All German Shares Part 18 (Nr. 351-375)

So back to the “new normal” with another episode of my German Stock series. Most of these summaries have been written before the crisis hit, so I just added a few comments here and there and updated the numbers.

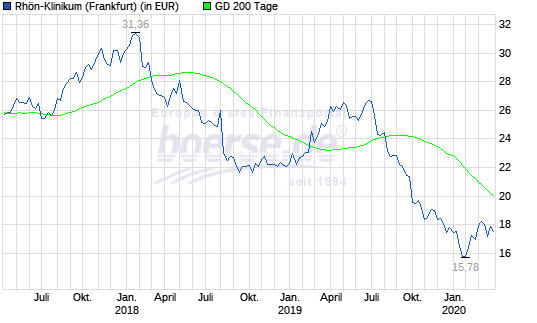

351. Rhoen Klinikum AG

Rhoen Klinikum is a 1.1 bn 1.2 bn EUR market cap company owns and runs a series of clinics in Germany. I used to own the shares some time ago but more like a “special situation” investment. The company was target of a take-over battle some years ago and sold a large part of its clinics to a competitor and kept the more difficult ones. The stock did quite well for some time but the started to decline with no end in sight:

In 2019, profit went down somewhat but it is still nor real explanation for a more than -50% drop from the 2018 peak. As a previous position, I will put Rhoen on “watch”.

Update: Just before the crisis hit, the founder Eugen Münch teamed up with former arch enemy Asklepios and “allowed” them to go for a majority stake. The resulting share transfer triggered a voluntary offer to all shareholders at 18 EUR/share.

352. RIM AG

RIM AG (ex Rücker Immobilien AG) is a 6 mn market cap company owning some real estate. The company is “dark”, issuing no financial statements. “Pass”.

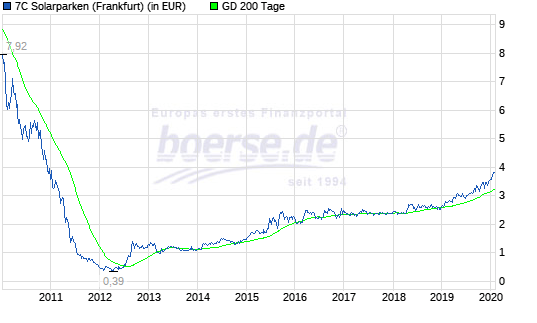

353. 7C Solarparken AG

A 233 196 mn EUR market cap company that buys and runs solar parks. Looking at the stock chart we can see that the stock developed very nicely over the last years since the low in 2012:

As most of theses players, 7C uses significant debt to buy the solar farms but the investors don’t seem to have an issue as solar parks are deemed “safe” assets. Personally, I don’t see solar parks in Germany as an economic vialble business in the long term, but as long the subsidiaries are flowing people will build this parks. For me it is a “pass”.

354. GUB Investment Trust

Another listed VC vehicle with a ~12 mn market cap. At first sight, the stock looks significantly undervalued. The biggest asset is a 6% stake in listed Nexus AG which alone is worth more than 30 mn EUR. However, the history of the company is not great, and the CEO seems to be a “colorful” character. There are better opportunities out ther. “Pass”.

355. Porsche Holding SE

Porsche Holding, a 20 11.3 bn market cap stock, actually has nothing to do with the actual Porsche cars but is now a holding company, holding Volkswagen shares on behalf of the Porsche family as a result of the failed take over attempt in 2007/2008. I have written in the blog about Porsche several times and although a few years have gone by, nothing has changed. As I don’t want to own Volkswagen, there is no sense in woning the Porsche shares, independent of any discount (although I haven’t checked how much that might be). “Pass”.

356. Neschen AG

Insolvent 0.1 mn market cap zombie stock. “pass”.

