All German Shares Part 17 (Nr. 326-350)

The next batch of 25 randomly selected German stocks.

In the last post, someone asked why I do not filter out certain stocks (Nanocaps etc.). I have thought of this, but decided against it. The main reason is that some of these “Zombie’s” have really interesting stories that might contain important lessons. Plus there is a VERY small chance that a real gem is hiding somewhere, although I haven’t found one yet.

This time, I only put 3 stocks on my watch list, but some of the “passed” stocks have really interesting stories.

326. United Labels AG

United Labels is another child and survivor of the Dotcom boom. The 8.7 mn market cap company is active in licensing brands to producers of everyday articles like T-Shirts etc. Top line is however shrinking since a few years and this year they had to put their Spanish subsidiary into insolvency. “pass”.

327. Bavaria Venture Capital & Trade AG

0.8 mn market cap investment company. Little information and despite the name the company seems to be located far away from Bavaria in Essen. “pass”.

328. Deutsche Lufthansa AG

At the time of writing, Lufthansa just gt hit by the news of the Corona Virus. The 6.5 bn market cap company looks cheap from a trailing P/E perspective, but under the hood there are a lot of issues. Perosnally I would call Lufthanse more a flying pension plan than an airline. Maybe interesting for investors who can time cycles. As I can’t, I’ll pass.

329. SCI AG

SCI is a 9,5 mn EUR investment company. The company specializes on “special situations”, mainly squeeze outs etc. For anyone interested in this area, follwoing the company is recommended. Historic track record is OK, although they have soem controversial bets going on (IFA Hotel). “Watch”

330. Deutsche Wohnen AG

One of the Real Estate high flyers of the past few years with a 13,7 bn market cap. Residential property only with a focus on Berlin, might be hit most by the cap on rents. Anyway, not my circle of competence, “pass”.

331. Osram SE

Readers of my blog know that I “played” Osram as a special situation in 2019, made some money but got out to early. After being majority acquired by Austrian AMS, I do have little insight into the combined business and also don’t find it fundementally attraxctive, therefore “pass”.

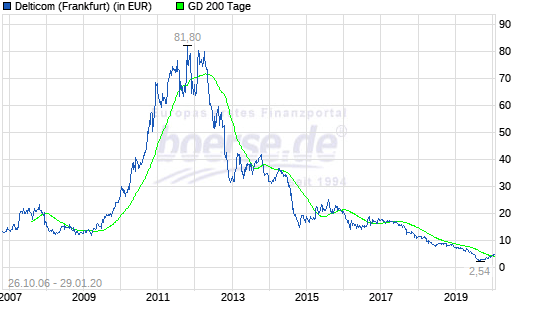

332. Delticom AG

At first sight, Delticom looked like a great company. One of the early E-Commeerce pioneers, the company quickly gained market share in online tire sales and became one of the dominating players. Helped by a regulation change, the stock price went up to 80 EUR per share in 2012, making the company an “almost unicorn”, still majority owned and run by the founders:

However since then, the company rapidly deteriorated, actually turning a loss in 2018. What happened ? In this case it was not Amazon, but a combination of bad management and bad economics. The company overpaid for a “built to sell “competitor called “Tirendo” in 2013. Then, they found out that acquiring customers on the web becomes more and more expensive, especially if customers only return every few years. they also might have underestimated the marekt power of the big suppliers.

Finally, the founders made very strange moves and decided that Food Delivery fits perfectly to their tire business. 2018 and 2019 they increased debt significantly while business deteriorated which is a toxic combination. They managed to renegotiate debt but were forced to focus on the tire business (surprise…). The remaining founder got kicked out of the supervisory board a few days ago. Delticom is a good lesson taht not every founder owned/led business wil do long over the long term.

Despite rumours on a sale of the company, I’ll pass.

333. Metro AG

Metro, the 4.6 bn “cash and Carry” food chain is a stock that I don’t have very fond memories. I invested into it as a “spin-off” opportunity but found out the hard way that both parts of the initial Metro (Metro, Ceconomy) were not good business.

Since then, not a lot has changed and I’ll gladly “pass” on Metro.

334. Teleservice Holding AG

0.6 mn Nano cap with no information. “pass”.

335. Gold-Zack AG

Once a star of the “neuer Markt”, now a 0.16 mn insolvent shell company. “Pass”

336. Hoftex AG

Hoftex is a low profile, 62 mn market cap textile company. The company has been transitioning slowly from more genral textiles, where no money can be made to a specialist textile company that is supplying the car industry. This worked well for some time, but with the weakness in the car industry, Hoftex also suffered:

In September, the company issued a profit warning. As the business is quite capital intensive, I’ll pass.

337. elexxion AG

2.9 mn market cap “hI tech” company with a cool name but only 400K of sales and 500K of losses. Pass.

338. Klöckner & Co SE

Klöckner is a 580 mn market cap steel trading company which stock has been stagnating now for over 10 years:

For Deep Value investors the stock might be interesting (less then 0,5 Price/Book), but the business is volatile and in the first 9 months 2019 they have shown a loss. They try to play the “digital” theme but honestly I don’t see them making more money “digitally”. Pass.

