share price. Main new business of the company seems to be an online job portal. “pass”.

261. GIEAG Immobilien AG

A 85 mn market cap real estate company. Although I had never heard of this company, the comapny seems to have increased its stock price by 20x over the last 5 years. As a real estate developer, the company seems to have benefited a lot form the recent real estate boom in Germany. Investments into real estate developers are risky and have to be timed perfectly. As I am not an expert in this, I’ll “pass”.

262. Fleischerei-Bedarf Aktiengesellschaft von 1923

This is one of the oddest companies on German exchanges There seem to be only 1000 shares, “trading” at 10.000 EUR per share. There is little information available but the published numbers (profit of ~100k EUR) would not justify a 10 mn valuation. Maybe there is real estate. Not my kind of stock, “pass”.

263. MyHammer Holding AG

MyHammer was another one of the dotcom bubble”internet stocks”. MyHammer connecting craftsmen with customers over the internet. The 106 mn market company has a pretty interesting journey behind them as the stock chart shows:

The stock has performed well over the last years comingn from a low basis. The company is currently growing at ~30% p.a. but a valuation of 6x sales is clearly not a bargain anymore. However still a candidate to “watch”.

264. Advantag AG

1.4 mn Nanocap trying to ride the ESG wave. “Pass”.

265. HSBC Trinkaus & Burkhardt AG

HSBC Trinkaus is the stock listed German subsidiary of HSBC. The 1,6 bn EUR market cap stock has suffered significantly over the last few years:

The most recent drop was clearly driven by their profit going down -50% yoy in the first 6M 2019. With 2.4 bn in equity, the stock trades at 2/3 of book value but also ROEs don’t look good. “Pass”.

266. Dorstener Maschinenfabrik

Bankrupt zombie stock. Pass.

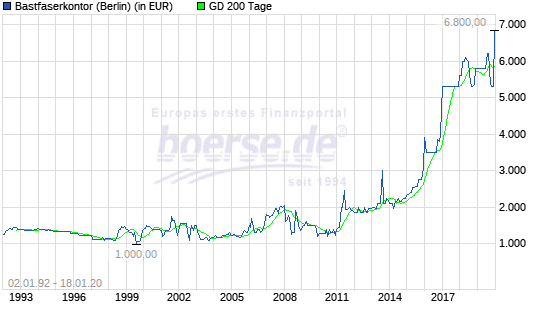

267. Bastfaserkontor AG

This is a thinly traded 56 mn EUR stock that I had never heard of despite being in existence for a long time. The stock chart shows an impressive gain over the past few years:

Again, htis seems to be one of the many Real Estate stories going on which excludes this from my area of interest. “Pass”.

268. Ahlers AG

Ahlers is a 33 mn market cap “men’s fashion” company that has always been “cheap” and would often show up in stock screeners. However the company went on a long decline path at it was clearly not able to cope with fundamental changes (online commerce, fast fashion etc.). In theory, the company has a lot of ingredients for success (family owned, family run, some decent brands) but in a fundamentally changing environment this is not enough, Maybe there is a “Last puff” in this share but for me it is a “pass”.

269. Palatiumm Real Estate

0.6 mn EUR nanocap. Pass.

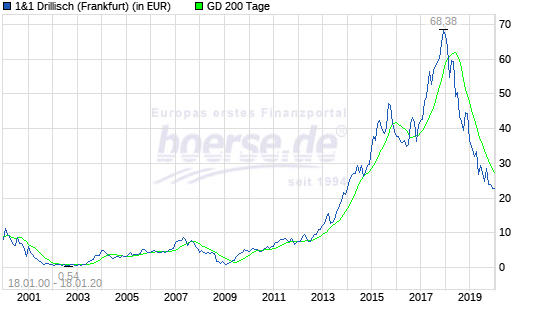

270. 1&1 Drillisch

1&1 Drillisch AG is a 75% subsidiary of United Internet. The 4 bn market cap company is a reseller of mobile phone and broadband interent access and has been quite successful in the past. The stock chart however could be described as a “Christmas Tree” chart:

The man reason for this chart are two issues: First, the business has been stagnating lately with more or flat revenues and slightly decreasing margins. Secondly, the company decided to bid for a 4th 5G license and won. The overall case for 1&1 Drillisch of course changes with this significantly. The company will need to spend billions in order to build this network with a very uncertain outcome. A mobile market with 4 networks is usually very competitive. The stock therefore is a lot more risky than it used to be. I will still “watch” it but with low priority.

271. X-FAB Silicon Foundries AG

X-FAB is a 617 mn market cap company that manufactures equipment for the semiconductor industry and has been IPOed in 2017 at a stock price of 8 EUR. Since then, the stock has lost ~-50%. It looks like a well timed IPO in the cyclical semiconductor business, as sales have been shrinking in 2019 more than .10% and the company started making significant losses. “pass”.

272. AS Creation AG

AS creation is a 51 mn EUR market cap wallpaper manufacturer that has actually once been part of the V&O portfolio but I sold it in 2014. Although the company seems to have recovered slightly after 2 (deeply) loss making years, sales and profits are still significantly lower than when I owned the shares which is the reason for the very disappointing stock performance:

The reasons for this are in my opinion mostly a failed attempt to enter the Russian market, a huge fine for anti-competition behavior and the hope that a structural decline in product attractiveness can be compensated with international expansion. On the positive side, they seemed to have been able to sell the Russian operation. For me, maybe for sentimental reasons, I will “watch” the stock.

273. SHF Communications Technologies

Tine struggling small cap that used Germany’s lax rules to delist in 2018. “Pass”.

274. CTS Eventim AG

CTS Eventim is a 5,5 bn market cap “multi-bagger” whose success is quite obvious when seen through the rear view mirror: When recorded music can be accessed anywhere from anyone through streaming, the value of “live” music increases as especially the artists have to concnetrate much more on tours to make the “real” money. CTS started out as a normal concert ticket selling shop but morphed successfully into one of the leading live event promotion agencies in Europe. The ticketing business still drives the profitability with EBIT margins of 30%, wheres the lower margin Live event business is growing more. The business as such also provides a decent “float” as people seem to be willing to pay for tickets long before the event.

The stock chart is really impressive:

As always these days, a lot of this is priced into the stock. At around 25 EV/EBIT, there is also a clear downside risk if things don’t turn out well at some point. SO for me the stock is a “Pass”.

275. Ganaria AG

Bankrupt “zombie stock”, former “Shopimore”. Pass.

Very interesting series – what about one about European software companies? There aren’t as many unfortunately though.

Another post within this great series 🙂

Regarding #251 ATOSS Software AG (Pass): it is also a clear pass for me, it seems very richly valued, currently. Sales a growing but from a low level, and I guess Software companies only deserve high multiples if and only if they are likely to reach high levels of dollar sales, because that is when high fixed costs like RnD are allocated to a broad base…

I very much prefer Check Point Software (CHKP US), much higher sales with much slower growth, hich profitability, high net cash (important to adjust multiples accordingly), high share buy backs. Read more about it here:

http://bit.ly/36j0rf9