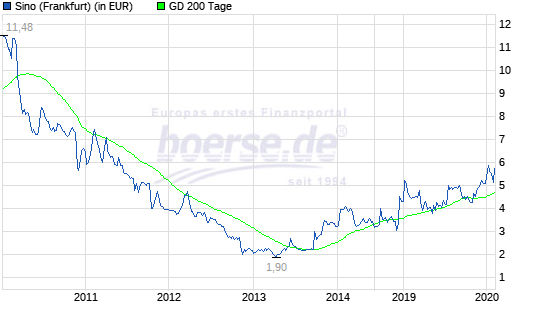

357. Sino AG

Sino AG is a 13.4 15.7 mn market cap “High end” brokerage company that caters to “High end” brokerage clients, i.e. heavy traders. Sino owns 25% of listed “Tick Trading AG” as well as 30% of unlisted “no fee” broker Trade Republic, the German version of Robin Hood. Sino’s core business however doesn’t look that good. The recent increase in the stock price then might have to do with the positive development at Trade Republic:

Anyway, Sino is for me a stock to “watch”.

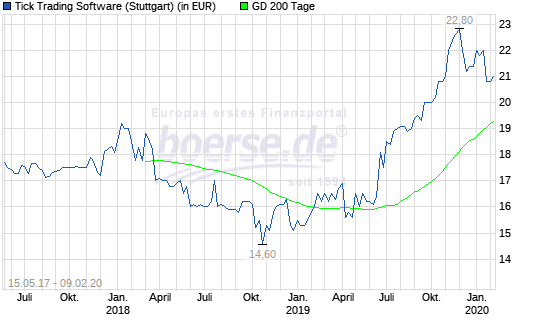

358. Tick Trading Software AG

Tick Trading is a 21 18 mn EUR market cap software company that sells trading software to large institutional clients (banks etc.). The company seems to be quite successful, their latest results look good. Topline +10%, EBIT plus 20%. With a P/E of around 16, the company doesn’t look that expensive, despite a nice run up of the stock price:

The company distributes 100% of its profits which at the time of writing represents a dividend yield of around 8%. Tick Trading Software is definitely a stock to “watch”.

359. Adler Real Estate AG

Adler Real Estate is a 869 597 mn EUR real estate company owning a portfolio of residential real estate. Adler is currently subject to a take-over attempt by ADO properties SA, a Luxembourg based property company. It seems to be an all share offer. As I have mentioned several times, real etsate companies are currently not interesting for me, so “pass”.

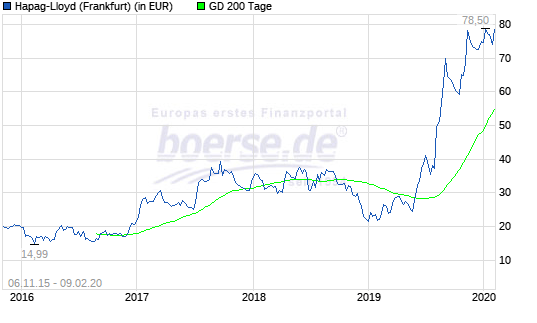

360. Hapag Lloyd AG

Hapag Lloyd is a 13,7 11.8 bn EUR market cap transportation and logistics group. The stock price has more than trippled in 2019 as the chart shows:

Looking at some analyst reports, no one seems to know why this happened. There are speculations that somehow the large shareholders fight each other over available shares. For me it’s a “Pass”.

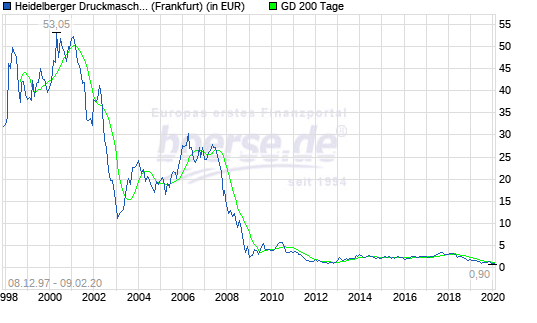

361. Heidelberger Druckmaschinen AG

Heidelberger Druckmaschinen is a 276 173 mn EUR market cap company that used to be one of Germany’s finest “tech” companies when printing was still relevant. A global market leader with exceptional technical capabilities. Unfortunately, print became less important and Heidelberger failed to adapt. The long term chart shows the long term decline:

The company is still burning money, increasing debt and share count and at first sight there is no “silver lining” anywhere. The company still shows “restructuring cost” as one-time item despite restructuring now for more than 10 years. the only surprise for me is that they haven’t filed bankruptcy yet. “Pass”.