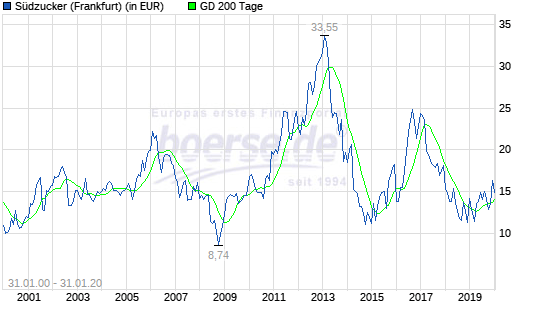

339. Südzucker AG

Südzucker is the 3 bn market cap European leader in refining sugar plus prodcuing some (sugary) ingredients for the food industry. Looking at the chart of Südzucker we can see that they also failed to create any long term value for shareholders despite the occassional spike over the last 20 years:

In general, sugar in the western world is clearly in decline due to the negative health effects. The company has significant debt, a large pension liability and is therefore a “Pass”-.

340. MAX Automation AG

MAX Automation is a 133 mn EUR market cap machinery company. The company is currently making significant losses, which they claim is not a problem as they put all the negative stuff into “discontinued operations”. In order to survive, they have to increase debt dramatically. “pass”.

341. DG-Gruppe AG

DG-Gruppe AG is a 16 mn market cap company with an in principle interesting business (company sponsored pension plans) but little information available and ambitious valuation (8xsales, only 10% growth). “Pass”

342. Alexanderwerke AG

Alexanderwerke AG is a 31 mn EUR market cap company that originally mainly produced meat grinders. The company for a long time was always close to insolvency until it was revived somehow a few years ago. Although current profitability looks ok, order entry dropepd significantly which shows the underlying volatility of the business. “Pass”.

343. Volkswagen AG

The largest German car company with an 82 bn market cap. Not only because of the Deisel scandal, I consider the company as badly managed and governed. The company is not necessarily run to the benefit of the shareholders. The structural changes in the car industry create significant risk for the incumbents. The local Government has a share in the company and can block any take over attempt. “pass”.

344. GEA Group AG

GEO Group is a 5 bn market cap diversified technology company. Once the pride of the Germany industry, the company has been struggling for some time. That might have attracted some activist investors, among them Paul Singer’s Elliott. The company has exchanged management and restructured, however results are still weakening. Nevertheless a “watch” for me but not with high priority.

345. Umweltbank AG

Another company that I didn’t here of before. Umweltbank is a direct bank, attracting deposits by promising only to lend to ecologically responsible projects. The bank is valued at 370 mn EUR. Especially in the first &M 2019, the bank was growing strongly. With around 120 mn in equity, this is an ambitious valuation, although their 16 mn in 2018 profit shows that ROE is much better than with the traditional banks. Nevertheless a “pass” due to the high valuation.

346. DEAG AG

DEAG is another former high flying “Neuer Markt” Stock that had a hard decade. The liev concert organizer company has now a market cap of 117 mn. Business has not be running that well in the first 9M of 2019, nevertheless the stock has gone up significantly in the last few months:

Thsi seems to be driven by insider buys. However I have no clue about the business, so I’ll “Pass”.

347. Hanse Yachts AG

Hanse Yachts is a 75 mn EUR sports- and sailing bpat manufacturer. Hanse Yacht has a colorfull past, haveing been IPOed in 2007, taken private by listed P/E company Aurelius in 2011 and the IPOed again in 2018. The company is not very profitable and according to the annual report, Aurelius is sucking out money via consulting arrangements. Plus, 30 mn debt for a company with 5 mn EBITDA is too much. “pass”.

348. Mountain Alliance AG

A 35 mn listed VC vehicle that I have never heard of before. It is majority owned by VC investor Mountain Partners which has a mixed reputation. It also seem to play the role of an Exit vehicle for the Mountain Partners incubator. The portfolio as such looks to a large extent like a “spray and pray” approach. The stock trades around -20% below NAV which looks like a justified discount. “Pass”.

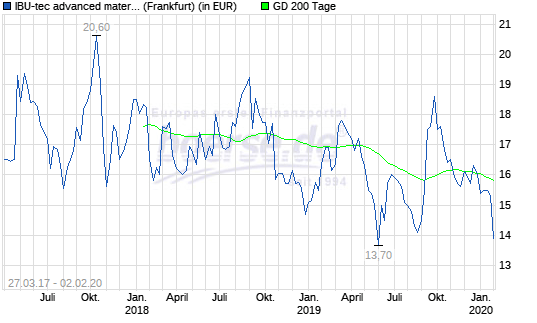

349. IBU-tec advanced materials AG

Another company that I never heard of before. IBU-tec, with a 56 mn EUR market cap seems to specialize in some kind of specialty chemical treatments. IBU-Tec went public in 2017, however the stock price since then mostly went south:

In the first 6M 2019, the company showed good growth but very thin margins. On the other hand, Management (CEO) holds significant equity. I’ll put IBU-Tec on “watch”.

350. DVS Technology AG

DVS Technology (es Diskuswerke) is a 158 mn market cap machinery group, producing specialy machinery under various brand names. As many autombile related companies, DVS saw rapidly deteriorating margins in the first 6M 2019. Although still profitable, the resulting profit has now relation to its market cap. The compnny also carries significant bank debt. “pass”.