362. HMS Bergbau AG

HMS is a 100 98 mn market cap commodity trading company, trading commodities like coal and iron ore. Looking at their numbers, I do npt see how a 100 mn market cap can be justified with a run rate of 1.5 mn EBITDA and 10 mn equity. “pass”.

363. Francotyp Postalia

Francotyp is a 59 45 mn EUR market cap stock that was long a “darling” of value investors as the stock always looked cheap. The problem was however, that the core business was facing structural headwinds, as their machines for managing physical post (letter) was clearly in terminal decline. The company tries to reinvent itself somehow to a “internet of Things” player. However the growth in the new segment does not yet compansate for the decline in the core business. Francotyp turned to a loss in 2018. 2019 so far looks okayish, still declining top line overall but good growth in the new segments. If they manage the transition, the stock would be interesting, but there is significant risk involved. In the meantime, Rolf Elgeti has become the largest shareholders which means for me: “pass”.

364. Blue Cap AG

Blue Cap is one of many “listed PE” companies with a market cap of 53 54 mn EUR. Their numbers are hard to read and I do not see a real strategy in their portfolio. “pass”.

365. Fast Finance24 AG

A company that has changed its name several times in the last few years and is now a “Fintech”. Market cap 3,8 3,4 mn EUR, “pass”.

366. Agrob AG

Agrob is a 115 mn commrrcial real estate company that I had written about as a “special situation”. Agrob owns basically one big commercial real estate park near Munich with mostly media companies as tenants. The company for a long time was a subsidiary of Hypovereinsbank (now Unicredit) until they dicided to sell their majority stake last year to a PE company at 32 EUR/share. At the current price of <30 EUR per share, the stock is interesting again. “Watch”.

367. Xin Rui Ke AG

Some kind of Chines company with several name chances. For some reason 61 mn EUR market cap. “Pass”.

368. Landshuter Kunstmühle AG

23 mn EUR market cap company grain mill that rarely trades and doesn’t issue reports. “Pass”.

369. Q-Soft Verwaltungs AG

A 3,5 mn market cap company with little useful reporting. Pass.

370. Dt. Balaton AG

A 191 mn EUR holding company that has collected a pretty wild mixture of assets. Based on teh mixed reputation of the management (i.e. making really stupid investments into fraudulent German-China companies), I’ll happily “pass”.

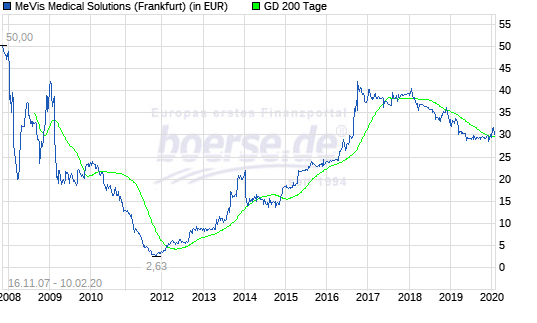

371. MeVis Medical Solutions AG

MeVis is a 57 49 mn EUR market cap software/technology company that offers solution for image based medical diagnosis. The company is highly profitable (EBIT margins of 43% 9M 2019, however the top line is not growing much. The stock price has been a pretty rough roller coaster ride, indicating that the underlying business is maybe not too stable:

Nevertheless, the stock looks quite cheap compared to profitability so it is a clear “watch” candidate.

372. Lena Beteiligungs AG

0.2 mn EUR nanocap. “pass”.

373. Smart Grids AG

0.06 mn EUR nano cap with frequent name changes. “pass”.

374. Vtion Wireless AG

0,85 mn market cap German-Chinese fraud. “Pass”

375. Pilkington Deutschland AG

1.1. bn market cap Glas product producer (for construction and car industry). Stock is thinly traded and has a P&L transfer agreement with the main shareholder, so little or no upside for shareholders which explains that the stock price hasn’t done anything for a long time. Fundamentally the business is not in good shape either (declining top line, strongly declining profits). “Pass”.

Wow, Sino AG indeed is/was an interesting candidate to watch…

https://www.dgap.de/dgap/News/corporate/sino-high-end-brokerage-trade-republic-schliesst-eine-millionen-series-runde-angefuehrt-von-accel-und-founders-fund-ab/?newsID=1316869

I should have watched less and bought some….

Uh? and Marcelinum, can you pleases discuss the investment ideas? I am not interested in your „psychological“ analysis.

Thank you

@Uh?: please ignore Bon’s comment.

Btw, seems as only Mevis Medical Solutions is the only company potentially worth our time, based on reasonably high margins etc. Yet, it’s small, and I would prefer better options.

Sino and Tick seem interesting to me, added to my long-term to do list…

When lloking where to start an ETF savings plan, I finally decided to go with Trade Republic, since others seemed to expensive for me. The app (trade Republic) works very well!, currently with very limited functionalities though…

A german blogger wrote an article about Tick Trading Software

https://www.preis-und-wert.com/tick-trading-software-zu-guenstig-um-wahr-zu-sein/

Insider selling is in contrast to positive business development.

Good morning Chris. Thank you very much for your comment. Know this website.

“There are many reasons for insider selling, but there is only one reasons for buying”

(much truth in it I believe. Some buying might be mandatory, though)

Best, s4v

Kapitalerhöhung: https://www.boersen-zeitung.de/index.php?l=5&isin=&dpasubm=all&ansicht=meldungen&dpaid=1274825

Check out Intertrust (Dutch company, but next to Germany!): very cash-generative trust and corporate services firm that trades on an 14% 2020 free cash flow yield. Revenues are 80-85% recurring. There is an operating profit margin inflection point in 2020/21 that should lead to a re-rating of the stock. They bought a US fund administrator in 2019 and are in the integration process. 90% of total run-rate synergies of USD22 million are expected to be reached by 2021 and 20% by 2020. The synergies are mostly coming from labour arbitrage, that is offshoring, and are tangible.

Thanks. Will look at it.

Love it – was just looking at privately held Continental Transfer & Trust and was bugged by the fact that they are private….. very defensive business line.

So the value of this blog lays in the readership it seems….thanks for moderating.

Thank you for the compliment. So I guess I should stop posting then.

I would certainly invite ideas from others on top of your much appreciated contributions. Shifting away from a 1 guy’s narrative to a collective, MMI to We Us and I.

Well, the purpose of this blog is to function as my diary which is open for anyone to read and comment. I am clearly open to post constructive ideas of any reader, but I think there are a lot of forums that already serve that purpose.

Changing an over-egocentric character? Mission Impossible !!!!

The compliments start getting better and better. Thanks for the motivational boost.

“an over-egocentric character” That’s too much. i would not go there.

Now keep sharing please. But reviewing ideas like Majestic and Silver Chef and the associated comments highlights the value of the collective.

I strongly believe that echo-chambering works against you. You may want to explore a way of harnessing the power of your readership to your own (and the collective’s) advantage.

“I strongly believe that echo-chambering works against you. You may want to explore a way of harnessing the power of your readership to your own (and the collective’s) advantage.”

That’s exactly what I try to achiev now for 9+ years. For “echo-chambering” I would just turn off the comments or not blogging at all.

This is a blog, you know?

Some of the comments are valueable, no doubt.

If I wanted some random strangers opinion on random stonks, I would check out some random forum.

There is a reason why I prefer to read mmi’s take on things he finds interesting.

Fair enough.

I am told there is a forum out there that stands out: you have to submit an interesting idea (write up) to be admitted. Can you think of what it’s called?

Thanks again Marten

Click to access NL%20OEIC%20March%202020%20_1.pdf

Marten, Intertrust indeed looks kind of interestign,. although the debt load is high and the price they paid for the acquistion is really rich.It is definitely worth to watch though.